ORLA - Orla Mining: Tracking To Top End Of Already Upward Revised Guidance

2023-12-13 12:56:17 ET

Summary

- Orla Mining Ltd. reported more impressive results at Camino Rojo Oxides, enjoying industry-leading margins and generating nearly $19 million in free cash flow in Q3 alone.

- Unfortunately, this was overshadowed by Panama passing a bill imposing a moratorium on metal mining concessions, potentially affecting Cerro Quema's future (development asset).

- In this update, we'll look at the Q3 results, how this affects the stock's valuation, and where Orla's updated low-risk buy zone lies.

Just over eight weeks ago, I wrote on Orla Mining Ltd. ( ORLA ), noting that while the company put up another exceptional quarter, the stock would need to make new correction lows below US$2.85 to head closer to a low-risk buy zone. Since then, the stock has corrected sharply, and there's now a foggier outlook for its Cerro Quema Project in Panama, with First Quantum ( FQVLF ) recently ordered to stop mining at an asset that accounts for ~5% of Panama's GDP and employs ~40,000 people.

Although an unfortunate development, this does not affect Orla's current mining operations, it doesn't affect its South Railroad Project in Nevada, and it doesn't impact plans to potentially develop an underground mine with Camino Rojo Sulphides. Still, this has dented valuation slightly and certainly sentiment, sending the stock to new 52-week lows despite continued operational excellence.

In this update, we'll look at the Q3 results , how this affects the stock's valuation, and where Orla's updated low-risk buy zone lies.

{kind=link}

Q3 Production & Sales

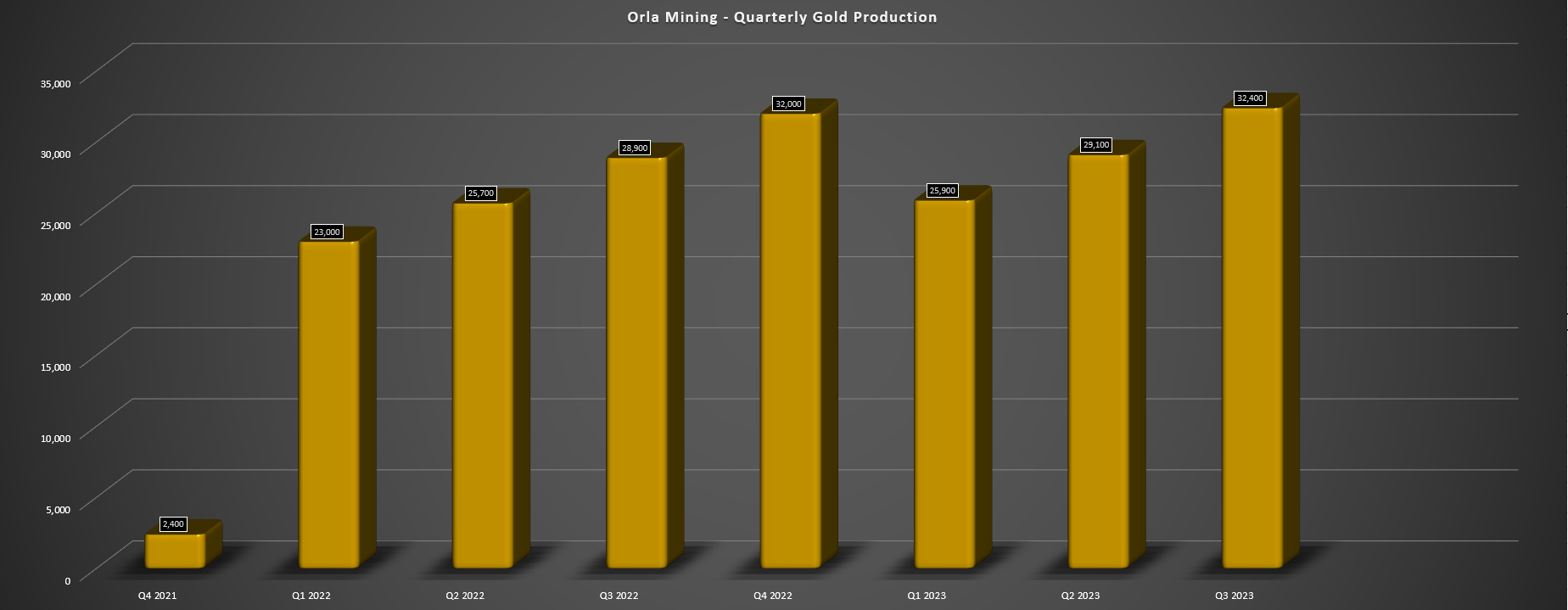

Orla Mining released its Q3 results last month, reporting quarterly production of ~32,400 ounces of gold, a 12% increase from the year-ago period. This solid performance has pushed year-to-date production to ~87,400 ounces (83% of initial guidance midpoint and 76% of updated guidance midpoint), and the company looks well positioned to deliver at the upper end of its already upwardly revised guidance (110,000 to 120,000 ounces) given its disclosure that October was a record with ~11,800 ounces produced.

Although these results are phenomenal, they are consistent with Orla's delivery on objectives to date, with the company building Camino Rojo Oxides on time/under budget despite headwinds from the global pandemic, and consistently over-delivering on promises since it went into production two years ago. The company also noted that it could see better recoveries with a switch to a lower crush size made in August based on metallurgical testing.

Orla Mining - Quarterly Gold Production - Company Filings, Author's Chart

{kind=link}

As for the company's financial results, Orla reported 23% revenue growth to $60.3 million on the back of higher gold sales and a much stronger average realized gold price ($1,921/oz vs. $1,699/oz). Meanwhile, operating cash flow and free cash flow came in at $25.0 million and $18.8 million, respectively, pushing year-to-date free cash flow generation to $31.7 million. This has allowed the company to continue paying down its debt, with Orla set to be net cash positive by year-end and with $25.0 million repaid after quarter-end to reduce its total debt to ~$111 million (includes deferred payments as part of layback agreement). Just as importantly, the strong cash flow generation is allowing to aggressively drill across its portfolio to grow ounces and ultimately production, which should ultimately lead to peer-leading production, cash flow, and growth in NAV per share as the company has seen minimal dilution while continuing to de-risk the future underground potential at Camino Rojo and chase low-hanging fruit at South Railroad.

{kind=link}

As it stands, Camino Rojo's deeper sulphide resource is ~8.8 million ounces of gold (81% indicated) plus ~75 million ounces of silver, with additional lead and zinc credits, with an average grade of ~0.30% lead/zinc.

Costs & Margins

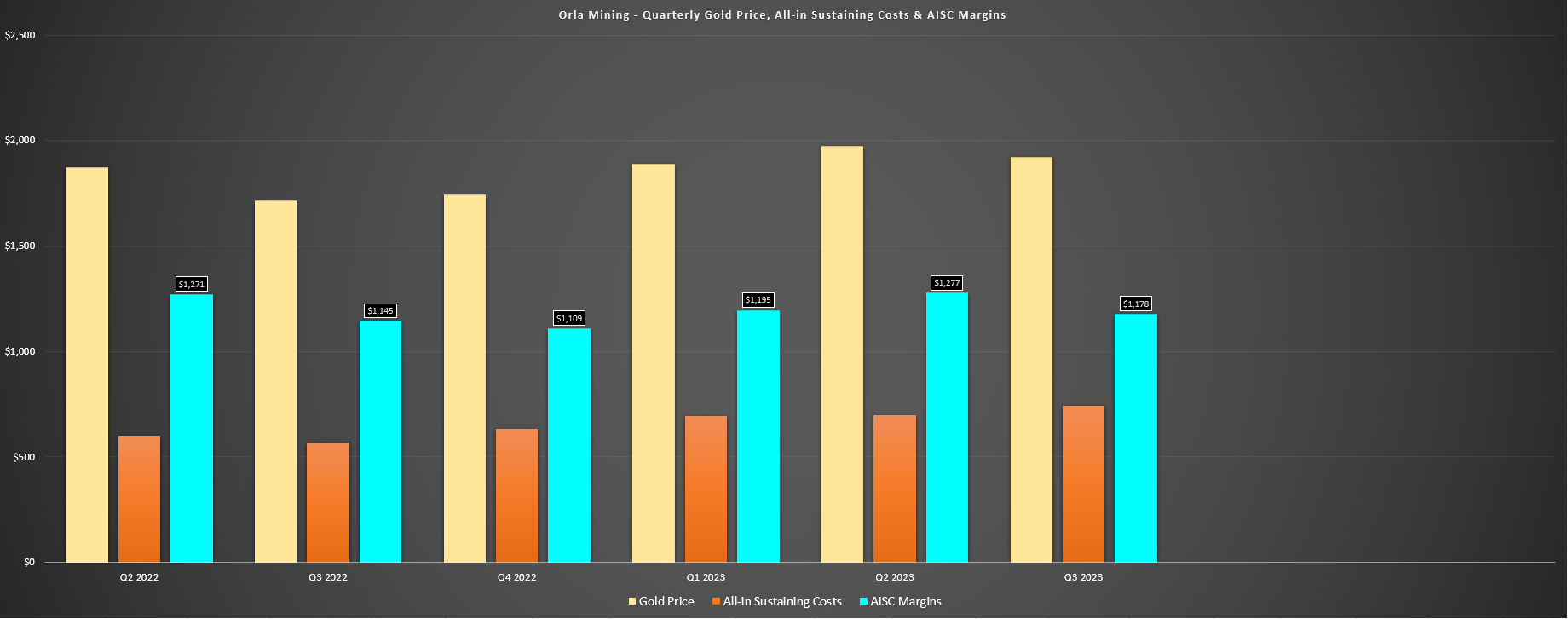

Moving over to costs and margins, Orla had another exceptional quarter and trounced its peers from a margin standpoint. This was evidenced by all-in sustaining costs [AISC] of $743/oz ($712/oz year-to-date) and AISC margins of $1,178/oz, a 7% improvement year-over-year with help from the higher gold price. And while all-in sustaining costs were higher year-over-year despite an increase in ounces sold, this was largely because of the increase in sustaining capital spend (the construction of dome for ore stockpile, construction of water wells, and IT network infrastructure) to $2.5 million and higher lease payments, up from ~$0.8 million in the year-ago period, as well as higher lease payments and G&A expenses. Still, costs are on track to meet the lower end of downward revised FY2023 guidance ($700/oz to $800/oz) and with Orla set to enjoy industry-leading costs yet again in 2023.

Orla Mining - Quarterly Gold Price, AISC & AISC Margins - Company Filings, Author's Chart

{kind=link}

That being said, while Orla benefited from lower mining costs this year, we should costs tick up in 2024 with more waste mined, related to delays securing permits from SEMARNAT for accessing certain pit areas. Fortunately, this has not affected 2023 production and a continued delay in receiving these permits should not affect 2024 either. Plus, while permits have been slow to arrive, they are at least being delivered, with Torex Gold ( TORXF ) receiving the in-pit deposition permit for the mined-out Guajes Pit in October.

In summary, while cost performance was ahead of my expectations this year, especially given the strength in the Mexican Peso, Orla benefited from less wasted mined and a more robust production profile overall, but with AISC likely to be closer to $800/oz next year with a higher strip ratio and the potential for a full year of currency headwinds if the Peso strength persists (albeit less than 50% denominated in Pesos according to the company).

Recent Developments

Unfortunately, while production, costs, and cash flow generation were positive, and Orla now has one of the best balance sheets among its junior producer peers, we did see one negative development in the period. As noted by the company, the National Assembly of Panama passed Bill 1110 , which included a suspension on granting, renewing, or extending concessions for the exploration, extraction, or exploitation of metal mining in Panama. The legislation was passed with 63 votes in favor, spurred by to public opposition to mining activity in Panama, with the government voicing its responsibility to prioritize public health and the environment. The most significant loser from this major shift is First Quantum, whose Cobre Panama Mine has been ordered to close, taking nearly 2% of global copper production offline at the massive 100,000 tonne per annum asset.

{kind=link}

In Orla's case, the company has spent a fraction of what First Quantum has at Cobre Panama given that Orla's Cerro Quema is a development-stage asset. This means that the potential loss if this project can't be moved forward is not all that significant to the company, even if it does impact its growth. Still, Cerro Quema's 2021 PFS highlighted an impressive (albeit small scale) project capable of producing ~80,000 ounces at sub $800/oz all-in sustaining costs and barely $200 million in upfront capex even if we adjust the 2021 figures ($626/oz AISC, $164 million capex) for inflationary pressures. And while I was only assigning $80 million in value to Cerro Quema ($0.23 per share), I think it's safer to assign no value today given the lack of hesitation by the Government of Panama to shut one of its largest contributors to GDP.

As for Orla, it stated the following:

"The impact of these recent developments on the company's Cerro Quema project remains uncertain. The company expects that various factors, including potential court challenges in the May 2024 for Panamanian general election may impact its strategy in Panama. The company will continue to monitor these developments and make an informed assessment of its strategy once additional information is available. We have and will continue to take a conservative approach to spending and development in Panama, awaiting more certainty to inform our strategy."

- Orla Mining, Q3 2023 Conference Call .

The second development worth noting is that Orla's application for a Change of Land Use permit related to its planned pit layback was declined for procedural reasons by SEMARNAT in Mexico, with the company having to resubmit the additional permit application. This is not a huge deal and certainly not nearly as significant a development as the news in Panama, but the slow permitting process for both outstanding permits in Mexico could impact ultimate permitting at Camino Rojo Sulphides, suggesting it might be safer to model a later production start than planned assuming the asset is approved for full construction later this decade.

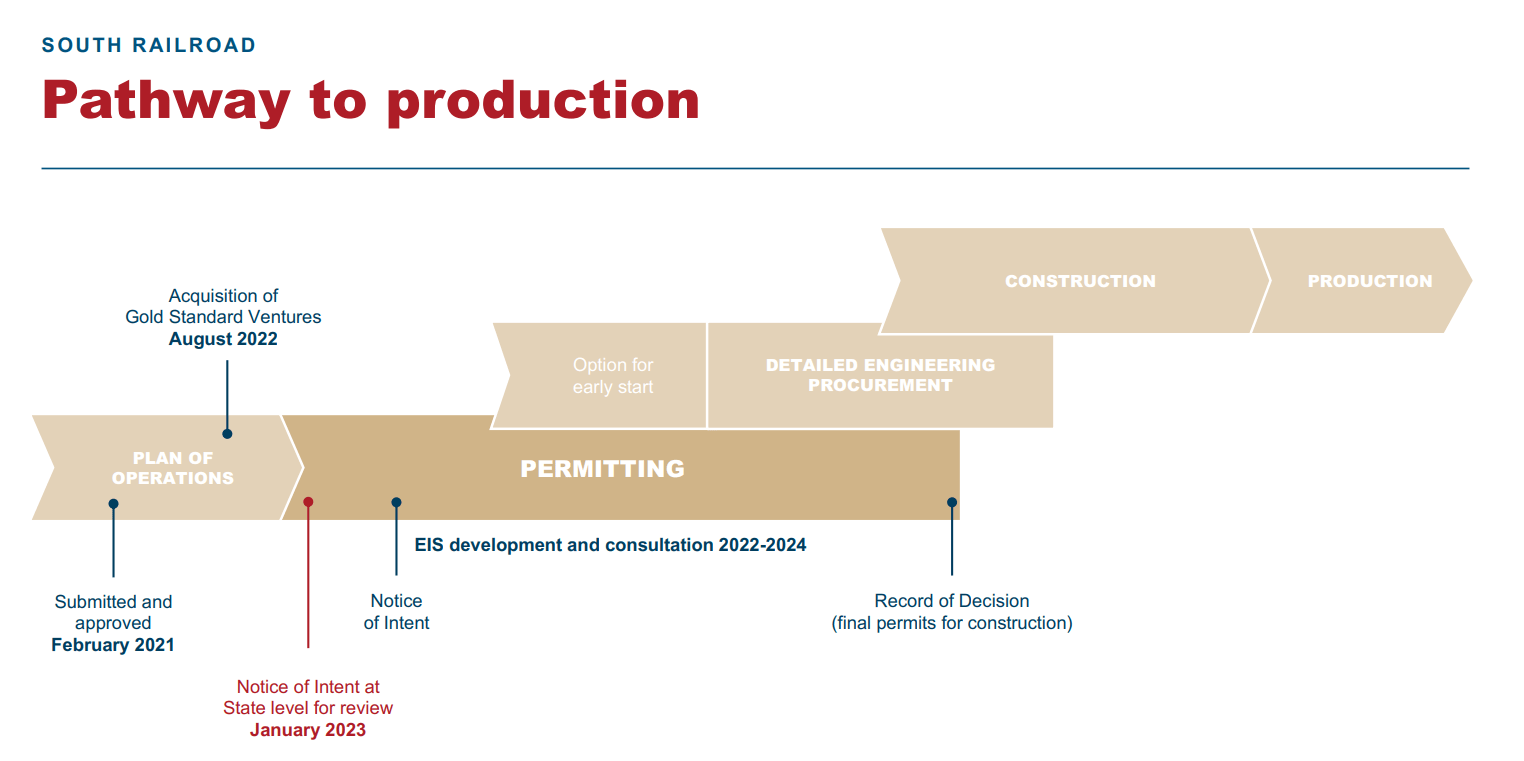

Finally, at South Railroad in Nevada, the company noted that it expects the Bureau of Land Management to file the Notice of Intent in the Federal Register in 2024, with a Record of Decision expected thereafter. Previously, I had expected commercial production by early mid-2026, but it looks like commercial production could be pushed to late 2026 earliest judging by the current timeline.

{kind=link}

Overall, the slower permitting in Nevada and Mexico is not a huge deal, and like Mexico, permits are being handed out (Goldrush recently obtained its Record of Decision) even if at a slower pace. And while production may be pushed out at South Railroad vs. more ambitious estimates highlighted at the time of the Gold Standard Ventures acquisition, the company is having no shortage of exploration success and I still expect it to be contribute meaningful production at attractive margins, with first five year average production of ~143,000 at sub $1,050/oz AISC (inflation-adjusted).

However, the developments in Panama are undoubtedly negative for Orla Mining Ltd., and it's hard to be optimistic about this asset, suggesting that it might be better to discount this asset significantly for the time being when valuing the company or simply remove it from Orla's valuation on a sum of the parts basis.

Valuation

Based on ~351 million fully diluted shares and a share price of US$2.70, Orla trades at a market cap of ~$950 million, making it one of the highest capitalization junior producers in the sector today. This premium valuation can be attributed to the company's industry-leading margins and strong pipeline relative to peers, with a massive sulphide resource at Camino Rojo and a relatively high-grade oxide heap-leach development asset on the Carlin Trend in Nevada (plus the 2nd largest land package on the prolific Carlin Trend).

That said, while Orla remains cheap on a P/NAV basis with an estimated net asset value of ~$1.96 billion and it trading at just 0.50x P/NAV, it is one of the more expensive names from a P/CF basis at ~10.8x FY2024 estimates. Hence, while the stock is down ~50% from its all-time highs, it still trades at a premium to some smaller producers sector-wide.

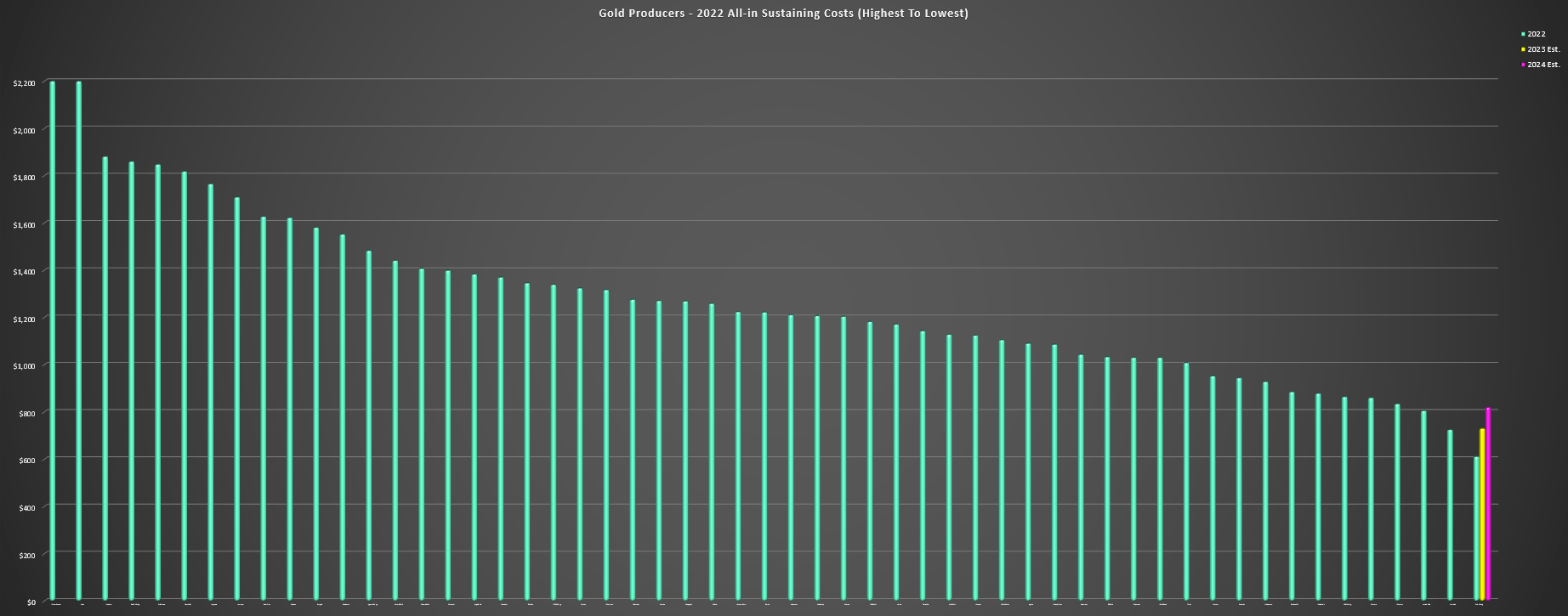

Gold Producers 2022 Costs vs. Orla Mining & Orla's 2023/2024 AISC Estimates - Company Filings, Author's Chart & Estimates

{kind=link}

Using what I believe to be a fair multiple of 0.90x NAV (bulk of NAV tied to Mexico) and 8.5x cash flow and a weighting of 65% to P/NAV and 35% to P/CF, I see a fair value for Orla of US$4.05 (down slightly to account for sector-wide multiple compression and no value assigned to Cerro Quema). This points to a 61% upside from current levels, but I am looking for a minimum 40% discount to fair value to justify starting positions in small-cap producers, and ideally closer to 50% for single asset producers in Tier-2/Tier-3 ranked jurisdictions. And if we apply this discount to ensure an adequate margin of safety, Orla's updated low-risk buy zone comes in at US$2.45 or lower. Hence, while the stock is getting closer to a low-risk buy zone after what's been a violent correction, it's hard to rule out a final lower low before the stock bottoms out in what's been a period of brutal underperformance since September.

Obviously, I could be wrong, and given Orla Mining Ltd.'s success to date, this is certainly one of the sector's better buy-the-dip candidates for an investor that is patient. This is because Orla can ultimately become a 270,000+ ounce producer in peak years with South Railroad online (2027?) and ultimately significantly higher production (to be determined) depending on what throughput rates it envisions for Camino Rojo Sulphides and if the asset is moved forward to a positive construction decision.

Hence, while the current ~$950 million valuation may look high, this is a company with a portfolio capable of producing closer to 400,000 gold-equivalent ounces per annum even without Cerro Quema in Panama, and this doesn't factor in any sulphide upside at Railroad South, with the company certainly having the right address southeast of Nevada Gold Mines' massive Carlin Complex on the other side of Interstate 80 in Nevada.

Railroad South Targets & Location - 2021 TR, Company Website

{kind=link}

Summary

Orla Mining reported more exceptional operational results in Q3, continues to lead the sector from a margin standpoint, and even with higher operating costs next year it should remain a top-3 producer when it comes to margin performance.

That said, permitting is taking a little longer than I expected at Railroad South, the uncertainty around Cerro Quema is not ideal, and although exploration success is exceeding my expectations across the portfolio, the key to filling in Orla's previously somewhat lofty valuation was graduating to dual-producer status and beefing up its production profile. These plans are not affected by Cerro Quema, but a slower permitting process at Railroad South suggests commercial production may have to wait until 2026.

Hence, using more conservative multiples to account for sector-wide multiple compression and removing Cerro Quema from my valuation, I see an updated low-risk buy zone for ORLA of US$2.45 or lower.

For further details see:

Orla Mining: Tracking To Top End Of Already Upward Revised Guidance