ORA - Ormat Technologies: High Earnings Not As Attractive Compared To Capital Required To Grow

2023-10-04 09:00:00 ET

Summary

- Ormat Technologies is reinvesting heavily for growth, but the company's economic value is clamped due to high reinvestment requirements and low returns on business capital.

- The company has expanded its capacity by 100MW this year and secured new contracts for geothermal projects in New Zealand.

- The market's expectations for Ormat's sales and earnings growth may already be reflected in the company's current market value.

Investment summary

Those within the renewables space are at an interesting juncture for equity investors to consider. In the investment context, the industry enjoys cost differentiation and consumer advantages given its differentiated offerings from traditional electricity and energy suppliers. This is something to factor in. On the other hand, reinvestment requirements are obscenely high to grow sales and earnings, reducing the economic value of many companies involved.

Such is the case with the investment debate for Ormat Technologies ( ORA ) stock in my best estimation. For starters, the company is reinvesting heavily for growth, feeding all its cash flows back into the business in order to expand its capacity. Indeed, it has broadened capacity by a further 100MW this YTD, and also has big ambitions for its total wattage by FY'25. It also secured a number of business wins this YTD, including its latest geothermal ventures in New Zealand. Wall Street is eying 13% sales growth on 31% earnings growth this year as well.

There is no denying ORA's momentum in this regard. However, treating the business as a fellow investor, albeit investing in a portfolio of business lines vs. securities, capital appears more valuable in our hands vs. what ORA is producing on its own investments. The market's expectations are quite flat based on this examination, and in my view, these expectations may be warranted. This is despite the fact ORA still sells at ~32x forward earnings and 31.5x forward EBIT as I write, quite the ask. This report will unpack all of these points and more, linking back to the broader hold thesis. Net-net, rate hold.

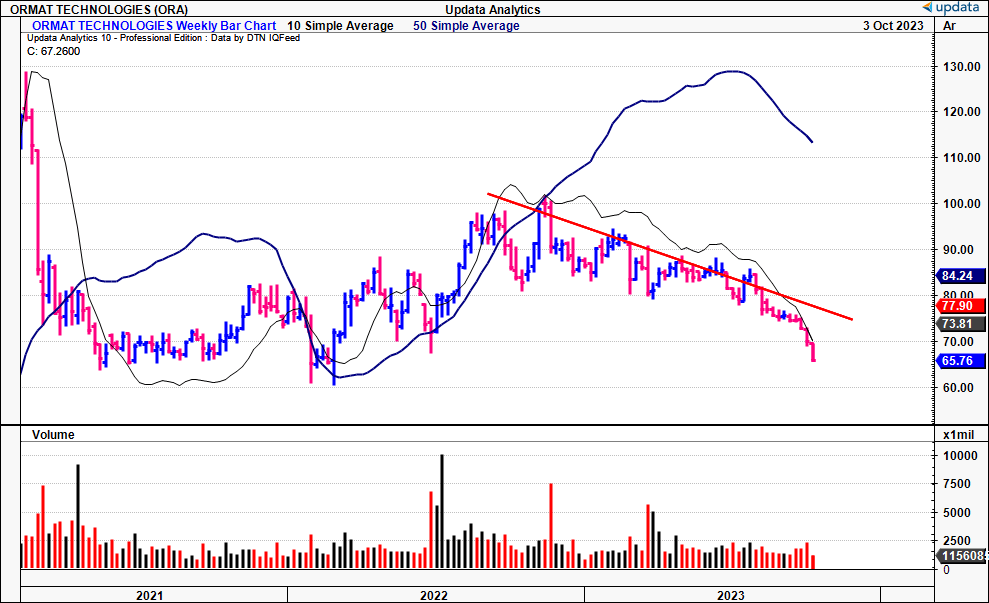

Figure 1. ORA 3-year price returns, weekly bars—little-to-no value creation over this time. ORA's business economics corroborate this view.

{kind=link}

Critical facts pattern supporting hold thesis

1. Recent developments

- Key updates

Last month, ORA confirmed it had signed new contracts to construct a 56MW geothermal plant in New Zealand ("NZ"). It signed the contract with Mercury NZ Limited, the 3rd contract between the pair, and covers the following:

- An extension of the existing 96MW geothermal plant, built by ORA back in FY'12. It is to be built on the same platform as the existing plant.

- Once functional, it will have capacity and output of 150MW, including the Ormat Energy Converter.

- Will supply ~45% of NZ's geothermal energy market. For reference, geothermal supplies ~18% NZ's total energy, so this new site would be supplying ~9–10% of the country's total capacity.

In addition, ORA announced several updates achieved in Q2. For starters, in its electricity segment, the company signed other agreements for the construction of another 50MW geothermal project in NZ, alongside a 10MW expansion at its power plant in Guadeloupe. The company also signed a 20-year power purchase agreement ("PPA") to provide an extra capacity of 35MW at its 42MW Arrowleaf solar project, available for when solar isn't operational.

It also ORA initiated operations at 2 new battery storage facilities, the Upton project (23MW), its Andover project (20MW) and two additional sites at Bowling Green (12MW) and Howell BESS (7MW).

- Latest numbers—mixed performance down P&L, cash flows

ORA's Q2 FY'23 revenue was $194.8mm, a YoY growth of 15.2%, underscored by strong growth in its products segment. Product mix is crucial for any firm's margin + income profile. For ORA, its products business is the lower-margin business by far. So it pulled the ~$195mm in sales to gross profit of just $49.5mm, on a substantial YoY margin decline from 34.1% to 25.4%, all thanks to this mix shift at the top line.

Still, it has added 100MW of additional capacity during H1 FY'23, and management is calling for a capacity of 1.9—2GW in its portfolio by the end of FY'25. This is 70% higher than its 2022 capacity. For FY'23, management anticipates revenue between $823mm—$858mm, equating to a 12%-17% YoY increase. Of this, the Electricity segment is expected to drive revenues 7% higher and produce $670mm—$685mm, whereas its products segment is projected to grow 79% YoY, with revenues between $120mm—$135mm.

Figure 2. ORA's growth outlook into FY'25

Source: ORA Q2 Investor Presentation

There were several operational highlights worth noting:

- The firm left Q2 with a backlog position of ~$120mm. It has secured additional contracts worth $44mm secured since the onset of FY'22. With the negotiated contracts in NZ, my estimate is that backlog will be higher entering into the last 2 quarters. Further, its energy storage pipeline stood at 3.3GW of capacity at the end of Q2.

- The Electricity business grew sales 2.7% YoY to $155.3mm. This growth was driven by portfolio expansion at its CD4 and North Valley sites.

- Its Products business grew 222% YoY to $33.5mm, which constituted 17.2% of the top line Q2. The growth was primarily attributed to the higher backlog mentioned earlier.

- In contrast, its Energy Storage segment did $6mm of business, down ~$1.5mm YoY. Most of this was pricing, as the company realized lower merchant energy prices in the Pennsylvania-New Jersey-Maryland Interconnection ("PJM") area.

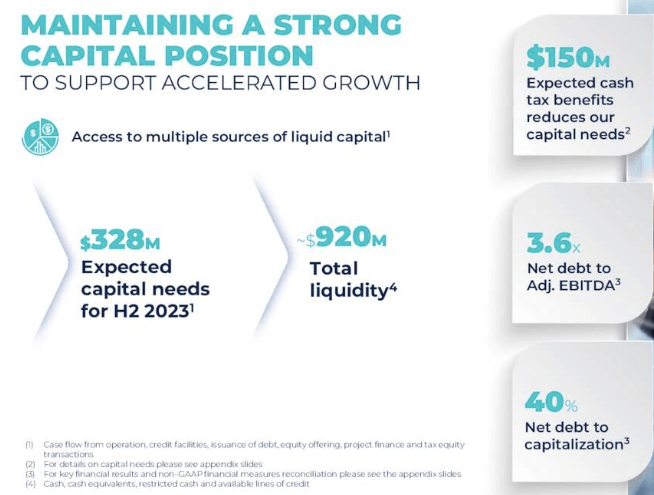

As to its investments made, ORA invested ~$247mm in CapEx in H1. The company currently holds a total of $920mm in liquidity, including cash reserves and an available line of credit. Critically, it expects CapEx of $328mm for H2, bringing its total investment to $575mm for the year. Of this, it is eyeing $35mm in pure maintenance CapEx, $446mm to its electricity segment, and $111mm and $18mm invested towards storage and products, respectively.

Figure 3. Expected CapEx + Liquidity

Source: ORA Q2 Investor Presentation

{kind=link}

2. Price implied expectations

It's fruitful to gauge the embedded expectations in ORA's current market values to see what makes sense at its asking multiples.

ORA currently sells at ~ 32x forward earnings and 31.5x forward EBIT. At the current market value of $4.21Bn, this implies an expected $2.13 in earnings per share and $133.6 in FY'23 EBIT (4,120/31.5= $133.6).

Notably, the market expects a 31% YoY growth in earnings, but a 28% decrease in EBIT from FY'22 numbers of $185.6mm, and a 27% decrease from the TTM value of $182.5mm. Consensus is also eyeing 13% sales growth in both FY'23 and FY'24.

Investors have also priced the company at 1.43x EV/invested capital. Consider that (i) EV = the market value of equity + market value of net debt, and (ii) invested capital roughly = the book value of equity + net debt. So ORA has generated a 43% total market return on its business capital. Comparing its current performance of ~5% return on capital to a 12% hurdle rate (in line with long-term market averages, representing the opportunity cost of capital), the firm's current returns on investment equate to a 0.4x multiple.

Taking the ROIC/12% ratio as a no-growth multiple, and then comparing this to the market's appraisal, it would appear any growth is well reflected in ORA's current market values, as seen in Figure 4. Further, we can obtain the market-implied ROIC from this data (1/(EV/IC)xROIC). Plugging the values in spits out an implied ROIC of 3.4% (1/(6,150/4,292)x4.9% = 3.4%).

BIG Insights

So the market's expected 13% sales growth and 31% growth in earnings is expected to produce 3.4% return on the capital ORA will have invested in the business. This presents a problem with rating ORA a buy in my opinion. Consider the following:

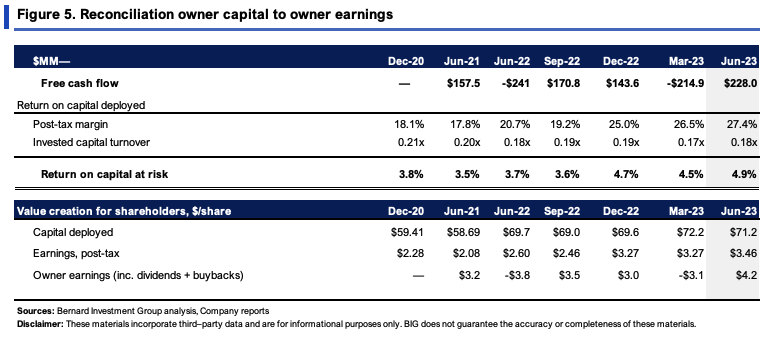

- ORA's trailing returns on capital deployed have ranged from 3–5% for the last 3 years. In Q2, it had $71.20/share invested, producing $3.46/share in trailing NOPAT.

- The business model is a reasonably high margin, low capital turnover machine and this squares off with the economics of the business (Figure 5). Being in renewables enables ORA to provide cost differentiation, as its 'products' differ from traditional energy. Hence the high post-tax margins. This is something I've noticed in covering this space, that renewables can differentiate on cost and command higher post-tax margins.

Hence, the market isn't far off ORA's current performance in its estimates, and these aren't attractive economics. The question is, do we believe the market, or is there reason to think otherwise for ORA?

Another way to think about things is what ORA's recent investment and profit patterns have been. From 2020–date, each new $1 in sales required $16 in investment to grow—$17.84 on the dollar in fixed capital and $2.25 per $1 in intangibles, but it managed to reduce its NWC requirements by $4.00 per $1 in sales growth. Said differently, $1 in sales growth took $17.84 + $2.25 from free cash flow, but $4 in free cash was generated from NWC changes.

{kind=link}

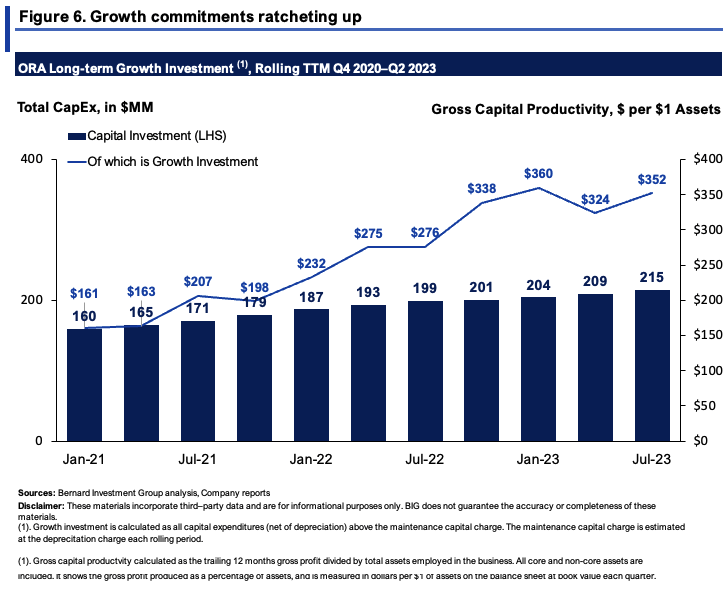

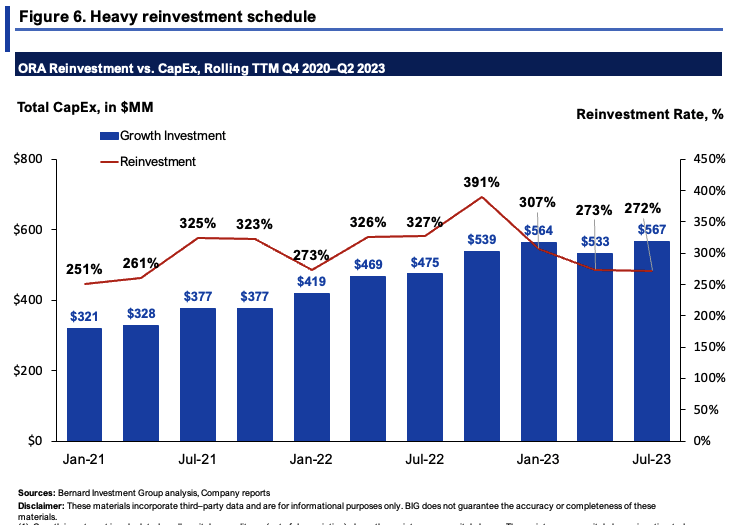

On face value, these might seem overstated. But the calculus adds up just fine. In Figure 6 you can see the firm's investment to CapEx broken into 2 parts. In the first chart, it shows the maintenance capital charge, approximated as the rate of depreciation each period, compared to the growth investment, which is all CapEx above the maintenance charge each period. Not only has ORA been investing heavily toward growth, but the amount of growth investment has increasingly expanded each period as well.

ORA has heavy investment plans moving forward too. The planned $575mm in planned FY'23 CapEx ($328mm planned for H2 '23) is more than 4.3x the consensus $133mm in FY'23 EBIT outlaid earlier. Again, this may seem excessive, but it stacks up with what ORA has been doing in recent times. The second chart of Figure 6 (seen below) shows the reinvestment rate as a function of CapEx investments made in each period since 2020 on a rolling TTM basis. The reinvestment rate is the reported CapEx over NOPAT. Clearly, the firm has been investing 250–390% of its post-tax earnings over this time—the issue to date has been, these reinvestments have been redeployed into the business at unattractive rates of return.

{kind=link}

{kind=link}

Valuation and conclusion

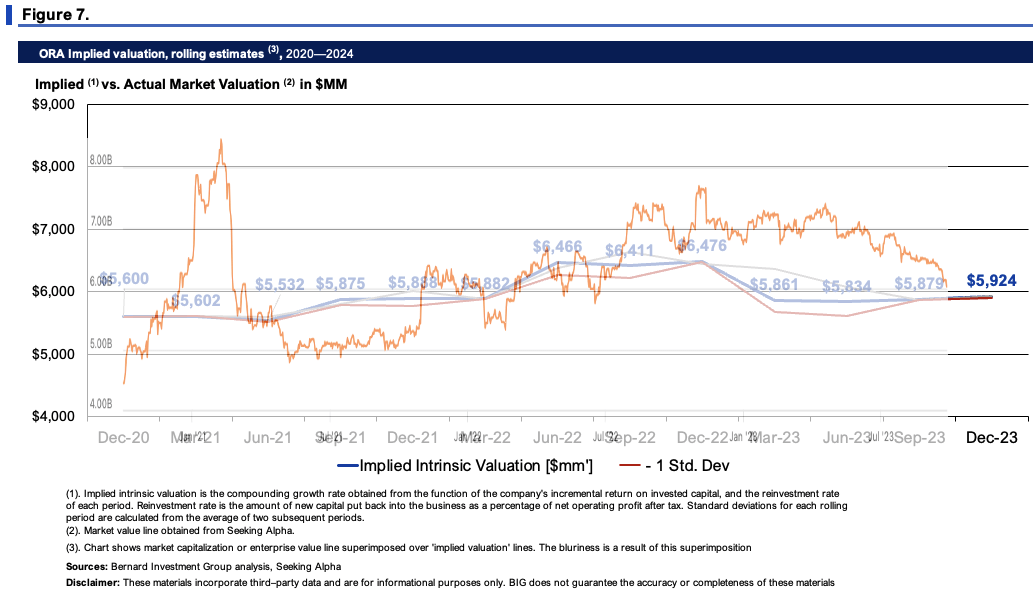

Consequently, it appears the market expects a reinvestment rate of 430% and a return on invested capital of 3.4%, suggesting it expects ORA to compound its intrinsic value by 14.7% (4.3x0.034 = 0.147). This appears fair in my estimation, and my numbers point to a 4.1% ROIC and similar reinvestment rate, arriving at a current EV of ~$6Bn, just below the market's $6.15Bn EV (Figure 7). By best estimation, the current market value reflects three key principles:

- That ORA's earnings rate on capital is not economically valuable, below a threshold margin that reflects market rates (12% here).

- Therefore, despite the financial growth expectations, this growth is unlikely to create shareholder value given these economic characteristics. It may even be erosive to value.

- Consequently, the market has repriced ORA's EV to a level that reflects both the earnings and assets employed to run its business.

Based on the calculus presented here today, there is no major reason to disagree with the market here. It would appear that it has been an accurate judge of fair value, and captured the moving parts feeding into ORA's valuation. This supports a hold rating in my best estimation.

{kind=link}

In short, ORA presents with a number of interesting characteristics. This is a reasonably high margin, low capital turnover business, with cost differentiation and consumer advantages given its presence in renewables. But the reinvestment requirements to grow sales + earnings is obscenely high in my view. This would be acceptable if the rates of business returns were high and above a comparable market rate. That's not the case, however. All ORA's FCF must be ploughed back into the business at sub-par rates of return. So we have a situation where 1) no cash is left for shareholders, and 2) what cash is produced must go back into the business, only to throw off modest rates of return on the firm's capital. Net-net, these factors support a hold rating in my view.

For further details see:

Ormat Technologies: High Earnings Not As Attractive Compared To Capital Required To Grow