ORLA - Orla Mining: Tracking Well Against 2023 Guidance

2023-07-18 03:00:00 ET

Summary

- Orla Mining reported strong Q2 results, producing ~29,100 ounces of gold, a 13% YoY increase, putting the company on track to meet its FY2023 guidance of 100,000 to 110,000 ounces.

- Despite a strengthening Mexican peso, Orla is expected to beat cost guidance, with all-in-sustaining costs likely to be at or below the low end of guidance of $750/oz.

- At an enterprise value of ~$1.71 billion, I don't see a low-risk buying opportunity here, even if Orla has one of the best development pipelines among small-cap producers.

The Q2 Earnings Season for the VanEck Gold Miners ETF ( GDX ) begins next week, and one of the most recent companies to report its preliminary results is Orla Mining ( ORLA ). True to form, the company put together another exceptional report in Q2, producing ~29,100 ounces of gold on the back of strong throughput rates, which continue to exceed nameplate capacity. This has set the company up to deliver into its FY2023 guidance of 100,000 to 110,000 ounces with ease, and despite the impact of a strengthening Mexican Peso, it's looking like it could beat cost guidance as well, with all-in sustaining costs [AISC] likely to come in at or below the low end of guidance of $750/oz (FY2023 cost guidance: $750/oz - $850/oz). In this update, we'll look at Q2 production and recent developments and how the stock looks from a valuation standpoint after its recent rally:

All figures are in United States Dollars unless otherwise noted.

Q2 Production & Margins

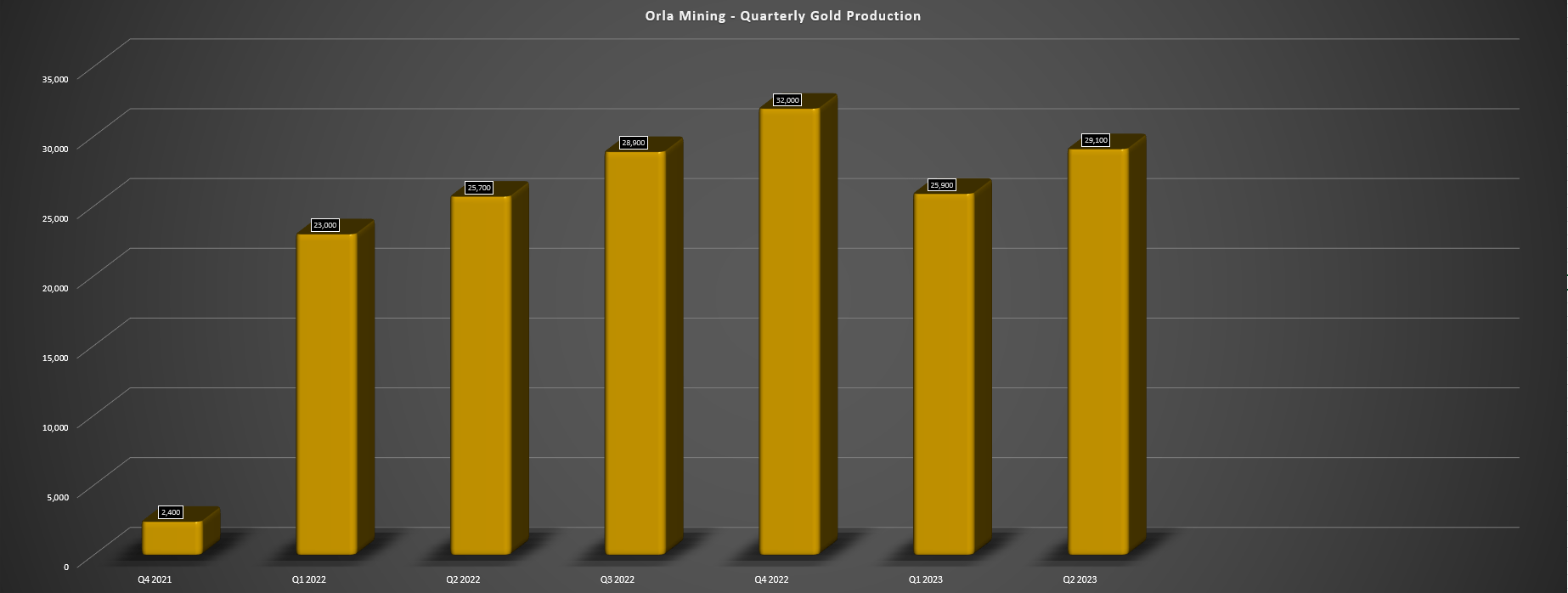

Orla Mining released its preliminary Q2 results last week, reporting production of ~29,100 ounces of gold, its second-best quarter to date and a 13% increase on a year-over-year basis. The company's impressive performance at its Camino Rojo Oxides Mine in the period was helped by daily throughput rates of ~19,700 tonnes per day that continue to exceed nameplate capacity by nearly 10%, and stacked grades also remained elevated at 0.77 grams per tonne of gold, only down slightly from 0.80 grams per tonne of gold in the year-ago period. This solid performance in Q2 has pushed Orla's year-to-date production to ~55,000 ounces, tracking at ~52.4% of its FY2023 guidance midpoint and setting the company up for a second consecutive beat on guidance since the mine went into commercial production last year.

Orla - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

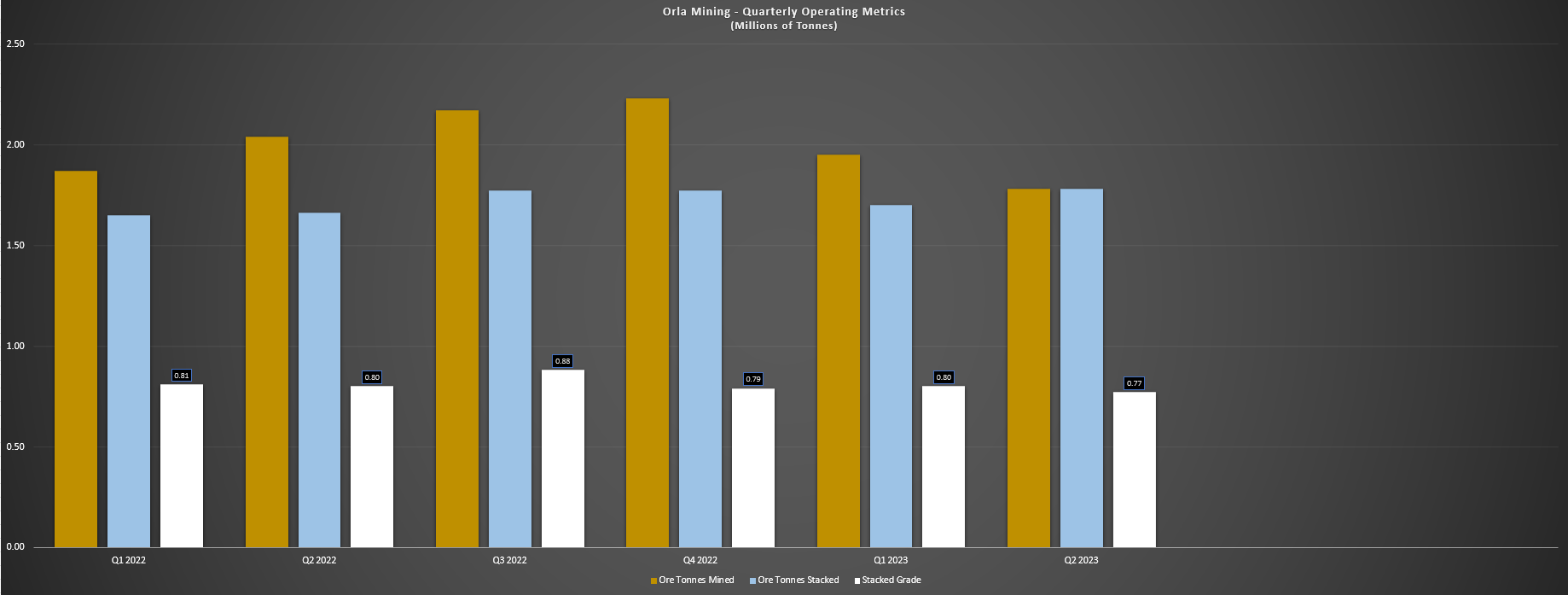

Digging into the results a little closer, we can see that the company mined ~1.78 million tonnes of ore in the period and benefited from an ultra-low strip ratio of 0.61 (ahead of higher strip ratios in H2), and stacked ~1.79 million tonnes in the period at 0.77 grams per tonne of gold. This figure compared favorably to ~1.66 million tonnes stacked in Q2 2022 at an average daily throughput rate of ~18,200 tonnes per day as the asset ramped up, and the strong production & sales should translate to a material increase in revenue year-over-year with 17% higher ounces sold (~29,800 vs. ~25,400 in Q2 2022) and what should be a 5% higher average realized gold price ($1,970/oz vs. $1,872/oz in Q2 2022), translating to $57+ million in revenue.

Orla Mining - Quarterly Operating Metrics (Company Filings, Author's Chart)

{kind=link}

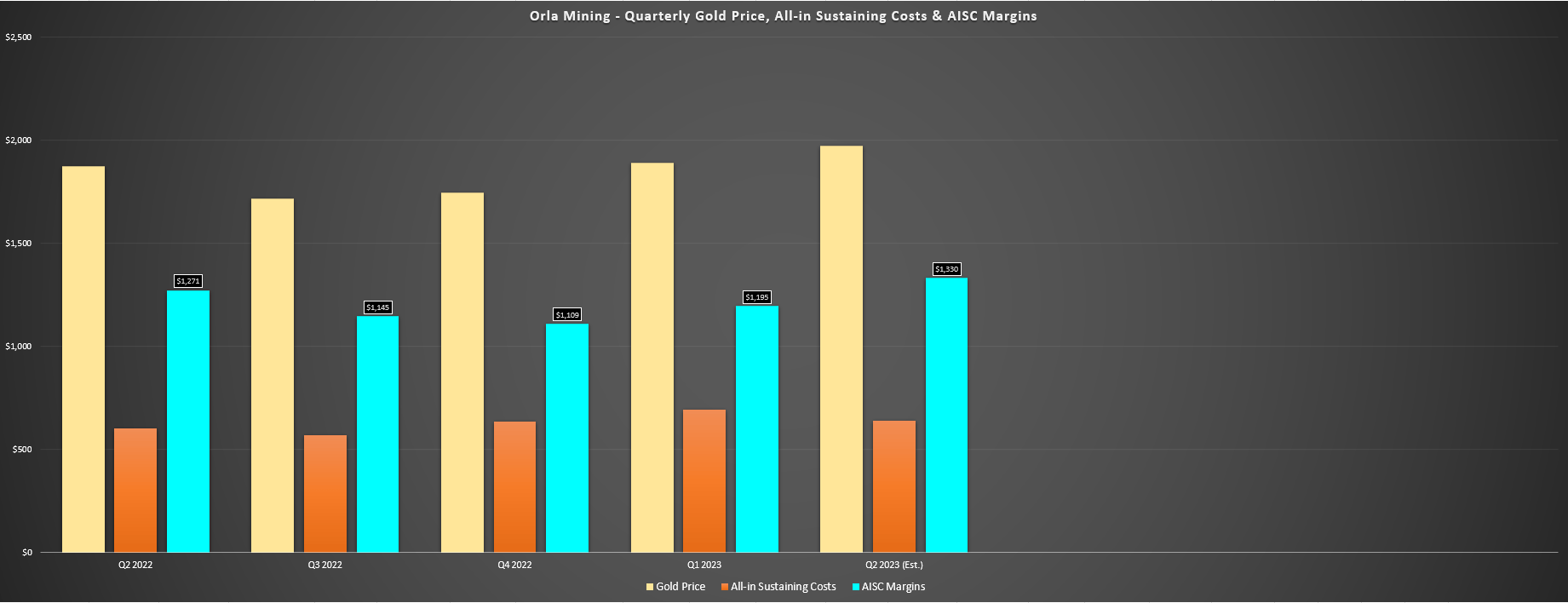

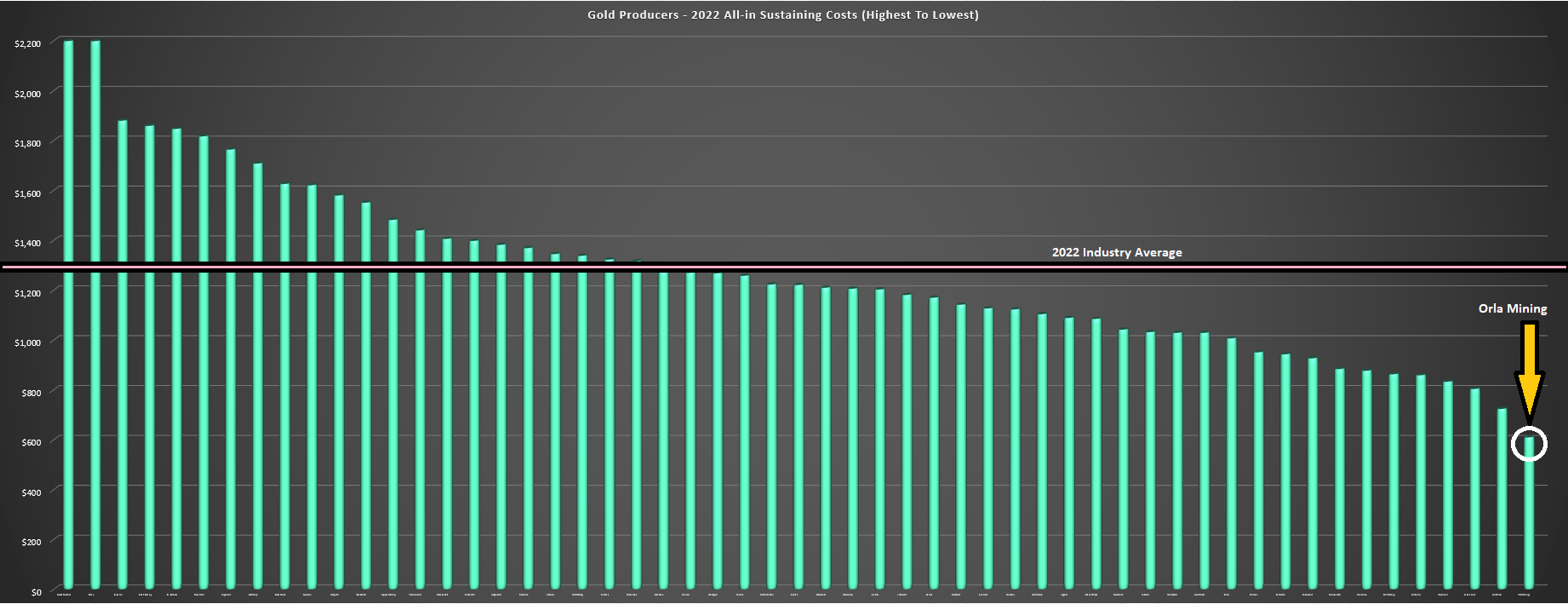

Finally, if we look at margins, 2023 was on track to be a higher cost year for Orla Mining relative to FY2022, which is one reason I noted that the stock could underperform its peers this year because of having difficult comps on deck . However, the gold price has picked up most of this slack given its strong year-to-date performance, and Orla should meaningful margin expansion in Q2 2023 if we assume an average realized gold price of $1,970/oz and all-in sustaining costs [AISC] of $640/oz, pointing to AISC margins of $1,330/oz (Q2 2022 AISC margins: $1,145/oz). Assuming its AISC margins come in at this level, this would place Orla's Q2 AISC at more than double the industry average, with Q2 AISC margins likely to come in below $620/oz based on an average realized gold price of ~$1,970/oz and industry average all-in sustaining costs of ~$1,350/oz. And on a full-year basis, Orla looks to have an excellent shot at being the sector's lowest-cost producer yet again (sub $750/oz AISC which would meet the low end of guidance), a feat it achieved with ease in FY2022.

Orla Mining - Quarterly Gold Price, All-in Sustaining Costs & AISC Margins (Company Filings, Author's Chart) Orla Mining FY2022 AISC vs. Industry Average & Peers (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Recent Developments

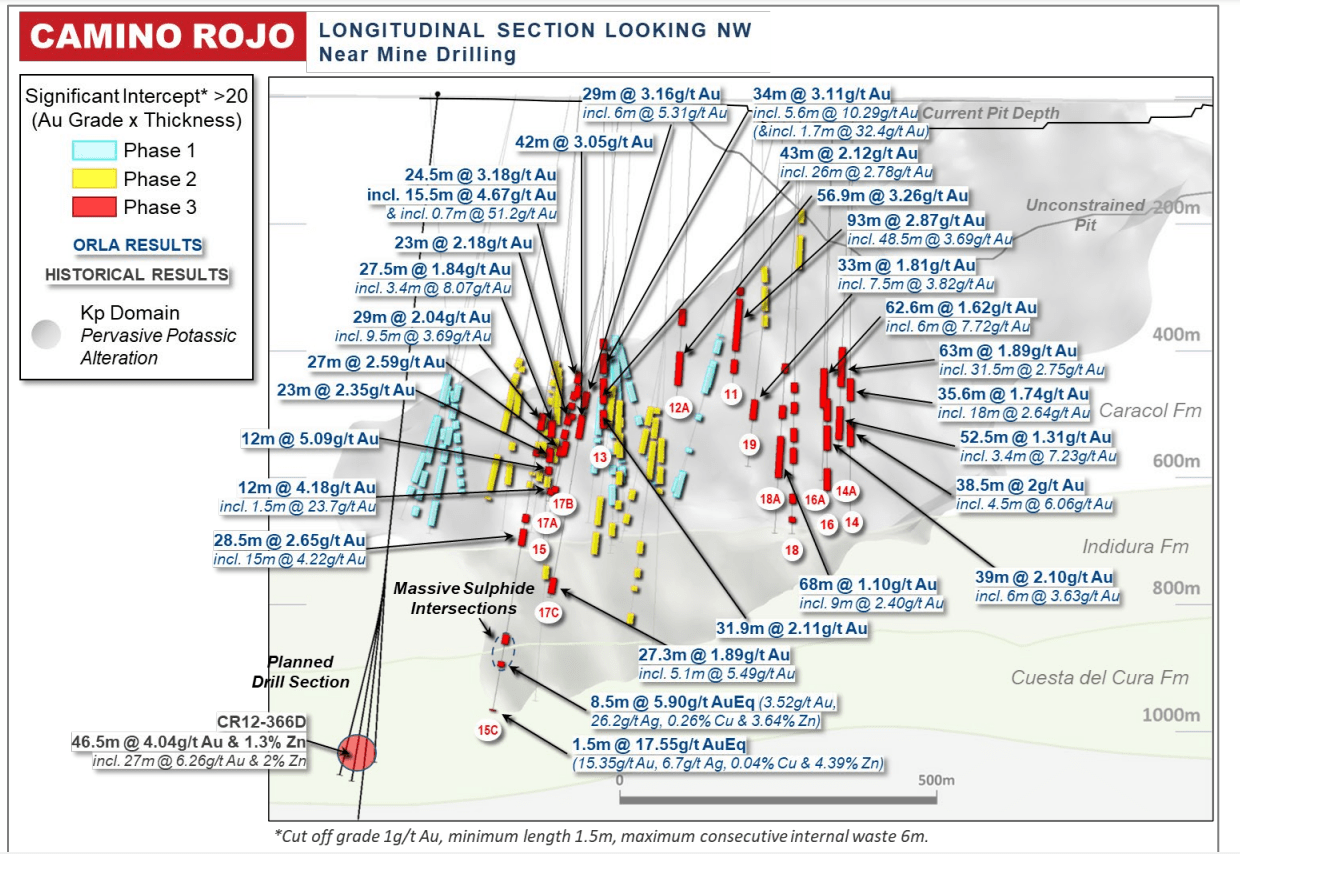

Moving over to recent developments, Orla released a comprehensive exploration update from Camino Rojo in late Q2, where it released results from Camino Rojo Sulphides and regional drilling at its first satellite target, Guanamero. Beginning with Camino Rojo Sulphides, holes released year-to-date have been nothing short of spectacular, with infill intercepts designed to tighten drilling spacing to 25-30 meters hitting multiple thick mid-grade intercepts. Highlight intercepts in the most recent June release included 93 meters at 2.87 grams per tonne of gold, 56.9 meters at 3.26 grams per tonne of gold, and 42 meters at 3.05 grams per tonne of gold, which continue to support a stand-alone processing scenario at Camino Rojo for processing its large sulphide resource. And these intercepts complemented already impressive intercepts drilled earlier this year, which were:

- 64 meters at 4.66 grams per tonne of gold

- 79 meters at 2.76 grams per tonne of gold

- 70 meters at 2.81 grams per tonne of gold

- 40.5 meters at 3.83 grams per tonne of gold

Outside of Orla's successful infill drilling that could support an underground operation later this decade, the company also targeted deeper mineralization and came away with a hit of 8.5 meters at 5.9 grams per tonne gold-equivalent (3.52 grams per tonne of gold, 26.2 grams per tonne of silver, 0.26% copper, and 3.64% zinc), and another intercept of 1.5 meters at 17.55 grams per tonne gold-equivalent with even higher gold and zinc grades. These results suggest the potential to add even further tonnage at depth and are not unusual, with historic drilling further down-plunge hitting 46.5 meters at just shy of 5.0 grams per tonne gold-equivalent. Orla noted in its release that it plans to conduct additional drilling to better define the grade and extent of this polymetallic potential (" replacement-style mineralization which is interpreted to be in close proximity to interpreted feeder-like structures" ), and also plans to test mineralization in proximity to historic hole CR12-366D (46.5 meters of 4.04 grams per tonne of gold, including 27 meters at 6.27 grams per tonne of gold with additional silver/zinc credits).

Camino Rojo Sulphides - Long Section Drilling Highlights (Company Website)

{kind=link}

Overall, Camino Rojo Sulphides continues to impress and deliver grades above my expectations and there's certainly reason to believe Orla has another operation here right next door to its high-margin oxides operation. However, investors will have to wait until year-end or later for a look at its planned Preliminary Economic Assessment [PEA] on Camino Rojo Sulphides and a better idea of its future economics. That said, while Camino Rojo Sulphides and regional drilling at the South Railroad Project (Nevada) have met or exceeded my expectations, drilling at the recently tested Guanamero Target (northeast of Camino Rojo Oxides) has been underwhelming, though we've only seen results from less than ten holes to date, which are shown below:

CRED23-02: 0.90 meters at 0.27 grams per tonne of gold

CRED23-03: 0.30 meters at 0.52 grams per tonne of gold

CRED23-04: 0.30 meters at 104 grams per tonne of silver and ~2.5% lead+zinc, and 0.80 meters at 1.51 grams per tonne gold-equivalent

CRED23-05: 3.3 meters at 0.94 grams per tonne of gold and 10.5 meters at 0.69 grams per tonne of gold

CRED23-06: 1.5 meters at 2.72 grams per tonne of gold and 1.3 meters at 61.2 grams per tonne of gold

While the average intercept drilled at Guanamero to date has been below my expectations on thickness and grades and sub-economic, it's nice to see a high-grade intercept of 1.3 meters at 61.2 grams per tonne of gold with visible gold, and I wouldn't count this asset out just yet. Orla noted in its release that it plans to follow up on drilling to test the southwest plunge of mineralization at Guanamero, and even if it doesn't meet expectations, this is just one of multiple regional targets at Camino Rojo. Plus, there's no immediate rush to find new oxide feed at Camino Rojo with the asset supporting production of 80,000+ ounces looking out to 2028, and this not including ounces likely to be added to resources and reserves from the Layback Program next to the current Camino Rojo Oxide Pit.

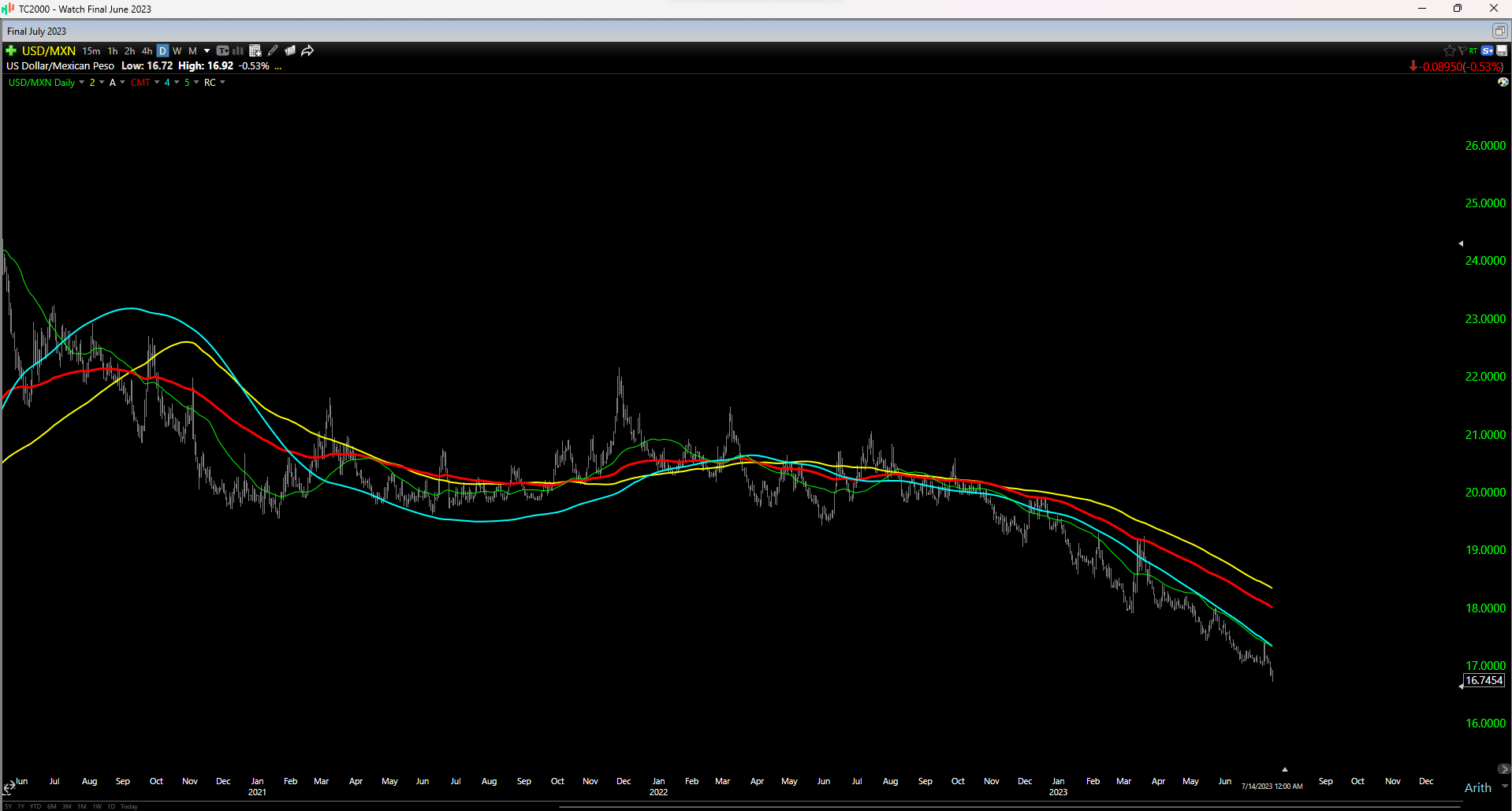

The final recent development worth noting is negative, and this is the fact that the Mexican Peso continues to soar against the US Dollar ( UUP ), hitting its highest levels in over three years last week, evidenced by the steep downtrend in the USD/MXN exchange rate (shown below). This is not ideal for producers with solely Mexican operations, and especially high-cost producers like Endeavour Silver ( EXK ) and Guanajuato Silver ( GSVRF ) which have razor-thin margins. However, Orla Mining is unique because it is among the top-5 lowest-cost producers sector-wide, it has benefited from less consumption on consumables, and it is benefiting at the same time from a rising gold price and lower fuel prices. So, while the impact from a strengthening Mexican Peso is not ideal short-term, I don't see this headwind as nearly as significant for Orla Mining as it is for other names where AISC margins are below 10% even in a good quarter, and all-in cost margins are negative.

USD/MXN Exchange Rate (TC2000.com)

{kind=link}

Valuation

Based on ~351 million fully diluted shares and a share price of US$4.73, Orla trades at a market cap of ~$1.66 billion and an enterprise value of ~$1.71 billion, making it one of the mostly expensively priced junior producers in the market today (sub 200,000-ounce producers). However, as highlighted in previous updates, the company is unique, with a development pipeline capable of growing its production to 400,000+ gold-equivalent ounces across multiple jurisdictions, with one of its assets (South Railroad) in the #1 ranked mining jurisdiction globally, Nevada. Hence, while the company may look expensive at first glance, its clear differentiator is industry-leading margins ($1,200/oz plus AISC margins in FY2023), and a strong pipeline, helping the company to command a premium multiple vs. its peers. The latter point is evidenced by Orla trading at over 25x EV/FCF vs. some peers at single-digit free cash flow multiples.

Using what I believe to be a fair multiple of 0.90x P/NAV and 9.0x FY2024 cash flow given its industry-leading margin profile and a 65% weighting to P/NAV and 35% weighting to P/CF, I see a fair value for the stock of US$5.00. This points to only a 6% upside to its estimated fair value, making it hard to justify paying up for the stock at current levels, even if it is in a league of its own among junior producers (sub 250,000 ounces per annum) from an operational excellence standpoint. Therefore, while I continue to see Orla Mining as a top-15 name sector-wide and one of the better growth stories, I don't see nearly enough margin of safety at current levels. Hence, I see the stock as more compelling from an investment standpoint, either at much lower prices or as an H2-2024 story when it's closer to first pour at South Railroad and trades at a more attractive cash flow multiple.

Summary

Orla Mining continues to be the sector's lowest-cost gold producer by a wide margin and is on track to enjoy a year of $1,200/oz plus AISC margins if the gold price can continue to provide a tailwind for gold producers in the second half of this year. That said, Orla trades at less than 10% discount to its estimated fair value (US$5.00), and I prefer to buy at a minimum 35% discount to fair value, making it difficult to justify paying up for the stock at current levels. For this reason, I continue to focus on names where I see a better relative value setup with single-digit forward free cash flow multiples, and those names trading at less than 0.50x P/NAV. However, with Orla being one of the top-5 growth stories sector-wide if it can execute successfully, it's certainly a name worth monitoring, and I would view any pullbacks below US$3.65 as buying opportunities.

For further details see:

Orla Mining: Tracking Well Against 2023 Guidance