NEE - Otter Tail: Manufacturing Arm Facing Headwinds But Stock Still Looks Decent

2023-10-17 18:11:40 ET

Summary

- Otter Tail Corporation is a regulated electric utility that also owns manufacturing companies producing industrial plastic components.

- The company's manufacturing subsidiaries have struggled with growth due to recent economic weakness.

- Despite the challenges, Otter Tail Corporation has a stable financial position and is investing in its electric utility business to offset the weakness in manufacturing.

- The company will probably see earnings weakness over the next few years, but this appears to be priced into the stock.

- The current dividend is well covered by free cash flow, and the valuation is quite reasonable.

Otter Tail Corporation ( OTTR ) is a regulated electric utility that serves customers in the U.S. states of Minnesota, North Dakota, and South Dakota. However, this company is more than a simple utility, as it also owns a number of companies that manufacture various industrial plastic components. This sets it apart from typical utilities, as the company is not only purchased by people seeking financial stability and a high dividend yield. In fact, Otter Tail Corporation only has a 2.33% dividend yield at the current price, so it is not especially impressive in that regard. After all, this is lower than the yield of the U.S. Utilities Index ( IDU ).

Rather, the company is sometimes purchased by those investors who are interested in the growth potential possessed by its manufacturing operation. That may be a long-term story, however, as recent economic weakness has caused the company’s manufacturing subsidiaries to struggle in terms of growth. Fortunately, the company still has the benefit of the electric utility’s financial stability to help it weather through whatever may be coming down the pike.

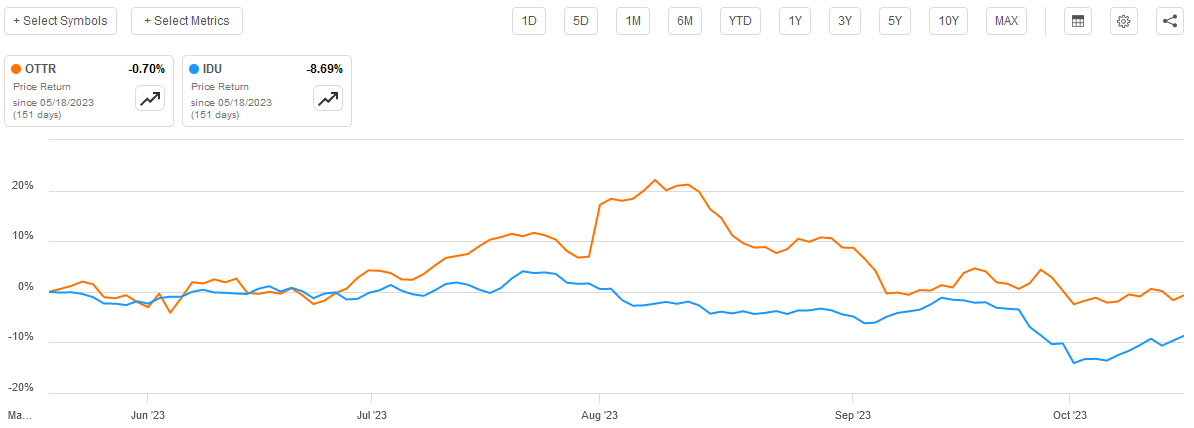

As regular readers may recall, we last discussed Otter Tail Corporation in the middle of May. At that time, market conditions were very different than they are today, as investors were generally optimistic about the potential for a near-term monetary policy pivot and were buying up bonds and keeping yields down. That is different today, as rising rates have caused investors to push down the price of both long-duration assets and most things whose valuation is dependent on yield. This second category includes companies in the utility sector like Otter Tail Corporation. For its part, Otter Tail has held up much better than the rest of the utility sector, however:

{kind=link}

This is fortunate and is almost certainly caused by the company’s manufacturing arm which accounts for a sizable portion of its revenue. The company also has a fairly reasonable valuation at its current level, so it is possible that it was not affected as much when investors started to revalue assets as long-term rates began to increase. Regardless, the fact that the valuation is still fairly reasonable at the moment means that we have not lost our opportunity to get into the stock. Let us try to determine if we want to.

About Otter Tail Corporation

As mentioned in the introduction, Otter Tail Corporation is a rather interesting company that consists of two main segments. The first of these is a regulated electric utility that serves parts of Minnesota, North Dakota, and South Dakota:

{kind=link}

The second segment is a group of manufacturing companies that primarily produce plastic components that are used for industrial purposes. These include things such as PVC pipe, specialty containers, and custom metal stamping.

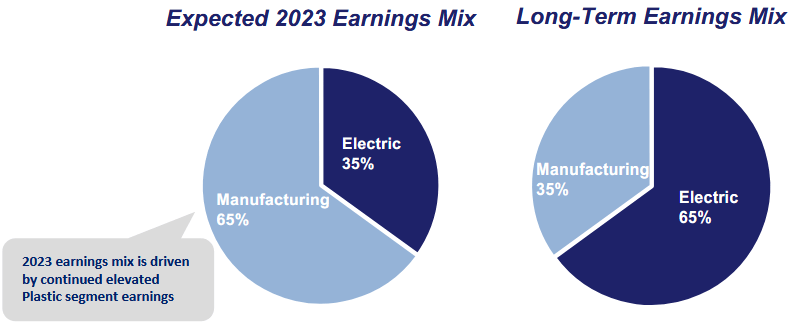

Otter Tail Corporation is therefore part of a very small group of utilities that include operations other than the provision of electricity, natural gas, and water in a certain geographic area. Otter Tail is even more unique in the fact that the utility is the smaller of the two business segments, at least for right now. Otter Tail currently expects that approximately 65% of its 2023 earnings will come from its manufacturing operations. However, long-term it is expected that the two segments will be reversed:

{kind=link}

This, unfortunately, means that Otter Tail is a bit more exposed to economic fluctuations and problems than most other utility companies would be. That is something that might be concerning for those investors who are seeking to buy a company that will prove to be a safe and secure investment in a weakening economic climate.

We are seeing some signs that the economy is weakening right now, particularly in industry. For example, we can look at the Leading Economic Indicators, which are widely considered to be a very accurate measure of economic activity occurring in the economy. According to the most recent data , the Leading Economic Indicators fell by 0.4% in August, which follows a 0.3% decline in July:

The Conference Board Leading Economic Index for the U.S. declined by 0.4% in August 2023 to 105.4 (2016=100), following a decline of 0.3% in July. The LEI is down 3.8 percent over the six-month period between February and August 2023 – little changed from its 3.9 percent contraction over the previous six months (August 2022 to February 2023).

‘With August’s decline, the US Leading Economic Index has now fallen by nearly a year and a half straight, indicating the economy is heading into a challenging growth period and possible recession over the next year,’ said Justyna Zabinska-LaMonica, Senior Manager, Business Cycle Indicators, at the Conference Board. ‘The leading index continued to be negatively impacted in August by weak new orders, deteriorating consumer expectations of business conditions, high interest rates, and tight credit conditions. All these factors suggest that going forward economic activity probably will decelerate and experience a brief but mild contraction. The Conference Board forecasts real GDP will grow by 2.2 percent in 2023, and then fall to 0.8 percent in 2024.’

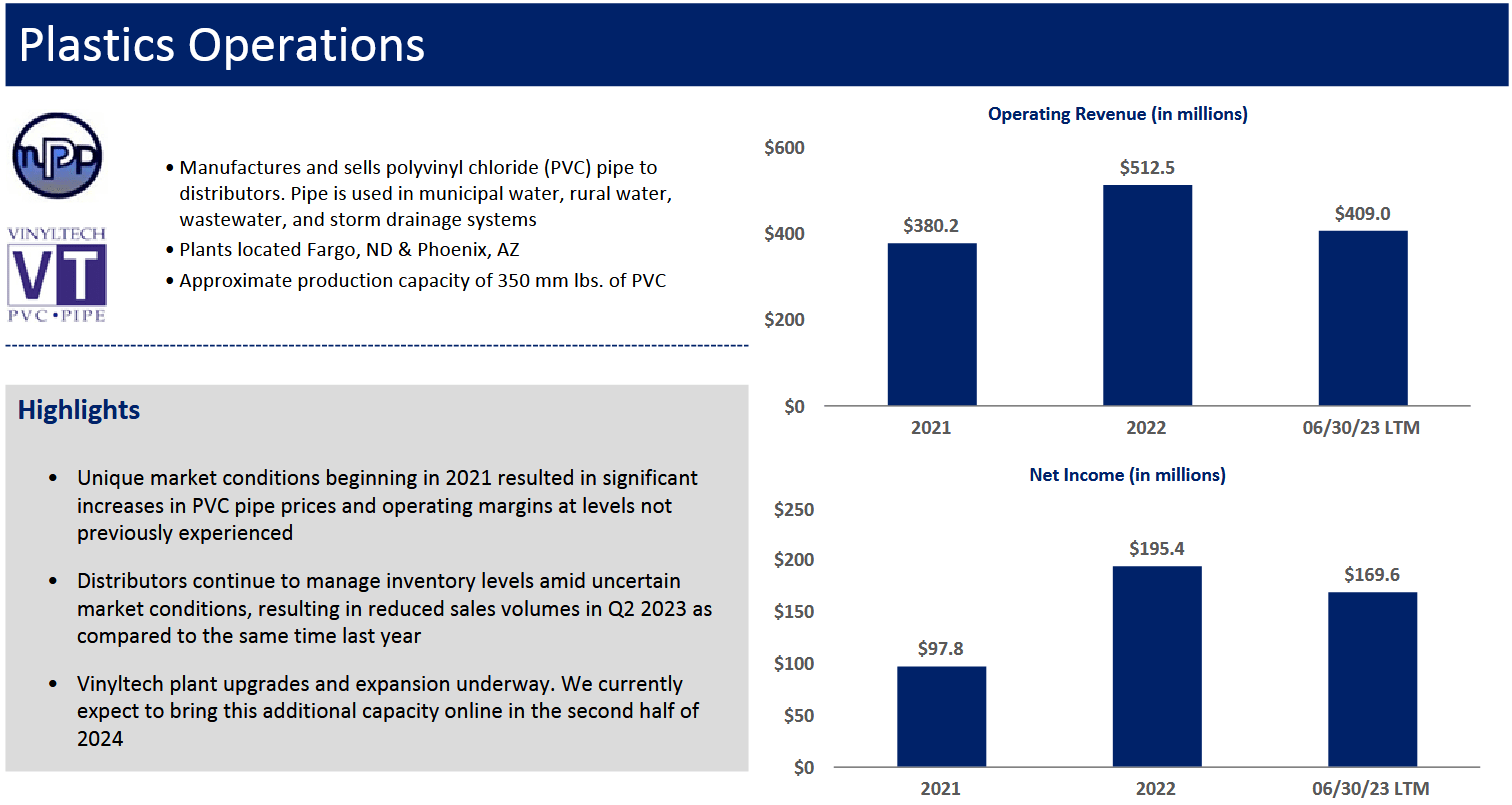

A slowdown in manufacturing activity could have a negative impact on Otter Tail Corporation due to the large impact that the company’s manufacturing operation has on its overall results. In fact, the company has already reported that it is beginning to encounter profit headwinds from this segment of its operations. For example, we can see here that the company’s plastics operations have seen both its revenue and profit drop off quite a bit in the most recent twelve-month period compared to 2022:

{kind=link}

That is by far the largest component of its manufacturing operations, as all of the company’s other manufacturing subsidiaries combined only had $22.1 million in net income during the trailing twelve-month period. That was a $1.1 million increase over the full-year 2022 period, but a $1.1 million increase from the BTD and T.O. Plastics subsidiaries in aggregate cannot offset a $25.8 million profit decline from the plastics operation. The electric utility managed to grow its net income by $4.7 million over the period, but even that was not enough to offset the headwinds from an uncertain economic climate. After all, the slide above from the company specifically states that the problem that this business is encountering is weaker sales volumes as industrial customers are uncertain about the forward direction of the economy. This is exactly what the Leading Economic Indicators also point to.

That is unfortunate, as one of the nice things about electric utilities is that they tend to enjoy incredible financial stability regardless of economic conditions. In fact, as I pointed out in my last article on this company, people tend to prioritize paying their electric bills during periods in which money gets tight. After all, electricity is a necessity. While this means that the electric utility should be able to provide a bastion of stability for this company, it only accounts for a minority of the company’s profits so it will not be able to completely overcome the weakness that we see in manufacturing.

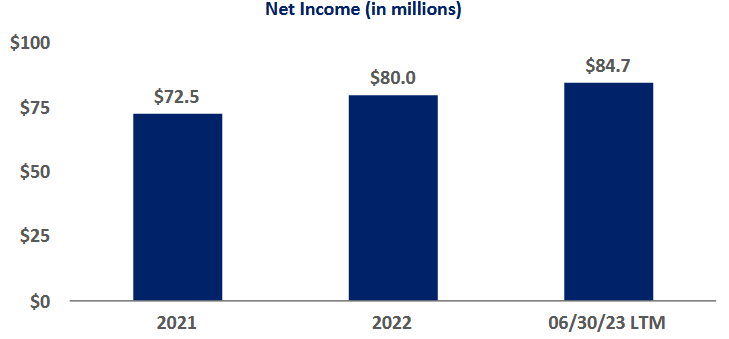

The electric utility reported a net income of $84.7 million over the past twelve months, which confirms the earlier statement that this business is less important to Otter Tail’s near-term financial performance than its manufacturing operation. However, the utility’s net income has been consistently growing, as we can see here:

{kind=link}

This business should be able to continue this growth going forward, even if economic growth stalls or even if the economy contracts. The primary way that it will do this is by growing its rate base. As I explained in my previous article on Otter Tail:

The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the company’s rate base allows it to increase the prices that it charges its customers in order to earn that specified rate of return.

The usual way that a utility grows its rate base is by investing money into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure.

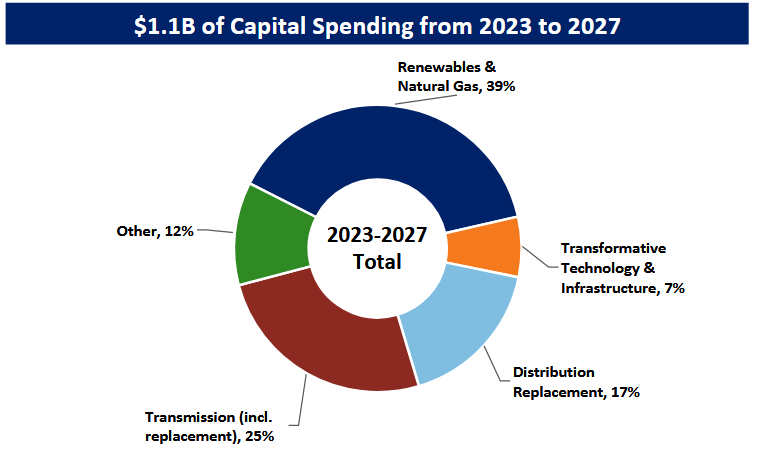

Otter Tail Corporation is planning to make some investments to grow its rate base. In fact, the company is currently in the midst of a $1.1 billion capital investment program spanning from 2023 to 2027 that is intended to do exactly that:

{kind=link}

This program is expected to grow the company’s rate base at a 6.5% compound annual growth rate over the 2022 to 2027 period. The company has not stated exactly what impact it expects this program will have on its earnings, but it should result in the electric utility business segment delivering a net income growth rate that is pretty close to that level. This would therefore help to offset some of the earnings weakness from the company’s manufacturing operations, however, it is still quite likely that Otter Tail’s financial performance will decline over the next year or two as the utility company is not a large enough contributor to the company’s finances to completely offset the weakness there.

Financial Considerations

As I explained in my previous article on Otter Tail Corporation:

It is always important to look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the money to repay the existing debt. This can cause a company’s interest expenses to increase following the rollover, depending on the conditions in the market.

Right now, interest rates are at the highest levels that we have seen since February 2001. This has already begun to weigh on the financial performance of other utility companies, which I pointed out in a recent article . As such, a high level of leverage is a bigger problem today than it has been over most of the past two decades.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. As of June 30, 2023, Otter Tail Corporation had a net debt of $723.6 million compared to $1.3284 billion of shareholders’ equity. This gives the company a net debt-to-equity ratio of 0.54 today. This is nice as it is a clear indication that the company has sufficient equity to completely pay off all of its debt in a worst-case scenario. This is a rarity for a utility, although it seems likely that the more cyclical manufacturing operation has caused management to be somewhat more conservative with the company’s use of debt.

Here is how Otter Tail Corporation compares to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Otter Tail Corporation |

| 0.54 |

| DTE Energy ( DTE ) |

| 1.89 |

| NextEra Energy ( NEE ) |

| 1.30 |

| Eversource Energy ( ES ) |

| 1.58 |

| Exelon Corporation ( EXC ) |

| 1.68 |

As we can see, Otter Tail Corporation is by far the least leveraged company out of its peer group. This is not surprising, since this company is one of the only utilities in the industry that is more reliant on equity than on debt to finance its operations. This is a very good sign though, as it clearly indicates that investors should not have to worry too much about the company’s financial structure or the impact that its debt will have on its financial performance. After all, as we can see here, the company’s interest expenses have not really changed that much over the past three years:

{kind=link}

Thus, for those investors who are worried about the impact of rising debt servicing expenses across the companies in their portfolios, there is no real reason to be concerned here.

Dividend Analysis

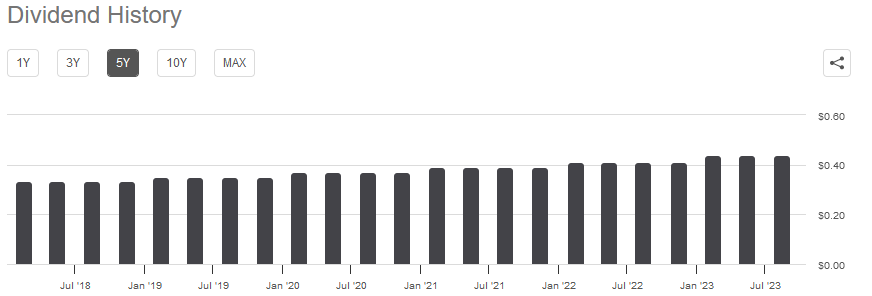

One of the biggest reasons why investors purchase shares of utility companies is because they tend to have relatively high dividend yields. Otter Tail is not a pure-play utility, but the company does still derive 35% of its net income from its utility operation and it expects that figure to be more than half over the long term. The company also has a 2.33% dividend yield at the current price, which is substantially higher than the 1.49% yield of the S&P 500 Index (SP500). Unfortunately, Otter Tail’s current yield does compare fairly poorly to the U.S. Utilities Index, which yields 2.94% today. Fortunately, the company has a long history of raising its dividend over time:

{kind=link}

If we assume that this dividend growth trend continues, investors who purchase the stock today will end up with a much higher yield-on-cost after only a few short years, which helps to offset the fact that its current yield is pretty low. It is also nice to see dividend growth right now considering that inflation still remains high. After all, the fact that the company pays a higher amount every year helps to ensure that we can buy the same goods and services with the company’s dividends year to year.

As is always the case, it is critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual way that we judge a company’s ability to pay its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, Otter Tail Corporation had a levered free cash flow of $81.3 million. This was sufficient to cover the $70.9 million that the company paid out in shareholder dividends over the period. Thus, it does appear that the company can afford the dividend.

We can draw further confidence in the safety of the dividend in the fact that the company’s levered free cash flow has been higher than its dividends during every twelve-month period extending back to the second quarter of 2022. Thus, we should not need to worry too much here.

Valuation

Unfortunately, Zacks Investment Research estimates that Otter Tail Corporation’s earnings per share will decline this year. The analytics firm projects an earnings per share figure of $5.79 this year compared to $6.78 per share last year. I likewise expect that this year will prove to be weaker than last year due to the challenges facing its manufacturing arm that we discussed in this article.

However, the stock still has a very reasonable valuation right now. The stock has a forward price-to-earnings ratio of 12.99 at the current price based on that earnings per share projection. Here is how the stock compares to its peers:

| Company |

| Forward P/E |

| Otter Tail Corporation |

| 12.99 |

| DTE Energy |

| 15.86 |

| NextEra Energy |

| 17.47 |

| Eversource Energy |

| 12.86 |

| Exelon Corporation |

| 17.07 |

As we can clearly see here, Otter Tail Corporation compares very reasonably to its peers in terms of valuation right now. This is nice to see as it is a clear sign that right now would be a reasonable place to enter the stock if you want it.

Conclusion

In conclusion, Otter Tail Corporation is likely to encounter earnings headwinds as its manufacturing arm contends with a weakening economy. However, this is priced into the stock already and the current valuation is very reasonable compared to the company’s peers. Otter Tail continues to boast a very attractive balance sheet and a high free cash flow to cover its dividend. The yield is admittedly not very impressive, but the company’s dividend growth should result in investors receiving a reasonable yield-on-cost in a few years. Overall, the company looks like a very reasonable purchase right now.

For further details see:

Otter Tail: Manufacturing Arm Facing Headwinds, But Stock Still Looks Decent