ORLA - Orla Mining: Producer Debutante Concludes A Stellar Year

Summary

- By all accounts, Q4 was another solid quarter at the Camino Rojo mine, bringing 2022 to an impressive conclusion.

- The outlook for 2023 is more of the same.

- Plenty of speculation is baked into the current market valuation.

Orla Mining ( ORLA ) declared commercial production at its Camino Rojo heap leach gold mine in Zacatecas, Mexico, effective April 1, 2022. Fast forward three quarters and the company has just released operational results for Q4, concluding a transformational 2022. Orla Mining will present its annual financial results after markets close on March 16, followed by a conference call the day after. Here is our preview for the call, as well as for the year 2023 based on the company's guidance which was also included in the latest news release.

Camino Rojo Operations

Orla Mining has transferred from a development company to an operating gold miner seemingly without a glitch. Mine construction was accomplished within budget and on time, and the commissioning and ramp-up phase took less time than expected. This is a rare success story in a sector where plenty of mine developments turn into comedies of errors. The operational data for Q4 confirms our favorable view of Orla Mining's operational prowess.

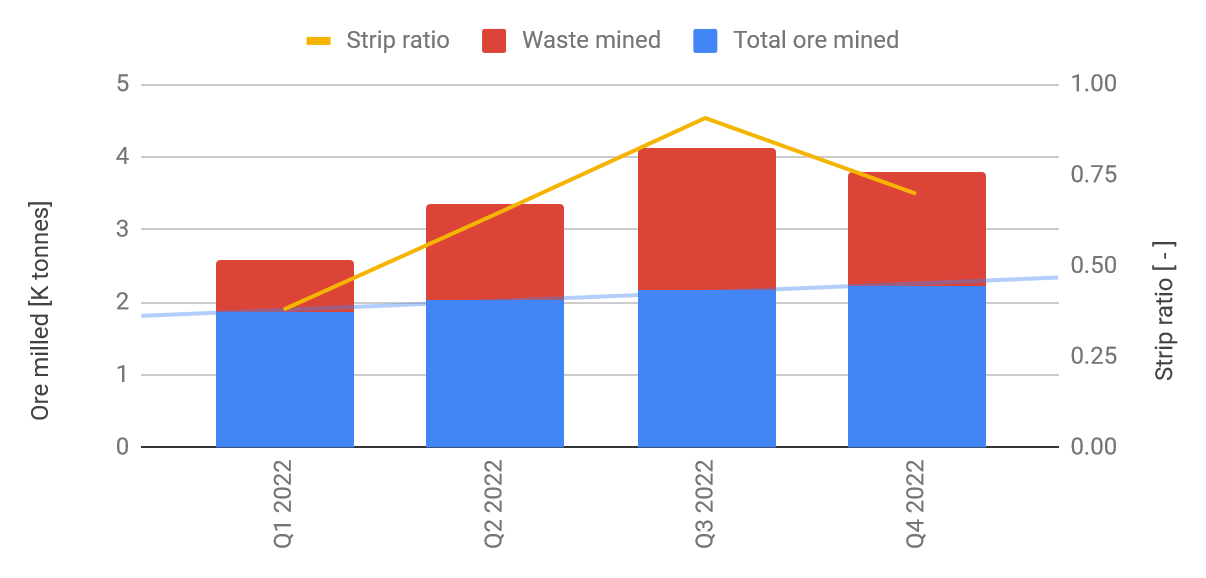

Ore production from the open pit has been trending up all year, and Q4 numbers were no exception (blue bars and trendline in the chart below). Less waste mining was required in Q4, leading to a favorable strip ratio of just 0.7.

{kind=link}

{kind=link}

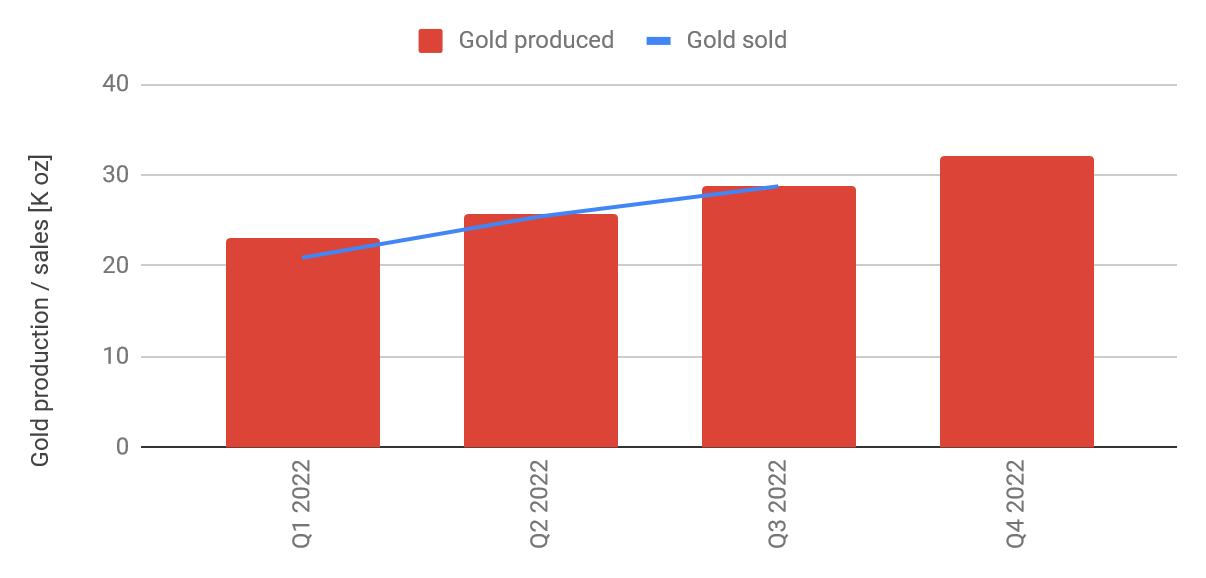

Nevertheless, Orla Mining posted another quarterly gold production record in Q4, ensuring the company's annual number came in right at the top of the guided range. Mind you, that's the updated guidance too, as Orla Mining increased its guidance in the Q3 report.

{kind=link}

Reading across Royal Gold's ( RGLD ) Q4 operational data (typically the first company to provide an average quarterly realized gold price) we can glean $1,710/oz as a measure of the gold price for our Q4 forecast for Orla Mining. Assuming that most of the gold production has been sold, we estimate a top line just shy of the $55M mark -- another quarterly record.

We expect Q4 costs at the Camino Rojo mine to have dropped quarter-on-quarter due to the reduced stripping tonnage, and thanks to the record ounce count spreading fixed costs around. Conservatively assuming a similar cost structure and capex spending as in Q3, we expect Q4 free cash flow to print well in excess of $20M.

The company stated a $7.5M cash position increase during Q4, and also reported a $15M repayment to Fresnillo ( FNLPF ), plus a $5.6M repayment on the credit facility. Our free cash flow estimates compare well with these numbers.

The Q4 report sure looks like a continuation of Orla's success story from these numbers and estimates. And the market seems to expect no less, judging from the company's share price outperformance over the past six months when compared to peers ( GDXJ ).

2023 Guidance and Financial Preview

Orla Mining's production guidance projects a repeat of 2022 numbers, which correlates well with the mine plan tabled in the current technical report on the Camino Rojo mine. The company also guides for all-in sustaining costs around $800/oz, or 30+% higher than in 2022.

{kind=link}

The mine was still in pre-production mode in Q1/22, and Orla Mining has exceeded the quarterly production implied by the guidance in all three quarters of commercial production. Given the operational performance along with the cost control exercised during commercial production so far we submit that this guidance is conservative and we would not be surprised to see an adjustment to the upside again in 2023. Nevertheless, using guidance mid-range numbers points to $90M of free cash flow before growth capital during 2023, or $22.5M per quarter (assuming a gold price of $1,700/oz). Deducting growth capex and exploration expenditures (guided to $37M), and corporate level G&A (guided to $15M) leads to our best free cash flow estimate of $38M for the full year 2023.

Orla mining will be obliged to pay Fresnillo a last installment in the amount of $22.5M at the end of 2023, and there are $22M in repayments scheduled on the term facility over the course of the year. The total of these debt repayments exceeds our free cash flow estimate by $4.5M, a small shortfall well within the rounding error margin of our trusted back of the envelope, and manageable without problem considering the $96.6M cash position at the end of 2022.

In other words, funding this year's debt obligations and a highly ambitious exploration program should be possible from cash on hand and cash flows generated at the Camino Rojo mine. Agreed debt repayments will ease off after this year as there will be no more payments due to Fresnillo.

2023 Growth Initiatives

We mentioned $37M earmarked for growth and exploration programs in 2023, and more than half of this amount will be spent on exploration around the Camino Rojo operations. To quote the latest news release:

Exploration at Camino Rojo will focus on confirmation drilling of the oxide pit layback, resource and reserve conversion, additional Camino Rojo sulphide drilling to support development planning, and drill testing of regional targets.

This is a good mixture of low-hanging fruit (oxide pit layback), and long-term mine planning (sulphide, regional targets). We see a high potential for oxide mining at Camino Rojo to remain operational beyond the current 10-year mine life, and Orla Mining seems to share this view. And beyond the oxide potential, this mine has a significant sulphide resource which will attract a significant share of the development capital.

The Railroad project in Nevada is going to receive the lion's share of the remaining growth capital. Judging from the news release wording, we expect an exploration push with a goal of adding oxide resources to the existing inventory, potentially supplementing the low-grade ore from the Pinnion pit in the latter years of the mine plan outlined in the current feasibility study.

Valuation

Orla Mining shares traded for $3.90 at the time of writing, which translated into an enterprise value of ~$1B. That's more than twice the stated book value of $459M, a highly unusual multiple for a junior gold miner with a single operating asset. Using our 2023 cash flow estimates from earlier in this piece we calculate a FCF multiple of 11 which is perhaps more reasonable, but still on the high side compared to suitable peers.

The potential of the mentioned sulphide resource at Camino Rojo serves as a plausible explanation for this apparent premium. The market is obviously betting on Orla Mining finding ways to bring this resource to account. In this sense, we argue that Orla is still a highly speculative investment proposition, a valuation hybrid between a development company and a fledgling producer.

Summary & Investment Thesis

Market valuation for Orla Mining is difficult to justify simply from operational results at the company's Camino Rojo mine, despite stellar results in every quarter since the declaration of commercial production. The potential of the underlying sulphide resource seems to feature strongly in the market's view of this particular gold miner. The metallurgical results announced in May 2022 lend support to these high market expectations.

The company bought the Camino Rojo mine from Goldcorp, now Newmont ( NEM ), and there are strings attached to the sulphide ore stemming from this deal. Orla Mining had targeted the end of 2022 for the completion of a PEA for the sulphide project but hasn't released the results of this study yet. We view this study as the first major catalyst of this year, and we suspect that it will provide direction for the market valuation going forward. Technical solutions will be important in this context, but also the strategies of how to cooperate with Newmont (if at all) when it comes to processing the sulphide ore.

At this moment, an investment in Orla Mining represents a bet on the sulphide project, to be presented in the upcoming PEA. Depending on the results of this study, there is room to move both to the upside and to the downside; however, given the multiples currently applied by the market we argue the downside potential is greater than the upside. We are holding our position for now and will re-evaluate our stance after the release of the PEA for the sulphide project.

For further details see:

Orla Mining: Producer Debutante Concludes A Stellar Year