ICE - OTC Markets: Unique Business At Discount

2023-12-22 02:13:12 ET

Summary

- OTC Markets is considerably undervalued, with a fair price of $70.28 per share.

- I expect it to deliver a 12.3% CAGR plus a 4% yearly dividend yield over the long term.

- OTCM has no debt, high returns on capital, and a strong competitive advantage.

- Its President and CEO, who led the acquisition in 1997 is still running the company, and the management combined owns ~43% of the company.

Investment Thesis

OTC Markets Group (OTCM) has a strong competitive position in a particular niche, providing critical infrastructure to the U.S. and global financial markets.

Its unique business has led to above-average returns since its IPO in 2009, driven by a highly profitable business model with impressive returns on capital, an asset-light business model, and a negative net working capital, avoiding the need for debt to grow the company.

The slowdown over the last quarters after a rapid increase in revenues during 2020 and 2021 has brought valuation to its low range, presenting an opportunity for investors to buy into a company that is led by experienced management with strong skin in the game.

Background

The demand for investing in over-the-counter securities dates back many years before the introduction of electronic-based quotation systems, and in 1913 the National Quotation Bureau was established, which published prices for stocks and bonds in the paper-based pink and yellow sheets.

With the surge of electronically-run stock markets during the 1970s, the pink sheets lagged behind due to a lack of interest in innovating and continued being paper-based until Cromwell Coulson, the current President, CEO, and Director of OTC Markets Group led the acquisition of the business in 1997.

He immediately developed electronic products and information services which have greatly facilitated trade and improved transparency, increasing the annual trading volume from less than $30B in 2000 to over $500B in 2022 .

Mr. Coulson and his family currently own 34.7% of the company, which I see as highly positive.

OTC Markets Overview

OTC Markets Group Inc., which I will refer to as OTCM, operates regulated markets for trading more than 12,000 U.S. and international securities, of which over 2,600 have a $1B market cap or higher .

The company operates under three business segments:

- OTC Link (17% of revenues ): It operates three SEC regulated Alternative Trading Systems ((ATS)) providing quotation, messaging, trade execution, and reporting services to 195 subscribed broker dealers . This segment generates revenues based on a subscription model and transaction-based fees.

- Market Data Licensing (41% of revenues): Since OTCM has a significant amount of data, this business segment generates revenue through monthly, quarterly, or yearly subscription fees to broker-dealers, investors, traders, institutions, companies, accountants, and regulators. Depending on the license type, the prices range from $250 to $25,000 per month for broker-dealers, and from $5 to $85 for individual accounts.

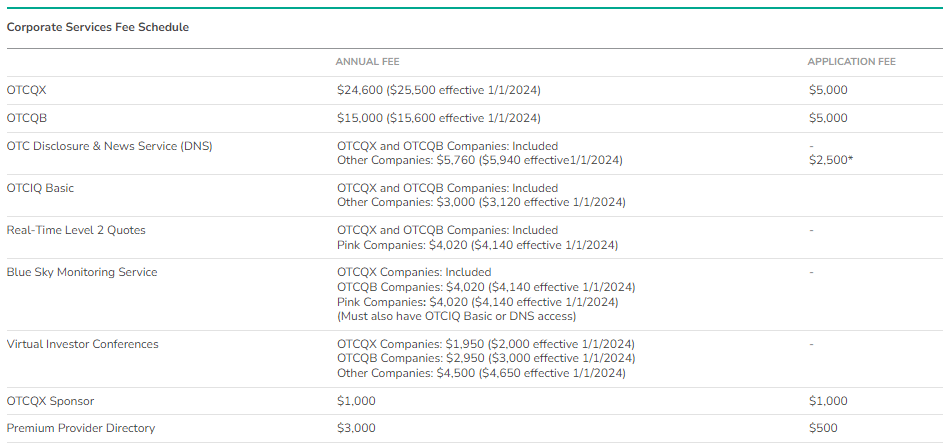

- Corporate Services (42% of revenues): This segment allows issuers, which are classified between three markets depending on the level of financial and corporate disclosure, to communicate and engage with stockholders and potential investors. Companies pay a one-time application fee and annual fees upon renewal.

Source: OTC Markets Fee Schedule

{kind=link}

Most of OTCM's revenues (86% in Q3 2023) are derived from recurring subscription-based arrangements, which provide significant stability and a negative change in net working capital as the company grows, avoiding the need for debt.

What drives its long-term growth is the number of listed companies and trading volumes, the increasing need for market data and financial information, and the corporation's demand for disclosure and regulatory compliance products.

The addressable market for OTC Link services is limited, since members can only be U.S. registered broker-dealers and the platform is already widely utilized, but the market data segment can be consumed also by foreign broker-dealers, making it a larger addressable market.

Apart from the offices in New York and Washington, D.C., the company has established sales offices in London and recently incorporated an office in Singapore, reinforcing its presence in Asia.

Competitive Advantage

OTCM provides critical infrastructure to the U.S. and global financial markets in a particular niche where it covers the needs of smaller companies at an affordable price since getting listed in a major exchange has higher costs, and regulatory and disclosure requirements.

The stock exchange overall market operates as an oligopoly shared between many exchanges such as CME Group Inc. (NASDAQ: CME ), Intercontinental Exchange (NYSE: ICE ), Euronext N.V. ( OTCPK:EUXTF ), or Nasdaq (NASDAQ: NDAQ ), but I believe each of them operates as a monopoly in its particular niche, and that is why they deliver superior returns.

OTCM's markets are not registered as securities exchanges, so they can operate with less complexity and lower costs, providing an alternative to those companies that don't want to be listed on a major exchange or do not meet the requirements. At the same time, this model has its limitations compared to the major exchanges, such as lower liquidity, reputation, and recognition.

Its only competitor in this particular niche is Global OTC, which is operated by the NYSE Group, but its trading volume is less than 10% of OTCM's and I don't expect major exchanges to go after this market niche given its relatively small size.

As has been demonstrated over the last decades , I would rather expect a merger or an acquisition than direct competition, which would probably be more expensive.

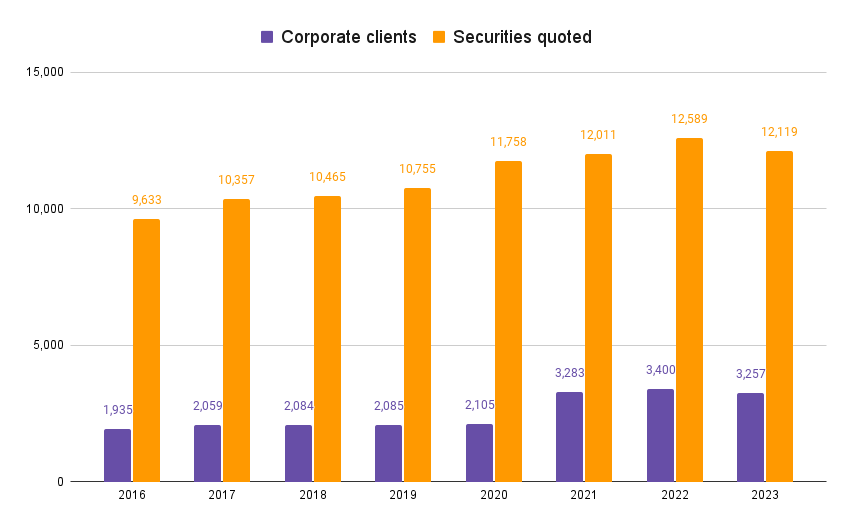

OTCM has been strengthening its competitive position and improving its market reputation through the implementation and development of technological tools and access to data, improving the speed, accuracy, and functionality of its markets. The constant improvement has resulted in an increasing number of corporate clients and listed securities on its exchanges, improving its retention rates from 89% in 2016 to the current 95%.

Source: Author (Data from OTC Markets Financial Reports)

{kind=link}

There are two significant facts that I believe prove OTCM's competitive advantage:

- Price increases above inflation.

- Closing of FINRA's OTC Bulletin Board (OTCBB) in 2021.

In 2008, there was a similar amount of securities quoted on OTC Link compared to OTCBB, but the higher level of functionality of the former drove a shift towards OTCM's markets.

The elimination of its main competitor provides OTCM with significant competitive advantages due to the network effects of its market, making it hard for a new competitor to enter the market.

The reflection of its strong competitive advantage is the pricing power OTCM exercises on its clients. Since it is providing a critical service that represents a small cost compared to the overall expenses of a company, that doesn't have the choice to go for a cheaper alternative in the U.S., OTCM has been increasing its prices faster than inflation.

As shown before, the current cost for being listed in the OTCQB market has an application fee of $5,000 and an annual cost of $15,000, while in 2016 the costs were $2,500 and $10,000 respectively. This is an increase of 100% in the application fee and 50% in annual fees in 6 years, which is significantly faster than inflation even with the recent above-average spikes.

Financials and Valuation

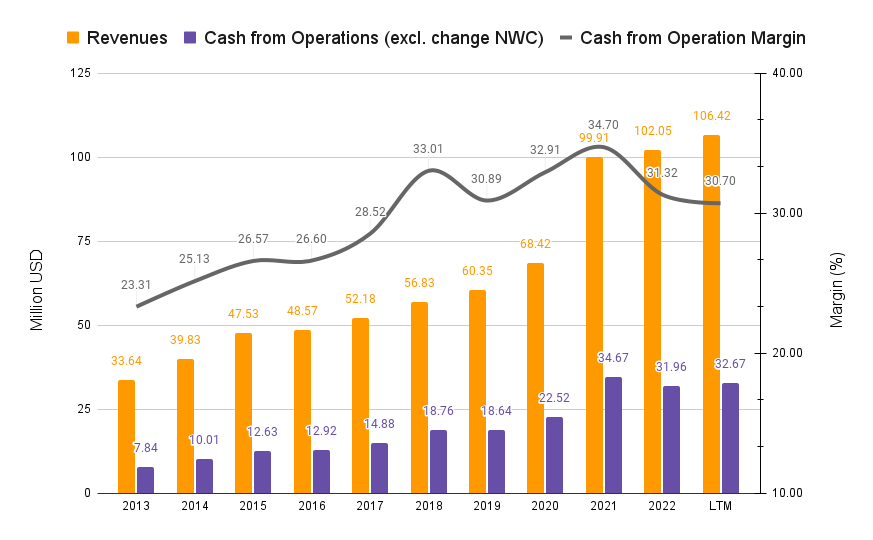

Its strong competitive position on top of a highly profitable business model has led to above-average financial performance.

Source: Author (Data from OTC Markets Financial Reports)

{kind=link}

As shown in the chart above, as revenues increase, operating margins become higher, showing the scalability of the business. OTCM only employs 132 people, and its operating expenses are mainly personnel costs and IT infrastructure:

Source: OTCM Q3 2023 Financial Statements

A percentage of compensation to employees (6% on average over the last 10 years) is paid as a stock-based compensation, which I believe is positive and aligns employees interests with the performance of the company, but it is important to note that OTCM repurchases a similar amount of shares to limit dilution, so this amount should be subtracted when calculating free cash flow available to shareholders.

Balance

OTCM is the kind of business that makes the life of a Chief Financial Officer easy since it operates with a negative net working capital by receiving the subscription fees in advance and paying most of the expenses later.

This has allowed OTCM to grow the business without incurring any long-term debt other than the lease liabilities, which I am excluding in my adjusted balance sheet presented ($12.2M) since I believe it paints a clearer picture:

Source: Author (Data from OTCM Q3 2023 Financial Statements)

As shown in the adjusted balance sheet, most of OTCM's assets are cash (47%), receivables (9.3%), and intangibles (14.5%). Until the two acquisitions were completed in 2022, which increased goodwill and intangibles by $11.68M, the balance was even smaller.

Other current assets are mainly prepaid expenses and taxes, while net property is software and computer equipment excluding accumulated depreciation.

On the liabilities side, from an accounting perspective, unearned revenues increase the balance, but at the end of the day, these are fees received in advance, so it is highly positive when they increase.

Profitability

Due to its asset light business model, OTCM is able to achieve impressive returns on capital employed.

Source: Author (Data from OTC Markets Financial Reports)

As stated before, it is important to note that the recent decrease is caused by the higher goodwill and intangibles.

When compared to other exchanges, we can see that CME has significantly higher net income margins, which makes sense taking into account that the business model has increasing margins as revenues grow and CME's revenues are above $7.5B, or 75 times OTCM's.

Returns on equity and assets are lower in all of them, but the latter should be adjusted given the clearing house nature that OTCM's business doesn't have.

{kind=link}

Capital allocation

This high return on invested capital and the asset-light nature of the business doesn't allow for a significant reinvestment rate, making OTCM a perfect investment for the dividend lovers (which I am not).

The management combined owns ~43% of the company, and while it is true the company could increase its share buybacks, I understand they can be willing to receive dividends and avoid the need for selling shares, which is always negatively viewed by the market.

Mr. Coulson has addressed this matter during its last earnings call in an interesting way:

There's one way is build a business from organic growth that creates capital over the long term and grows in a positive, profitable manner and I think we've done that pretty well and when we've been focused on that organic growth side, we have thought of ourselves in many ways the way Buffet will buy very good companies that create that - that serve their clients well, and he sucks all the capital out.

So he takes away capital allocation from the management and pulls it up to where he's got a superior skill and he allocates out there. We luckily have some great shareholders. So we push out on dividends.

Source: Cromwell Coulson, Q3 2023 Earnings Call

While I may not particularly favor dividends, I view last year's developments related to strategic acquisitions as highly positive.

OTCM was able to deploy over $15M into the acquisitions of Blue Sky Data Corp ($12M), a provider of equity and debt state-law compliance data, and EDGAR Online ($3.5M), a supplier of SEC disclosure data and financial analytics.

These acquisitions significantly enhance OTCM's Market Data Licensing business by expanding its customer base and incorporating the necessary tools for monitoring issuers' compliance under Rule 15c2-11, which has increased reporting requirements.

Valuation

OTCM has been trading at an average multiple of 23.5x net income over the last years, which I believe is fair given the quality of the business, the recurring nature of revenues, and its asset-light business model.

{kind=link}

After a fast increase in revenue during 2020 and 2021, growth rates slowed its pace in 2022. For 2023 I expect a modest 5% increase in revenues and an 8% decrease in net income as a result of lower margins due to the recent acquisitions and the higher headcount, IT, and amortization costs.

These short-term headwinds have brought valuation to its low range and it currently stands below 22x next year's net income.

Expected Growth

For the upcoming years, I expect Market Data to be the main driver for OTCM's revenue growth, given the higher addressable market, the company's efforts to expand internationally through the new Singapore office, and the recent acquisitions that widen the services offered.

Within the OTC Link segment, the most volatile due to its exposure to trading activity, I project an annual revenue growth of 7%, in line with its historical growth rates. These projections are relatively conservative, as they do not factor in potential revenue boosts resulting from the recent FINRA approval allowing the trading of digital assets on the platform.

As for the corporate services segment, I anticipate a 9% annual growth due to a faster-than-inflation increase in prices and a 3% increase in the number of clients.

{kind=link}

I foresee a recovery in EBT margins for the next year, increasing from the current 31% to 34.5% as the company deals with certain one-time costs attributed to the recent acquisitions. While the Blue Sky product is now fully integrated, the optimization of Edgar Online remains in its early stages.

With a 9% discount rate derived entirely from the cost of equity and excluding stock-based compensations from the cash flows - given that OTCM will need to allocate equivalent amounts to limit dilution, making it unavailable to shareholders - my fair price averages at $70.28 per share, suggesting a 21% upside potential.

Looking ahead, I expect OTCM to deliver a 12.3% CAGR plus a 4% yearly dividend.

Risks

As a long-term investor, I am going to avoid the most obvious short-term risks that most companies could face related to a slowdown in the economy, or less trading activity and a reduction in IPOs. Instead, my focus is on the particular risks that can impact OTCM's business.

The main risk I see is the one related to regulation . OTCM's alternative markets are subject to regulation and examinations by FINRA and the SEC, and as we saw with the amendments to Rule 15c2-11 taking effect since September 2021, the amount of information and the regulatory environment could change over time, impacting OTCM's business and cost structure.

Furthermore, if other securities exchanges, beyond NYSE's OTC Global, are granted permission to establish specialized exchanges for thinly traded securities, the rising competition could damage OTCM's competitive edge.

The second risk I'd like to highlight is the persistent consolidation within the broker-dealer industry over the past decade, which could decline the number of subscribers to OTC Link, reducing OTCM's pricing power.

{kind=link}

Lastly, there are the risks associated with reputation and technology . OTCM heavily relies on its ability to adapt to changing technologies and improve its platform, and considering its smaller size compared to other national exchanges, the resources available to deploy into R&D are limited.

If the company is not able to keep up with the technological development, any failure could cause important reputational risk leading to some of its clients moving to bigger exchanges despite the higher costs.

Conclusions

Putting it all together, OTCM has been able to deliver superior returns over the last decade as a result of its monopolistic position in a particular niche and its strong business model.

The company has been improving its competitive position through technological developments, increasing transparency in the over-the-counter markets, widening its range of services, and expanding internationally to increase its customer base.

Despite showing an impressive financial position, with negative net working capital, no debt, and high returns on capital, the company has been lately trading in its low valuation range.

While acknowledging some potential risks I consider OTCM to be considerably undervalued with a fair price of $70.28 per share and expect it to deliver a 12.3% CAGR plus a 4% yearly dividend yield over the long term.

For further details see:

OTC Markets: Unique Business At Discount