ORA - Ormat Technologies: Promising Future But Valuation Is Worrying

2023-06-09 07:09:20 ET

Summary

- Ormat Technologies has established itself as a major player in the geothermal energy market, but its current valuation of 44x forward earnings is too high for a comfortable investment case.

- The company has shown strong growth, with net income growing by 57% YoY, but risks include negative levered free cash flow and continuous share dilution.

- A more attractive investment option could be Clearway Energy, which offers more safety and less downside risk, but holding onto ORA shares could still be beneficial in the long run as the shift toward renewables continues.

Investment Rundown

Getting exposure to geothermal energy generation could be very beneficial seeing as the market is expected to grow quite rapidly . Ormat Technologies Inc (ORA) has been taking strong steps to secure and establish itself as a major player in this market. With establishing the plants and securing contracts internationally ORA has grown its revenues and earnings impressively over the last few years. This has led to the share price running up a fair bit and with a p/e of 44 on a forward basis right now it is too high for my liking to comfortably make an investment case. I see them having strong potential but I would much rather buy at a lower valuation, somewhere around 20-25 seems far better and presents less downside risk too. For me, ORA is a hold as it still has potential, but the current price is too high to pay, even if the growth has been strong.

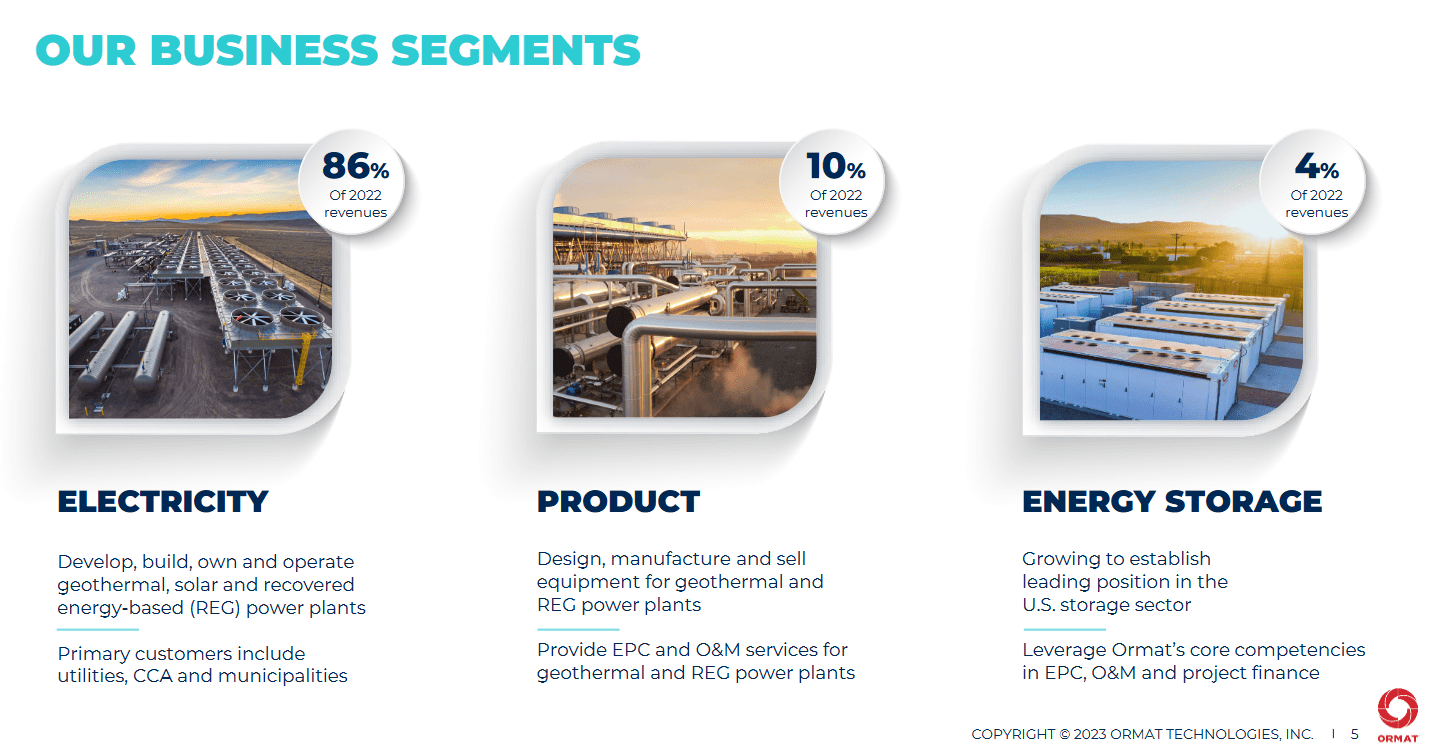

Company Segments

The company has three segments in the business and the largest one being the electricity segment, which is responsible for 86% of the total revenues in 2022. Besides that however the company has the product segment and lastly the energy storage, with the last one being very intriguing and interesting to me, as I see that market growing rapidly over the next few decades as we strive to decrease emissions and maximize our output potential and also preserve what we produce.

{kind=link}

Over the years, ORA has managed to diversify its largest segment very well and now has 27% of revenue coming from international customers, and the rest being in the US. In the geothermal space, ORA has managed to grow into the second-largest owner and operator. Despite having already installed 16GW of geothermal capacity, ORA sees there is a 9x global potential still out there, compared to what has already been installed. That leaves a lot of growth for ORA still.

Market Position (Investor Presentation)

Some of the markets ORA is entering are most notably in the Indonesia market, which is the largest economy in Southeast Asia. Looking at the energy storage market, ORA sees strong tailwinds emerging in the US, most notably in California and Texas. I think this is an exciting space to enter as the necessity and demand are already very strong and it could help a crucial role in our mission to reduce reliance on non-renewable energy sources.

Earnings Highlights

Looking at the last earnings report you might quickly realize why the company is trading at the valuation it does. The net income grew by 57% YoY which certainly makes ORA a growth company right now. With growth like that, you often associate it with a higher p/e, which for ORA is 44x forward earnings right now.

Earnings Breakdown (Earnings Report)

Looking closer at the margins for the quarter it is slightly worrying seeing the energy storage segment making a steep decline. Going from 13.5% in 2022 to negative 3.6% is not the development I want to see. To be fair though, it is capital-intensive to enter that industry and become established. Going into future quarters, however, if the share price should be able to stay at the current level, there needs to be an improvement here. Otherwise, I fear the downside risk is quite large as a value compression would be necessary to reflect the lower growth potential of the company.

2023 Guidance (Investor Presentation)

Looking at the guidance from the company, they see the revenues growing around 14% YoY, which isn't really enough to justify paying 6x forward sales . What is comforting here is the strong margins the company sees they will maintain. That will help them keep debt somewhat under management. But I fear that if they see headwinds resulting in lower margins, the company looks rich on other metrics than just the p/e. The net debt/EBITDA sits at 3.7 right now which I find too high. Under 3 is my preference, as it would indicate the company won't be likely to dilute shares in order to raise capital for debts, as the EBITDA would be enough. Seeing strong demand and margin expansion in the next quarters of 2023 will be very important to not make investing in ORA too risky at current prices.

Risks

Regarding ORA, I find the biggest risk facing investors is the valuation right now. With 44x forward earnings, an unfortunate disappointment in a report could send shares sliding. The company isn't really trading based on fundamentals. They have a negative levered FCF in TTM, but what is more worrying is that the levered FCF has been negative for the last 7 years. That makes share dilution very likely and so far that has been true for ORA as shares outstanding have grown by around 10% in the last 5 years. Not the development you want to see if you are considering them as a long-term investment. Improvements will need to happen in order for ORA to present less risk to investors. Reaching positive cash flows is a first step, which hopefully will be possible if they can continue growing and streamlining their electricity segment.

Final Words

As has been mentioned throughout the article already, the valuation of ORA right now seems too high to justify a buy case. The company has proven itself able to grow substantially, with EPS growing 54% in the last quarter alone. But with guidance suggesting a 14% YoY growth in revenues for 2023, I think investors will be left with a richly valued company operating in a capital-intense market where margins aren't that easy to increase. Apart from that, shares are being continuously diluted, and distributing a dividend when FCF is negative seems irresponsible to me.

I still see ORA benefit in the long run from the established market position as the shift towards renewables won't be slowing down, but rather increasing instead. What would need to happen for me to change my hold rating to a buy would be a valuation somewhere around 20 - 25x earnings and positive cash flows. Skipping out on the dividend to preserve capital seems like a good first step also. Perhaps a more intriguing option right now to investors would be Clearway Energy Inc (CWEN) as they have superior margins to ORA and positive FCF. Benefiting from similar trends, CWEN offers more safety and less downside risk compared to ORA right now in my opinion. Nonetheless, in 10 years' time, I don't think you'd be disappointed holding onto shares in ORA.

For further details see:

Ormat Technologies: Promising Future, But Valuation Is Worrying