OTCM - OTC Markets Group: A Good Buy Even With Slight Margin Contraction

2023-03-23 10:51:58 ET

Summary

- Solid results showed a slight slowdown in the business, but not as bad as thought.

- Integrations of the latest acquisitions will continue to weigh on margins, however, in the short term only.

- The balance sheet is very strong, and I argue even with contractions in margins and revenue declines, the company will weather a recession without a problem.

- A 10-year conservative DCF model suggests the company is a good buy at these levels for the long run but might drop more in the next couple of months, caution is advised.

Investment Thesis

The impressive balance sheet and solid free cash flows over the long run got me intrigued. With decent FY2022 results out, showing not-as-bad revenue numbers as many other companies, got me thinking that the OTC Markets Group (OTCM) has a solid moat that can withstand economic downturns even if revenues start to slip into declines over the next couple of years. In this article, I will argue that the strong free cash flow and subsequent strong balance sheet will be able to continue to propel the company further and reward shareholders as it has in the past. I will present a conservative 10-year DCF model where the revenues decrease in the next 2 to 3 years and slight decreases in margins due to increased costs of further implementation of the latest acquisitions and subsequent bounce back to current margins, the company is a buy at these levels even with conservative assumptions.

Briefly on FY2022 Results

The company managed to eke out record revenues in '22 despite the tough economic environment. Revenues were up 2% to $105m, margins saw slight contractions due to acquisitions of EDGAR Online, a premium supplier of real-time SEC data and financial analytics, and Bly Sky Data Corp a leading provider of equity and debt compliance data regarding the rules and regulations of Blue Sky.

Outlook '23 and Beyond

The management mentioned they will be working harder at attracting more subscribers in '23 and beyond and are looking to retain more of their existing clients by making the company more efficient and user-friendly. One key aspect is that with the acquisitions of the two mentioned above, the company is looking to become one platform. What that means is that all of their offerings of OTC securities, financial data and analysis, and everything else they have will be streamlined into one platform, which will make everything more efficient and appealing to long-established clients and new clients alike.

Advancing its IT structure is going to be very beneficial in the long run. Other companies that focused on streamlining their cloud platforms and transitioning more towards digitization have seen dramatic improvements in operating and net margins in the long run. The company already boasts fantastic margins and if further digitization is one of its priorities, it can only be a good thing in the long run. There might be some hiccups along the way as they may not be as efficient and slightly slow in the first couple of years, but the reward will be substantial once everything is ironed out and works as intended. The digitization measures will become cost-effective and prioritizing customer experience will be very beneficial.

The acquisition of EDGAR Online will boost its Market Data Licensing offering in the long run, but it will be tough to integrate at first as the company is going to integrate all of the data anew onto its cloud platform. The company did not have anything similar to EDGAR before the acquisitions, so it will be a lot of work to have 72 terabytes of data in its cloud infrastructure. So the IT team has a tough job ahead of them and I believe this will be quite costly in the beginning, but once everything is implemented, the costs will start to come down and the company will be more efficient once again.

Overall, it seems that the company is going to invest heavily into its core offerings with integrations of the acquisitions and by getting more subscribers onto their platforms. The decline in margins in'22 is understandable and I won't be surprised that margins would contract a little more due to continuing implementation, and what may again be a year or two of turmoil in the economy which could reduce activity on their platforms, especially from non-professional users.

Financials

What attracted me to the company in the first place was the company's impressive ability to generate returns to shareholders with very good free cash flow generation and zero debt. Another minuscule reason behind looking at the company is that I used to work for a custodian bank in the OTC derivatives department, so I thought it'd be interesting to delve deeper.

The company's un-levered free cash flow has been positive for at least 5 years (my model goes back to 2018 only). The company has been able to cover its capital expenditures and working capital needs efficiently. This is a very positive sign for me. The company is very financially stable and there's a good chance that it can use this free cash flow for further growth through organic means or acquisitions. With such efficiency in place, the company does not need to take on debt to fund its working capital needs or cover dividends.

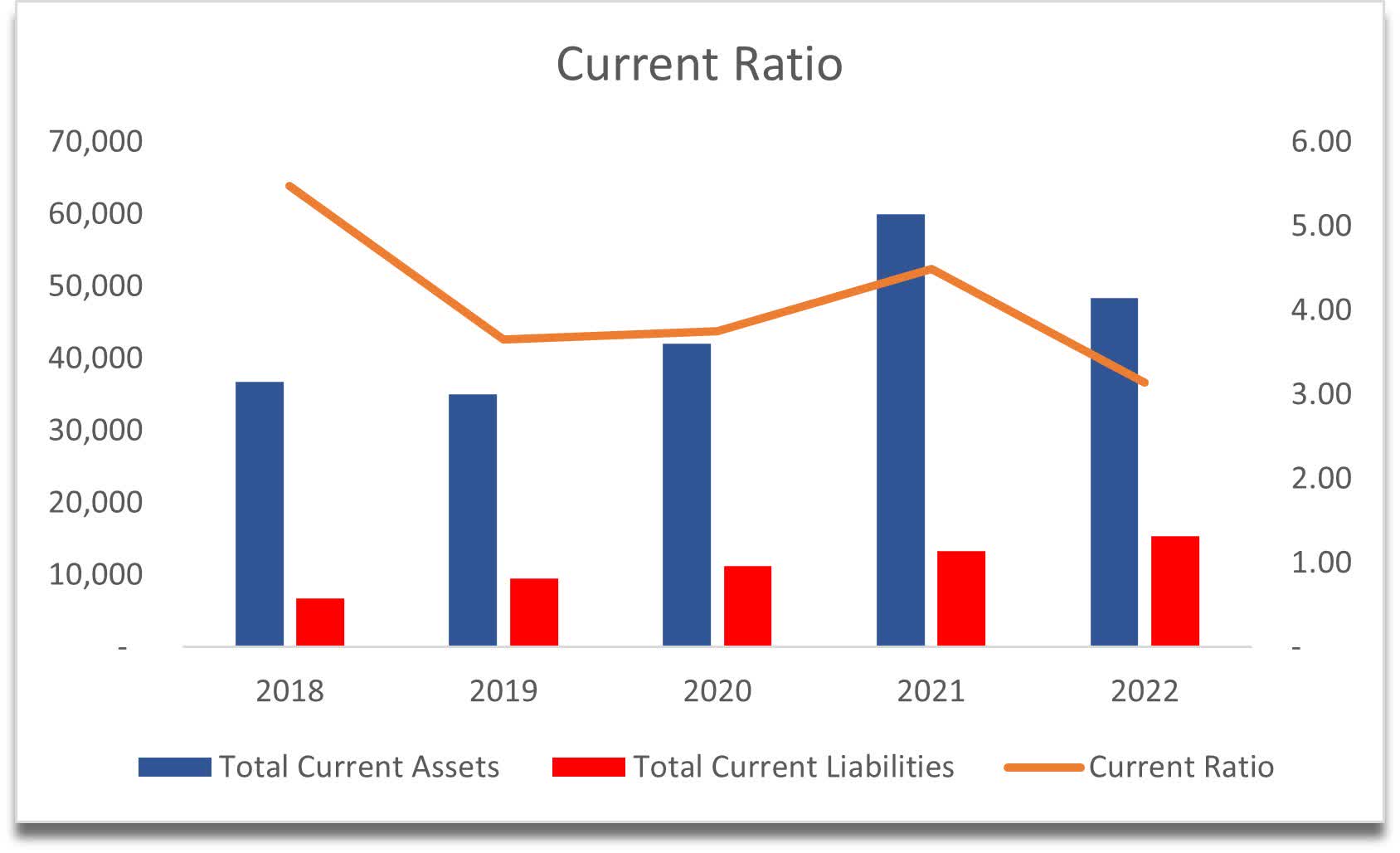

I have a problem with companies not being able to pay off their short-term obligations, however, right now I almost have an issue with OTCM's high current ratio. The management could utilize their assets more efficiently in that sense, however, we can see that it has come down slightly and if the company finds more potential acquisitions in the future, it could bring the ratio down to what I believe is good management of assets to around 2.0.

{kind=link}

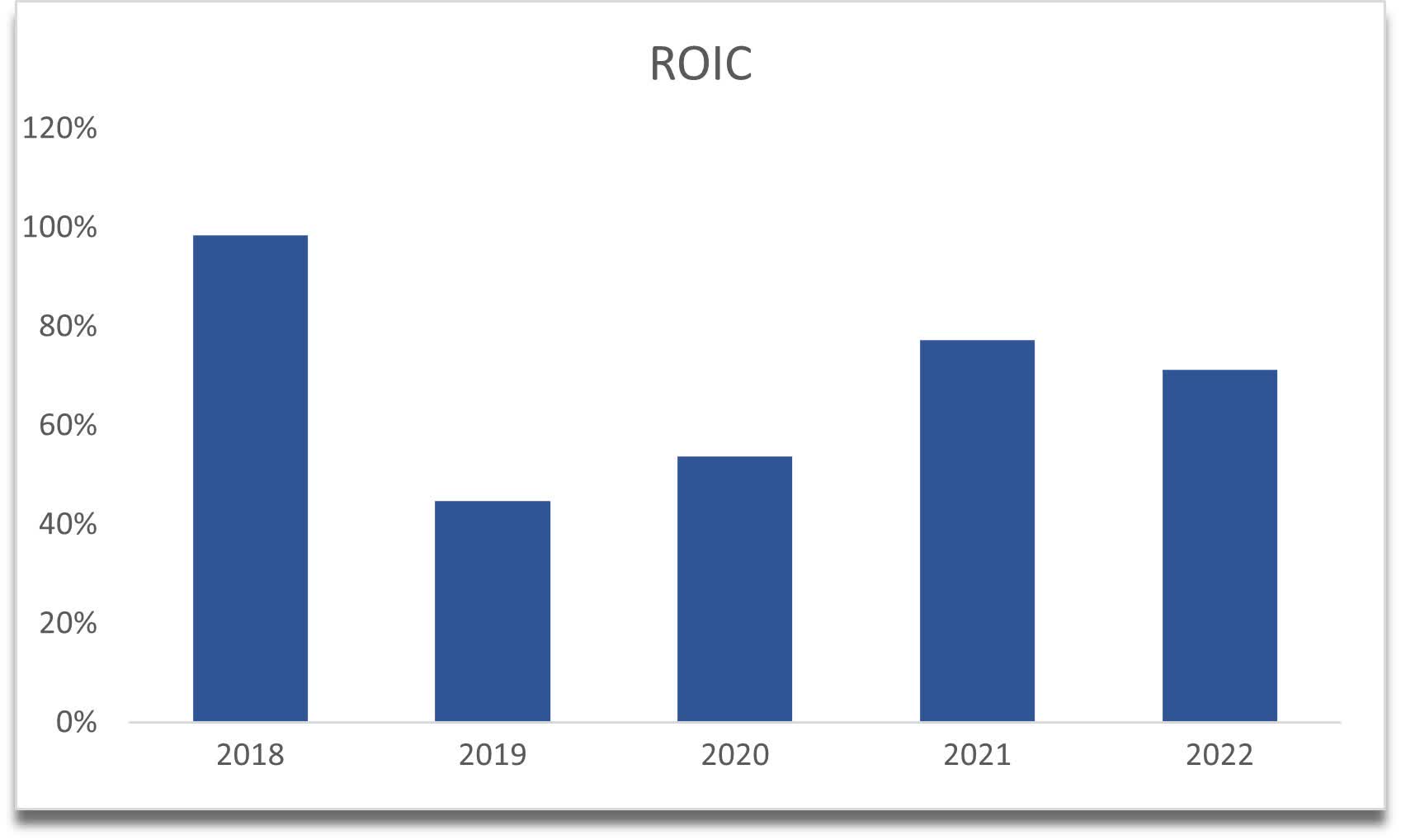

It's unsurprising that the company also boasts really good efficiency and profitability metrics. ROIC has been very high in the last 5 years, reaching close to 100% returns and coming down just slightly. It is much higher than their WACC, which by my calculations is around 6.3%, while a quick google search says it's around 8%. I'm going to stick with my calculations as I don't think 8% is right, seems too high. I also feel ROIC could come down a little bit as it kind of indicates that the company is not investing in more growth opportunities and is hoarding cash and we are already seeing that progress with the two acquisitions in '22.

{kind=link}

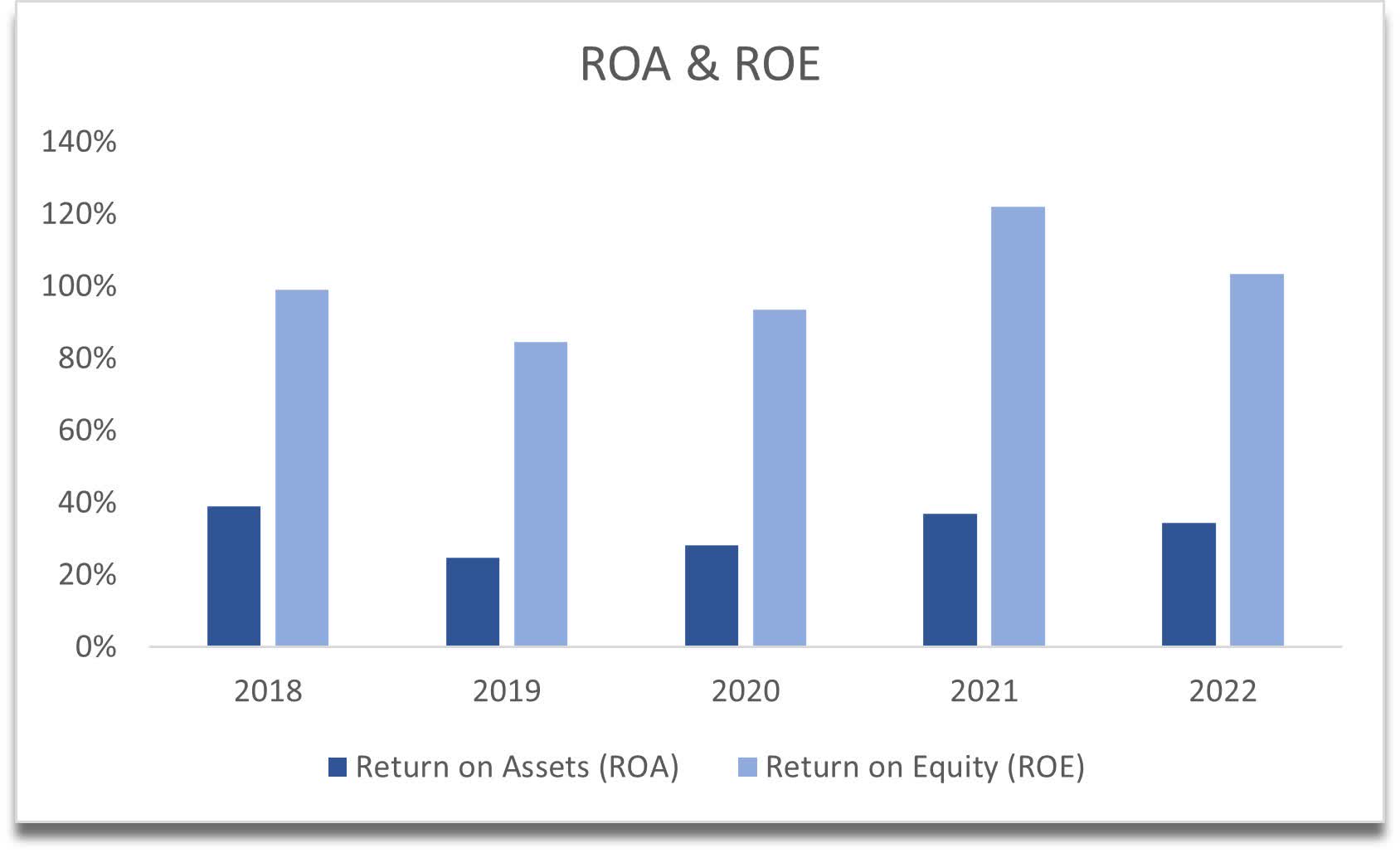

The same story can be said about ROE and ROA metrics. They are impressively high as well and wouldn't hurt if these come down a little bit too if they find some more acquisitions in the future that require this capital.

{kind=link}

Overall, the company is nowhere near any liquidity issues it is in the opposite boat by a long mile, and it has been operating like that for a lot of years. Even with the recession coming in the next year or two, the company can easily weather any downturn because of the strength of the balance sheet alone. The management could be more proactive in growth opportunities, but it is a good sign that they have started that process now and I am excited to see what they can do next for further growth.

Valuation

As I mentioned in the article above, the company is going to have little issues handling an upcoming downturn in the economy because of its strong free cash flows and very solid balance sheet. I decided to implement some revenue declines in the next couple of years because of that looming uncertainty, and contraction of margins because of higher capital requirements of implementing the two acquisitions that will certainly drag down margins in the short run and subsequently come back to the margins we saw at the end of '22 period.

I like to be conservative in all of my models to not overpay for a company, the only thing that changed is how conservative I should be, and it all depends on the company. Here the company is very solid so the assumptions don't have to be too conservative.

For the base case scenario, I assume a slight decline in revenues in '23 and '24 of -5% and -2% respectively, after that, the revenues have a little recovery of 12% and grow down linearly to 5% by '32. This gives me an average yearly growth of 6%. I feel these assumptions are very reasonable as the company has not seen any negative revenue growth in the last 10 years at least and so a slight decline built-in makes it somewhat conservative.

For the more conservative case, the company grows at 4% per year for the decade, and for the optimistic case, it grows at 8% per year.

For the margins, gross margin comes down around 5% in '23 and '24, then increasing every year slightly to the point where the company has the same margin as it saw at the end of '22. Net margins decline by around 7% in'23 and came back to the same margins at the end of '22. Same situation with EBIT % also.

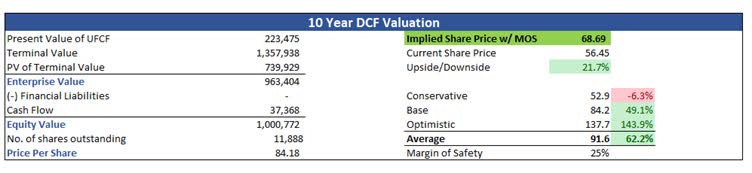

I believe these estimates are conservative enough, as I don't predict a company improving on margins any more than it already has. To make my assumptions even more conservative just because I like to be safe, I will also put in a 25% margin of safety to my intrinsic value calculation. A company like OTCM could do with less margin of safety, but I will rather be more pessimistic. With that said, the intrinsic value of OTC Markets Group with a 25% MOS is $68.69, which implies the company is undervalued and is a good buy at these levels, with around 22% upside.

{kind=link}

Conclusion

I rarely see companies that have such a strong balance sheet, maybe I'm just not looking at the right areas, nevertheless, I think OTCM is a good investment in the long run for sure. The company's ability to generate strong cash flows over a long period, combined with the ability to deploy that cash flow to further grow its business makes it a very attractive investment that can reward the shareholders massively if they stick with it for the long run. The company has seen steady price appreciation over the last 5 years, sitting at around 162%, and the P/E ratio at a lower end of its recent history, which may indicate it is time to buy. Some people might not like that it is over 20, however, higher ROIC requires a higher premium in my opinion, and so I believe 20x is still relatively cheap for what the company can do in the future.

Even with such conservative estimates, the company comes out undervalued, so I believe the company is a good buy right now. It may drop further right now because of uncertainties in the economy, but I like the price point here and it wouldn't hurt to open a small position as a start and average in at lower prices if the markets take a dip further. It all depends on how comfortable you are with the volatility that we most likely going to experience over the next couple of months.

For further details see:

OTC Markets Group: A Good Buy Even With Slight Margin Contraction