DUK - Otter Tail: The Tail Wagging The Company

2023-11-30 10:18:07 ET

Summary

- Otter Tail is a regulated utility serving Minnesota, North Dakota, and South Dakota with decent growth and stable margins.

- The company's plastics business experienced significant revenue growth and margin expansion due to unique market conditions in 2021.

- In my view, the stock is not properly discounting a true normalization of earnings, and a target price closer to $50 is more reasonable.

Basic Thesis:

Otter Tail ( OTTR ) is a regulated utility serving Minnesota, North Dakota and South Dakota. It also owns a manufacturing and plastics business. The utility is a perfectly fine operation. Decent growth and stable margins with a solid move to renewables.

Utility Business Mix (OTTR Company Presentation)

{kind=link}

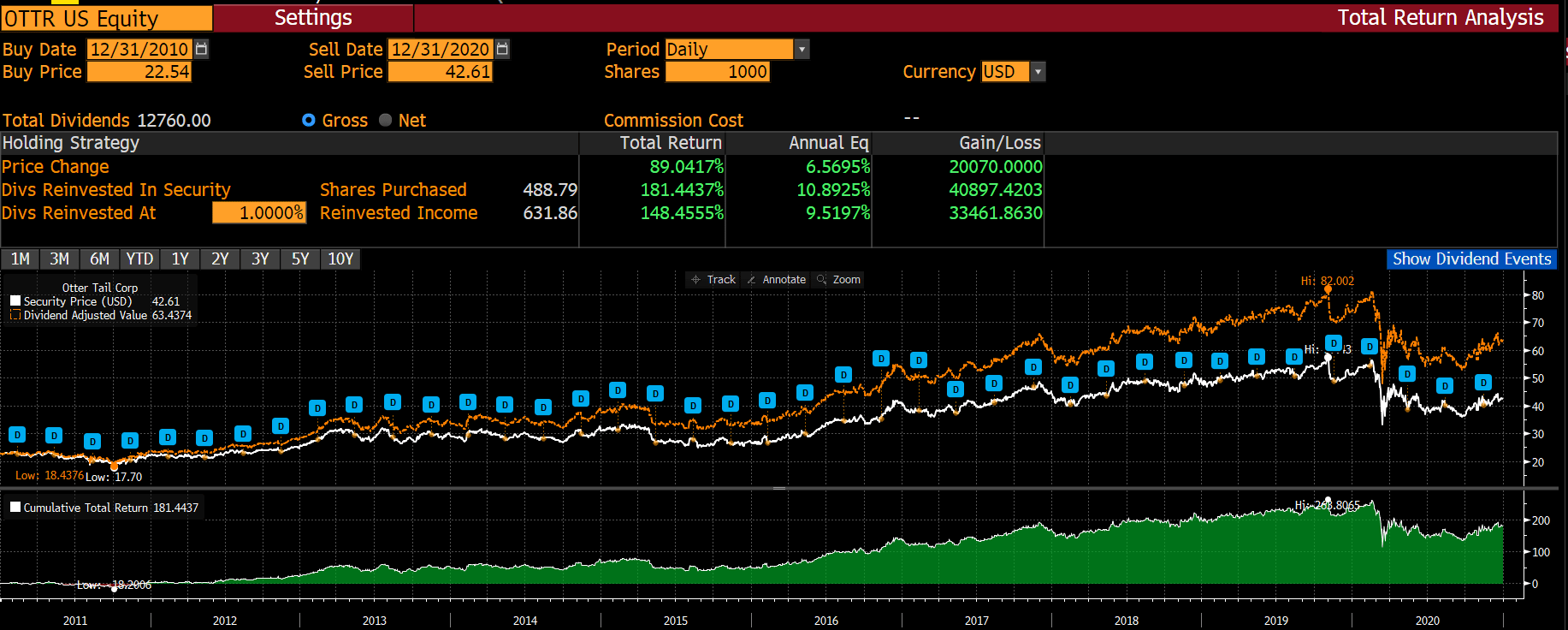

I don't think anyone would ever consider Minnesota or the Dakotas wonderful growth venues. But the utility is a stable, widow and orphan performer and historically has been the main profit driver of solid if boring performing stock.

OTTR Total Return from 2010-2020 (Bloomberg)

{kind=link}

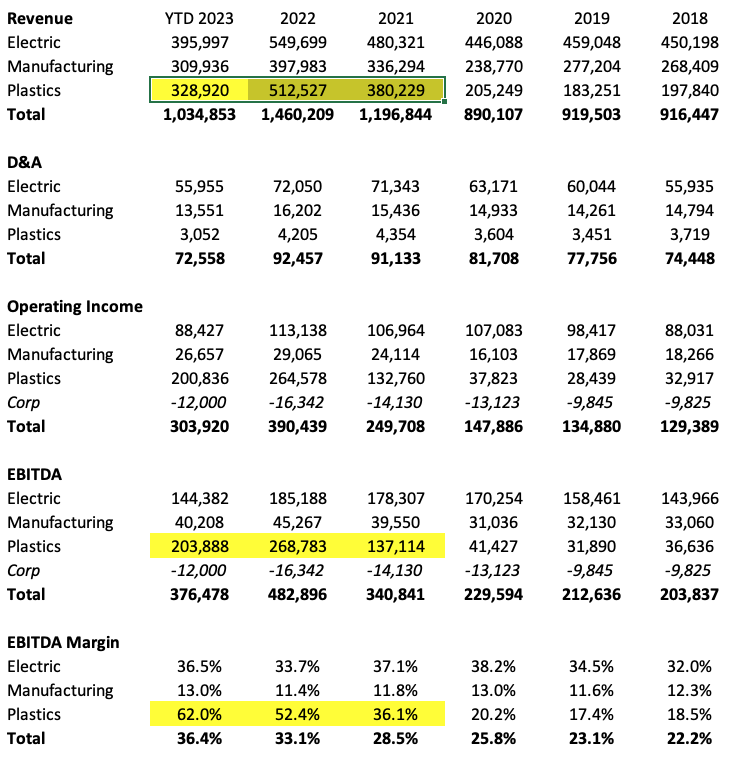

The Covid Bump

Covid had an enormous impact on the company's business, particularly its revenue and profit mix. As you can see below, prior to 2021, the utility dominated operating income and EBITDA.

OTTR Revenue and Profit by Segment (OTTR 10-K and 10-!Q)

{kind=link}

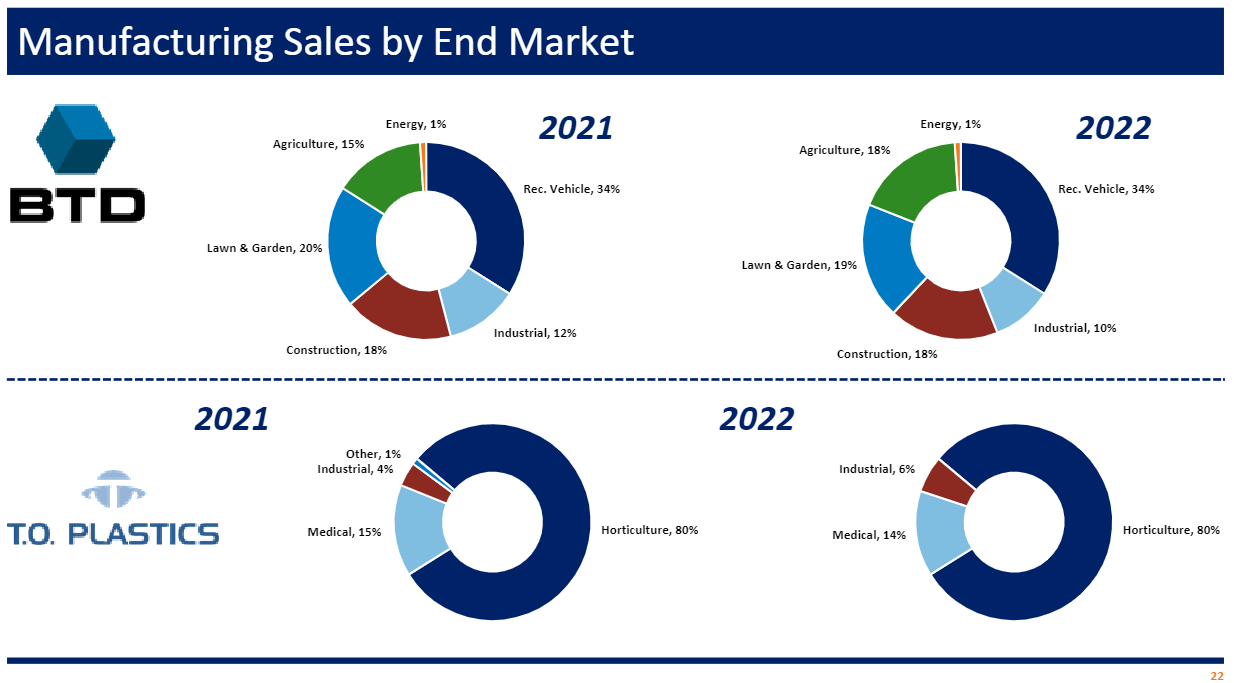

Manufacturing has diverse end markets and plastics are dominated by PVC water and sewer piping primarily for the horticultural industry.

OTTR Manufacturing and Plastics Business (OTTR Company Presentation)

{kind=link}

As you can see above, none of the end markets are highfliers. However, starting in 2021, plastics experienced insane revenue growth and margin expansion. As the company describes it: Unique market conditions beginning in 2021 resulted in significant increases in PVC pipe prices and operating margins at levels not previously experienced.

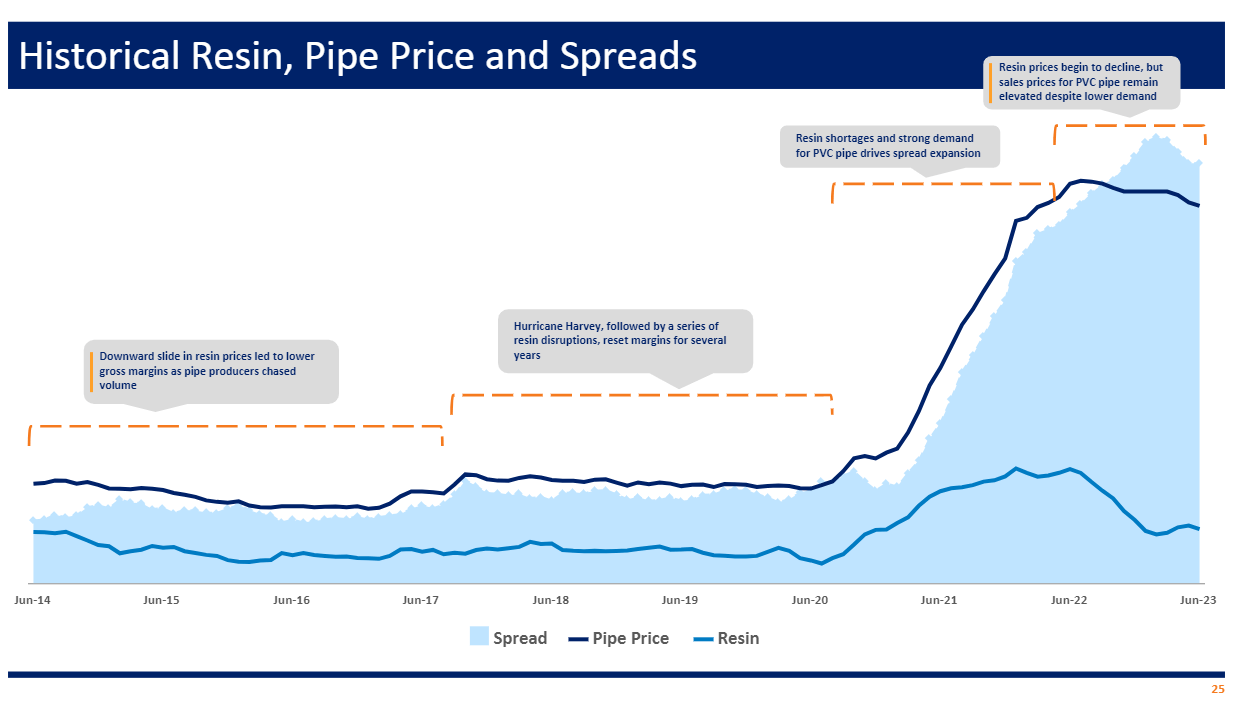

In short, there was a massive supply/demand imbalance in PVC. Those who could supply pipe made hay. The below offers a great visualization of the PVC boom.

Historical Resin Prices (OTTR Company Presentation)

{kind=link}

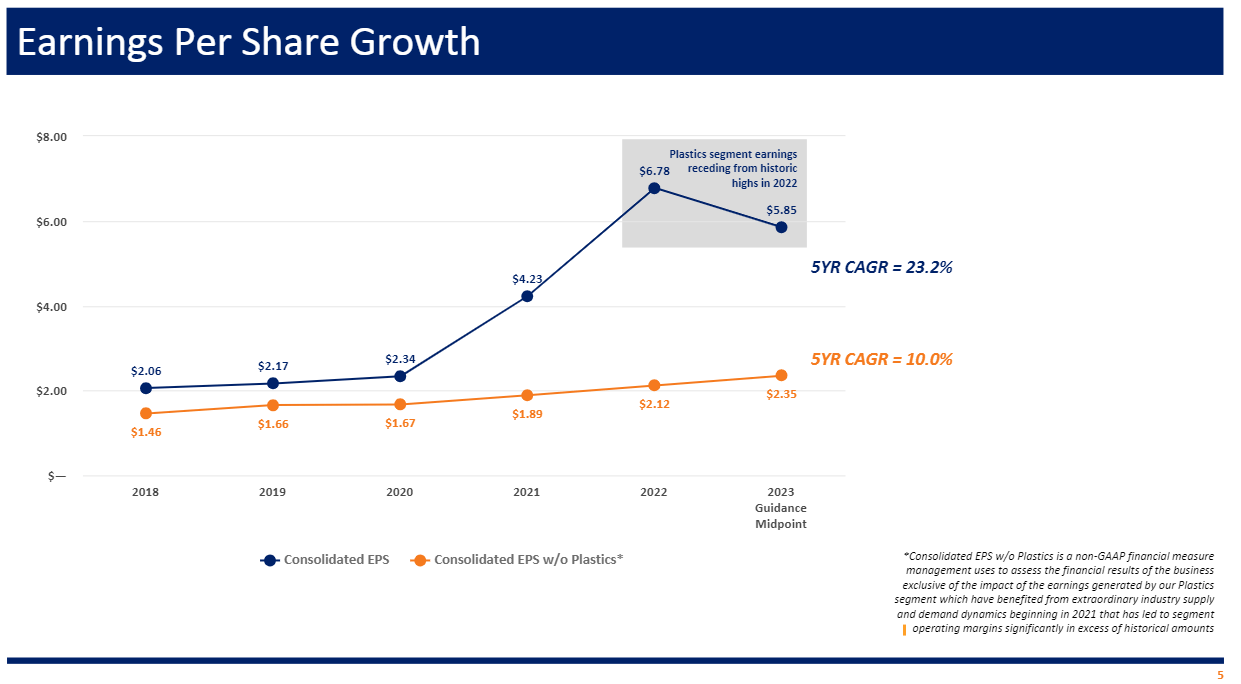

This boom flowed through to dramatically outsized earnings per share growth that the company itself is calling out as receding. While the stock has come off from its highs, in my view, I don't think it is properly discounting a true normalization of earnings.

OTTR EPS with and without Plastics (OTTR Company Presentation)

{kind=link}

As you can see above, the midpoint of guidance for earnings excluding plastics is $2.35. Plastics used to add about $.60/share to the company's earnings. Let's say a new normalized number is $.65/share for a clean $3 of eps. Even a 20x multiple, which would be extremely generous for either the utility (in this interest rate environment) or the manufacturing/plastics businesses, would only yield a $60 stock. Every turn of multiple would obviously bring down the price by $3. Since large utilities like Dominion ( D ) and Duke Energy ( DUK ) trade at 17, I think a target price closer to $50 is likely more reasonable.

Risk:

The main risk to the short is PVC prices staying elevated or even growing. Should that happen, earnings would beat and the stock could trade higher. Similarly, a fast drop in interest rates could also goose the multiples of utilities. A major rate increase for the regulated utility could also help earnings. A reversal of the decline in PVC piping, a near-term steep drop in interest rates and/or a major rate case win would cause me to reconsider my short thesis here.

There is no large dividend (2%) one has to pay out as part of the short and only 10% of the shares are sold short, although that is over twenty days to cover. To mitigate a potential squeeze from those days to cover, short position via put options could be attractive here. The company likely won't report earnings until the middle of February. One could buy a March put spread (e.g. $70-65 probably costs around $1.00-1.25) or one could be more creative and buy February puts and the same or lower strike January puts to fund the time decay.

Conclusion:

With PVC pricing coming down, overall construction slowing, and interest rates seemingly staying higher for longer, I see fairly major earnings degradation coming for this company, more than the market is discounting in my opinion. I see the stock potentially losing at least 20% of its value perhaps more.

For further details see:

Otter Tail: The Tail Wagging The Company