OSIS - OSI Systems: Beneficial Guidance 2 Large New Contracts And Cheap

2024-01-18 04:29:42 ET

Summary

- OSI Systems recently reported two large contracts valued at close to $700 million, which could drive future net sales growth.

- OSIS offers significant diversification with customers in the defense, aerospace, telecommunications, and healthcare industries.

- New EU regulations and growing demand for security systems and trace detection systems could contribute to net sales growth.

Editor's note: Seeking Alpha is proud to welcome Dahlia Investments as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

OSI Systems, Inc. ( OSIS ) recently reported many new contracts , which may enhance future net sales growth. Also, with guidance including 2024 double-digit net sales growth and double-digit growth in Non-GAAP Adjusted EPS, OSIS could bring significant earnings momentum soon. Additionally, I identified other potential net sales drivers thanks to new EU regulations with regard to baggage screening systems and the growing demand for trace detection systems. Yes, there are obvious risks coming from goodwill impairments and changes in the regulations in the U.S. and Europe, however, OSI Systems seems undervalued.

OSI Systems

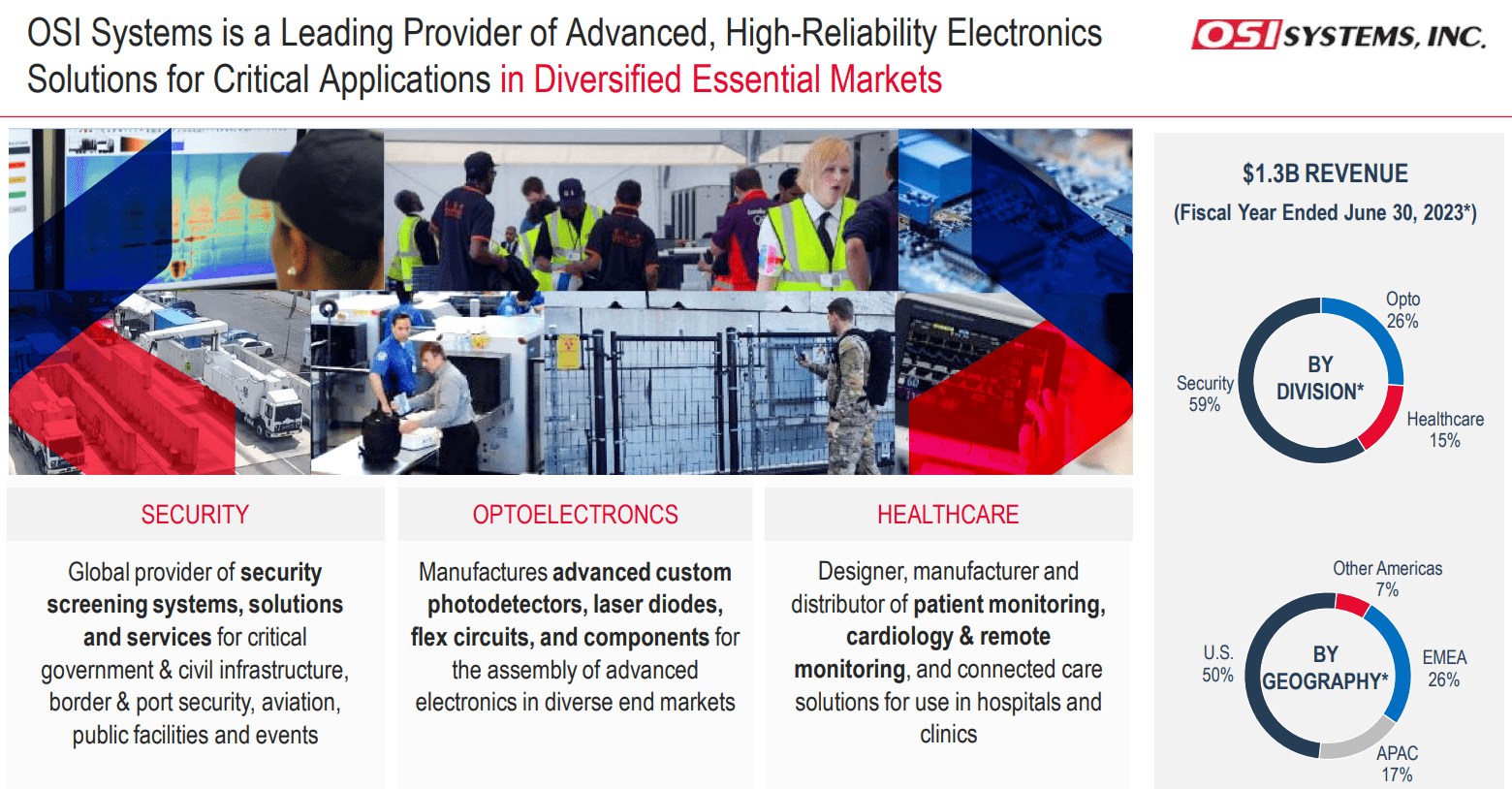

With customers within the defense, aerospace, telecommunications, and healthcare end markets, OSI Systems designs electronic systems and related components .

Operations are organized into segments that respond to each of the end markets in which their products are marketed: Security, medical care, and industrial purposes in general. The company also sells different types of components that serve the equipment or the final products of the manufacturers. With access to different industries and revenue coming from the USA, EMEA, Asia, and Pacific, I believe that OSI offers significant diversification.

{kind=link}

I believe that forecasts for these industries are currently of growth and long-term projection with regard to the increase in security systems, the complexity and technological innovation that have been developed in recent years, and the insertion of a large number of digital technologies in the diagnosis and treatment of various diseases within the medical industry. For instance, the healthcare security systems market is expected to grow at close to 5.1% from 2023 to 2032.

Healthcare Security Systems Market size reached USD 2.7 Bn in 2022, to reach USD 4.3 Bn by 2032, exhibiting a growth rate of 5.1% during 2023-2032. Source: Market.us

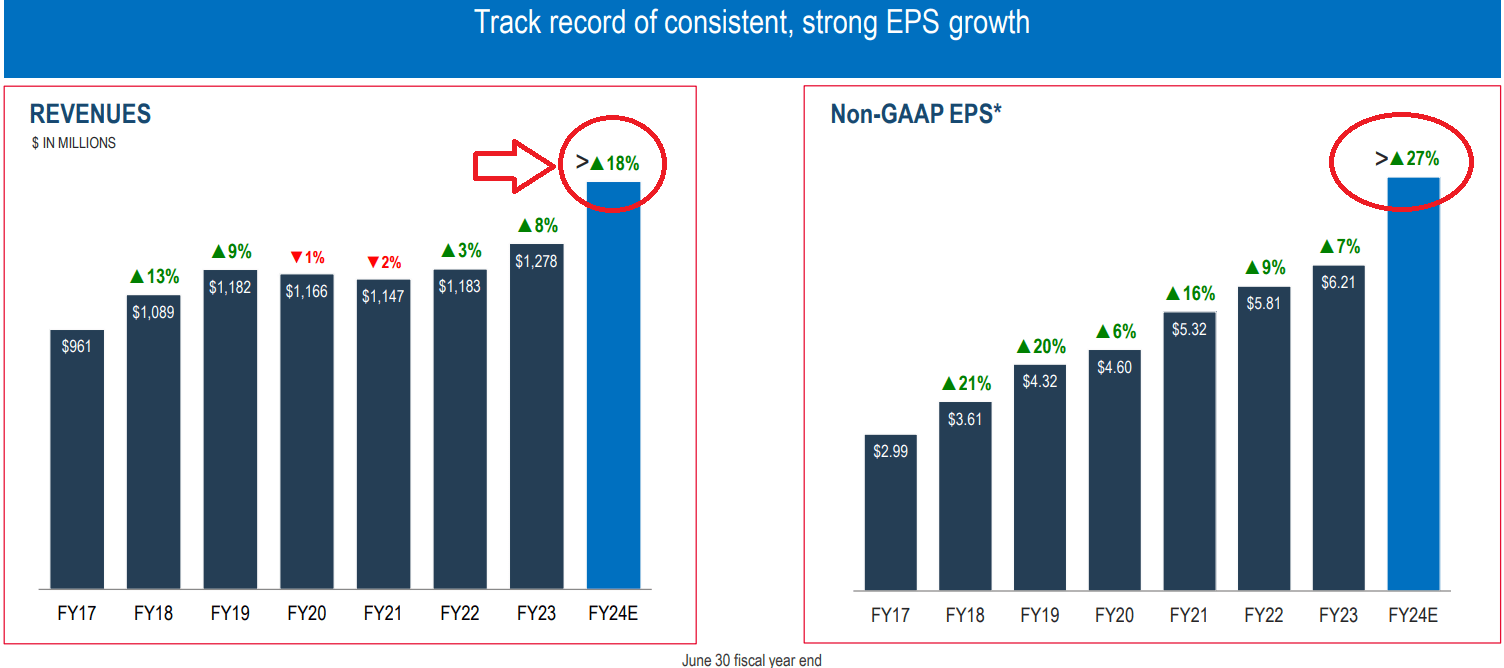

I also believe that the guidance given for 2024 is worth having a close look at. In a recent presentation, OSI promised 18% net sales growth with 27% growth in non-GAAP Adjusted EPS. With these expectations and taking into account recent backlog growth and product pipeline growth, I decided to run a financial model about OSI Systems.

Source: December Presentation Source: December Presentation

{kind=link}

New Market And New Regulations In The EU

In my view, new markets or the implementation of the available technology in the development of existing products based on the needs of other markets wherein the company has had no historical participation could bring net sales growth. Clear examples include the international aviation market opportunity for trace detection products and potential business growth from new certifications in prisons, international borders, or narcotics.

Source: December Presentation

With regard to baggage screening systems, new regulations in the EU, and new bio-security technologies needed could also bring significant net sales growth. In this regard, management prepared the following slide.

Source: December Presentation

Vertical Integration Could Be A Net Sales Driver

In the last annual report, OSI Systems notes that vertical integration differentiates the company from its competitors. OSI Systems also discussed in the previous annual report that the company offers a wider variety of technologies than competitors. I believe that these two factors may be an excellent net sales driver.

We believe that our vertical integration differentiates us from many of our competitors and provides value to our customers who can rely on us to be an integrated supplier. Source: 10-K

Although our competitors offer products in competition with one or more of our products, we can supply a variety of system types and offer among the widest array of solutions available from a single supplier. This variety of technologies also permits us to offer unique hybrid systems to our customers that utilize two or more of these technologies, thereby optimizing flexibility, performance and cost to meet each customer's unique application requirements. Source: 10-K

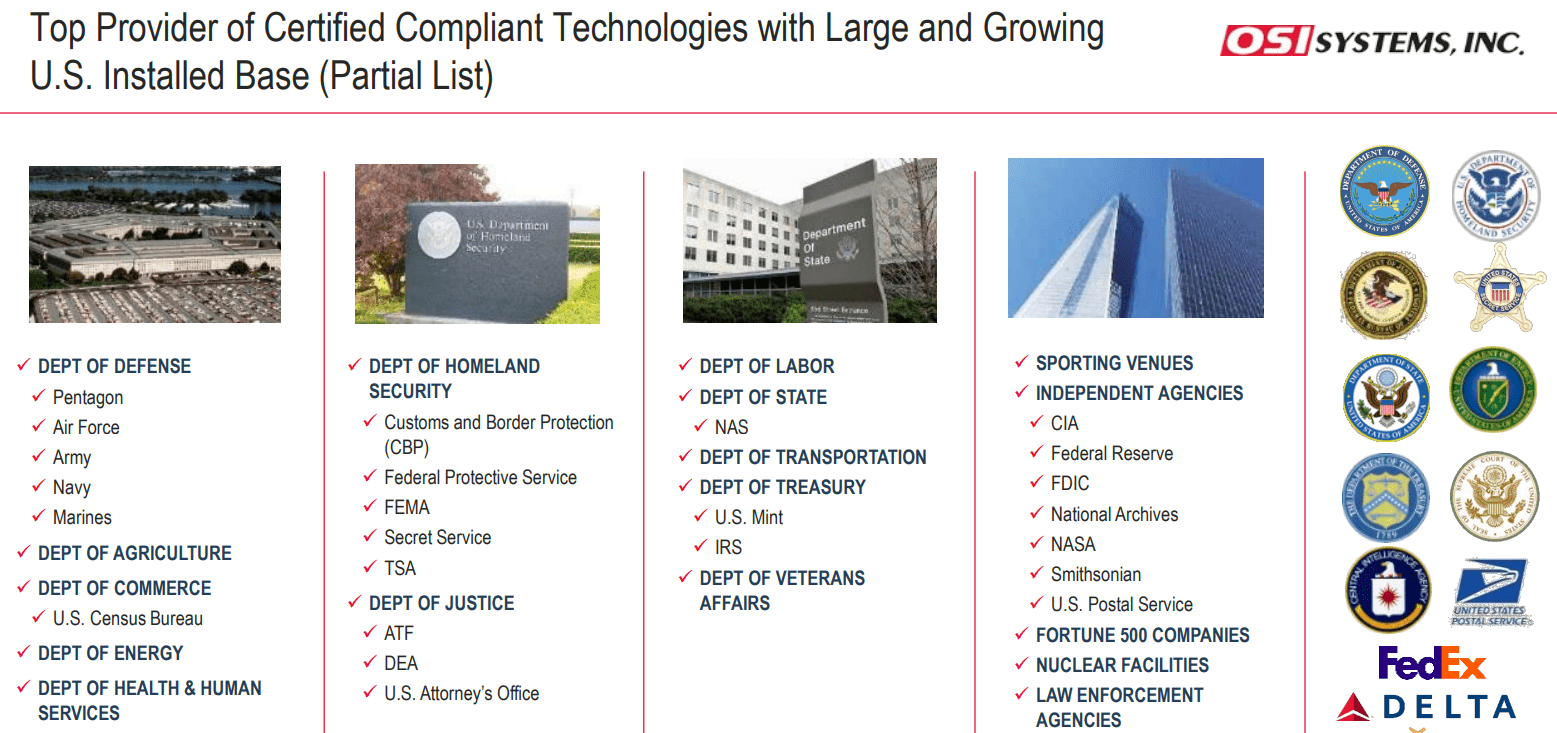

Large Clients

Regarding the security segment, the majority of clients are concentrated within the United States and correspond to the defense industries or federal institutions linked to this type of development. In my view, the United States is carrying out a modernization of its intelligence and security programs, and this transformation is a great opportunity for companies like OSI Systems.

{kind=link}

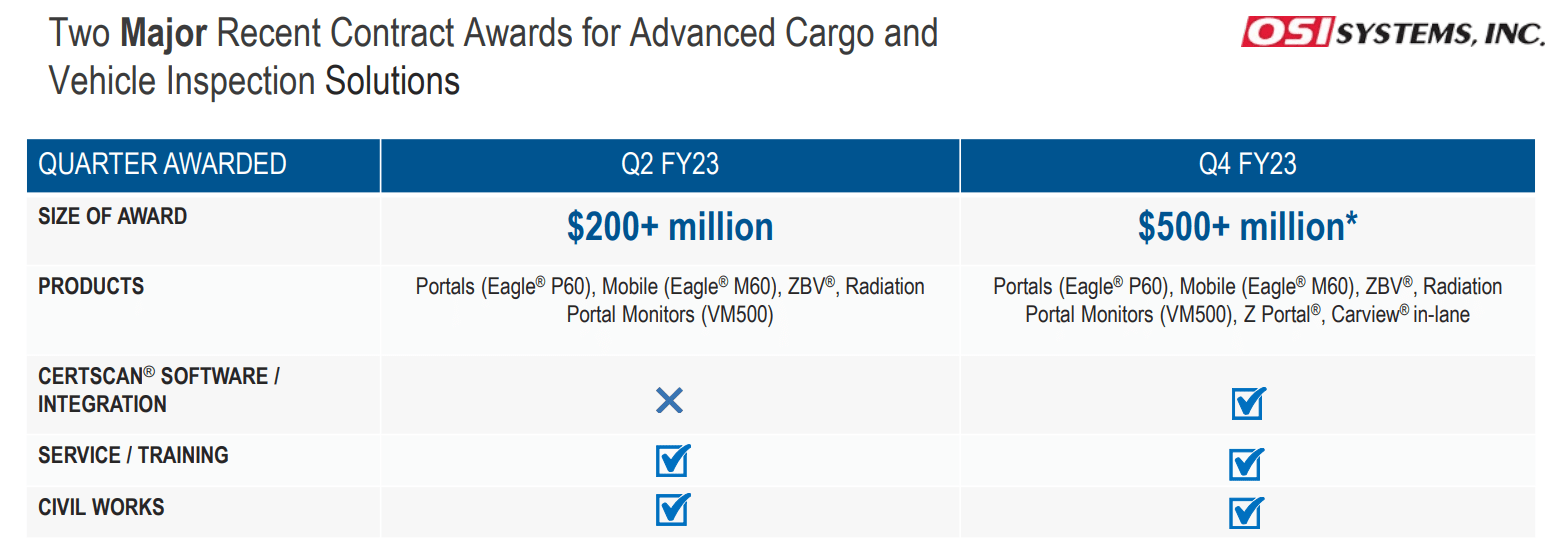

Two Major Recent Contracts

Management recently noted two large contracts for Portals, Mobile, ZBV, and Radiation Portal Monitors among other products. We would be talking about a total amount of close to $700 million, which I believe could serve as a revenue catalyst in the coming years. In my opinion, as soon as new investors see the recent increase in backlog, the demand for the stock could increase.

{kind=link}

Acquisitions In Cash, And Customer Growth

Some of the debt financing is also used to acquire other competitors. The goodwill is not small. The company acquired four targets during fiscal year 2023 and two businesses during fiscal year 2022. I did appreciate that the acquisitions were made in cash. It means that OSI does not want to use its own shares to buy companies. In my view, management may believe that its shares are cheap. You usually use your own shares when they are expensive.

In April 2023, we (through our Optoelectronics and Manufacturing division) acquired a privately held provider of engineering and contract manufacturing solutions for approximately $2.5 million plus up to $2.5 million in potential contingent consideration. The acquisition was financed with cash on hand. In February 2023, we (through our Healthcare division) acquired a privately held provider of software and solutions for approximately $2.1 million plus up to $5.0 million in potential contingent consideration. The acquisition was financed with cash on hand. Source: 10-k

It is also worth reviewing the intangibles acquired from targets. I believe that OSI acquires companies based on their patents, developed technology, software, and customer relationships. With this in mind, I believe that we could expect not only cost synergies because of the acquisitions but also net sales growth and customer count growth.

Source: 10-Q

Healthy Balance Sheet With No Liquidity Issues

OSI Systems gets paid a bit late by clients and holds a significant amount of inventory on the balance sheet. With a small amount of accounts payable, OSI uses some lines of credit and long-term debt to finance the working capital.

As of September 30, 2023, the company noted cash of about $82 million, with accounts receivable close to $323 million, inventories worth $418 million, and total current assets worth $872 million. The current assets/current liabilities ratio is larger than one, so I believe that liquidity is not a problem here.

Non-current assets include property and equipment of about $109 million, with goodwill worth $348 million, intangible assets of $140 million, and total assets of $1.588 billion. The asset/liability ratio is close to 2x. I believe that the balance sheet is quite healthy .

Source: 10-Q

I am not really worried about the total amount of debt as the FCF/Debt ratio appears quite limited. It is also worth noting that this ratio recently decreased. If OSI continues to reduce the total amount of leverage, I believe that we could see an improvement in the EV/FCF ratio and the stock valuation.

Source: Ycharts

In the last quarterly report, bank lines of credit stand at close to $235 million, with the current portion of long-term debt worth $8 million, and accounts payable of about $164 million. Besides, with advances from customers of about $31 million, the company also noted long-term debt of $134 million and total liabilities of about $863 million.

Source: 10-Q

My Revenue Growth Expectations

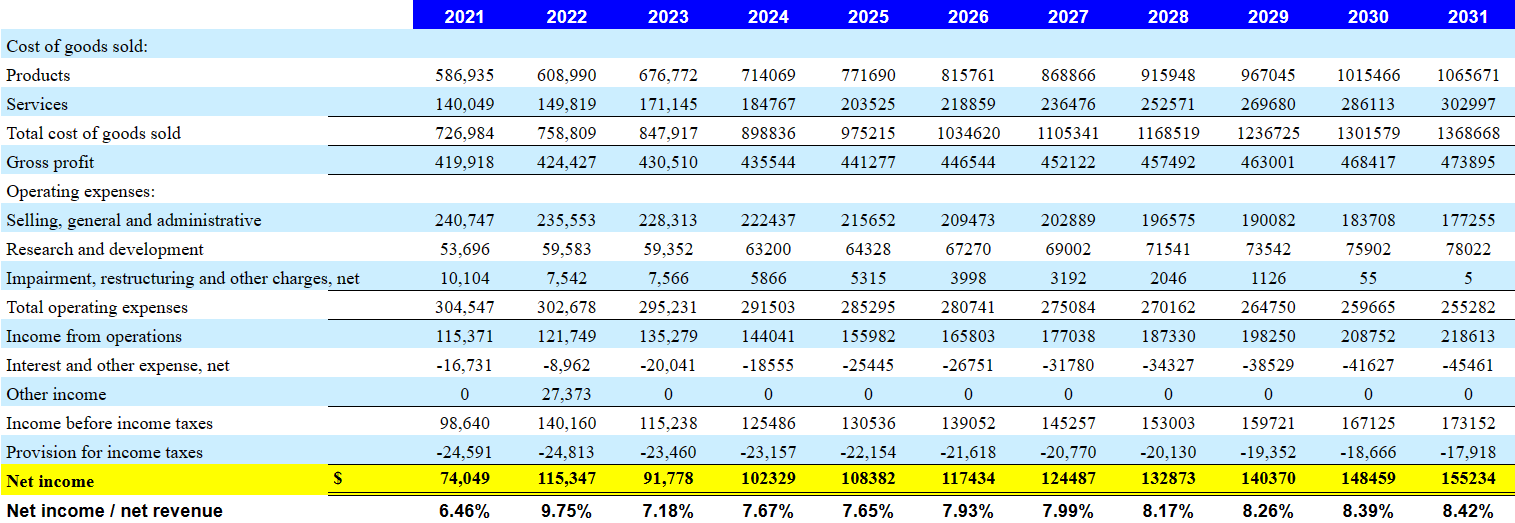

I tried to be as conservative as possible with my revenue growth figures. With total revenue growth close to 3% and 6%, I used median revenue growth of 4%. 2031 net revenue from products would be close to $1326 million, with services revenue of $515 million and total revenue of $184 million.

Source: My Financial Expectations

{kind=link}

My assumptions also included the 2031 total cost of goods sold of $1368 million, with a gross profit of $473 million. Besides, with 2031 selling, general, and administrative expenses of $177 million and 2031 research and development expenses close to $78 million, I obtained income before income taxes of $173 million. Finally, 2031 net income would stand at close to $155 million. My assumption with regard to net income/net revenue was equal to close to 7%-8%, which I believe is quite conservative.

Source: My Financial Expectations

{kind=link}

Current Trading Multiples, And DCF Model

According to OSI, the term loans and financial lease obligations include an average interest rate close to 6% and 3%. With these figures, I believe that assuming a cost of capital close to 3.77% and 8.77% makes sense.

{kind=link}

OSI Systems trades at close to 24x and 37x FCF, however the company traded at less than 17x FCF in the past. With these figures in mind, I believe that using exit multiples close to 15x and 21x FCF appears conservative.

Source: Ycharts

With the previous assumptions and FCF expectations between $48 million and $195 million, I obtained an equity value close to $1.9 billion and $3.7 billion. However, the median result was close to $2.5-$2.8 billion. The current valuation is lower than my results. I believe that OSI is quite undervalued.

Source: My DCF Model

If we divide by the share count, the implied fair price would be close to $124 and $218 per share with a median result close to $159-$179 per share. Finally, the maximum internal rate of return would be close to 9%.

Source: My DCF Model

Competition

The competition for each of the segments is high and is given by international companies that offer similar services, and in some cases have access to resources greater than that of OSI Systems. Particularly with regard to the optoelectronics and components segment for the industry, the company is one of the leaders nationally in the United States and internationally since there are no other companies that have developed such specific products for specific operations within the production chain of its clients.

Risks

Within the United States, the future allocation of budgets towards the area of ??security and defense plays a key factor since a large part of the company's income comes from its contracts with public institutions dedicated to these purposes. I believe that lower demand from clients in the United States or changing regulations in Europe or other regions could push future net sales growth down. I also think that legislation on recognition systems and the use of user and patient data could also be a matter of concern for the company.

In addition, the launch of new products and the ability to innovate according to market demand in the face of the emergence of competition are also risk factors that must be taken into account. Accumulation of inventory that cannot be marketed could also be an issue for OSI Systems.

Given the total amount of goodwill accumulated and intangible assets, I believe that future impairment could occur. As a result, I think that the book value per share and expectation of synergies could lower, which may lead to net sales expectation reductions. In the worst-case scenario, lower net sales guidance may lead to a reduction in the stock price.

My Takeaway

With two large contracts reported at the end of 2023, OSI Systems also noted a double-digit increase in net sales growth for the year 2024. This news, new regulations in the EU with regard to baggage screening systems, growing demand for trace detection systems, and bio-security technologies seem clear net sales catalyst drivers. I obviously see some risks with respect to goodwill impairments or changing regulations in the U.S., Europe, or the APAC region. With that, in my view, the company could see significant stock price improvements in the coming years.

For further details see:

OSI Systems: Beneficial Guidance, 2 Large New Contracts, And Cheap