OR - Osisko Gold Royalties: A Solid Buy-The-Dip Candidate

2023-03-07 12:32:37 ET

Summary

- Osisko Gold Royalties is one of the best-performing royalty/streaming companies, up 11% year-to-date and flat in 2022 vs. a 3%/11% decline in the Gold Miners Index, respectively.

- I attribute the outperformance to disciplined growth and considerable exploration success across its portfolio, with it set up for several record years ahead.

- A key development is the AUY/AEM/PAAS deal that increases AEM's mill capacity in the region, making Osisko the premier way to get exposure to AEM's world-class portfolio with inflation protection.

- Given Osisko's industry-leading growth, capital discipline, and superior jurisdictional profile relative to peers, I see the stock as a Buy on dips.

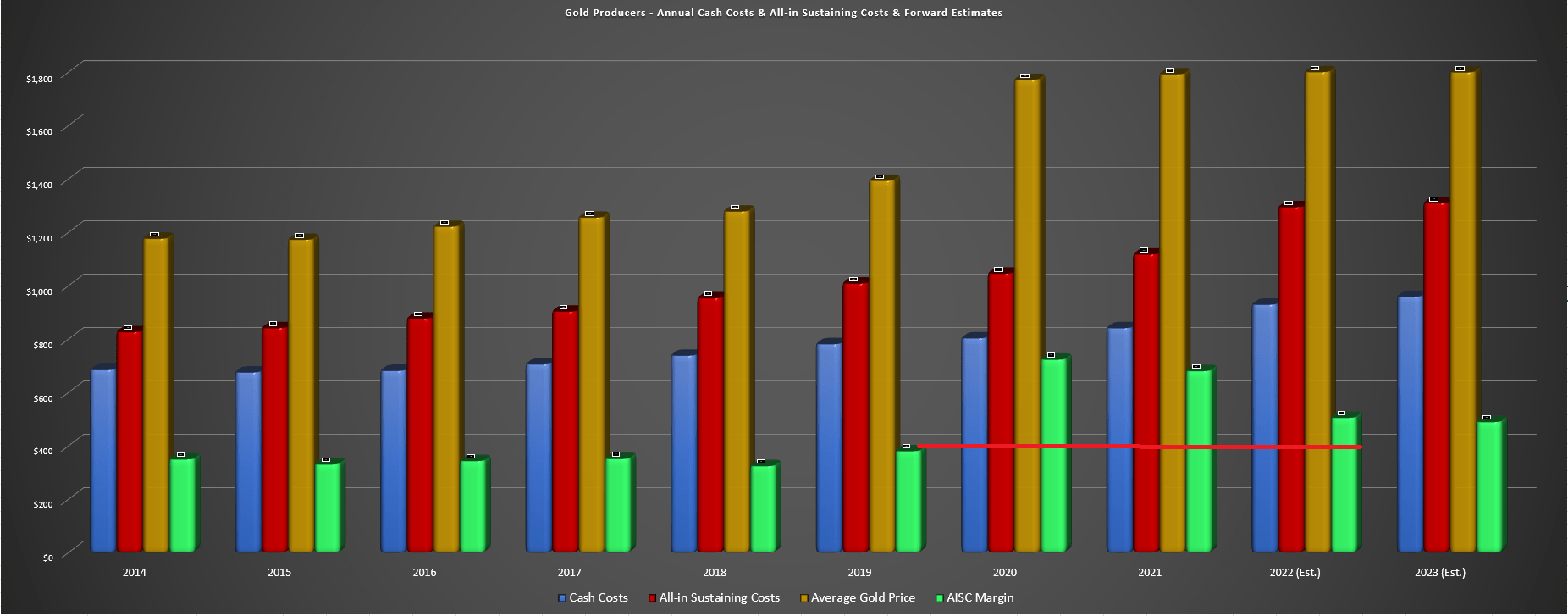

2022 was a tough year for the Gold Miners Index ( GDX ) and while several miners rallied to finish the year in the seasonally strong period, we've seen considerable gains given back since January. The poor performance on a trailing one-year basis for the producers among the GDX isn't surprising given that the majority of the margin benefit from a $400/oz increase in the gold price ($1,800/oz vs. $1,400/oz) has been eroded by inflationary pressures (fuel, electricity, labor, steel, cyanide, lime, and other consumables), with minimal margin improvement and higher share counts for many companies due to acquisitions and or capital raises to fund growth projects or pad balance sheets.

Gold Producer Universe - Annual Cash Costs, AISC, Gold Price, & AISC Margins (Company Filings, Author's Chart)

{kind=link}

Some investors have argued that the Gold Miners Index has no business trading below $35.00 when it traded as high as $45.00 in July 2020 with the gold price trading just $150/oz lower. However, I see this as a very superficial argument when we have seen meaningful share dilution among producers and even some royalty/streaming companies and margins are in much worse shape than 2020. In fact, AISC margins sector-wide declined ~30% from FY2020 (~$725/oz) to FY2022 (~$500/oz), and that is despite a slightly higher average realized gold price reported sector-wide. So, while one might believe gold producers should trade higher if the gold price is at higher levels, this argument is only valid if that benefit actually flowed through to their bottom line ( which it didn't ).

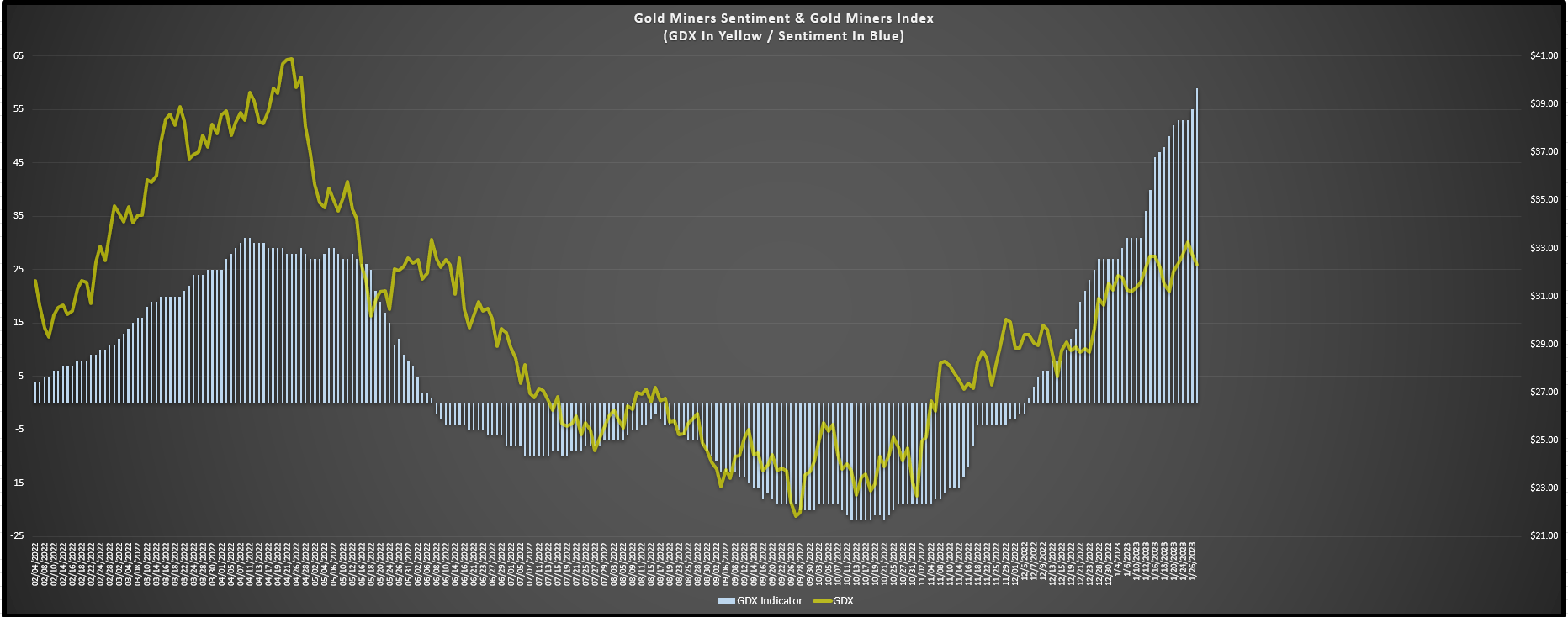

As I pointed out when I was taking profits on several positions in January and early February, I couldn't disagree more with this view because it completely ignores share dilution for most companies (with some cases of 40% plus dilution) and severe margin compression for roughly 70% of the index. To ignore this is to bury one's head in the sand and only selectively look at the data points that fit one's bullish thesis and that's a great way to guarantee underperformance long-term. In fact, despite the weaker margins and share dilution witnessed over the past twelve months, sentiment for miners (shown below) rocketed higher than April 2022 levels, providing an excellent opportunity to book some profits into strength.

{kind=link}

Fortunately, not all GDX holdings are created equal, and the royalty/streaming companies have been insulated from this severe margin compression due to their attractive business models. In fact, Osisko Gold Royalties ( OR ) put up record results last year despite the challenging year for the sector. Let's take a closer look below:

All figures are in United States Dollars unless otherwise noted. All references to "Osisko" refer to Osisko Gold Royalties.

Q4 & FY2022 Results

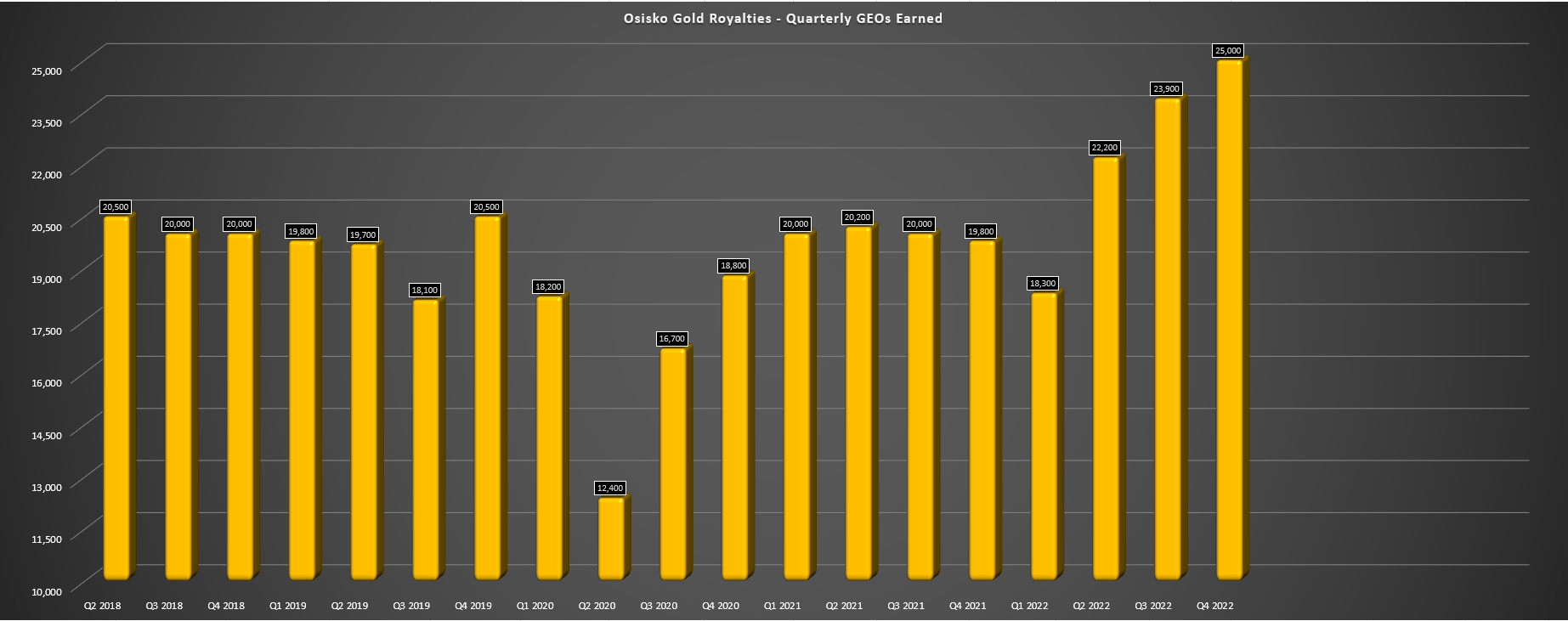

Osisko Gold Royalties ("Osisko") released its Q4 and FY2022 results last month, reporting record quarterly gold-equivalent ounces [GEOs] earned (~25,000 GEOs), record annual GEOs earned (~89,400 GEOs), and record FY2022 revenue and cash flow of C$217.8 million (9% growth year-over-year) and C$175.1 million (15% growth year-over-year). These strong results were driven by the resumption of contributions from Renard, higher production from Seabee, Island, Lamaque, and Mantos Blancos, and a solid contribution from First Majestic's ( AG ) Ermitano Mine that feeds its Santa Elena Operation. Notably, these record results were achieved despite no help from metals prices and a tough year at Eagle and a slower than planned ramp-up to 7.3 million tonnes per annum throughput rates at Mantos Blancos.

Osisko - Quarterly GEOs Earned (Company Filings, Author's Chart)

{kind=link}

While the operating results were solid with an impressive 93% cash margin, investors can look forward to new records this year as well based on guidance of 95,000 to 100,000 GEOs (6% growth at the mid-point). However, for a royalty/streaming, the real news isn't so much rear-view mirror annual results or this year's guidance, but the long-term outlook and developments occurring in real-time at partner's assets across the royalty/streaming portfolio. In this department, Osisko's partners had an incredible year from an exploration success and resource growth standpoint and Osisko will benefit from these developments for years (and in some cases decades) to come.

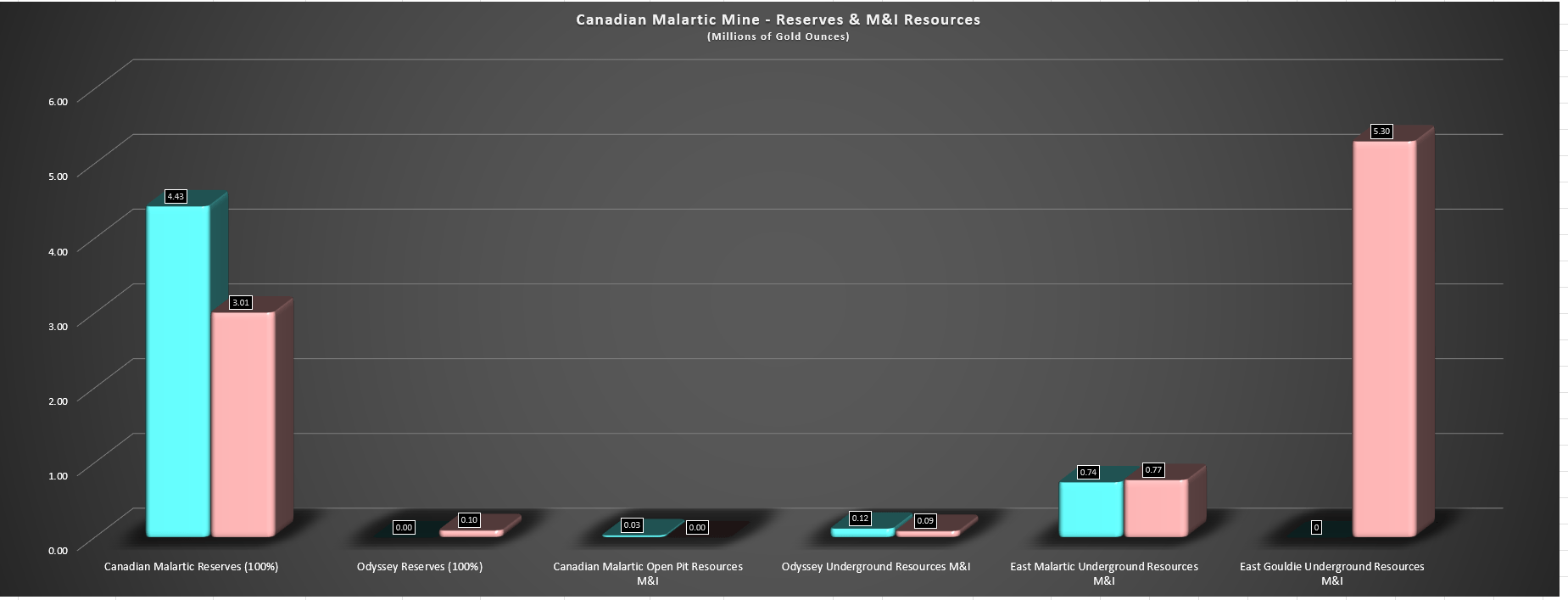

Canadian Malartic Mine/Odyssey - Reserves & M&I Resources (Company Filings, Author's Chart)

{kind=link}

One case worth highlighting is the Canadian Malartic Partnership's success hitting mineralization more than 1.5 kilometers east of the current East Gouldie resource at the Odyssey Underground Mine which will begin production this quarter and growing the total resource base. As the chart above shows, while open-pit reserves declined due to mining depletion, Odyssey reported its first reserves, its measured & indicated [M&I] resources were relatively flat, and East Malartic saw a slight increase in M&I resources. Meanwhile, East Gouldie saw a significant portion of inferred resources moved into the higher confidence M&I category, with 5.3 million of indicated resources in place at year-end at an average grade of 3.29 grams per tonne of gold (triple the current head grade at Canadian Malartic).

Notably, this excludes ~9.2 million ounces of inferred resources at East Malartic, East Gouldie, and Odyssey, and we still haven't seen any resources reported at the eastern extension of East Gouldie, Titan, nor the potential western extension of East Gouldie towards Norrie. Hence, there looks to be significant upside to this resource base, with the potential for this to ultimately grow to 20.0+ million ounces of gold combined across all categories (reserves, M&I, and inferred resources). This is an enviable position to be in for Osisko Gold Royalties which holds a massive 5.0% NSR on the highest-grade and highest-priority zone (East Gouldie), and an effective ~4.50% NSR on Odyssey when averaging out its 3-5% royalty that differs across zones. Let's look at other developments below:

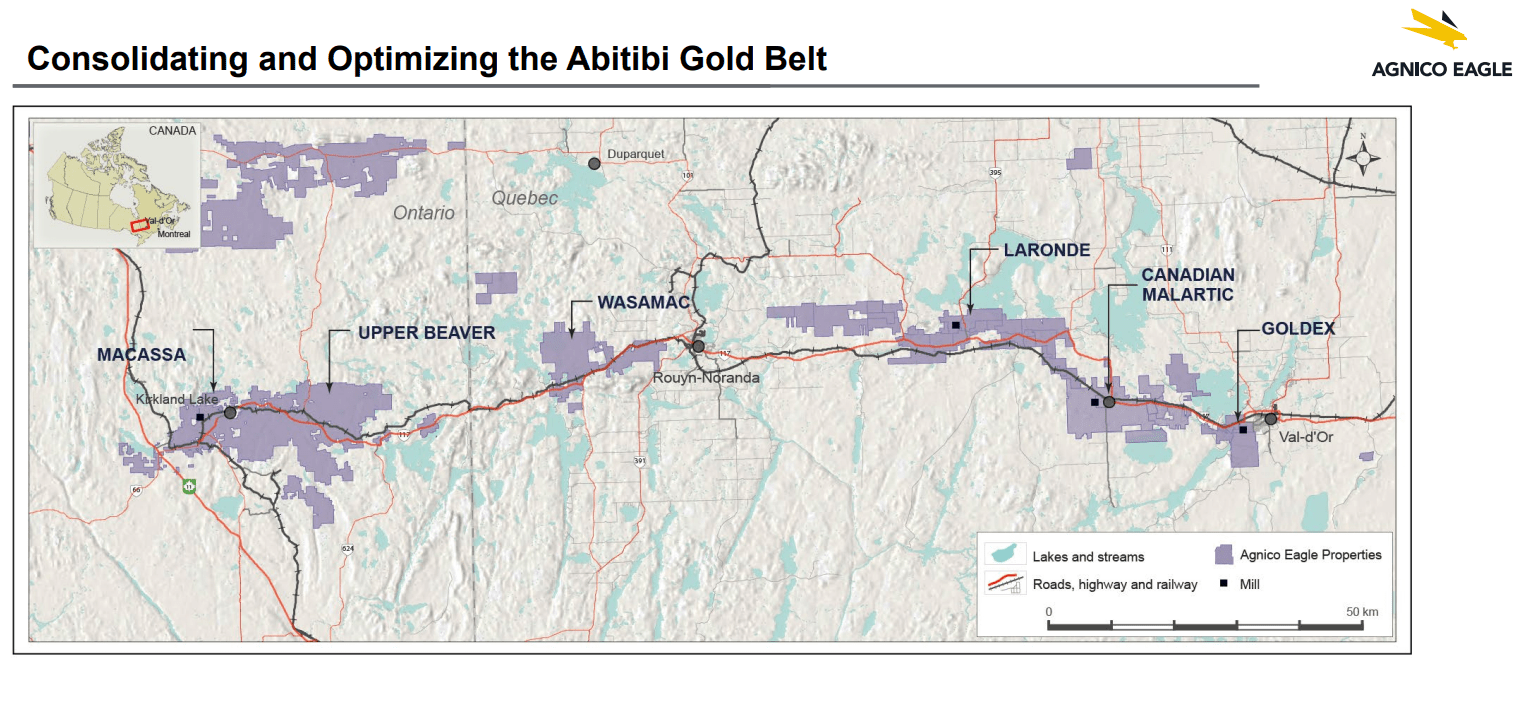

Double Dipping In The Abitibi Gold Belt

Unless an investor has been living under a rock, they're likely quite familiar with Agnico Eagle Mines ( AEM ), the third largest gold producer globally that has extended its lead past names like AngloGold Ashanti ( AU ) and Gold Fields ( GFI ) with its recent M&A activity. Given that Agnico is one of the most well-respected miners with industry-leading margins, a glowing track record of reserve replacement, and a predominantly Tier-1 jurisdictional profile, one would be hard-pressed to find a better way to get leverage to the gold price outside of Agnico Eagle. However, in Osisko's case, it offers exposure to several of Agnico's assets (including one of its top-2 assets) with the added benefit of insulation from growth capital, sustaining capital, and inflationary pressures because of its royalty business model, with the following exposure:

- Akasaba West (2.5% NSR)

- Canadian Malartic, excluding Odyssey (5.0% NSR)

- Hammond Reef (2.0% NSR)

- Holloway McDermott (15% NPI)

- Kirkland Lake Camp, including Amalgamated Kirkland (2.0% NSR)

- Odyssey Underground (3.0 -5.0% NSR)

- Upper Beaver (2.0% NSR)

- Teck Hughes (1.0% NSR)

The most significant asset is the producing Canadian Malartic Mine (5.0% NSR) and the soon-to-be producing Odyssey Underground Mine, with a 5.0% NSR on the most well-endowed zone: East Gouldie (plus 5.0% on Odyssey South and the western half of East Malartic). However, there are several other key assets in this list, and one important one is the Kirkland Lake Camp. The exposure to the ~25,000 hectares of land in this camp is one reason I was bullish on Osisko last year , given that the borders were coming off of this camp following the Agnico/Kirkland merger, similar to when the two largest gold majors teamed up in Nevada to create Nevada Gold Mines LLC and a more profitable and sustainable set of mining complexes (Carlin, Cortez, Turquoise Ridge).

Abitibi Gold Belt - Agnico Eagle Operations/Projects (Agnico Eagle Presentation)

{kind=link}

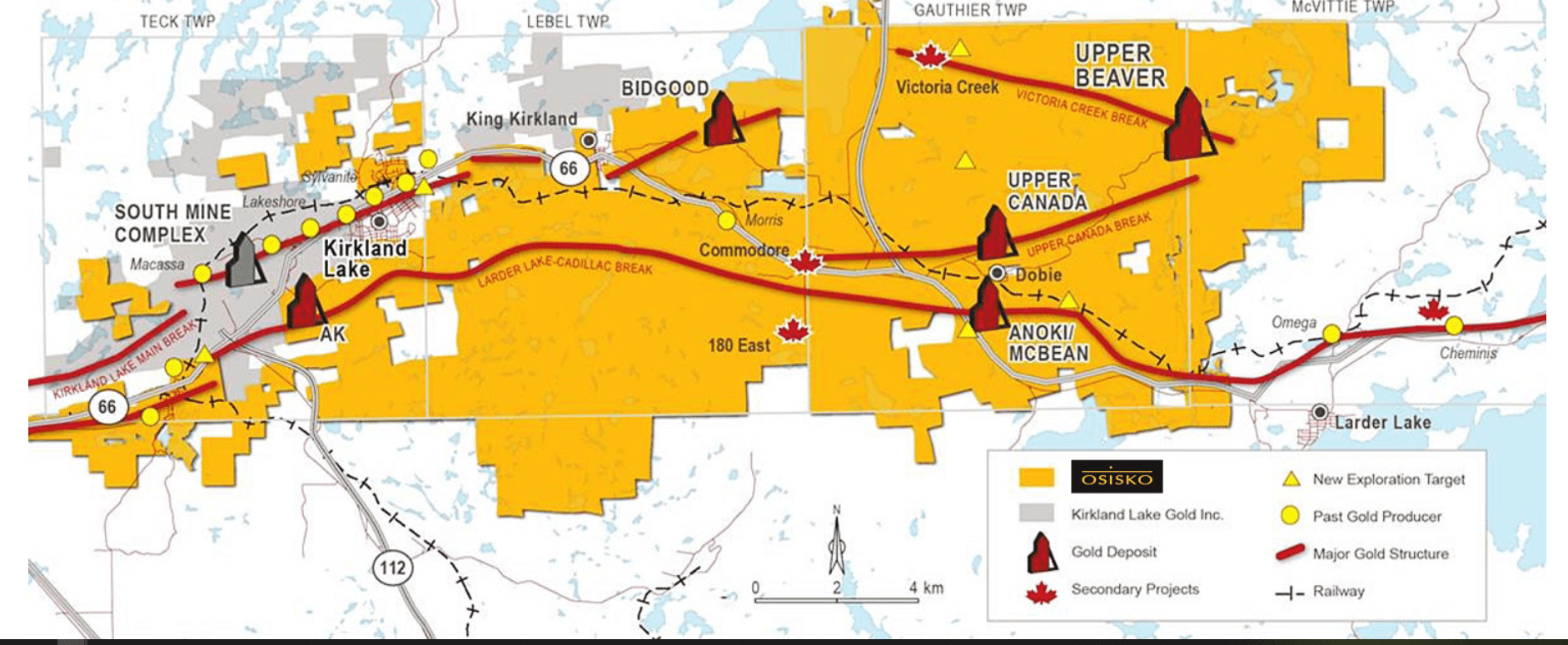

Kirkland Lake Camp - Osisko Royalty Coverage (Company Filings)

{kind=link}

With the Abitibi Gold Belt (shown above), Osisko Gold Royalties has seen an upgrade in the sense that Amalgamated Kirkland (potential to contribute up to 40,000 ounces) is no longer orphaned next to the Macassa Mine and Upper Beaver either in the camp, with two Agnico owned mills to the west and northwest (Macassa and Holt). However, with the acquisition of Yamana by Agnico (which gives Agnico complete control of what gets fed to the 60,000 tonne per day Canadian Malartic Mill), the outlook has improved even further. The reason? Post-2028, the Canadian Malartic Mill will have ~40,000 tonnes of excess capacity, and rather than building a stand-alone plant to process Wasamac, Upper Beaver (2.0% NSR), and or Upper Canada material (2.0% NSR), Agnico could look at making room at existing facilities, such as Canadian Malartic.

Based on an assumption of average annual production of ~200,000 gold-equivalent ounces from Upper Beaver for the first five years and a 2.0% NSR, Osisko Gold Royalties would enjoy $3.8 million in revenue beginning in 2029 at a $1,900/oz gold price. However, given that Agnico is now looking at potentially processing ore at the Canadian Malartic Mill, given the excess capacity and its strategy of leveraging off existing infrastructure, Osisko Gold Royalties could "double dip" based on its $0.40/tonne royalty on any material processed at Canadian Malartic that's not on its royalty ground. Assuming a 4,500 tonne per day processing rate for Upper Beaver material, this would translate to an additional ~$660,000 in revenue per annum, translating to total revenue from Upper Beaver of ~$4.5 million.

Although this figure may not appear that significant in the grand scheme of things (2,000+ GEOs per annum), there are other assets likely to be unlocked in the region, and that could also have double-dip potential depending on grades and haulage costs. This includes Upper Canada and Anoki-McBean in the Kirkland Lake Camp that are lower-grade than Upper Beaver at ~6.0 grams per tonne gold-equivalent, but still have attractive grades in a scenario where there is excess mill capacity and sunk capital just over 100 kilometers east, which is the case for Agnico Eagle. Of course, another option (although Osisko wouldn't get the double dip benefit) is processing at a closer mill such as Holt. While early to speculate, this could add another 1,000 GEOs per annum outside of Upper Beaver.

Finally, and as I pointed out at the time of the Kirkland/Agnico merger, Osisko Gold Royalties could see a small contribution starting in 2024 with material from Amalgamated Kirkland (AK Deposit), that sits just east of Macassa and closer to surface. Although not a huge needle-mover, ~30,000 ounces from AK sent to the LZ5 mill circuit at the LaRonde Complex (130 kilometers to the east) would translate to an additional ~$1.1 million in revenue per annum, giving the region total contribution potential of 4,000+ GEOs (~4% growth vs. FY2023 guidance) when factoring in Amalgamated Kirkland, Upper Canada, and Upper Beaver, plus upside from double dipping at the Canadian Malartic Mill (per tonne royalty on outside feed).

As noted in Agnico's recent Q4/FY2022 results, it is evaluating the possibility of transporting ore from Upper Beaver to the major railway line, which lies 7.0 kilometers away, which would then drop this material less than five kilometers north of the Canadian Malartic Mill to be scooped up for future processing.

Osisko's Other Opportunities Continue To Grow

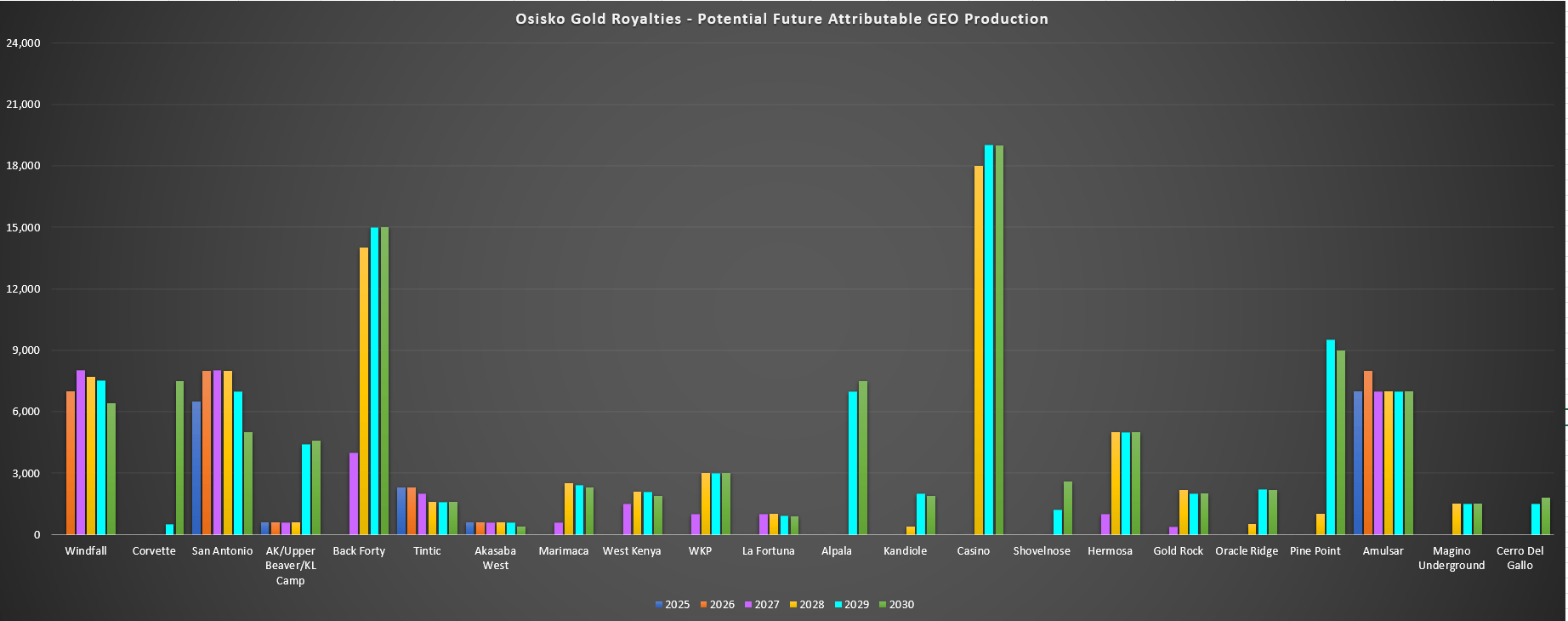

Aside from the elephant in the royalty portfolio, Odyssey Underground , which I have discussed at length in past updates, Osisko has several other proverbial irons in the fire that will contribute to future attributable production. The below chart highlights some of these opportunities with potential contribution dates as well as how significant these could be from a gold-equivalent ounce standpoint. Some of these include advanced stage projects like Windfall (Quebec), Hermosa (Arizona), and Alpala (Ecuador), with these three combined having the potential to contribute well over 15,000 GEOs per annum.

Other relatively earlier-stage opportunities include Marimaca (Chile), West Kenya (Tanzania), Kandiole (Mali), Gold Rock (Nevada), Oracle Ridge (Arizona), La Fortuna (Mexico), WKP (New Zealand), and Marban (Quebec). These eight opportunities could combine for another ~15,000 GEOs per annum. I would argue that there's a high probability that at least half of these projects head into production by 2030. In addition, there are some opportunities where it was difficult to assign value that appear to have a brighter future. Some examples include Amulsar which was recently approved for restart , Magino Underground, which may be pursued more actively under a new CEO and a focus on Tier-1 jurisdiction operations, and a sleeper asset that's turned into a giant: Corvette.

Assuming all of the opportunities highlighted in the below chart are in production as of 2030, we would see incremental annual production of 100,000+ GEOs per annum. However, even if we take a conservative view and assume just half of them come online, this still adds up to 50,000+ GEOs or nearly 60% growth vs. current attributable production levels. So, there is considerable growth here given that this is outside of organic growth on currently producing assets and it assumes Osisko completes no further transactions on producing/near-term producing assets in the next six years.

Osisko - Potential Future Contributions (Potential GEO Production Per Asset) (Company Filings, Author's Chart & Estimates)

{kind=link}

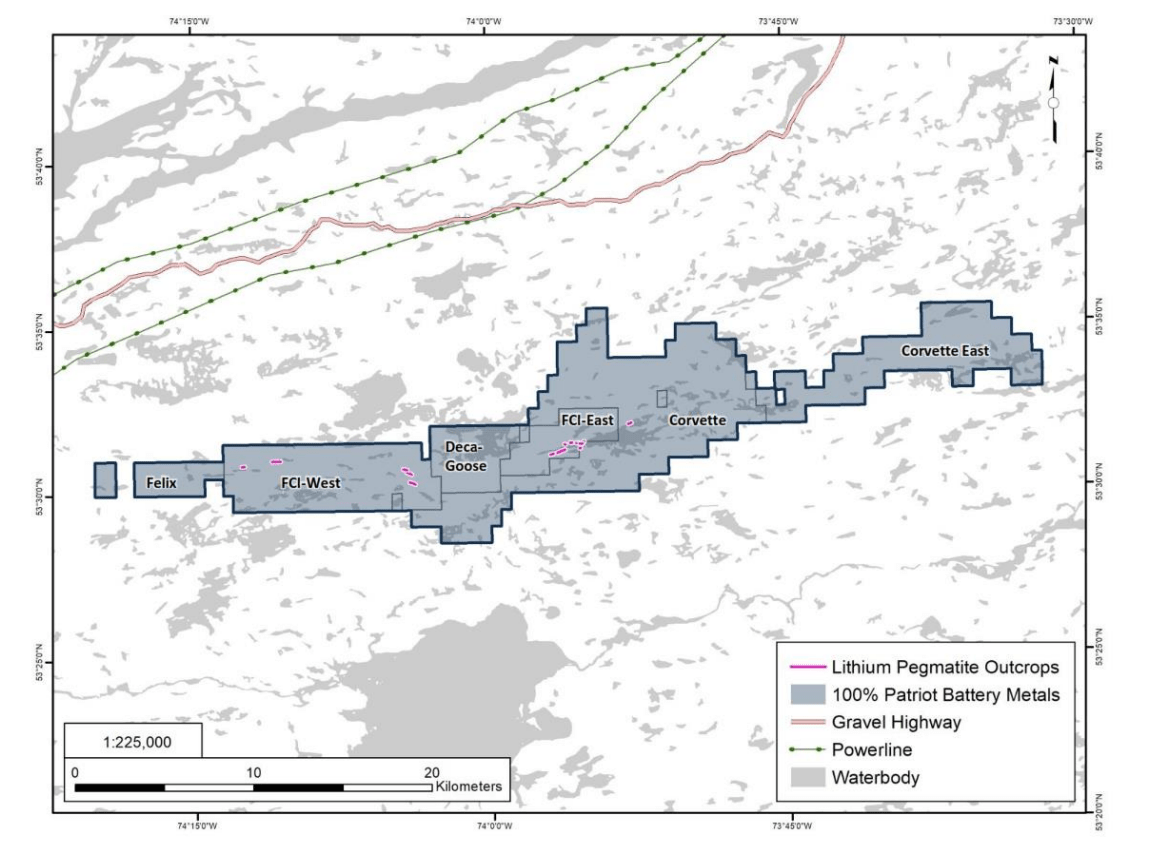

Regarding the latter opportunity, Osisko holds a 2.0% NSR on Patriot Battery Metals ( OTCQX:PMETF ) Corvette Property in Quebec, with the company reporting blockbuster results over the past year. Highlight intercepts include 159.7 meters at 1.65% lithium oxide (Li2O) and 131.2 meters at 1.96% Li2O intersected earlier this year, which are not only high-grade, but very thick intersections, making this a special discovery. It's still early days and I wouldn't expect first production until 2029 earliest. Still, the grades, scale and potentially simple flow sheet could attract a major. However, even if not operated by a major, this looks to be a project capable of generating upwards of $1.0 billion in revenue per annum once in commercial production, even at conservative spodumene prices.

Corvette Property & Lithium Pegmatite Outcrops (Corvette Technical Report)

{kind=link}

Patriot Battery Metals noted in December that it had achieved 79% recovery in dense media separation [DMS] test work, with the potential for a simple DMS processing plant without the requirement for floatation. According to Patriot Battery Metals' recent Technical Report, all 111 claims on the FCI East and West claim blocks at Corvette are subject to a 2.0% NSR held by Osisko Gold Royalties with no buyback provisions (plus a 1.5% to 3.5% sliding scale NSR on precious metals).

Patriot Battery Metals - CV-5 Mineralization (Company Website)

{kind=link}

Even using a very preliminary estimate of $800 million in annual revenue from this project beginning in 2030, this is certainly a needle-mover. This is because based on a 2.0% NSR and just 70% royalty coverage, this could translate to annual revenue of $11.2 million or ~6,200 GEOs per annum at an $1,800/oz gold price assumption. If we compare this to Osisko's ~90,000 GEO attributable production profile, this asset that I assigned no value to previously could offer ~7% production growth by the end of the decade relative to Osisko's current attributable production profile. So, while I would caution that it's still very early, this is certainly a welcome surprise to the Osisko investment thesis.

Finally, I'd be remiss not to note that Osisko has several other monsters in its royalty portfolio that could significantly increase the company's cash flow generation, including Casino (18,000+ GEOs per annum), Pine Point (8,000+ GEOs per annum), Horne 5 (20,000+ GEOs per annum), Back Forty (15,000+ GEOs per annum), White Pine (20,000+ GEOs per annum), and Spring Valley (4,000+ GEOs per annum). Even if just one of these assets heads into production, we could see 10-20% growth relative to Osisko's current attributable production profile, and if two or more head into production, Osisko's current path toward ~140,000 GEOs suddenly looks more like a path to 200,000 GEOs).

Recently, a joint-venture was announced at Pine Point with Appian Natural Resources Fund (~$80 million value) to acquire an undivided 60% interest in Pine Point, a nice vote of confidence in the asset, and a meaningful cash injection to help move it forward.

So, what does this all mean for the company?

Between organic growth at top assets like Island Gold (Phase III), Eagle (Project 250), Mantos Blancos (7.3 Million Tonne & Potential 10 Million Tonne Expansion), Tintic (Throughput Expansion), new large assets likely to come online or already in construction (Windfall, Upper Beaver, San Antonio, Tocantinzinho), the potential for a second shaft at Odyssey, and the deep portfolio outside of these assets, Osisko Gold Royalties is arguably a major royalty/streaming company (200,000+ GEOs per annum) disguised as a mid-tier. In fact, I would argue that the quality and scale of this royalty/streaming portfolio is unmatched outside of the top-3 precious metals royalty/streaming companies with an average market cap of ~$17.0 billion.

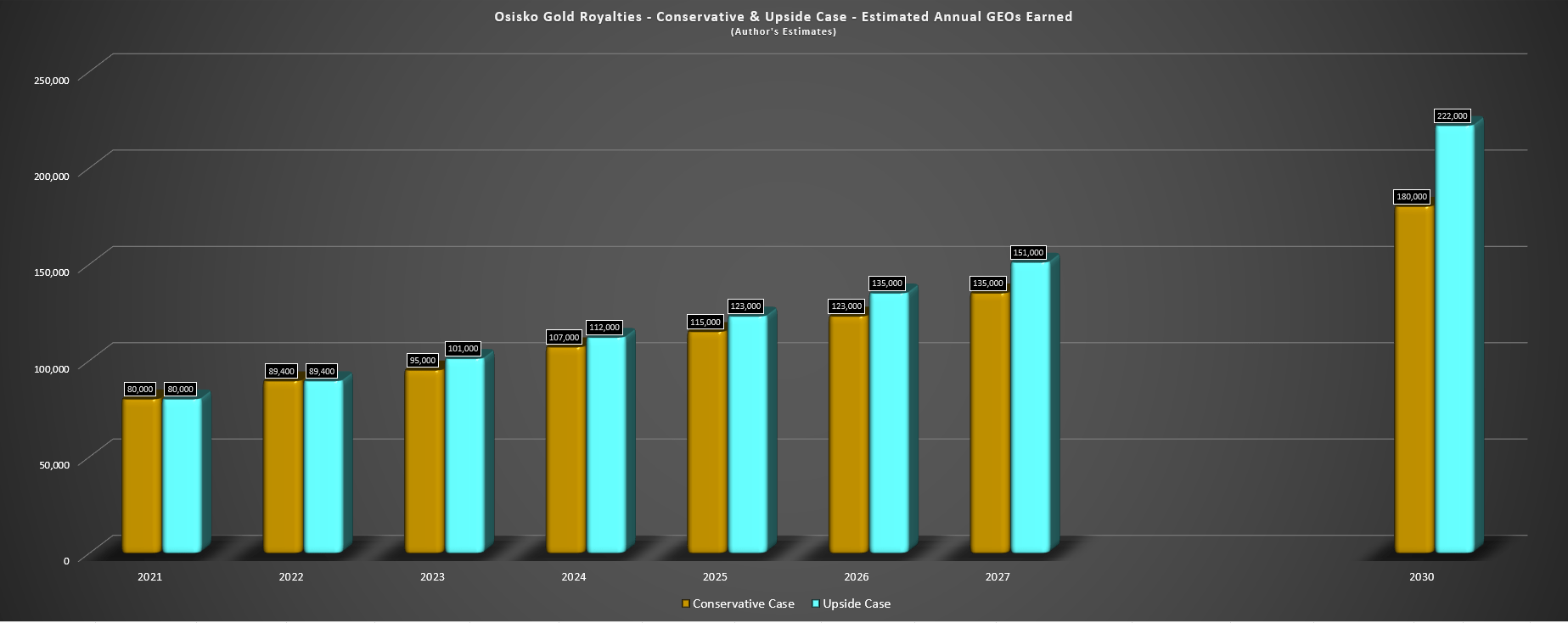

Osisko - Conservative & Upside Case of Estimated Annual GEOs Earned (Company Filings, Author's Chart)

{kind=link}

Looking at the chart which shows the company's current, historical and future attributable production profiles above (latter based on my estimates), I see the potential for Osisko to enjoy 38% growth in the conservative case (89,400 to 123,000 GEOs), and up to 50% growth in an upside case (89,400 to 135,000 GEOs) from FY2022 to FY2026. This means that regardless of what precious metals prices do over the next few years, Osisko will continue to record results in revenue and cash flow and this increased cash flow could help it to transact on larger deals assuming a favorable market for transacting. Looking out to 2030, I believe a conservative case is 180,000 GEOs (101% growth), with an upside case of 222,000 GEOs (~150% growth).

Even if we use a conservative $1,950/oz average gold price in 2030 and assume Osisko has an attributable production profile of 200,000 GEOs (mid-point of conservative and upside estimates), this would translate to roughly $390 million in annual revenue and $300+ million in annual cash flow. Applying a cash flow multiple of 24.0 to reflect its Tier-1 jurisdictional profile could translate to a long-term fair value for the stock of ~$7.2 billion or a fair value of ~$37.50 per share (assuming 192 million shares outstanding). This is a very conceptual long-term target, and much can happen in eight years. Still, the point is to show just how impressive Osisko's pipeline is and what the true potential is for this portfolio long-term.

While these further out estimates assume at least one modest transaction per year post-2024 to increase attributable production, I think this is a brutally conservative estimate given that Osisko will be generating over US$150 million in cash flow per year that it can put to work. This is a key differentiator vs. other high-growth stories in the junior royalty/streaming space that don't have the scale to make meaningful deals with cash flow, meaning that new deals will come at the expense of share dilution or high-cost debt, like we continue to see with Metalla ( MTA ).

So, with a strong balance sheet, significant liquidity, and one of the higher-quality royalty/streaming portfolios sector-wide, I am hard-pressed to find a better risk-adjusted way to play the precious metals sector for long-term investors. In fact, I am amazed that we have not seen a suitor look at acquiring Osisko Gold Royalties on the basis of adding exposure to two world-class ore bodies (Odyssey and Windfall), especially given the price we've seen paid to scoop up royalties elsewhere in Tier-1 jurisdictions, such as recent deals on Cortez, Great Bear, Red Chris, and Magino.

Summary

There's no question that Franco-Nevada ( FNV ) and other major players have exceptional business models and benefit from inflation-protection, scale, and diversification, making them staples for a portfolio hungry for precious metals exposure and diversification. However, the one thing missing from these names is the potential to double attributable production growth from current levels this decade given that they have grown to a scale where this is very difficult to achieve. Among the mid-caps, there are higher-growth options, but Osisko Gold Royalties is unique in the sense that its future growth comes from a deep development portfolio with dozens of assets, meaning that it can grow meaningfully even if a few opportunities don't pan out this decade, or at all.

This setup is quite enviable, and the visibility into future cash flow can comfort investors, with its cornerstone asset likely to produce into the 2050s and a significant portion of current and future production coming from mining-friendly jurisdictions. While the Cobre Panama dispute is likely to be worked out for First Quantum ( OTCPK:FQVLF ) and royalty holder Franco-Nevada, this isn't something that Osisko investors have to worry about given that its most significant cash flow contributors are in top-20 jurisdictions (Ontario, Yukon, Quebec, Chile). So, with a unique combination of industry-leading growth, a cornerstone asset held by a top-3 gold producer, and a mostly Tier-1 jurisdictional profile, I see Osisko Gold Royalties as the premier way to get precious metals exposure, and see it as a Buy on dips.

For further details see:

Osisko Gold Royalties: A Solid Buy-The-Dip Candidate