SHLRF - Otis Worldwide: Why You Should Look Past The New Equipment Slowdown

2023-11-08 10:39:49 ET

Summary

- Otis Worldwide Corp reported mixed Q3 results, with new equipment orders down 10% year-over-year.

- However, investors should look past this macro-related slowdown for several reasons, as I will explain in this update.

- I will take a look at Otis' backlog, its segment performance and, most importantly, its free cash flow.

- In addition, I will comment on how the currently expected "higher for longer" interest rate environment could impact Otis' debt service ability, earnings and cash flow.

- I present an updated valuation and share at what price I plan to buy the stock of what I consider a wonderful business with a strong moat.

Introduction

I first covered the market leader in elevators, Otis Worldwide Corporation ( OTIS ), in May 2022, examining its operating fundamentals, balance sheet and investment risks. I came to the conclusion that OTIS is a great and well-run company, albeit an expensive stock. I briefly held a small position, which I sold after the fairly quick recovery from the October 2022 slump due to the - in my opinion still difficult - macroeconomic environment.

Mainly due to the rather mixed Q3 results (e.g. 10% drop in New Equipment orders in the third quarter) and the market's expectation that interest rates will stay higher for longer, OTIS shares have fallen by around 12%, so far, from their 52-week high. However, with a blended price-to-earnings ratio of 23 and an unadjusted free cash flow yield of 4.5%, the stock is still far from cheap - especially for an industrial company.

Let's take a closer look at why the market continues to value OTIS shares at a premium - despite the obvious weakness in New Equipment orders - and at what point I will reconsider entering this undoubtedly wonderful business with a strong moat.

Why The Sharp Decline In New Equipment Orders Shouldn't Be Overinterpreted

Admittedly, Otis' Q3 results were somewhat sobering given the sharp decline in New Equipment orders. However, despite the decline, sales in the New Equipment segment were virtually flat on an adjusted basis compared to the prior year, or down 1% on a GAAP basis. Adjusted operating profit also remained virtually unchanged or fell by 6% on a GAAP basis.

The company is clearly benefiting from its strong backlog, which grew in all three segments (see slide 14 of the earnings presentation ). Understandably, growth was weakest in the New Equipment segment at just 2% year-over-year, while the total backlog grew by 5% thanks to strong demand in the Modernization (+15%) and Maintenance & Repair (+5%) segments. I will discuss the company's other two segments shortly, but first let's take a closer look at performance in the New Equipment segment.

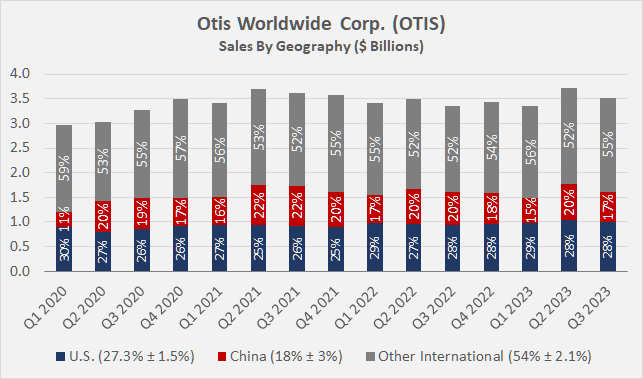

Order intake from the Americas was by far the weakest (-19.9%), and the Asia segment also slowed considerably (-9.5%). The slowdown in China is obvious, but it's important to note that Otis' exposure (Figure 1) is comparatively small. Kone Corp. ( OTCPK:KNYJF , OTCPK:KNYJY ) and Schindler Aufzüge AG ( OTCPK:SHLAF , OTC:SHLRF ) generated 31% and 16% of their 2022 revenues in China, respectively.

{kind=link}

Figure 1: Otis Worldwide Corp. (OTIS): Sales by geographic segment (own work, based on company filings)

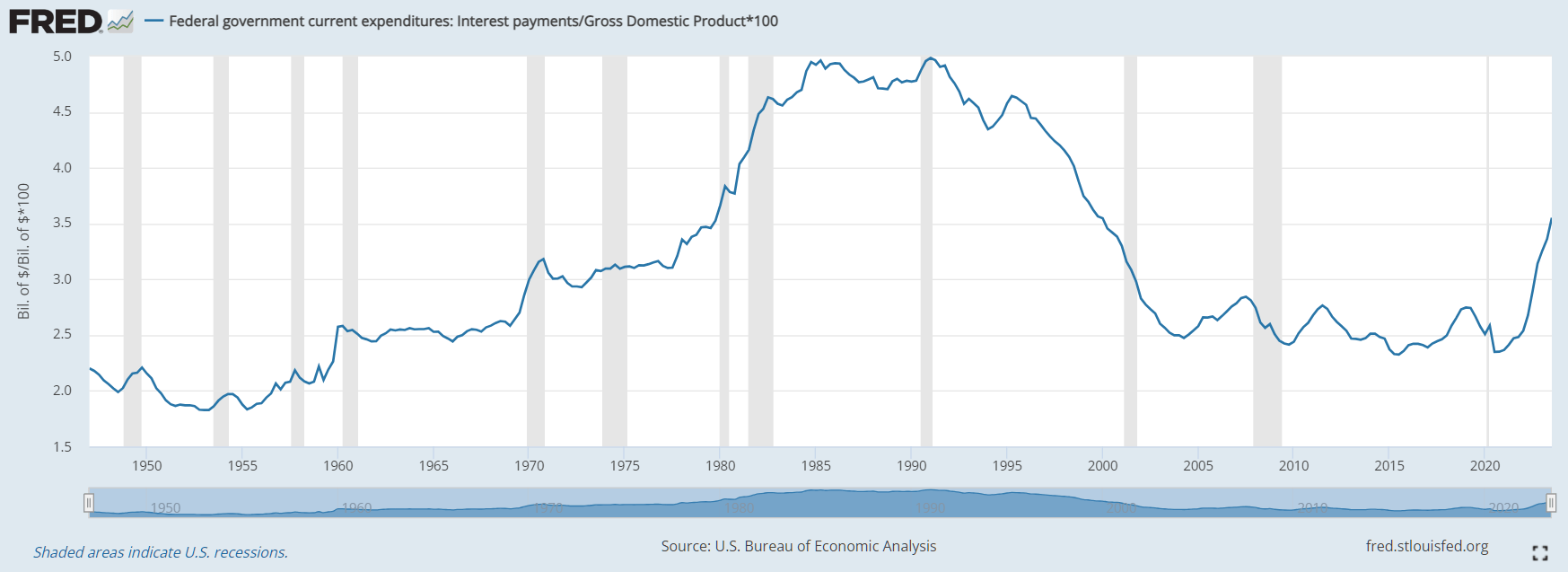

The only bright spot was the EMEA region with a 2.7% increase in new equipment orders. Clearly Otis is feeling the effects of the sharp rise in interest rates, and given the market's expectation that rates will remain higher for longer, it is reasonable to expect continued weakness in new orders. However, the Federal Reserve (and other central banks) will eventually have to lower interest rates, if only from the standpoint of gradually declining debt service capacity relative to GDP:

{kind=link}

Figure 2: U.S. interest expense in percent of GDP, A091RC1Q027SBEA/GDP*100 (U.S. Bureau of Economic Analysis, retrieved from FRED, Federal Reserve Bank of St. Louis)

Of course, it's impossible to predict with reasonable accuracy when central banks will return to a lower interest rate environment, but I do think the Federal Reserve will do whatever it takes to curb inflation - after all, a recession itself has a slowing effect on inflation, and bankruptcies will continue to rise as high interest rates work their way through the economy.

With this in mind, it is reassuring to see that Otis currently has an order backlog of $17.6 billion (of which more than $7 billion is attributable to the New Equipment segment), which protects the company quite well against a short-term economic downturn. According to the CEO , earnings visibility in the Americas segment is currently 12 to 18 months. And even if interest rates do indeed stay higher for longer ( loan defaults are still very low ), keep in mind the strong housing demand in the U.S. ( see my article on Lennar LEN and KB Home KBH ), and in this context, for example, the recently launched Gen3 core elevator, which targets the two- to six-story building segment - the largest by volume in North America. The continued strong demand for housing is probably also the reason why the company has not seen an increase in project cancellations, which would theoretically be expected given the higher rates and consequently less economically feasible building projects.

Finally, it was also encouraging to see that the company was able to increase its market share by 50 basis points since the beginning of the year. This is particularly good news considering that the elevator market in China is extremely fragmented and Western companies have a comparatively weak market share there. For example, around 75% of installations in China are serviced by independent service providers. Otis is acting very cleverly here - through convincing modernization contracts, the company installs its own hardware in third-party elevators, which increases the customer retention rate and thus leads to growing recurring revenues. Don't forget, Otis' backlog in the Modernization segment grew by 15% year-over-year.

Why OTIS Is A Great Business And Worth A Premium Valuation

In the previous section, I explained why I do not consider the short-term weakness in New Equipment orders to be particularly worrying. However, in addition to the various aspects mentioned, it is important to recognize Otis' growing Services segment.

New Equipment is understandably a rather low-margin business (6.4% operating margin on average since Q1 2020), but it should be seen as a gateway to recurring, high-margin repair and maintenance revenue. I've already mentioned how Otis is smartly "onboarding" third-party installations through its modernization programs, but keep in mind that Otis is also modernizing older elevators of its own, which in turn leads to improved retention rates.

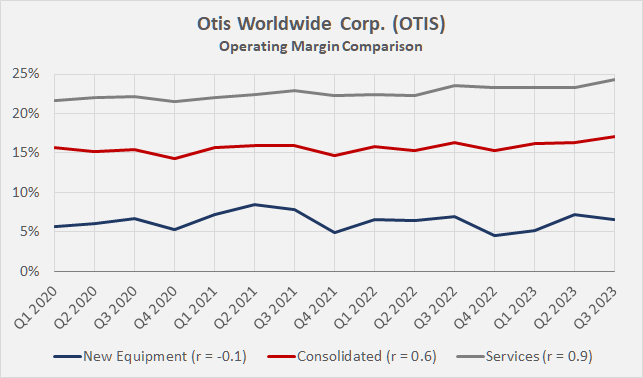

Figure 3 compares the GAAP operating margin of Otis' New Equipment and Services segments. It can be seen that the New Equipment segment is only making sluggish progress, while the operating margin of the Services segment continues to grow. While the New Equipment segment's operating margin shows a weak negative correlation with time (r = -0.1), the company's strong emphasis on service-related revenue, cost discipline and pricing power resulted in a fairly pronounced positive correlation of consolidated operating margin with time (r = +0.6). Figure 3 nicely illustrates the strength of Otis' business model. The company does not need to make a lot of money on its new elevator and escalator installations. Once the installation is complete, the operator is more or less locked into Otis' service offering.

{kind=link}

Figure 3: Otis Worldwide Corp. (OTIS): Segment operating margin comparison (own work, based on company filings)

However, the growing importance Otis is placing on service-related revenues is not only beneficial to the company's overall profitability. It is fair to say that this part of the portfolio is quite recession resistant, and we can already see that today. While adjusted sales of new equipment remained virtually unchanged in the third quarter and the first nine months of the year, services sales increased by more than 10% in the third quarter and 7.2% in the first nine months of 2023. The segment's operating profit rose by 14.6% in the third quarter and by 10.0% in the first nine months of the year. These are very good results considering that 64% of the company's U.S. workforce is covered by collective bargaining agreements (p. 10, 2022 10-K ).

Strong sales growth in the company's services segment (averaging 4.1% since Q1 2020) and a growing share of total sales (so far 60% in 2023) reinforce the impact of this high-margin business on the consolidated operating margin. Although Otis' profitability in the New Equipment segment remains quite muted at 6.4%, overall operating profitability has improved by 110 basis points when comparing the first nine months of 2023 with the same period in 2020 (recall Figure 3).

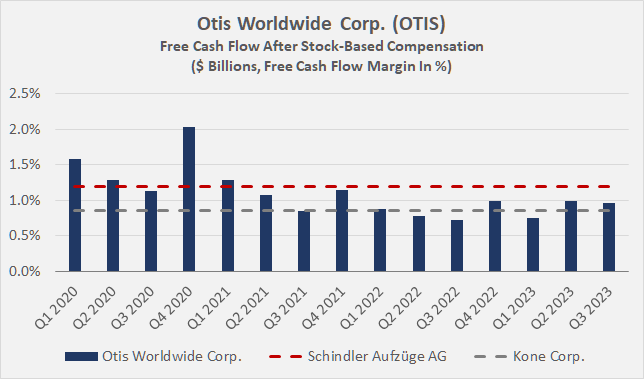

With this in mind, it is not surprising that the company has a very healthy free cash flow margin (three-year average of 9.3%) as well as good cash flow growth and conversion (the latter is expected at 105% of GAAP net income for 2023) (Figure 4). In this context, the low capex/sales ratio, which is typical for the industry, should be emphasized. Elevator companies generally reinvest only around 1% of their annual revenues back into the business. Figure 5 nicely illustrates the progress made by Otis' management since the spin-off from United Technologies in 2020 - the capex/sales ratio is now on par with competitors Schindler and Kone (Figure 5).

{kind=link}

Figure 4: Otis Worldwide Corp. (OTIS): Free cash flow, excluding stock-based compensation (own work, based on company filings)

{kind=link}

Figure 5: Otis Worldwide Corp. (OTIS): Capex/sales ratio compared with peers Schindler and Kone (own work, based on company filings)

Considering that Otis currently distributes only around 50% of its free cash flow to its shareholders and non-controlling interests in the form of dividends (significantly lower since 2022 due to the acquisition of most of the outstanding shares of Zardoya Otis S.A.), there is ample scope for share buybacks, provided the balance sheet allows for such additional return of cash to shareholders. A look at the updated maturity profile of Otis' debt (Figure 6) confirms that the company benefits from a very low weighted-average interest rate - currently around 2.3% - but maturities are slightly more skewed towards the earlier years.

{kind=link}

Figure 6: Otis Worldwide Corp. (OTIS): Maturity profile in three-year buckets, as of September 30, 2023 (own work, based on company filings)

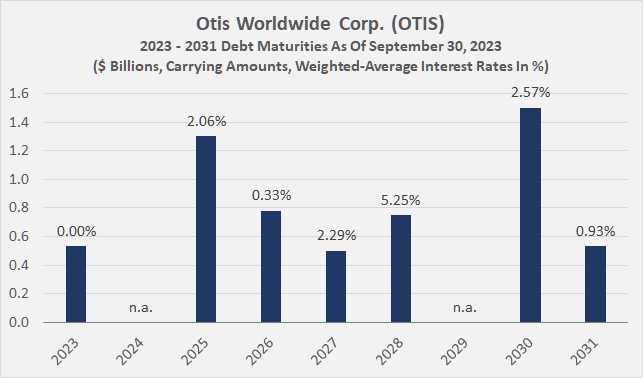

Admittedly, due to the low weighted-average interest rates and comparatively pronounced near-term maturities, the current interest rate environment represents a headwind if one assumes a "higher for longer" scenario. However, looking at upcoming maturities in detail, I do not believe the impact will be overly significant (Figure 7). Even if we assume that the company refinances all its debt maturing by 2027 at an interest rate of 5.0%, its interest expense would increase by a manageable $100 million.

{kind=link}

Figure 7: Otis Worldwide Corp. (OTIS): 2023 – 2031 Debt maturity profile, as of September 30, 2023 (own work, based on company filings)

All in all, I don't think the company will have trouble refinancing its debt, especially given its increasing focus on high-margin service revenues. Personally, I wouldn't mind the company paying down some of its debt as it comes due, considering that debt is somewhat pronounced at four times expected 2023 free cash flow. However, I admit to being rather conservative in terms of capital allocation and understand management's motivation to improve earnings and cash flow per share through buybacks. Finally, the $800 million worth of shares that management plans to retire in 2023 represents 2.4% of Otis' market capitalization.

The Price At Which I Will Buy Otis Stock

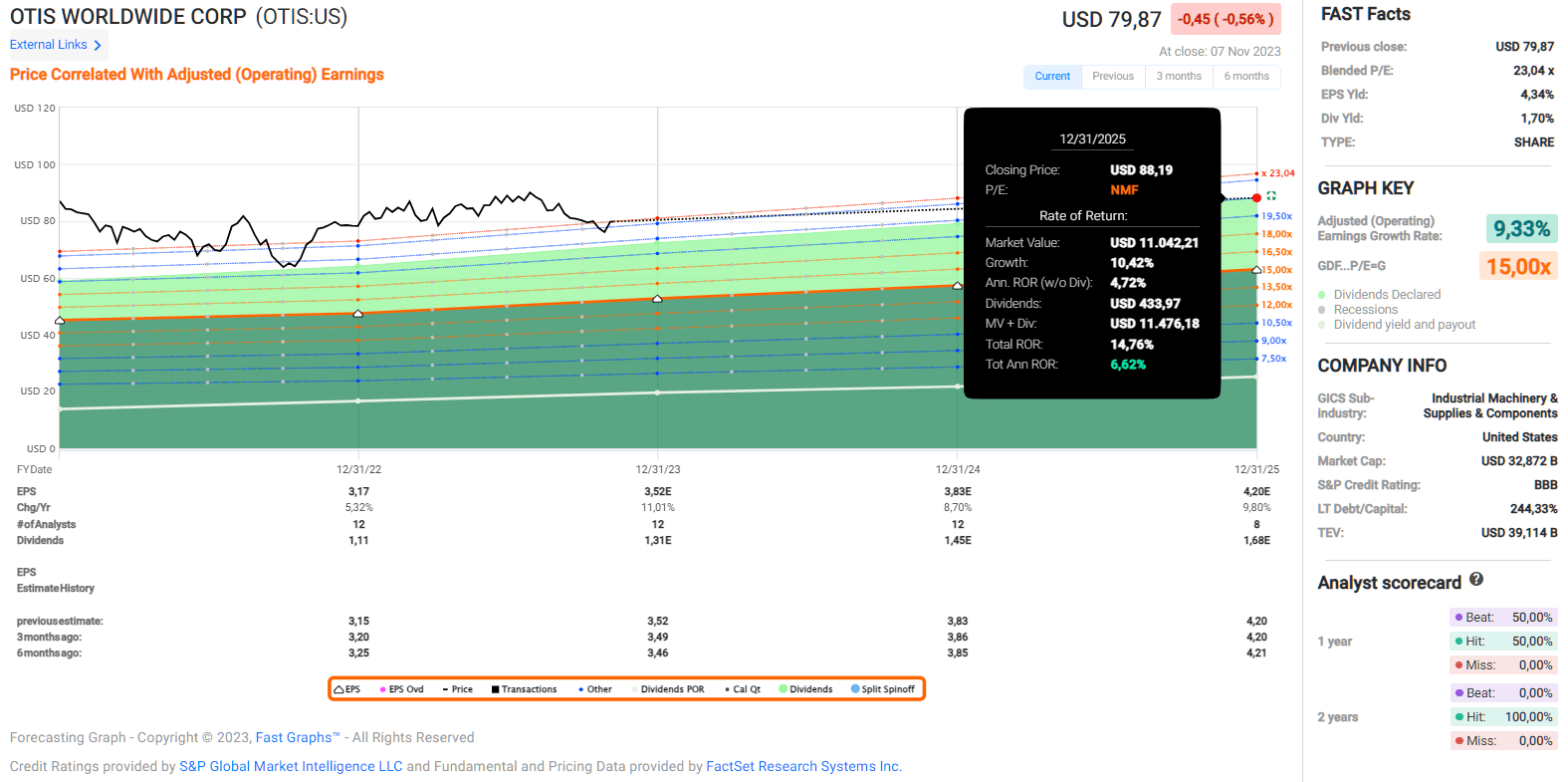

From an earnings per share perspective (which might be tricky given the still modest cyclicality of the business), OTIS stock still looks a bit expensive at $80. If we expect a modest multiple contraction to 21 times adjusted earnings, an annualized return of 6% could be achieved if analysts' estimates are correct (Figure 8). This isn't overly compelling and there is no real margin of safety.

{kind=link}

Figure 8: Otis Worldwide Corp. (OTIS): FAST Graphs forecasting chart, based on adjusted operating earnings per share (FAST Graphs tool)

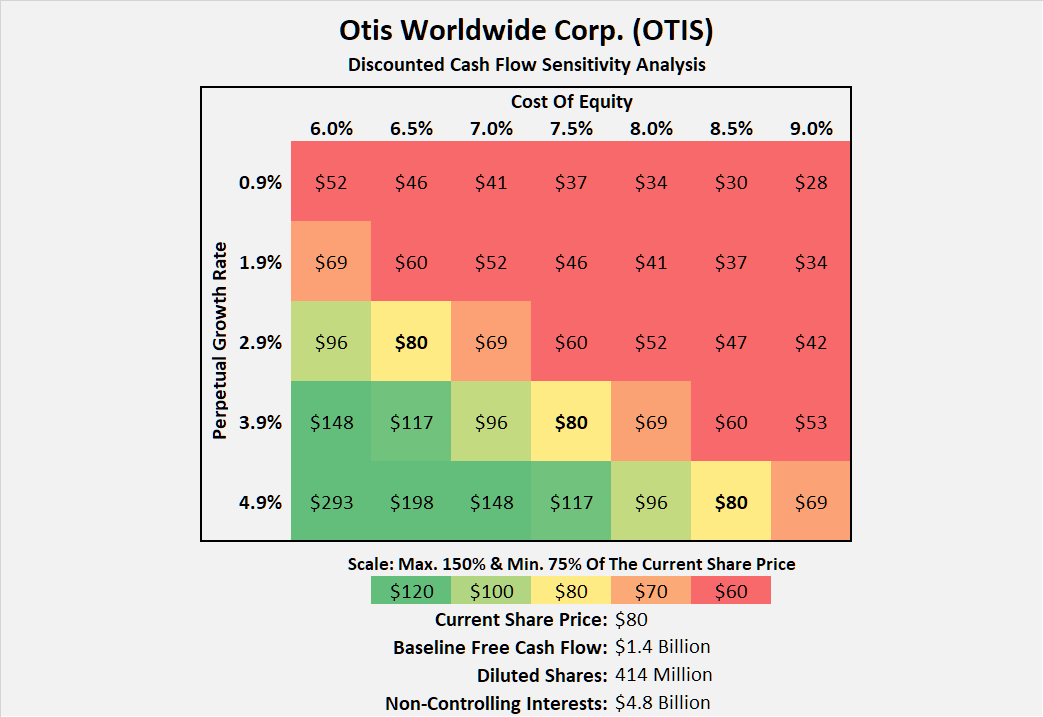

Based on a fairly well-supported baseline free cash flow of $1.4 billion (excluding stock-based compensation), FactSet consensus estimates for free cash flow growth and an expected long-term growth rate of 3%, OTIS shares appear slightly overvalued with a cost of equity of 7.5% (Figure 9). It can be argued that the cost of equity is too low for a still somewhat cyclical company and given the high interest rates (the current risk-free interest rate, measured by the 20-year Treasury , is 4.9%). However, considering that Otis is the market leader in this highly consolidated sector and generates almost 60% of its revenues through services, I think it would be too pessimistic to view the company as a traditional industrial company.

Figure 9: Otis Worldwide Corp. (OTIS): Discounted cash flow model (own work, based on company filings)

However, given the significant contribution of terminal value to the DCF model (65% of the sum of all discounted cash flows), it is only reasonable to perform a more detailed sensitivity analysis than the one presented in Figure 9. If we consider the expected growth in free cash flow in 2024 and 2025 as a kind of "hidden" reserve, the company would have to increase its FCF at an annual rate of around 4% in perpetuity in order for the shares to be fairly valued at a cost of equity of 7.5%. This doesn't seem like an unrealistic expectation given Otis' market-leading position and continued strong modernization of owned and third-party elevators, as well as secular tailwinds (ignoring the current high interest rate environment). However, I am personally skeptical of such high perpetual growth rates and therefore maintain that the stock is modestly overvalued.

{kind=link}

Figure 10: Otis Worldwide Corp. (OTIS): Discounted cash flow sensitivity analysis (own work, based on company filings)

Overall, I think Otis is a wonderful company with a strong moat, solid profitability and shareholder-friendly management. I have it on my watchlist and consider it a valuable addition to my long-term oriented dividend growth portfolio. However, considering the still quite expensive shares and the uncertain economic environment, I will wait for a better entry point before buying a significant position. In the low-$70s, I could see myself opening a position, but I won't be too aggressive until the stock is trading in the mid-$60s or below.

Conclusion

Otis Worldwide, the market leader in elevators, reported somewhat mixed third quarter results. However, to a certain extent, and especially given the sharp rise in interest rates, it is only natural for the demand side of the equation to come under pressure. Against this backdrop, the company's strong order book of New Equipment is very reassuring and gives management a good visibility on earnings, to which it can respond in a timely manner. Apart from this, Otis' Services segment continues to shine and is driving the company forward even in this difficult environment. The sustained sales growth on the one hand and the margin expansion in this segment on the other, more than compensate for the current weak development in the New Equipment segment. Although this is only a hypothesis, I am inclined to say that Otis is deliberately maintaining attractive offers on new equipment sales, as the company eyes the recurring high-margin income from service and maintenance work on its growing installed base. And that's not all: the company is "inorganically" expanding its service portfolio by modernizing and adapting its own older elevators and those of third parties.

From the data discussed in this article, it became clear that Otis is far less cyclical than the current performance of New Equipment would suggest. Free cash flow is very solid and the company is still benefiting from extremely low interest rates on its debt. As the debt matures and assuming interest rates remain high for longer, refinancing at current rates will naturally result in lower interest coverage and consequently a modest headwind to earnings and cash flows. However, given the maturity profile, I think it is reasonable to assume that the impact of higher interest rates will be very manageable. At the same time, I personally do not think it is realistic to expect interest rates to remain at current levels for a very long time, if only from the standpoint of historically high levels of government debt and consequently declining debt servicing capacity.

Consequently, the combination of a growing share of recurring and recession-resistant services income with a solid balance sheet and excellent profitability makes OTIS stock an ideal candidate for my dividend growth portfolio. The payout ratio of 50% of free cash flow (long-term average) is skewed by payments to non-controlling interests, making the current ratio even more conservative. It is only reasonable to expect the company to continue to increase its dividend at a healthy pace, which I believe is important not only from the standpoint of the generally low starting yield (currently 1.7%), but also from the perspective of maintaining and increasing the purchasing power of one's dividend income ( see this article ).

Otis is undoubtedly a wonderful company. However, that doesn't automatically make it a good investment, and at $80 I still think the stock is a bit too expensive. From an earnings and free cash flow perspective, I plan to open a position in the low $70s, but would only go "all-in" (meaning I would invest 1.5% of my portfolio value in OTIS stock, my position limit) if it falls to the mid-$60s or lower.

Thank you for taking the time to read my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.

For further details see:

Otis Worldwide: Why You Should Look Past The New Equipment Slowdown