VNO - Orion Office REIT: Not Cheap Enough

2023-05-01 15:45:48 ET

Summary

- ONL is an office REIT situated in 10 different states in the US.

- Quarter of their leases are going to expire in 2024 making 1.5-1.9 million square feet vacant.

- They have $175 million of debt due this year which might be difficult to refinance.

Investment Thesis

Orion Office REIT ( ONL ) is likely to experience trouble in the next few years because of high lease expiration in 2024 and a lot of debt due in 2023 that is going to have to be refinanced. On top of that, it is not well positioned towards its peers and should be cheaper.

Overview

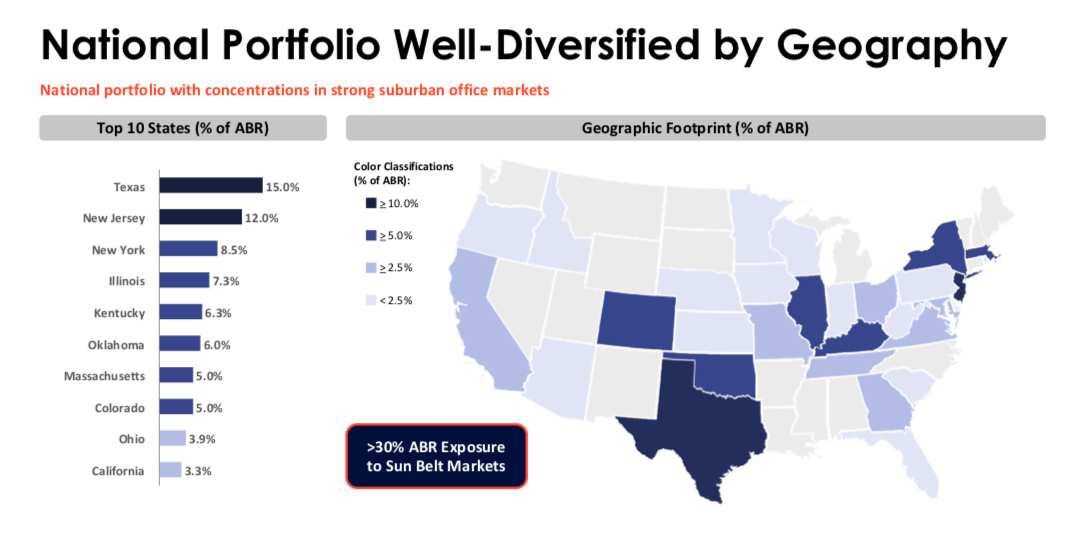

Orion Office REIT has a portfolio of offices distributed across the US. The two states with most of the properties from their portfolio are Texas (15%) and New Jersey (12%). As such the REIT seems to lack a clear geographical focus which can be a negative given its relatively small size. I’d much rather see them focus on one market. While their exposure to the currently unpopular California is only 3.3%, their New York market exposure (New Jersey + New York) represents almost a quarter of their ABR. Overall I’m not a big fan of their total geographical allocation, despite Texas having the highest exposure.

Orion Office REIT Investor Presentation

{kind=link}

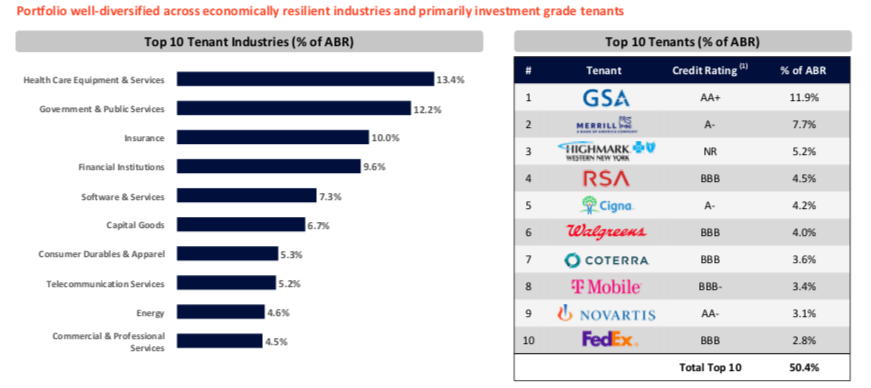

ONL provided their top 10 tenants in their investor presentation leading with health care equipment and services (13.4%), government and public services (12.2%), and insurance (10%). Their biggest tenant ((GSA)) accounts for almost 12% of the ABR, while the top 10 tenants account for over half of all revenues. This makes the REIT quite risky as a single tenant struggling to pay rent can have a major negative impact on the company.

Orion Office REIT Investor Presentation

{kind=link}

The REIT owns 81 wholly-owned properties with 89% occupancy and 4.1 years as the weighted average of remaining lease. That’s a very low WAULT (weighted average unexpired lease term) for an office REIT. What’s even worse is that in 2023 15.1% of leases are going to expire and this is going to be even higher in 2024 with lease expiration being at 25.1%. That means they will have to find tenants for 1.5-1.9 Million square feet of space each year. All of this at a time when office leasing is at an all time low (as confirmed by total 2022 leasing of 800 ths. Sft), many people are working from home and companies trying to cut costs in expectation of a potential recession. This put the company under immense pressure to either renew some of the leases or to find new tenants.

In their earnings release, the company states that they see lease maturities as a value creation opportunity for the coming years but from their current behavior it does not seem like it. Their strategy seems to be focused on selling properties rather than renewing leases or finding new tenants. In 2022 they sold over 1.3 million square feet for around $43 million and had an agreement to sell 7 additional properties just during the last quarter of 2022. On the other hand, they entered into lease renewals for a little over 1 million square feet across 10 different properties throughout the whole year some of which are for a 10 year WAULT. This is good but I don't think it is going to be good enough in the future. The 2024 lease expirations are unlike anything they had to deal with so far and I am not sure if they are going to be able to cope considering that they cannot just continue to sell all of their properties at this speed and need to start finding more tenants. So with a quarter of space becoming vacant next year, I don’t think the company will be able to deliver.

Orion Office REIT Investor Presentation

Financials

ONL has a core FFO of $101.8 million and a core FFO per share of $1.80. According to the guidance provided in the firm's supplemental the core FFO per share is supposed to drop during 2023 and be between $1.55 and $1.63. This is based on the assumptions of administrative expense rising by $1 million to $19.75 million and net debt/EBITDA rising from the current 4.3x to 5.3x and significantly negative net absorption as lease expirations exceed renewals and new leases.

Their balance sheet presents another problem. Their debt currently stands at $557.3 million with a weighted average interest rate of 4.42%. That’s not unreasonable, however, $175 million of debt is due in 2023. That’s a lot for a company with an FFO of about $100 Million and only about $20 Million in cash. I expect the company to have a relatively difficult time refinancing this as regional banks seem to be quite hesitant towards financing commercial real estate at the moment and even if they do manage to miraculously refinance the debt, it will be at a significantly higher interest rate than what they’re paying currently.

Orion Office REIT Investor Presentation

{kind=link}

Valuation

It should come as no surprise that the company is cheap, however, I do not think it’s cheap enough. Trading at a P/FFO of 3.8x, the company trades nicely below its historical average of 6.06x (as should be expected), but cannot be considered cheap relative to peers. Take Brandywine Realty Trust ( BDN ) for example – a healthy REIT, which is much better diversified in terms of tenants, has high exposure to WFH resistant life sciences and has no debt maturities over the next two years. Still, it trades at just 3.1x FFO suggesting that ONL has a lot further to fall. Other peers like SLG (3.78x) or VNO (4.87x) are both larger firms with a big part of their portfolio in New York, similar to Orion. They are also trading at similar multiples. This once again suggests that ONL could be cheaper based on its much smaller size. And if they do not deal with the maturities, as is expected, they will inevitably fall.

The share currently stands at $6.42 with a dividend of just $0.1 per share per quarter and the dividend yield is 6.23%. The payout ratio is 22% so the dividend is unlikely to get cut, but can hardly be considered as attractive given the overall outlook for the company. A dividend discount model with zero forward growth and a 10% discount rate would suggest a fair price of $4 per share. Of course, shorting at these valuation levels is quite dangerous, but I definitely don’t see the company as a buy here leading me to a hold rating.

Conclusion

Overall, the REIT is likely to struggle in the near future and is going to be under a lot of pressure to rent out their spaces and pay off their debt. Considering that their peers are trading at similar multiples but they have a better diversified portfolio and no debt maturities, ONL is overvalued right now and will probably fall. All of this leads me to a HOLD rating at this moment.

For further details see:

Orion Office REIT: Not Cheap Enough