OSCR - Oscar Health: Decreasing Memberships Is Worrying

2023-09-21 20:38:53 ET

Summary

- Oscar Health's share price has plummeted since March 2021, with a decline in memberships and lack of profitability.

- The company operates as a digital health insurance platform, focusing on the Affordable Care Act marketplace.

- The valuation of Oscar Health is a concern, with negative earnings and significant share dilution. The company faces inherent risks in the health insurance sector.

Introduction

Looking back since March 2021 the share price for Oscar Health, Inc. (OSCR) has plummeted. The highs were around $35 and now the company is nowhere near that. I think that the company looked too optimistic and the price has compressed as a result. The last report did show a fantastic improvement in the EBITDA which now is positive at least at $35 million. Last year it was a negative $75 million instead. But where there were some improvements, there were also some negatives as the total memberships declined on a YoY basis. This is certainly very worrying and speaks quite well about the current situation of the company and how important it is for them to raise memberships rather than see them decrease.

Since the last report back in early August this year the share price has declined by around 20% and I think we are likely to head even lower. Because of the lack of profitability of the company as well, I will have them as a sell for now.

Company Structure

OSCR operates as a digital health insurance platform, leveraging artificial intelligence to effectively match individuals seeking insurance coverage with the most suitable health plans, with a primary focus on the Affordable Care Act (( ACA) ) marketplace. The company's innovative approach aims to streamline the insurance selection process and enhance access to affordable healthcare options for its customers.

The company provides a range of insurance options, including Individual and Small Group plans, as well as Medicare Advantage plans. Additionally, OSCR offers +Oscar, an innovative technology-driven platform aimed at facilitating the transition of healthcare providers and payors toward value-based care models. In addition to its insurance offerings, the company also provides reinsurance products to further diversify its services within the healthcare industry. This comprehensive approach underscores OSCR's commitment to delivering innovative solutions across the healthcare spectrum.

Income Statement (Earnings Report)

Even though the company has been around for some years, it could not raise the bottom line to a profitable level. The last report did show some decent results as the net loss narrowed to negative $15 million, compared to negative $112 million 12 months earlier. Operating this heavily increased though, even faster than the premiums the company earned. This was a result of the lower memberships the company had for the quarter and is one of the most important factors to look at coming the Q3 and Q4 earnings reports.

Long-term debts sit quite still at $298 million for the company so it hasn't been that affected by the rising interest rates as the rate seems to have been set before rates went up. This should provide some stability to the bottom line, in my opinion, at least for now.

Earnings Transcript

OSCR is still very much a speculative company, or at least I think so as long as the bottom line is negative. From the last earnings call the CEO Mark Bertolini helped shed some light on the recent performance and where the company is heading right now too.

As we look to next year, we plan to maintain a disciplined pricing strategy that we believe appropriately targets both growth and margin expansion. Our growth strategy for 2024 focuses on leveraging the breadth of our deep provider partnerships to expand into more rural areas. We are planning to increase our service area footprint in more than half of our current states, which would meaningfully increase our overall TAM next year”.

OSCR is still very much a growing company and I think they need to continue taking steps like this to grow and justify any form of valuation. If they can broaden their TAM rapidly then I think the memberships could grow very well organically and the cost of acquiring new customers will be lower. That will likely bring stronger earnings growth as the expenses are lower.

On the margin side, we have identified increased benefits from our total cost of care initiatives in areas including the PBM and fraud waste and abuse efforts. We expect to drive further administrative cost savings from our increased scale and overall efficiencies from our technology. Most importantly, though, we are expanding our innovative and affordable product offerings to continue providing an member experience”.

With a lot of growth companies, I think you often see a management team that is just focused on growing the top line and then focusing on the margins later on instead. Seeing OSCR at least admitting right now that margin expansion is a key issue for them is bringing some reassurance at least. I think however that until we see otherwise, OSCR will remain to be a sell. The downside risk is quite high as long as they post negative earnings and are forced to dilute shares rapidly to raise capital and pay down liabilities.

{kind=link}

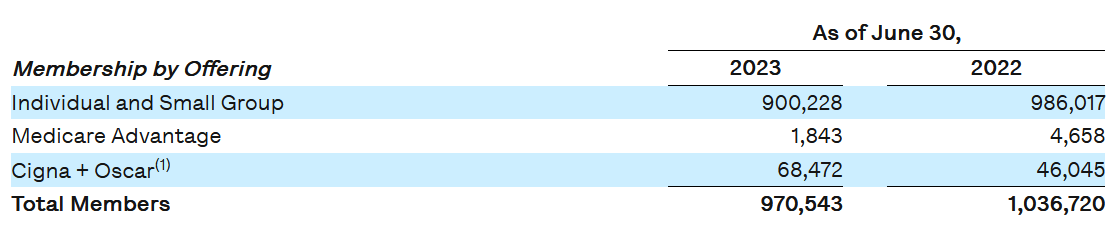

Looking above here we can see a pretty scary trend in that OSCR is losing memberships quite quickly. YoY it's down nearly 7%. In times with higher inflation and interest rates perhaps some are trying to save where they can and that has meant a downtrend for OSCR. Should this continue I think that the valuation of the company has to compress as the earning potential decreases. Just looking at the revenues for the company last quarter, they were over $1.5 billion, a 48% increase. This may go against my saying that decreasing memberships is harming growth. But what we need to look at is the significant amount of ceded premium OSCR had in Q2 FY2022, over $373 million. This skews the results to show an increase of just 9.4% instead. Perhaps a decent sign that OSCR can charge higher premiums and still have a membership base, but I don't think it is a trend that can continue for too long until the membership decreases start to pick up the pace even more.

Valuation & Comparison

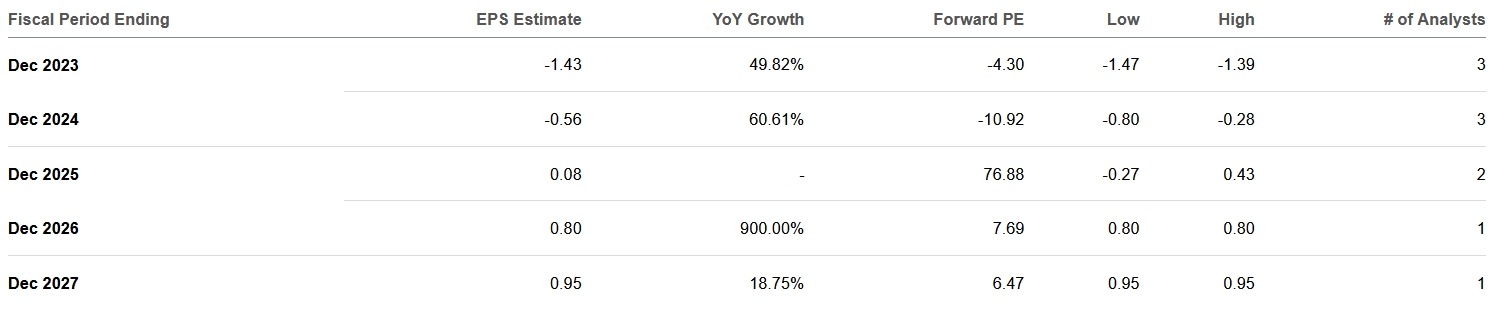

My biggest concern with OSCR is the valuation right now. Without any profitability, there aren't any solid fundamentals for the share price to trade on, unfortunately. The market anticipates the first positive EPS in 2025 and for that year OSCR trades at a p/e of over 70. By 2026 that goes down to 7.6 instead though.

{kind=link}

EPS Estimates (Seeking Alpha)

I am quite special in this type of growth as the margin expansion necessary is quite an undertaking. I do think that OSCR can grow its top line very well though if they expand their TAM even further. Nonetheless, though, OSCR exhibits a lot of risks as long as the EPS is negative and the share dilution practices continue the way it does. As a reference in 2020, the outstanding shares were 25 million. Now they are over 216 million. That has helped decrease the share price significantly in my opinion.

Risk Associated

Factors such as risk scores and their associated adjustments, unexpected developments at the state level (potentially leading to a withdrawal from a key market like California), and the ever-evolving landscape of regulations and market dynamics collectively contribute to the complexity and challenges associated with investing in this particular stock. Staying vigilant and well-informed about these multifaceted variables is crucial when considering an investment in this company.

Operating Expenses (Seeking Alpha)

Given that OSCR primarily operates as a health insurer, the company faces inherent risks within this sector. One notable risk scenario is the potential for OSCR to experience margin compression and increased expenses should the cost of healthcare rise beyond its initial projections. An essential metric to monitor in this context is the company's medical loss ratio, which is anticipated to fall within the range of 82% to 84% for the current year. This metric serves as a key indicator of how efficiently OSCR manages its healthcare expenses relative to its premium revenues.

Investor Takeaway

Insurance is not an easy industry to navigate. OSCR has seen strong net premiere increases but a decline in membership. If the latter is a trend that continues I think the share price for OSCR is going a lot lower. Growth is key for the company as it aims to expand the TAM it has in the US. Lacking profitability and significant share dilution makes this company a sell for now though.

For further details see:

Oscar Health: Decreasing Memberships Is Worrying