ORLA - Orla Mining: An Exceptional Year But Tough Comps Ahead

Summary

- Orla Mining was one of the better-performing gold miners in 2022, up 6% for the year vs. a 15% decline in the Gold Juniors Index.

- This can be attributed to Orla beating already ambitious guidance considering it was its first year of commercial production, with a ~15% beat vs. its initial guidance mid-point.

- However, 2023 is expected to be a less robust year based on guidance with higher costs and flat to down production, with the former impacted by inflation/higher sustaining capex.

- So, while I continue to see Orla as one of the best growth stories sector-wide with a team that is clearly over-delivering on promises, I think it's difficult to justify chasing the stock above US$4.30 with tough comps on deck.

2022 was a year to forget for most of the gold sector, with several companies missing guidance and set to report sharp increases in costs due to inflationary pressures. However, Orla Mining ( ORLA ) was one of the few exceptions in the group, trouncing its initial FY2022 guidance of ~95,000 ounces by reporting annual gold production of ~109,600 ounces. This was even more impressive given that this was Orla's first year of commercial production at Camino Rojo, and the company should also easily beat cost guidance, though the higher output helped this. Meanwhile, and as detailed in past updates, the company made a bold acquisition at the right price to upgrade its development pipeline.

However, while Orla is heading into 2023 with a very attractive development pipeline that includes two high-margin heap-leach assets and a massive sulphide project next door to its operating mine (Camino Rojo Oxides), 2023 is expected to be a softer year judging by guidance. It's important to note that its Camino Rojo Oxides Mine is still expected to be one of the lowest-cost assets in the sector this year, but with the impact of inflationary pressures and higher sustaining capital, costs are expected to increase materially. So, with Orla trading near 0.80x P/NAV, which doesn't offer much margin of safety and tough comps on deck, I don't see much value in chasing the stock above US$4.30.

Q4 Results

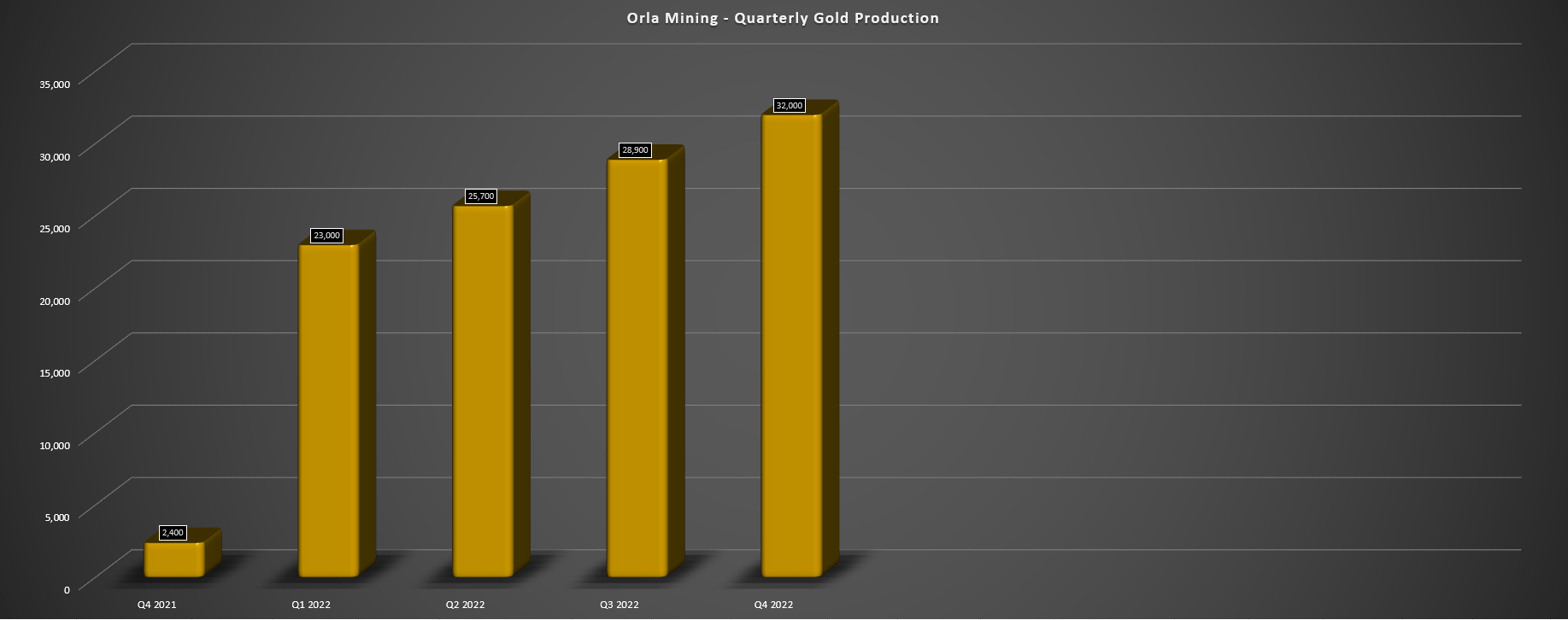

Orla Mining ("Orla") released its Q4 results this week, reporting quarterly production of ~32,000 ounces of gold, marking the company's best quarter to date and an 11% beat vs. its previous record of ~28,900 ounces. This was helped by continued outperformance relative to nameplate capacity for daily stacked throughput rates. In fact, its average daily throughput came in at ~19,600 tonnes per day in Q4, a record for the company, and a ~9% outperformance vs. nameplate capacity (18,000 tonnes per day). The result of this solid finish for 2022 is that Orla produced ~109,600 ounces of gold for the year, a 15% beat vs. its initial guidance mid-point of 95,000 ounces and a more than 4% beat vs. its updated guidance mid-point. This performance is commendable in a year with challenging weather for some jurisdictions, COVID-19 exclusions, and a tight labor market.

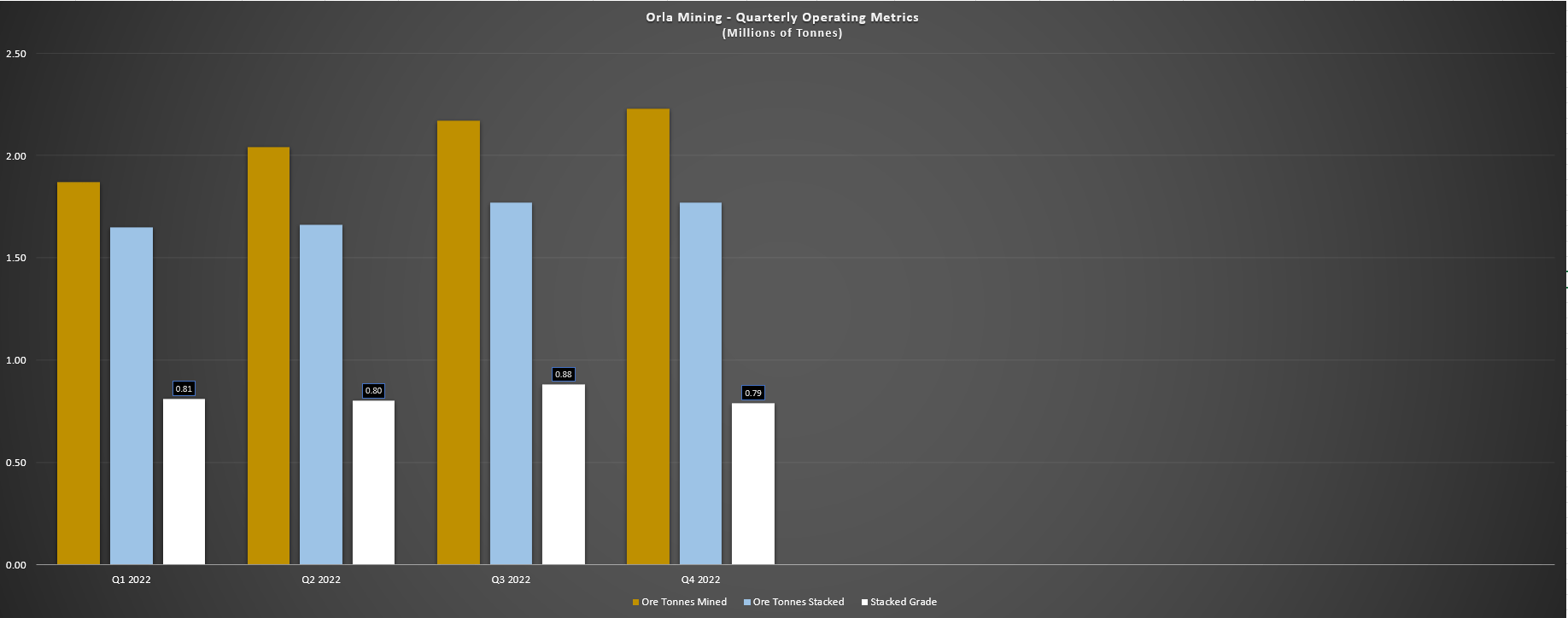

Orla Mining - Quarterly Gold Production (Company Filings, Author's Chart) Orla Mining - Quarterly Operating Metrics (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Digging into the results a little closer, we can see that Orla mined ~2.23 million tonnes in Q4 and processed ~1.78 million tonnes, representing a record for ore tonnes mined for the company. Meanwhile, while its stacked ore grade dipped slightly, the higher throughput made up for the slight dip in grades, allowing for another record quarter. In addition, the company's run-of-mine ore stockpile is sitting at ~2.12 million tonnes at 0.34 grams per tonne of gold, up from ~1.67 million tonnes at the end of Q3. Orla noted in its prepared remarks that it will be constructing a dome to improve dust control for its ore stockpile, with this expected to cost $2.0 million, one reason for the increase in sustaining capital expected next year.

Overall, Orla's 2022 performance was exceptional, and based on the production beat, the company will be one of the only gold miners to beat initial production guidance as well as initial cost guidance ($600/oz to $700/oz). In fact, with a significant beat vs. output guidance, I would expect all-in-sustaining costs [AISC] to come in below $620/oz, making Orla one of the lowest-cost mines globally and only behind a few mines that include Fosterville, Cadia, and Ernest Henry, with the latter two benefiting from copper by-product credits. So, while Orla may not be in a Tier-1 ranked jurisdiction (though pretty close with it being in arguably the most attractive mining state in Mexico, Zacatecas), the company certainly deserves a premium relative to most junior producers given its exceptional margins (~66% AISC margins at $1,800/oz gold).

2023 Outlook

While the Q4 and FY2022 financial results that will be reported next month will be glowing due to the strong Q4 performance, the market is forward-looking, and at least from an operational standpoint, margins could fall sharply next year, as will free cash flow. This is based on the fact that sustaining capital spending will be higher in 2023 (ore stockpiles dome cover, capitalized exploration, minor operational improvements), and production should be flat to down given Orla's guidance of 100,000 to 110,000 ounces (105,000-ounce midpoint) vs. ~109,600 ounces produced this year.

Camino Rojo Operations (Company Website)

{kind=link}

Meanwhile, costs are expected to increase sharply, partially impacted by inflationary pressures (reagents and consumables) and higher sustaining capital year-over-year. The result is that assuming a constant $1,825/oz gold price, AISC margins will dip from FY2022 estimates of $1,205/oz to FY2023 estimates of $1,035/oz. Meanwhile, I would not be surprised to see cash costs rise above $510/oz this year, a meaningful increase vs. Q3 costs of $452/oz and year-to-date costs of ~$450/oz. This combination of slightly lower production and higher costs is not ideal unless the gold price can pick up all the slack, and free cash flow should dip below $70 million this year, a high single-digit decline on a year-over-year basis.

As discussed earlier, even if margins dip to $1,035/oz ($1,825/oz average realized gold price in FY2023 [-] $790/oz AISC), Orla's margins will still be nearly 90% above the industry average. Hence, I am not putting down Orla by any means, and this story checks all the boxes with a simple high-margin mine in an attractive jurisdiction, a robust development pipeline, and, most importantly - a team that is over-delivering on promises. Still, stocks can underperform when they are coming up against tough comps if they are priced richly heading into these comparisons, similar to what we saw among retail stocks in 2022 as they lapped record years in 2021, benefiting from sales leverage due to government stimulus and wardrobe refreshes (pent-up demand). Let's dig into the valuation:

Valuation & Technical Picture

Based on ~347 million fully-diluted shares and a share price of US$4.30, Orla Mining trades at a market cap of ~$1.49 billion and an enterprise value of ~$1.57 billion. This has left the stock trading at ~0.70x P/NAV vs. an estimated net asset value of ~$2.0 billion. I would argue that a fair multiple for the stock is 0.90x P/NAV, given that while its margins are exceptional, it will remain a single-asset producer until at least 2025. After applying a 0.90x P/NAV multiple and subtracting net debt and estimated general & administrative expenses [G&A], I see a fair value for the stock of ~$1.78 billion or US$5.13 per share. The result is that Orla has approximately 19% upside to fair value, suggesting we could see further upside for the stock.

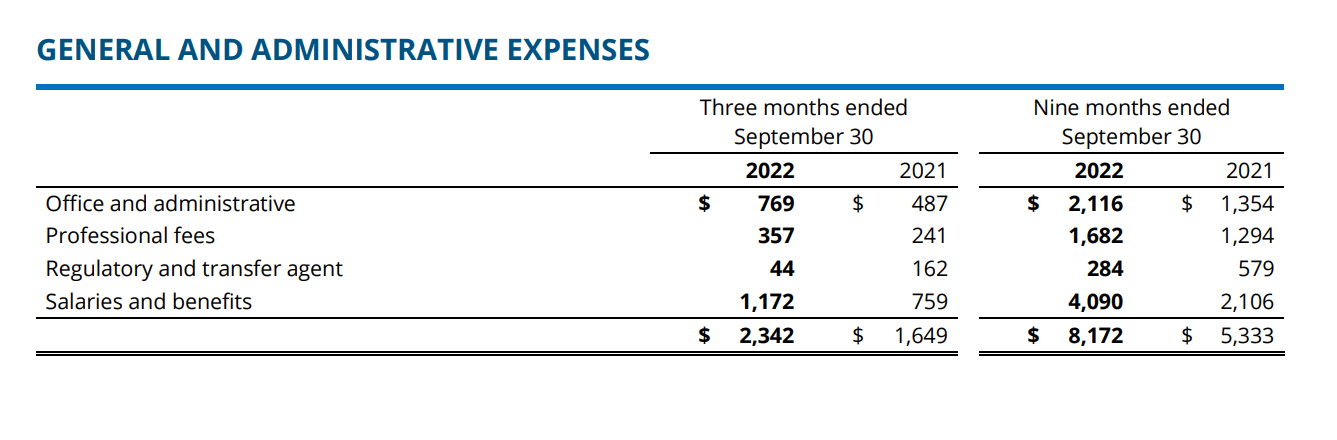

Corporate G&A looks like it will come in at ~$12.0 million in FY2022 by annualizing the year-to-date expenses and higher expenses in Q4 following the Gold Standard acquisition. It will increase to $15.0 million in FY2023 based on guidance.

Orla Mining - G&A Expenses Year-to-Date (Company Filings)

{kind=link}

However, when it comes to buying small-cap producers, I prefer to buy at a minimum 40% discount to fair value, and this is especially true when it comes to single-asset producers. If we apply this discount to Orla's estimated fair value, the stock would need to dip below US$3.10 to move into a low-risk buy zone, requiring a significant decline from current levels. This doesn't mean that the stock has to decline this far to meet my rigid buying criteria. However, with the stock no longer in a low-risk buy zone from a valuation standpoint, I think patience is the best course of action vs. chasing the stock after it's just enjoyed an ~87% rally.

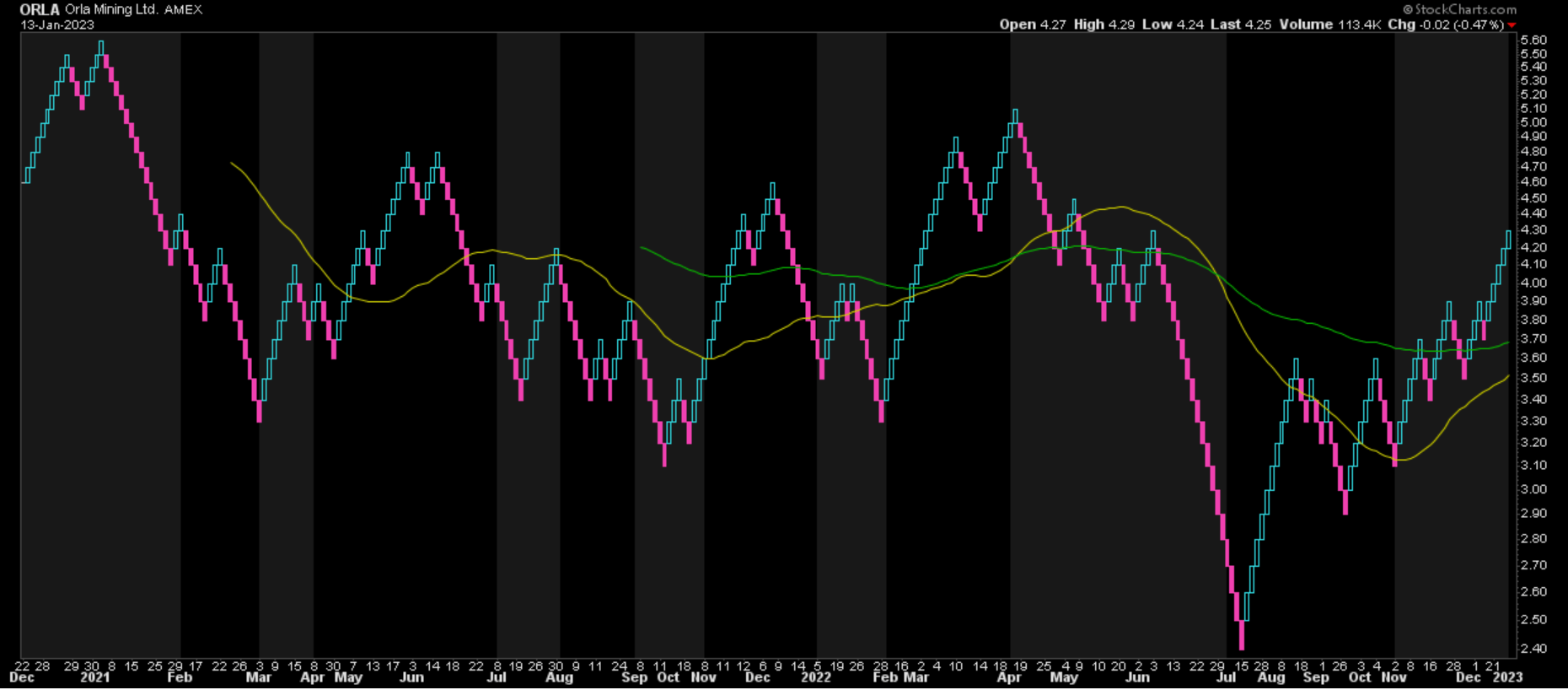

ORLA - 2-Year Chart (TC2000.com)

{kind=link}

Moving to the technical picture, we can see that Orla may have regained its key moving averages, but the stock is now sitting in the upper portion of its trading range, with upper support at US$3.00 and strong resistance at US$4.50. This translates to a reward/risk ratio of 0.25 to 1.0, with $0.35 in potential short-term upside to resistance and $1.30 in potential downside to support. So, while the stock may be trading shy of fair value, it's hard to argue for paying up for the stock here at US$4.30 with a limited margin of safety, and the stock extended above its next support level.

Summary

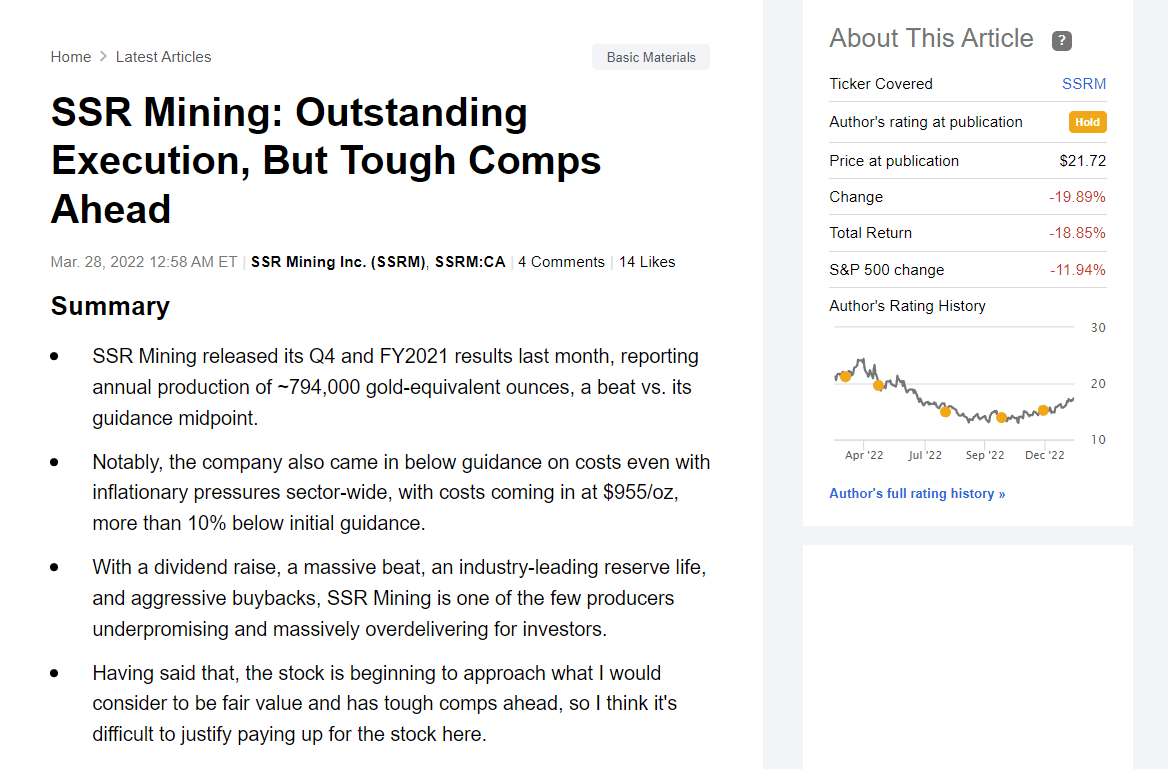

Orla Mining had an exceptional year in 2022 and is likely to report the lowest costs within its peer group, with AISC likely to come in below $625/oz. However, operating costs are expected to rise sharply next year on the back of relatively flat production, translating to tough comps ahead, similar to the position that SSR Mining ( SSRM ) was in heading into 2022, which I highlighted in my March article " Outstanding Execution, But Tough Comps Ahead ." While I certainly couldn't have foreseen the disruption of operations at Copler for SSR Mining, the stock was one of the worst performers in 2022, with the unfavorable combination of being priced close to full value and coming up against tough comps - a setup similar to Orla today.

SSR Mining Article - March 2022 (Seeking Alpha Premium/Pro)

{kind=link}

Obviously, Orla could be guiding conservatively and instead trounce guidance like it did last year. Still, with the stock trading near 0.80x P/NAV and coming up against more difficult comparisons, it's difficult to justify paying up for the stock here. So, while I think Orla Mining is a phenomenal story in the gold space with a top-10 growth profile and very solid assets, I think it's best to err on the side of caution and wait to buy sharp pullbacks vs. chasing rallies. In summary, I remain Neutral on the stock and continue to focus elsewhere in areas where I see better relative value within the sector. One example is Sandstorm ( SAND ), trading at less than 1.0x P/NAV with increased diversification and industry-leading growth with its royalty/streaming model.

For further details see:

Orla Mining: An Exceptional Year, But Tough Comps Ahead