OEC - Orion S.A.: Automotive Coatings And EVs Demand Could Trigger Price Action

2023-12-25 01:57:52 ET

Summary

- Orion S.A. recently delivered strong FCF growth and has potential for further growth driven by megatrend drivers like EV vehicles and demand for batteries.

- The company is using cash flows to buy back shares and lower its debt levels, indicating good financial management.

- The recent increase in R&D spending suggests the development of new products and potential net sales growth.

Orion S.A. ( OEC ) recently delivered beneficial FCF expectations driven by lower capital expenditures and megatrend drivers like new EV vehicles or demand for batteries. OEC also looks like a buy as management continues to use cash flows to buy back shares and lower its debt levels. Besides, the recent increase in quarterly R&D could indicate an acceleration in the development of new products. There are obvious risks from volatility in the price of certain raw materials, lower demand than expected, or higher capex than expected. With that, I would say that OEC appears significantly undervalued.

Orion

It is a public limited company incorporated in 2014 with executive offices located in Texas, United States. It is a global manufacturer of products based on carbon black, which is a form of powdered carbon with properties that allow the creation of materials with specific electrical and optical physical characteristics.

The company is one of the world's largest producers of rubber carbon black, primarily needed for tire manufacturing. It operates 14 wholly owned facilities across Europe, North America, South America, South Africa, and Asia along with a jointly owned German plant. In addition to the headquarters and offices in Texas, the company also has offices in Frankfurt, Shanghai, Seoul, and Tokyo among other locations.

It is organized into two reportable segments: Special Carbon Black and Rubber Carbon Black. The first segment focuses on the specialty production of carbon black for specific uses based on customer needs. Given the malleability of carbon black, it allows the manufacture of products with different performance characteristics for a wide variety of applications. This material is used for the production of polymers, batteries, printing inks, and other pigments besides making coatings.

Regarding the second segment, rubber carbon black products are used in tires and mechanical rubber products intended for construction, automobile production, certain food applications, consumption, and medical. Rubber carbon black is used to improve the physical properties of systems and applications in which they are incorporated, such as durability, physical or fluid resistance, friction reduction, etc. The company produces standardized grades of this material as well as advanced design grades for specific uses.

The supply of raw materials necessary for production is largely covered by short and long-term contracts with a variety of suppliers. Demand in the Western European and North American regions is mainly driven by road transport activity, strict tire regulation standards, and relatively stable tire replacement demand. Demand in developing markets such as China, Southeast Asia, South America, and Eastern Europe is primarily driven by rapid industrialization, infrastructure spending, and rising car ownership trends.

With that about the business model, I believe that it is a great moment to have a look at Orion considering its recent quarterly earnings release. EPS GAAP was larger than expected, close to $0.44 per share. Quarterly revenue stood at close to $446 million.

Source: SA

Expectations from other analysts are also worth having a look at. After some years of small FCF and EPS, Orion is expected to deliver net sales growth, operating margin growth, EPS growth, and positive FCF in 2023, 2024, and 2025. With these initial details in mind, I tried to assess the fair valuation of Orion and executed my own DCF model.

Source: Market Screener

Balance Sheet: Total Amount Of Debt Declined Recently

The balance sheet includes a significant amount of accounts payable and inventory. The accounts payable are rather small. Hence, Orion uses some debt to finance its working capital needs and the total amount of property and equipment. I do not think that the total amount of debt is significant, but investors may want to carefully follow the net debt/EBITDA levels. In this regard, I do appreciate that total debt declined in the most recent quarter.

In particular, as of September 30, 2023, the company reported cash and cash equivalents worth $59.1 million, accounts receivable close to $267.3 million, inventories of $276.9 million, and prepaid expenses and other current assets worth $68.5 million. Total current assets stand at about $680.7 million, and the current ratio is larger than 1x, so I do not see liquidity issues out there.

With property, plant, and equipment of about $845.5 million, right-of-use assets close to $110.3 million, and goodwill of $72.9 million, total non-current assets are equal to $1153 million. The asset/liability ratio is larger than 2x.

Source: 10-Q

Orion included accounts payable of about $170.9 million, with the current portion of long-term debt and other financial liabilities worth $149.1 million. Additionally, with employee benefit plan obligations of about $50.9 million, total non-current liabilities stand at about $901.5 million.

Source: 10-Q

Debt Assessment, And Cost Of Capital

I studied a bit about the debt obligations signed by Orion. The company reported agreements linked to the LIBOR plus a margin of 2.50% or close to it. With this in mind, investors may have to keep in mind that changes in the EUR/USD rate could affect the company’s interest expenses. With all this in mind, I assumed a cost of capital between 3% and 7%, which appears conservative.

The Term-Loan facility was allocated to one term loan facility denominated in U.S. dollars of $300 million and another denominated in Euros of €300 million with both having a maturity date of September 24, 2028. Interest is calculated based on three months EURIBOR (for the Euro-denominated loan) plus a margin of 2.50%, or three-month USD-LIBOR (for the USD-denominated loan) plus a margin of 2.25%. Source: 10-k

Recent Increase In R&D Will Most Likely Lead To New Products And Net Sales Growth

Carbon black-based products have high versatility, which creates significant opportunities for process and product innovation. Orion maintains research and development practices that aim to recognize these opportunities to introduce its specialty carbon black products into new application niches. The firm's innovation group is divided between the application technologies team, which seeks to develop products and expand the range of applications, and the process development team, which works together with the firm's productive teams to optimize the processes of manufacturing.

The company believes that it maintains a competitive advantage in terms of the development and management of its intellectual property and has patents on many of its products and processes.

Considering the recent increase in research and development costs, I believe that we could be expecting an increase in the number of new products. As a result, in my view, net sales growth may increase.

Source: 10-Q

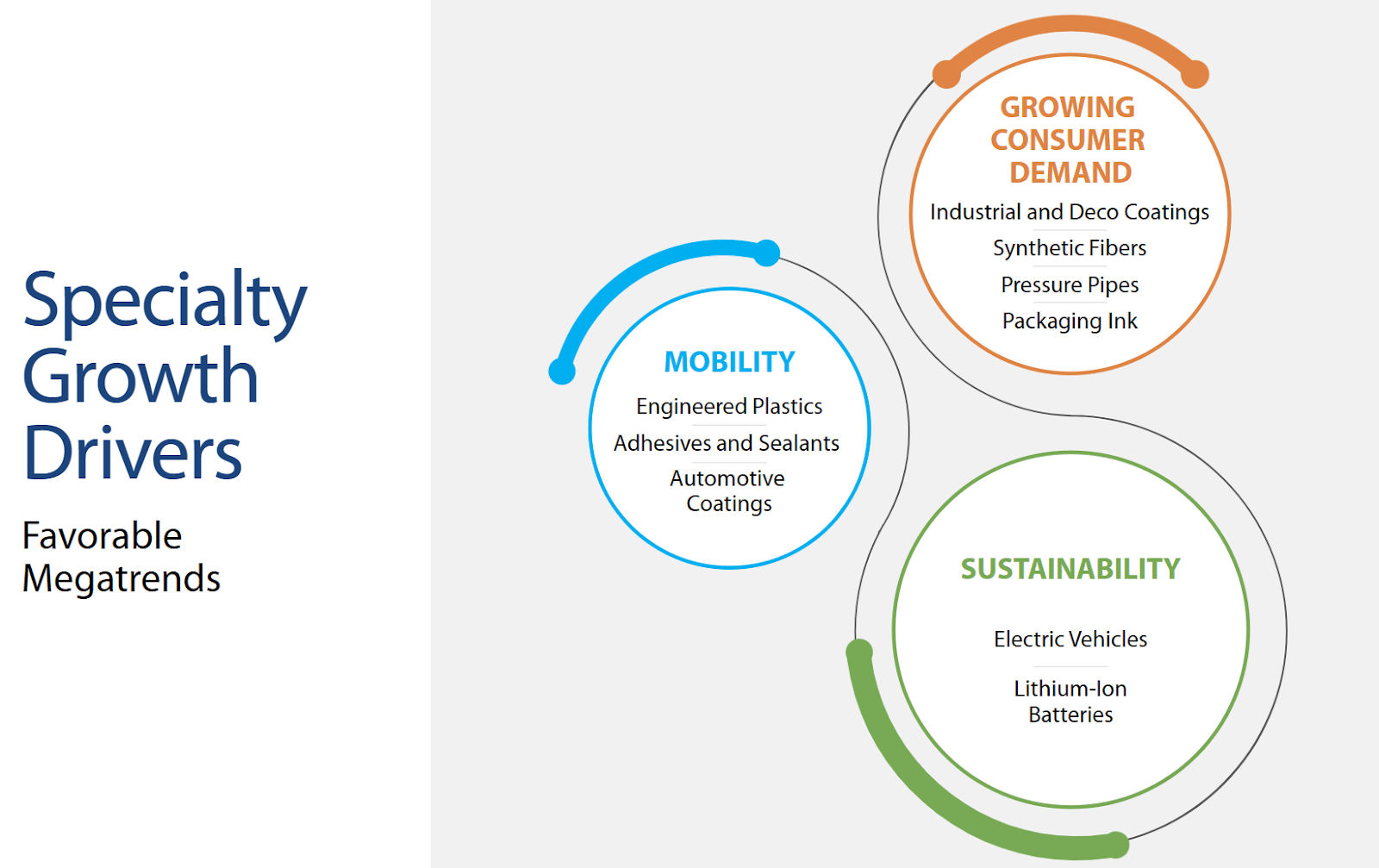

There Is A Significant Number Of Growth Drivers That May Bring Business Growth

There is also a significant number of growth drivers that could bring a lot of business growth. Among the megatrends noted there is the mobility revolution that includes automotive coatings, engineered plastics, electric vehicles, and demand for synthetic fibers and lithium-ion batteries.

{kind=link}

Demand for batteries is expected to grow at close to 15% CAGR from 2021 to 2026, but the company also noted that demand for coatings could grow at close to 6% CAGR. With this in mind, I believe that Orion could enjoy net sales growth in line with these growing markets served.

Source: Investment Presentation

Lower Capital Spending Announced For 2023, 2024, And 2025 Could Lead To Further FCF Generation

I also believe that we could see significant improvements in FCF in the coming years as Orion lowered its capital expenditure expectations. In 2023, 2024, and 2025, capex is expected to be close to $200 million, $33 million less than that in 2022. I did include some of these assumptions in my cash flow expectations.

Source: Investment Presentation

New CFO May Be Used To Lower The Total Amount Of Debt And For Stock Repurchases

The CFO was used to lower the total amount of debt as well as to finance stock repurchases. With these precedent transactions, I believe that we could expect new stock repurchases or a lower net debt/EBITDA ratio. As a result, I believe that we could see improvements in the stock price.

Net cash used in financing activities during the nine months ended September 30, 2023, amounted to $164.9 million. These outflows primarily consisted of $88.7 million related to the reduction of other short-term debt, $58.9 million for repurchase of common stock under the Stock Repurchase Program and $23.7 million, net related to repayment of our ancillary credit facilities. Source: 10-Q

Guidance, My FCF Expectations And Valuation

Orion offered impressive FCF expectations for 2023-2025. In a recent presentation, I could read beneficial FCF expectations. In 2023, Orion is expected to deliver EBITDA of $330-$340 million, with discretionary cash flow close to $170-$190 million, and FCF of about $90-$125 million. I took into account these expectations in my cash flow statement.

Source: Investment Presentation

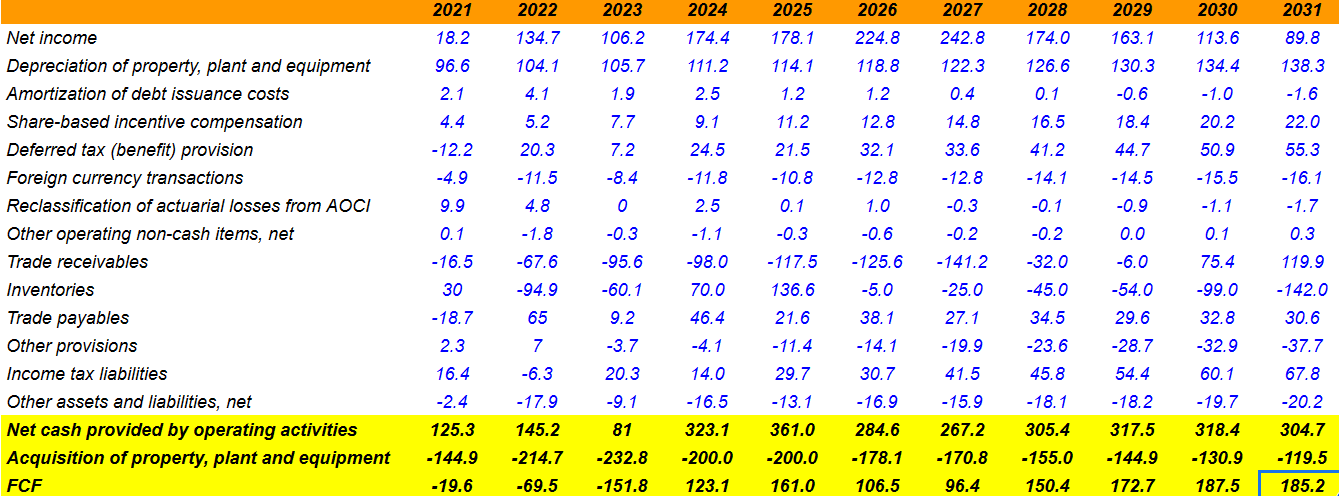

My expectations for the future include 2031 net income of close to $89 million, depreciation of property, plant, and equipment worth $138 million, and share-based incentive compensation of about $21 million. Additionally, with foreign currency transactions of about -$17 million, changes in trade receivables of about $119 million, changes in inventories close to -$142 million, and trade payables of $30 million, I obtained 2031 net cash provided by operating activities of about $304 million. Finally, if we assume the acquisition of property, plant, and equipment of close to -$120 million, 2031 FCF would be about $185 million.

{kind=link}

If we assume FCF close to $123 and $185 million, exit multiples close to 14x and 21x, and a WACC between 3% and 7%, the implied forecast price would not be far from $39-$44 per share. I also obtained a maximum valuation of close to $59 per share. My EV/FCF exit valued between 14x and 21x is in line with previous valuation multiples. The company traded between 15x and 22x in the past.

Source: YCharts

Note that for the calculator of the net debt, I included the cash in hand, the long-term debt, and short-term debt, but I did not include obligations with employees or pension liabilities.

Source: DCF Model

With the previous assumptions, the median internal rate of return would not be far from 4%-11%, however, I obtained a maximum IRR of 16.555%. I know that other investment analysts may offer different price targets with different assumptions. With that, I believe that most investors out there would conclude that Orion is undervalued.

Source: DCF Model

Competitors

The company is among the top 3 largest producers of specialty carbon black and rubber carbon black in the world. Its main competitors are Cabot Corporation ( CBT ) and Jiangxi HEIMAO Carbon Black Co., followed by Tokai Carbon Co. ( TKCBY ) and Birla Carbon.

Smaller regional competitors are primarily involved in standard or MRG applications, and these players are less likely to be in a position to provide specialized products used in MRG applications or for high-end tire manufacturing.

Risks

Orion is exposed to fluctuations in the price of the raw materials it uses to manufacture its products, the main one being carbon black oil composed of residual heavy oils. The raw material costs are influenced by the availability of various types of coal, and natural gas, the supply and demand for such raw materials, and related transportation costs.

On the other hand, the company was seriously affected by the development of the conflict between Russia and Ukraine, and events like this in relation to international energy markets can seriously affect the company's income.

The company is also exposed to the possibility that new regulations and tax impositions will be defined on the production of conventional energy in general and/or production related to coal and carbon black in particular as well as the technological advances that could affect the competitiveness of its business model.

Conclusion

Orion recently delivered expectations for FCF growth, lower capex expectations, and megatrend drivers like new EV vehicles or demand for batteries. Additionally, the company appears to be using new cash flow to lower its net debt as well as to buy back its shares. Furthermore, R&D is also trending north. All these are fair reasons to see Orion as a buy. The current stock price is also quite appealing. Yes, I do see risks from fluctuations in the price of the raw materials, new environmental regulations, and tax impositions. However, even considering the risks, Orion appears significantly undervalued.

For further details see:

Orion S.A.: Automotive Coatings And EVs Demand Could Trigger Price Action