NEE - Otter Tail: Positioned For Any Economy And Has An Attractive Valuation

2023-05-18 18:10:23 ET

Summary

- Otter Tail Corporation is unique in that it owns a manufacturing business that accounts for a significant amount of its income.

- The company's electric utility provides a baseline level of cash flow regardless of economic conditions.

- Otter Tail should have upside exposure to a strong economy and prove resilient in weak ones due to the nature of its businesses.

- The company has a strong balance sheet and should be able to maintain its dividend going forward.

- Otter Tail Corporation is trading at a reasonably attractive valuation.

Otter Tail Corporation ( OTTR ) is a regulated electric utility serving parts of Minnesota, North Dakota, and South Dakota. The company is more than just an electric utility, however, which makes it quite unique. In addition to providing electricity to homes and businesses throughout its service area, the company also owns a few manufacturing companies, which primarily manufacture plastic industrial and commercial products.

Despite the presence of non-utility operations, the company still enjoys many of the characteristics that we usually associate with electric utilities such as very stable cash flows over time. This is evidenced in the company's first-quarter results, which showed slow but steady year-over-year growth. These are the characteristics that have made utilities in general some of the most popular investments for retirees and other conservative investors, along with their high dividend yields.

For its part, Otter Tail Corporation yields 2.30% at the current price, which is quite a bit higher than the S&P 500 Index ( SP500 ) but admittedly not as good as some other utilities possess. As I discussed in my last article on the company, though, there are some very good reasons to consider including Otter Tail Corporation in your portfolio today. Let us investigate and see if this company makes sense as an investment for you.

About Otter Tail Corporation

As stated in the introduction, Otter Tail Corporation is a regulated electric utility that serves customers in parts of Minnesota and both Dakotas:

{kind=link}

This is one of the most rural areas of the country, which certainly shows up in Otter Tail Corporation's customer count. Unlike most of its peers, Otter Tail does not provide a customer count in its earnings reports but U.S. Census data states that the company's service territory contains 104,396 residential properties and a total of 134,150 residential and commercial properties as of mid-2022. That is probably a reasonable estimate of the customer base of Otter Tail's utility operations. That is a surprisingly small number of customers considering the geographic size of this service territory, but this does not prevent the company from possessing many of the qualities that conservative risk-averse investors appreciate in utility companies.

Perhaps the most important of these characteristics is that these companies have remarkably stable cash flows over time. We can see that by looking at Otter Tail Corporation's operating cash flows. Here they are for the past eleven trailing twelve-month periods:

{kind=link}

As we can see, while Otter Tail Corporation's operating cash flows did grow over time, there was surprisingly limited variation from one quarter to another. This comes from the fact that electricity service to a home or business is generally considered to be a necessity for modern life. As such, most people will prioritize paying their electric bills ahead of making discretionary expenses during periods in which money gets tight. That is especially important today since, as I pointed out in a recent blog post , the incredibly high inflation rate in the United States over the past eighteen months or so has strained the household finances of a great many people. This would be particularly true for people of limited means, which would include a significant percentage of the company's customer base. Thus, the fact that these people will likely make sure that their utility bill gets paid even if they have to make sacrifices in other areas of their lives is a quality that we very much like to see in a company in our portfolio. As there are numerous signs pointing to the possibility of a recession in the near future, this is doubly true.

Although the company is generally described as a utility, it does have some other businesses that have no particular relationship to utilities. This is similar to how Hawaiian Electric Industries, Inc. ( HE ) owns a bank. However, in Otter Tail Corporation's case, the company's non-utility operations are manufacturing firms. I discussed each of the manufacturing businesses in great detail in a previous article on Otter Tail Corporation so there is no need to do so again. The important thing is that the company's businesses primarily manufacture plastic containers, PVC pipes, and other industrial plastic items. The company also owns a metal stamping business.

{kind=link}

These businesses are actually more profitable than the electric utility. Thus, unlike peers, Otter Tail Corporation can be thought of as a manufacturing conglomerate with a utility company attached instead of the other way around. As we can see here, the manufacturing companies had significantly higher operating income than the utility company during both the first quarter of 2023 and the full-year 2022 periods:

Otter Tail Corporation

The two operations were much more equal in this respect back during the pandemic and the 2021 recovery phase. This is important to consider now that the country may be heading into a recession. The utility business is likely to prove much more recession-resistant than the manufacturing companies. As such, the utility basically provides a baseline amount of profit and cash flow that the company should be able to maintain during any economic conditions. The manufacturing arm, meanwhile, allows Otter Tail Corporation to benefit from strong economies in a way that other utilities cannot.

The fact that the company's manufacturing arm has accounted for an outsized portion of its performance over the past few years does not mean that it is neglecting its utility business. In fact, the electric utility is positioned to deliver respectable growth over the next few years. As it cannot count on a rapidly growing customer base in its area, Otter Tail Corporation is planning to grow its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the company's rate base allows it to increase the prices that it charges its customers in order to earn that specified rate of return.

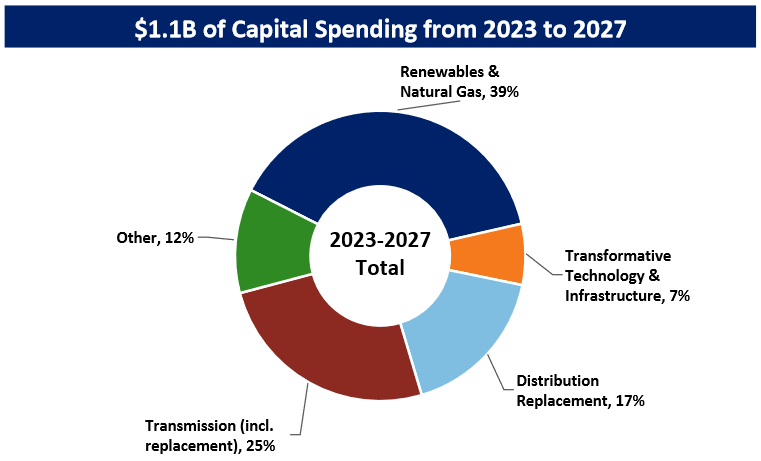

The usual way that a utility grows its rate base is by investing money into upgrading, modernizing, or possibly even expanding its utility-grade infrastructure. Otter Tail Corporation is planning to do exactly this, as the company recently outlined a $1.1 billion five-year capital investment program:

{kind=link}

As we can see, the company plans to invest approximately $1.1 billion into its utility-grade infrastructure over the next five years. This should grow its rate base at a 6.5% compound annual growth rate over the period, taking it from $1.62 billion at the start of this year to $2.23 billion by the end of 2027. As may be immediately apparent, this rate base growth will be somewhat less than the amount of money that Otter Tail Corporation is planning to spend. There are two reasons for this. The first of these is depreciation, which constantly reduces the value of the assets that the company places into service. As a result, something that it puts into service this year will have a lower value and a lower impact on the rate base in 2027. Thus, the company must spend enough to offset depreciation and still grow the rate base.

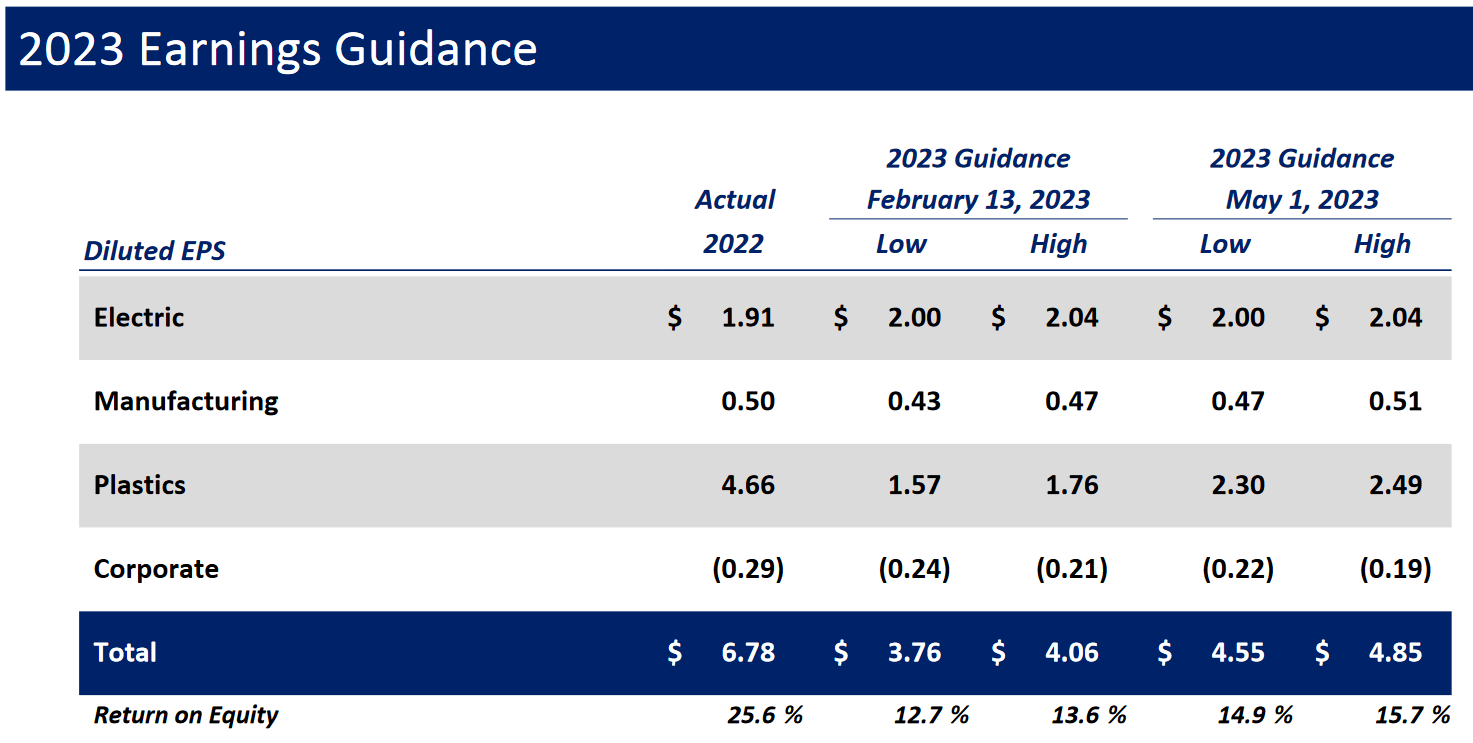

In addition to this, the company will be removing some things from service and replacing them with new things. The value of the things that are removed from service is permanently subtracted from the rate base, which offsets some of the value of the new equipment. The rate base growth is likely to grow the earnings per share of the electric utility by 4.70% to 6.80% over the next year and Otter Tail Corporation has provided guidance to this effect:

{kind=link}

However, as the electric utility is only expected to account for approximately 43% of the company's earnings this year, we cannot rely on this as an accurate way to estimate a total return for the stock over the entire five-year period. After all, the performance of the manufacturing company is dependent on the broader economy, and it seems likely that a near-term recession will hit and weaken this business. The question is how severe the recession will be, and I have seen projections by economists that are all over the place. As already mentioned, Otter Tail Corporation is much better positioned to weather such an event than many other companies due to the inherent stability of the electric utility.

Financial Considerations

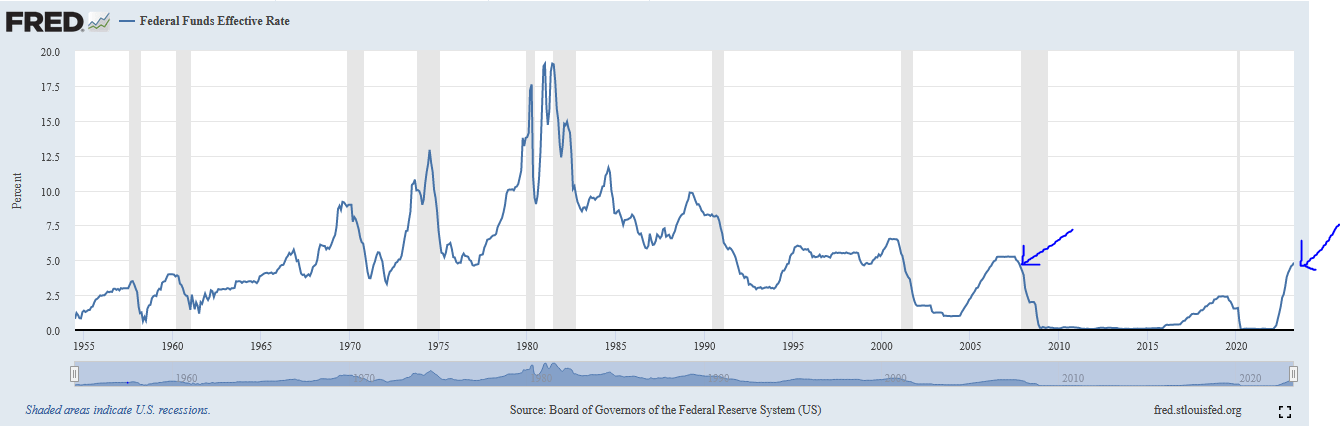

It is always important to look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt and using the money to repay the existing debt. This can cause a company's interest expenses to increase following the rollover, depending on the conditions in the market. This is an especially big concern today because the federal funds rate is currently at the highest rate that we have seen since 2007:

{kind=link}

As the interest rate that companies pay on their debt is directly linked to the federal funds rate, this undoubtedly means that any debt currently being rolled over will probably carry a higher interest rate than the company has been paying on it. In addition to this risk, a company must make regular payments on its debt if it is to remain solvent. Thus, any event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. Although utilities typically have remarkably stable cash flow, Otter Tail Corporation is not a pure utility, so it has somewhat greater risks than other companies in the sector.

One way that we can analyze a company's financial structure is by looking at its net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us how well a company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of March 31, 2023, Otter Tail Corporation had a net debt of $780.7 million against $1.2638 billion of shareholders' equity. This gives the company a net debt-to-equity ratio of 0.62 today, which is a significant improvement compared to the last time that we looked at this company. Here is how the company's net debt-to-equity ratio compares to other utility companies:

| Company |

| Net Debt-to-Equity Ratio |

| Otter Tail Corporation |

| 0.62 |

| DTE Energy ( DTE ) |

| 1.83 |

| NextEra Energy ( NEE ) |

| 1.29 |

| Eversource Energy ( ES ) |

| 1.49 |

| Exelon ( EXC ) |

| 1.65 |

We can clearly see that Otter Tail Corporation has a substantially lower debt load and overall, less reliance on debt to finance itself than most utilities. However, this has generally always been the case with this company, as I have pointed out in numerous previous articles. The reason for this is the company's manufacturing arm, which does not have the same cash flow stability as a pure electric utility so cannot support as heavy a debt load. The fact that Otter Tail Corporation has a stronger balance sheet than the last time that we looked at it is quite nice to see and investors in the company should not have to worry too much about the debt load.

Dividend Analysis

One of the reasons that investors purchase utility stocks is that they usually have a higher yield than most other things. Although Otter Tail Corporation is not a pure utility, it is still frequently thought of as one so it makes sense that the dividend will attract investors. As stated in the introduction, the stock yields 2.30% at the current price, which is higher than the 1.56% current yield of the S&P 500 Index, but it is not as high as the 2.54% of the U.S. Utilities Index ( IDU ). Fortunately, Otter Tail Corporation does have a long history of raising its dividend annually:

{kind=link}

The fact that the company increases its dividend every year is something that is very nice to see, especially in periods of high inflation like the one that we are experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time. The fact that the company increases its dividend over time helps to offset this effect and maintains the purchasing power of the dividend. In addition, after a few years of dividend increases, we will be receiving a very attractive yield on our initial investment.

As is always the case though, it is important that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our income and almost certainly causes the company's stock price to decline.

The usual way that we judge a company's ability to afford its dividend is by looking at its free cash flow. Free cash flow is the cash that was generated by the company's ordinary operations and is left over after it pays all its bills and makes all necessary capital expenditures. This is the money that is available for tasks such as repaying debt, buying back stock, or paying a dividend. In the twelve-month period that ended on March 31, 2023, Otter Tail Corporation reported a levered free cash flow of $79.0 million. The company paid $69.8 million in dividends over the period. As such, it appears that its free cash flow is sufficient to cover the dividend, so we should not really need to worry about the company's ability to maintain its dividend going forward.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility or a manufacturer, we can value it by looking at the forward price-to-earnings ratio. This ratio tells us how much we would have to pay today for each dollar of earnings that the company is expected to earn over the next year.

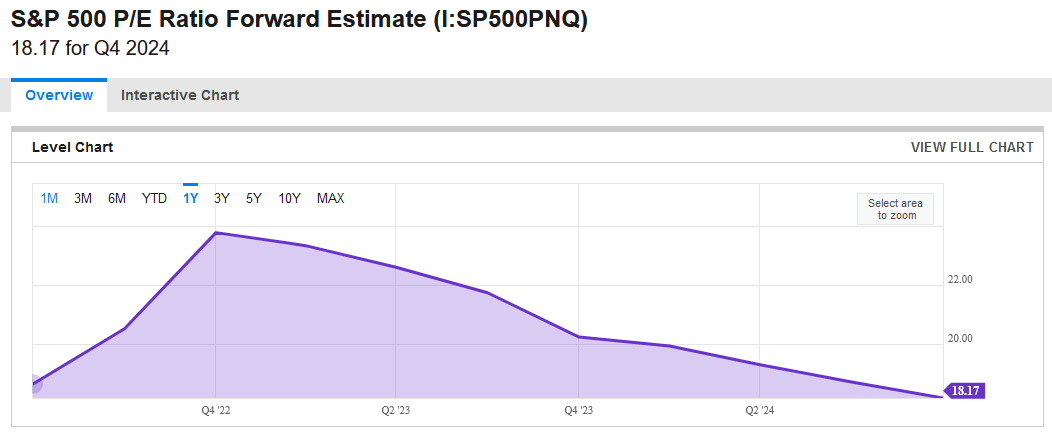

According to Zacks Investment Research , Otter Tail Corporation has a forward price-to-earnings ratio of 16.14 at the current stock price. This is less than the 18.17 forward price-to-earnings ratio of the S&P 500 Index:

{kind=link}

Thus, it appears that Otter Tail Corporation is cheaper than the market as a whole. This is a good sign, but let us see how it compares to our aforementioned peer group:

| Company |

| Forward P/E Ratio |

| Otter Tail Corporation |

| 16.14 |

| DTE Energy |

| 17.65 |

| NextEra Energy |

| 24.25 |

| Eversource Energy |

| 17.00 |

| Exelon Corporation |

| 16.72 |

This is actually pretty nice to see as Otter Tail Corporation currently looks cheaper than this collection of pure-play utilities. When we consider that the company's manufacturing arm gives it growth potential that exceeds the utility sector during periods of economic strength, this appears to be pointing to Otter Tail Corporation being undervalued at the current price.

Conclusion

In conclusion, Otter Tail Corporation is a unique entity in the utility sector due to the fact that a sizable proportion of its profits come from a manufacturing operation. This gives the company the recession-resistance of the utility as well as superior performance during periods of economic strength. The near-term economic outlook is uncertain, to say the least, but the fact that Otter Tail appears reasonably positioned for any scenario is rather appealing.

Otter Tail Corporation's valuation does not appear to reflect this though as it is quite reasonably priced, appears able to maintain its dividend, and boasts a remarkably attractive balance sheet. Otter Tail Corporation might be worth considering for a portfolio today.

For further details see:

Otter Tail: Positioned For Any Economy And Has An Attractive Valuation