OSCR - Oscar Health: Q3 Earnings Suggest Growth Can Continue Into 2024

2023-11-14 23:30:00 ET

Summary

- Oscar Health's stock has seen significant >100% growth since March this year but remains discounted to its IPO price by ~80%.

- The company has exited the Medicare Advantage market and focused on the Affordable Care Act markets.

- Oscar's Q3 earnings showed positive improvements, with increased premiums and a decrease in the medical loss ratio. The company has upgraded its guidance for FY23.

- Under its experienced, recently appointed CEO, the focus has been on profitability as opposed to growth, and a move into the Medicare Advantage - where Oscar previously experienced difficulties - is mooted.

- With ACA rules possibly set to change after 2025, there is uncertainty around the future viability of Oscar's business model, but the market will likely be seduced by 2024 performance and drive Oscar's valuation higher.

Investment Overview

I last covered Oscar Health ( OSCR ) in a detailed note for Seeking Alpha back in March this year, giving its stock a "Buy" recommendation - shares are up >100% since.

Oscar announced its Q3 earnings one week ago on November 7th, reviving the share price, which had been flagging since a bull run that began in April, and lasted until mid-June, reaching a peak of $10. Although performance has been strong year-to-date - shares are up >170% - the current price still represents a discount of >80% to Oscar's March 2021 IPO price of $36, which valued the company at >$7bn.

As I explained in my last note , as a relatively new market entrant in the fiercely competitive health insurance market, Oscar's technology-first approach ran into numerous challenges, most notably in the Medicare Advantage ("MA") business, arguably the most prized market for giants such as UnitedHealth ( UNH ), CVS Health ( CVS ), and Humana ( HUM ) due to its growth and profitability. Oscar opted to exit its MA businesses in New York and Texas at the end of last year, favouring the individualised Affordable Care Act ("ACA") markets. According to a statement in Oscar's latest annual report / 10K submission:

For the years ended December 31, 2022 and 2021, approximately 99%, and 98%, respectively, of our revenue was derived from sales of health plans subject to regulation under the ACA, primarily comprised of policies directly purchased by individuals and families and secondarily comprised of policies purchased by small employers and provided to their employees as a benefit

During the years ended December 31, 2022 and 2021, the direct policy premiums of approximately 85% and 73%, respectively, of our members were subsidized by APTCs (advanced premium tax credits).

Oscar recorded net losses of $(407m) in 2020, $(571m) in 2021, and $(610m) in 2022, which is clearly unsustainable over the long term, although not untypical for a new market entrant trying to establish itself and maintain a strong growth trajectory.

Oscar continues to be a cash-rich company, with ~$3bn of current assets, including ~$1.4bn in cash and >$1bn of short-term investments, meaning it can absorb losses, although across the first nine months of 2023, net loss has shrunk significantly year-on-year, to $(121m), versus $(380m) in 2022, and the company says it expects to be profitable on an adjusted EBITDA basis in 2024.

Back in March, it was relatively straightforward to make the bull case for Oscar's stock price, as the company's valuation represented only 20% of its available cash, losses were gradually easing, and past mistakes were being rectified - after this year's gains, however, does Oscar remain a "buy" opportunity, or would a "hold" or even a "sell" recommendation be more appropriate? In this post I will try to answer that question, beginning with a review of Q3 earnings.

Oscar Health - Q3 Earnings Review

There were certainly a lot of positives - and some negatives - that can be taken from Q3 earnings.

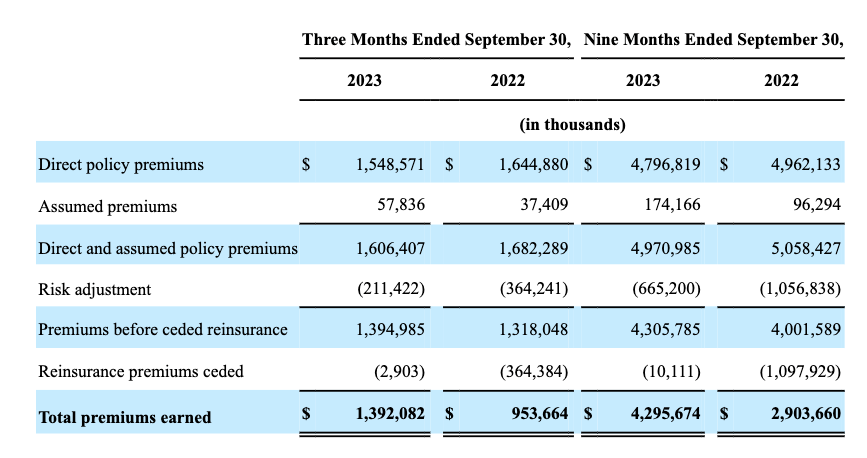

Oscar Health 2023 to date earnings overview (10Q submission )

{kind=link}

As we can see above, direct and assumed policy premiums actually decreased year-on-year, and overall membership also fell, from 1.08m total members, to 983k members, the vast majority of whom were individual and small group members, with Medicare Advantage members falling to 1.8k, and Cigna+Oscar, a co-branded partnership with the health insurance giant Cigna ( CI ), showing an increase from 53k members, to 69k members.

The shrinking membership number shouldn't necessarily be taken as a negative, however, as, according to the company's Q3 10Q submission:

the Company requested that regulators limit its membership growth in Florida above a certain threshold so that total membership across all markets would be within its previously announced target range of 900,000 to 1,100,000 members at the close of Open Enrollment.

Florida is Oscar's largest market, ahead of Texas, Georgia, and California, but the company hit pause on enrollment in the state owing to "capital and surplus requirements, escrows, or contingency guarantees" i.e. finances and infrastructure that must be in place to allow for further growth. The temporary halt was lifted on November 1st, however, implying that membership growth is likely going to rise substantially heading into 2024.

Thanks to more favourable risk adjustment figures, total premiums earned increased by ~46% year-on-year, to $1.4bn, and across the first nine months of 2023, by 48%, to $2.9bn. The medical loss ratio ("MLR") - a key measure for insurance companies, which is essentially the percentage share of total health care premiums spent on medical claims, also fell year-on-year, to 83.8%, a >600 basis point improvement year-on-year. Across the 9-month period, the MLR fell to 80%, versus 83.2% in the prior year period.

Oscar made an adjusted EBITDA loss of just $(20.3m), versus $(160m) in the prior year, and across the 9-month period, adjusted EBITDA was actually positive, at $66.4m, versus $(273m) in the prior year period.

In summary, by most measures Oscar had a good quarter, and indeed a good 2023 to date, with tangible improvements in most areas, and a good excuse for falling membership, which ought to resolve itself going into 2024. The company significantly upgraded its FY23 guidance, to $6.4bn - $6.6bn of policy premiums, an MLR of 82-84%, and adjusted EBITDA loss of $(60m) - $(50m), above the high-end of the prior range of $(175m) $(75m). The market bought into the good news story, sending Oscar stock up >40% across the past month.

Appointment Of Veteran CEO A Smart Move By A Maturing Company

In my last note on Oscar I was a little critical of the company's startup mentality and belief that technology had the power to "disrupt" the health insurance landscape. The reality is that healthcare and disruptive technology have traditionally made for uneasy bedfellows, and almost every company that has tried to ignite a "telehealth", or "virtual care" revolution has fallen flat - Teladoc Health, Inc. ( TDOC ), Bright Health Group, Inc. ( BHG ), UpHealth, Inc. ( UPH ), and American Well Corporation ( AMWL ), Ontrak ( OTRK ), Babylon Health (now almost bankrupt), for example, all of whom have experienced devastating share price losses.

In Oscar's case, however, the company took the wise decision (in my view) at the end of March to appoint an industry veteran, in Mark Bertolini, formerly Chairman and CEO of Aetna Inc., the health insurance giant purchased by CVS for ~$78bn in 2019, as their new CEO, with co-founder Mario Schlosser transitioning to Head of Technology.

The combination of a grizzled veteran who understands the complexities of health insurance markets, and knows that the likes of UnitedHealth, and Elevance Health ( ELV ) will make mincemeat of an inexperienced tech startup trying to muscle in on their territory, and a technology whizz who can streamline processes in the background and focus on making it easier for individuals to find their ideal health insurance plan, seems a much more sensible arrangement than the previous modus operandi, which had the veteran on the outside, and the tech whizz leading the company.

According to an interview Bertolini gave to CNBC , discussing Q3 earnings, the new CEO has applied the brakes to the breakneck growth the company experienced in 2021 and 2022, "so that we could get the organisation in shape and be able to move towards profitability and to expand its lines of business."

It is interesting to note that the ACA market opportunity is somewhat uncertain beyond 2025 - according to Oscar's latest quarterly report:

The ACA also established significant subsidies to support the purchase of health insurance by individuals, in the form of advanced premium tax credits, or APTCs, available through Health Insurance Marketplaces. The American Rescue Plan Act (ARPA) added additional APTCs for individuals at every household income level for 2021 and 2022; those additional APTCs have been renewed for three years through 2025 under the Inflation Reduction Act of 2022.

With Oscar being pretty much all-in on ACA at the present time, there will inevitably be a significant question mark over what happens after 2025 - as the company puts it:

the future elimination or reduction of APTCs or other subsidies could make such coverage unaffordable to some individuals and thereby reduce overall participation in the Health Insurance Marketplaces and our membership.

During his interview with CNBC, Bertolini suggested that "being just in the ACAs is a bit problematic", although he promised 20% membership growth in 2024, or ~500k "more lives that we can serve this year", and a 20% uplift in revenues in 2024, whilst insisting that the ACA market is "here to stay", and that "it will have 18.8m people in it next year." The CEO also endorsed the tech-first approach, adding "we think the whole market ought to be individual and digitised."

Unsurprisingly, however, given his experience and previous role at Aetna, Bertolini wants to see Oscar back in Medicare Advantage. the likes of CVS have made massive bets on Medicare Advantage - the fastest growing sector of the market, expected to account for >50% of total Medicare enrolment by 2030 - investing heavily in M&A to acquire firms that offer "value based care" services, with a focus on achieving better outcomes for patients, at a lower cost. Bertolini told CNBC:

allowing the people providing care to provide the service as well is a really powerful idea.

That is value based care in a nutshell, albeit looked at from the perspective of the care provider, rather than the insurer, and it is not surprising that the ex-CEO of a giant like Aetna sees most value in this market - but will this bring him into conflict with Oscar's board and management, who may see the company as an ACA focused, agile disruptor, already badly burned by MA?

In my view, Oscar's future direction and knowledge of where it can be most effective in the health insurance marketplace remains unclear, and that could be an obstacle to growth in the long term.

Concluding Thoughts - Can Oscar Complete Transition From Startup To Mature Business And Grow Its Valuation?

Oscar's business has been around since 2012, so although the company only completed its public listing in 2020, it would be (partially) wrong to view the company as inexperienced, with a disruptive startup mentality.

With its focus on ACA, however, and the APTC programme to grow membership rapidly in 2020 and 2021, the company has done what most promising startups do and grown as fast as it can, whilst taking some risks focusing exclusively on ACA, and slightly neglecting the financial side of the business. Under its new CEO, Oscar has hit pause on growth, and focused on profitability, and the company has been rewarded by the market with a growing valuation in 2023.

Today, however, the company does face an inflection point amid questions over future strategy. If there are signs that the ACA and APTC laws will change after 2025, Oscar's current business model may look vulnerable, while it will also be tough to follow the CEO's lead and target the MA markets, where the industry incumbents are dominant. A former strategy of undercutting the incumbents on price - essentially offering MA plans with no premiums to pay - appears to have backfired, with the likes of Humana, CVS and United wrestling back control.

As such, at this time, I find it tricky to make a call on whether Oscar's long-term future is secure - there are few guarantees in healthcare, when a company as large as RiteAid has recently filed for bankruptcy , and so many recently listed businesses have substantially failed to get to grips with the demands of the industry.

With that said, I do believe that Oscar's valuation can grow in the short term, based on the likelihood of profitability in 2024, a spike in membership growth, plenty of cash, few liabilities, a strong focus on innovation that is strategic rather than wildly over-ambitious, and a good blend of experience and ambition within the leadership team.

Targeting $6.5bn of revenues in 2023 gives Oscar a forward price to sales ratio of ~0.2x, which is extremely low, and although revenues without profitability is no guarantee of success (just ask RiteAid management), if profitability does arrive next year, and the short-term dynamics of the industry suggest this is likely, then Oscar's valuation has a great chance of adding to the gains made in 2023 to date.

What happens post-2025 is arguably a more troubling concern, but the market nearly always errs on the side of short-termism, and as such, whilst acknowledging the many risks I have discussed in this and my previous post on Oscar, my feeling is that I would not necessarily be surprised to see its share price up another 50-100% by the second half of next year.

The law of averages suggests one upstart insurance company can succeed where countless others fail - just look at Molina Healthcare ( MOH ), whose shares are up nearly 1,000% across the past decade - and at this moment, arguably, Oscar looks likeliest to be that company.

For further details see:

Oscar Health: Q3 Earnings Suggest Growth Can Continue Into 2024