GPN - Our Top Growth Idea For 2023: Global Payments

Summary

- Global Payments operates in an industry with exceptionally high margins, solid organic growth and free cash flow.

- The stock is off over 60% from its highs in late 2021, and now trades at a bargain 9x forward 2023 earnings (lowest in its history).

- As a Compounder, GPN is likely to grow EPS by 9-14% through the cycle.

- Despite EPS up 2.4x since 2017 (an impressive 16% per year), the stock is remarkably down over the past five years.

- There is cycle risk at GPN in 2023, but the long-term digital spending outlook remains intact. We peg fair value in 2-3 years as over $180.

Summary

The market has punished fintech stocks in 2022, with nowhere to hide among either legacy players like Global Payments ( GPN ), Fiserv ( FISV ) and Fidelity National ( FIS ); or among the fintech disruptors like PayPal ( PYPL ), Block ( SQ ), and Marqeta ( MQ ). The latter are down 60-80% depending on the name.

Despite the carnage in the space, Global Payments operates an incredibly high-quality business model.

GPN’s business is:

1) low capital intensity, with $600 million in expected capex this year compared to $4.1 billion in estimated EBITDA.

2) high return on equity (ROEs typically mid-teens),

3) high margin (EBIT margins of 44%, and expanding every year),

4) scalable, and one that benefits from inflation (more credit card spending against largely fixed costs).

5) moat-y as massive scale is required to operate profitably in this industry. Popular disruptor Block has been around since 2009 and yet still loses money at the EBITDA level.

6) growthy with 16% EPS CAGRs over the past five years (with revenue up 9% constant currency and EPS up 18% in Q3).

GPN was a stock market darling for years until the pandemic unleashed a flood of fintech disruptors on the space. Growth investors abandoned Global Payments in favor of the Square's and PayPal's of the world. Buy Now Pay Later also created more market share loss worries.

The narrative that Global Payments was losing credit card processing market share and hence its growth slowing has decimated the stock.

But as we’ll show, GPN has not lost one iota of market share over the past two years and has seen improving pricing for its card processing services .

We also continue to like the secular growth story in digital payments, which we view as in the middle innings. We note that 50% of the world continues to transact using cash. The migration of spending to debit/credit cards and away from cash has years to go.

At 9x forward earnings, GPN is simply too cheap. We peg 14-15x as a fair value multiple for this business, which in a couple of years works out to $180 per share give or take. There is cycle risk at GPN, and the company is levering up to purchase a European competitor (EVO Payments). But as they de-lever back to normalized levels by the end of 2023, GPN should recapture a normal earnings multiple again (typically trades at 18x dating back to its IPO).

In our recession case, with EPS dropping 25% next year (almost as severe as the Great Recession), then at 10x earnings we see EPS dropping to $7 and the stock at perhaps $70 per share.

Capitalization

Company financials / author spreadsheet

Business

Global Payments is a payments technology company that provides credit/debit card processing and software solutions to 3.5mm merchants and 1,300 financial institutions globally. They are based in Georgia and employ 24,000 people.

The company originally was spun out of National Data Corporation in 2001 at $4.50 per share (on a split-adjusted basis). GPN has earned faithful shareholders 16% annual returns, up over 2600% in 21 years. The stock has returned 14% annually since 2011.

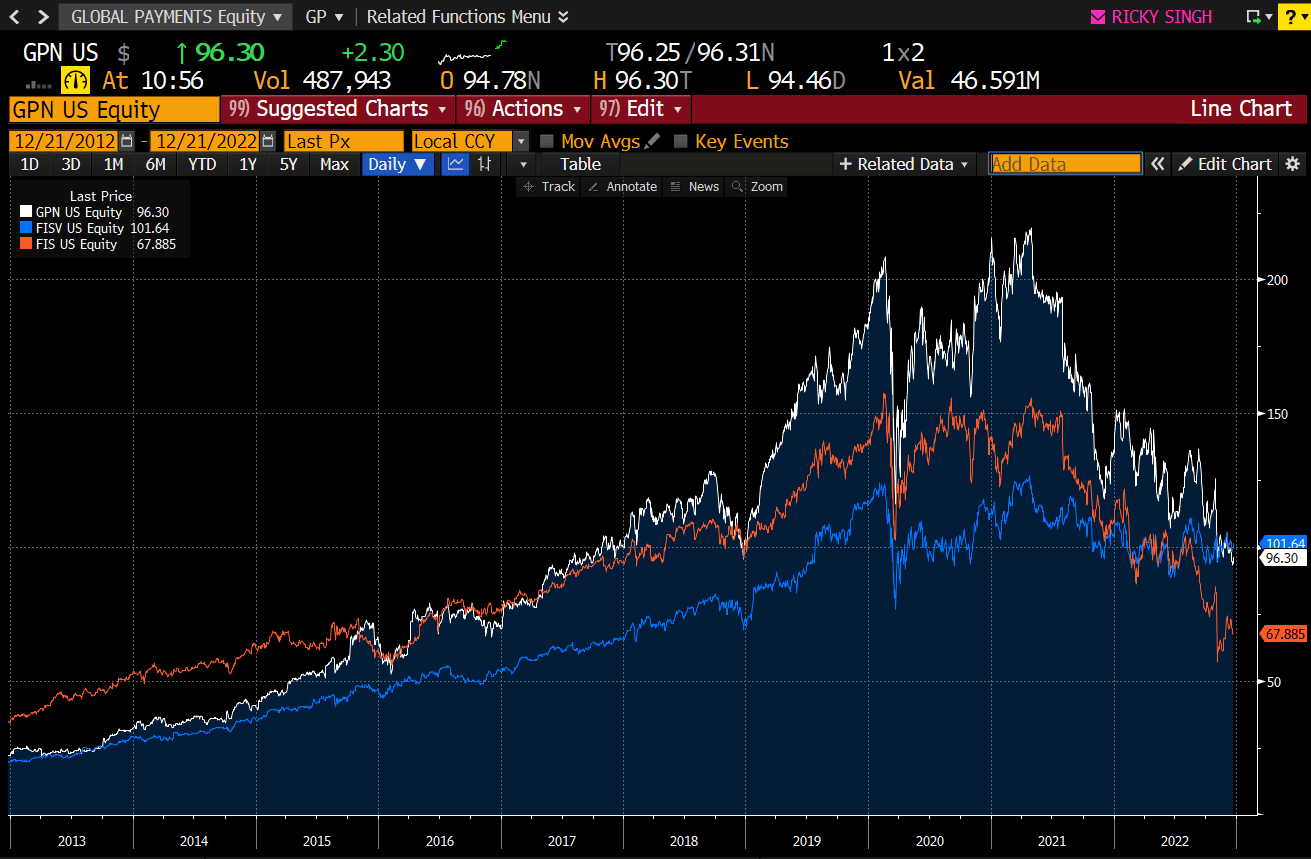

Here is a chart of GPN, FISV, and FIS below going back 10 years. FIS has been the underperformer given its weaker growth profile and market share losses. GPN has been especially hit hard of late (despite meeting or beating Street estimates every quarter dating back to 2013).

{kind=link}

Bloomberg

Global Payments Networks ( GPN ) operates in three segments: Merchant Solutions, Issuer Solutions, and Business & Consumer Solutions. GPN is selling its Consumer business for $1 billion (deal expected to close in Q1 2023) and is purchasing EVO Payments ( EVOP ) for approximately $3.2 billion.

The Consumer business is slower growth and lower margin than EVOP and the other segments at GPN, so we deem the transactions as valuation/quality accretive, if not EPS accretive.

Merchant Solutions

Merchant Solutions is GPN’s largest segment and sells systems and software in order for merchants to accept credit cards either on-site or online (usually both these days, called omni-channel). When a consumer for example submits a credit card in order to pay for a good or service, GPN’s readers verify cards, ensure amounts are within credit limits, and ultimately processes the payment (taking it from an issuing bank to the merchant).

Roughly speaking, on a $100 transaction, GPN keeps $0.50 (0.5% of the amount), and the issuing bank and the network operator split $1.50. That is, a Chase Visa card means that Chase Bank and Visa each get $0.75, and GPN collects $0.50. The merchant collects $98 on the $100 transaction.

On a debt transaction, there are caps that limit fees at $0.21 plus 5 basis points. Pricing has remained stable for the past few years despite the influx of competition.

During Covid in 2020, there were fewer credit transactions, which are more profitable, as consumers opted to use debit cards instead. Spending also dropped dramatically. In the recovery phase in 2021 and this year, credit spending has jumped with growth in the mid teens this year to date.

Big picture, over time as more and more transactions migrate to debit and credit cards from cash, GPN should continue to grow its topline.

Merchant Solutions is 75% of GPN's revenue and 83% of operating income (proforma for the Consumer sale).

Issuer Solutions

Issuer Solutions offers banks an outsourced solution to credit card management. Banks often use GPN to deal with the complexity of issuing cards to their customers, managing payments, statements and other services like fraud detection and customer correspondence.

Global Payments picked up this segment from its acquisition of Total System Services ( TSS ), a $24.5BB all-stock transaction completed in mid-September 2019. At 19x 2019 EBITDA, it wasn’t a cheap acquisition, but synergies and comps tell us that the deal was a pretty good one.

Consolidated 2019 EPS was $6.22 (with only one quarter of TSS financials). This year we are expecting about $9.33 in EPS, a 3-year stacked EPS CAGR of ~15%. 2020 was of course only a 3% EPS growth year amidst the pandemic, but EPS is expected to be up by 14% in 2022 compared to last year.

Issuer Solutions totals 25% of revenue, and 16% of EBIT. It grew 2% last quarter topline and 9% at the EBIT level. It is less cyclical than the Merchant business.

Banking and Consumer Solutions

GPN announced the sale of this slower growth business in mid-2022, with the deal expected to close in Q1 next year.

It is already marked as discontinued in the latest financials, and we excluded it below and in our consolidated projections.

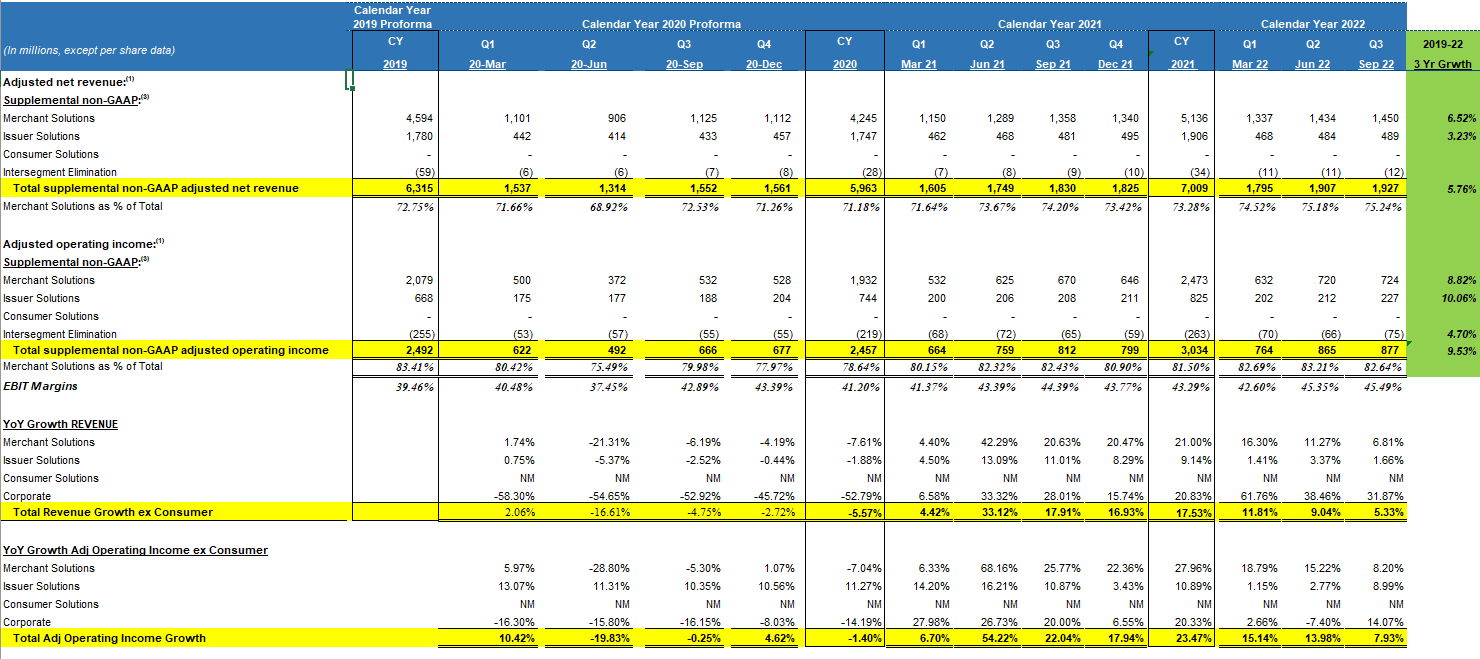

Segment Financials

{kind=link}

Company financials / author spreadsheet

Source: Company financials, author spreadsheet

In the green box above, we highlight 3-year growth figures. More recently, in Q3 2022, Merchant Solutions grew revenue 6.8% and EBIT by 8.2%. Over the nine months ending September, revenue grew 11%. Currencies have been a huge headwind to growth for GPN this year, reducing revenue by 300 basis points.

In 2009, GPN was a different business, but overall EPS fell 34%. In our bear case we assume a 25% decline in EPS to $7 per share, as we are not anticipating a recession in 2023 as devastating as the Great one.

In 2020, overall revenue (ex-Consumer) fell 5.6%, but EBIT only declined by 1.4%. EPS in fact grew 2.9% before rebounding by 27.5% in 2021.

Merger Activity

We highlighted the TSS merger from September 2019.

We thought it was worth highlighting M&A activity from prior years too, as it is an important component of their growth plan.

In 2017, GPN purchased Athlaction for $1.2BB. In September 2018, the company picked up AdvancedMD, a physician focused payments processor, for $707mm.

In October 2018, GPN scooped up SICOM Systems for $409mm. Another payment processor in the restaurant industry, it was quite complementary to their Xenial restaurant merchant processing business.

The company claims never to have acquired a company in a dilutive deal and their fundamentals support this.

Since 2017, Global Payments has spent a total of $4.3BB in capex and acquisitions (excluding TSS). EBITDA, also excluding TSS, has increased by $1.05BB. That indicates a healthy 24% ROIC, or paying just over 4x EBITDA for growth. Management gets high marks in our view here.

Most recently, GPN announced the sale of NetSpend (the Consumer segment) and the acquisition of EV Payments ( EVOP ). Overall it makes strategic sense, eliminating a small, slower growth segment and picking up a faster growth one. Our math suggests minimal accretion in 2023, with likely more in 2024 as synergies ramp up.

Digital Spending Trends and Disruption Risk

Global Payments benefits as consumers globally transact on either debit or credit cards. The narrative that PayPal and Square are disrupting these businesses seems a bit misguided. With cash usage in secular decline, credit and debit card usage will continue to grow. The only demographic that prefers cash are those over 65.

Big picture, globally, according to this , cash represented a remarkably high 50% of payments globally last year. In developed economies, the trends are clear. An IMF study focused on 11 countries concluded that cash payments fell from 49% of volumes to 29% of volumes (from 2006 to 2016). These trends were evident in all 11 countries examined, with none showing an increase in cash usage.

Last year in the US, cash spending dropped from 26% of transaction volumes to only 19% of transaction volumes. The Fed pointed out that in 2016, US consumers used credit cards for 18% of transaction volumes. That jumped to 27% in 2020.

Even more relevant to GPN, according to Business Insider, the number of Point of Sale systems in place is forecast to grow by 6.4% per year from 2018 to 2024.

Business Insider

From 2014 to 2019, debit and credit card transaction volumes grew 6.26% per year (per Statistica). In absolute dollars that is $5.16 trillion in card spending growing to $7.0 trillion in spending in 2019.

We ran the numbers on Global Payment’s market share.

Company financials / author spreadsheet

In two years, GPN has maintained steady market share at ~8.3% of industry spend (using Visa global data). The orange line above illustrates market share, and in two years it has declined by 0.1% points. That is pretty small. GPN has less travel related customers and so perhaps lost a smidgen of share in the summer as consumers fled the country.

Others argue that pricing has been under pressure given the plethora of new fintech entrants. But in fact, pricing has increased for GPN over the past two years.

Company financials / author spreadsheet

In orange above, pricing in Q4 2020 was 0.56% of processing dollars. Last quarter it was 0.60%.

On the Buy Now Pay Later (BNPL) front, the industry last year was $90 billion in total growing at a 13% CAGR. Even if it doubles in three years, that would still only represent 2% of card spending. Again, the dollars are just not that material and now dozens of credit cards now offer BNPL options.

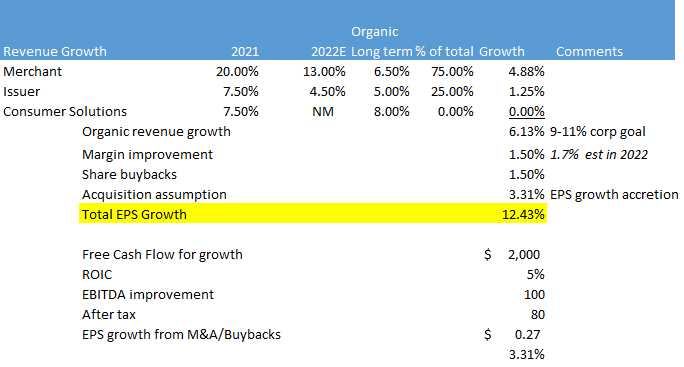

Growth Estimates

In 2022, management expects 10-11% revenue growth, proforma for currency/Russia and excluding the Consumer segment. EPS will be approximately $9.33 in 2022 compared to 2021, or up 14%. Guidance did get cut last quarter (killing the stock), but that was entirely due to currency impacts. FIS missed estimates and cut guidance in Q3. Their reduction hit GPN stock despite Global Payments having already reported.

Longer term, on a 3-year stacked basis, GPN’s Merchant business has grown revenue by 6.5%, with total company revenue up 5.8% per year.

The Issuer segment is expected to grow low to mid single digits topline in 2022 (and 5% long term).

Adding that up and we get the following (~12% long term EPS growth potential with some value added M&A/buybacks):

{kind=link}

Growth rate estimate (GPN financials / author spreadsheet)

Given that the 3-year annualized EPS growth has been 15% (2022E compared to 2019), we think these numbers are conservative. Our margin assumptions are probably too low, as EBITDA margins have expanded from 21% in 2014 to 45% last year.

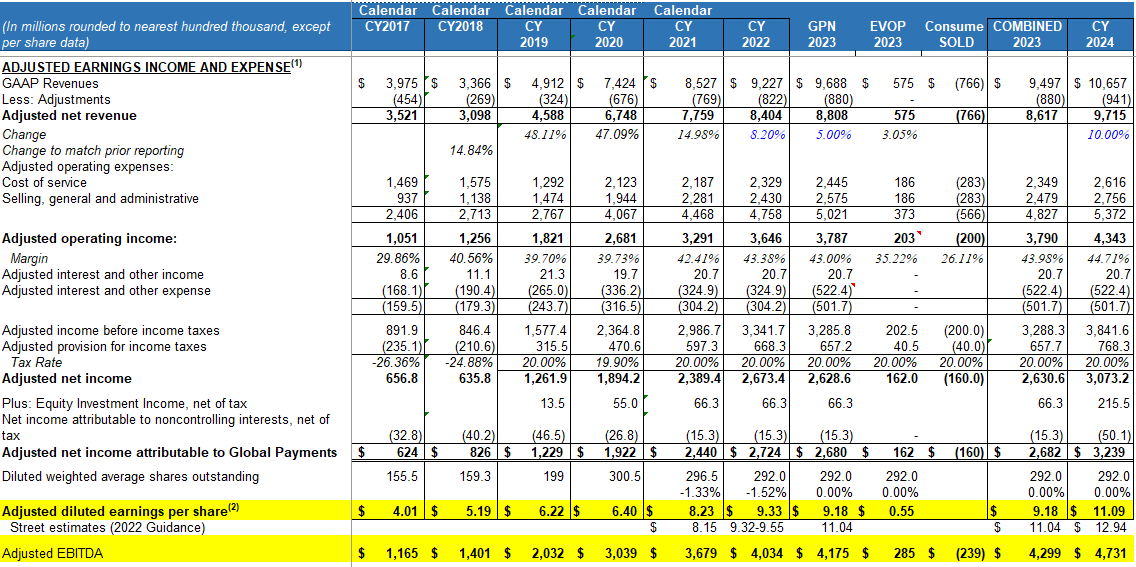

Updated Model and Projections

With the odds of a recession increasing, we took a conservative view on 2023 estimates. Street figures are $10.35 in EPS next year, but we assume roughly flat earnings (at $9.18) with a bounce in 2024 to $11 in EPS give or take.

{kind=link}

Projections (GPN Financials and author spreadsheet)

With leverage higher and weakness likely in 2023, GPN could be dead money for a few months (along with the entire stock market). But, impressively the company has experienced only one year of negative earnings growth dating back to its 2001 IPO.

That was in 2009, when EPS fell 34% (fiscal year ending May 2010).

As mentioned, even in 2020, EPS grew 3%.

Valuation

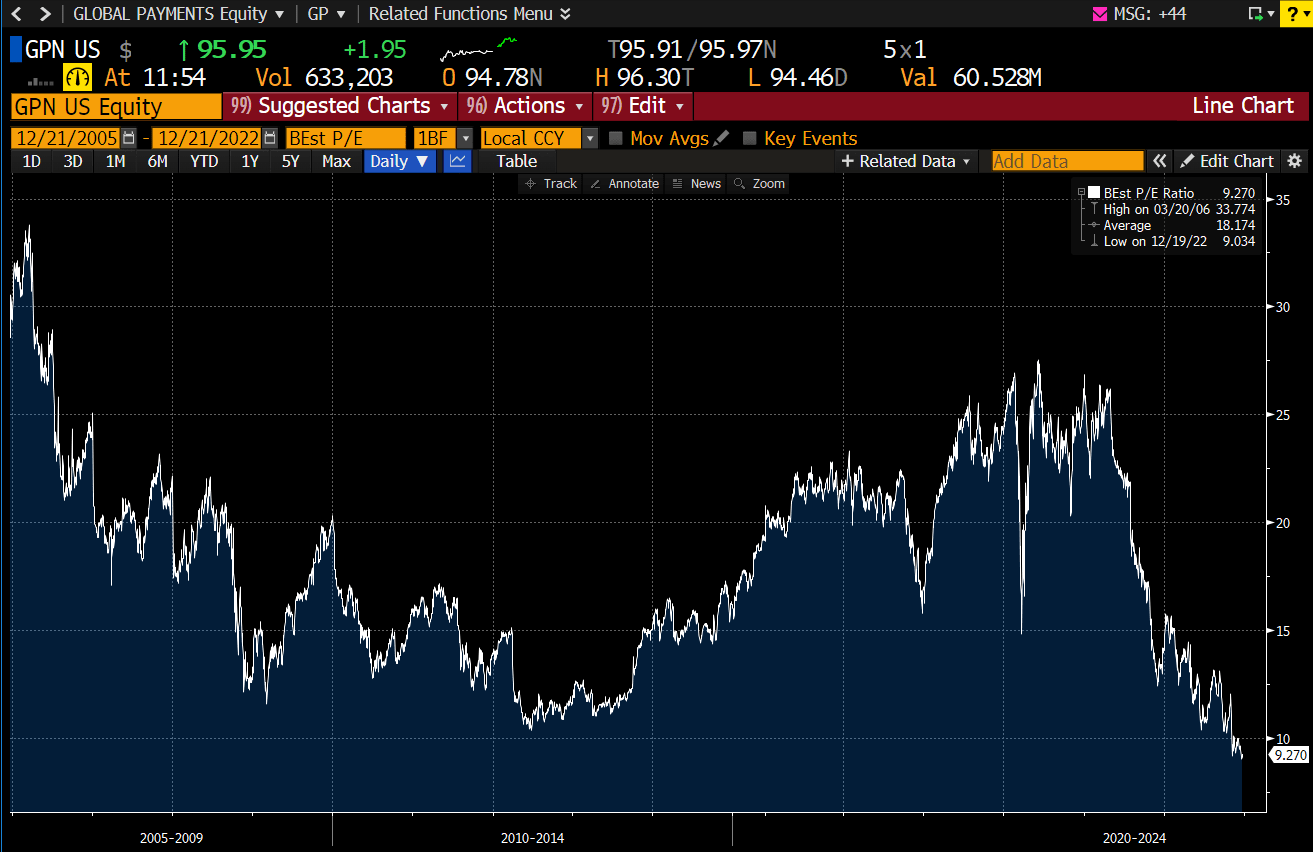

Below is a chart of Global Payment’s P/E ratio on a long term basis. These are based on forward 12-month estimates, and long term GPN has traded at a multiple of 18.2x earnings.

{kind=link}

Bloomberg

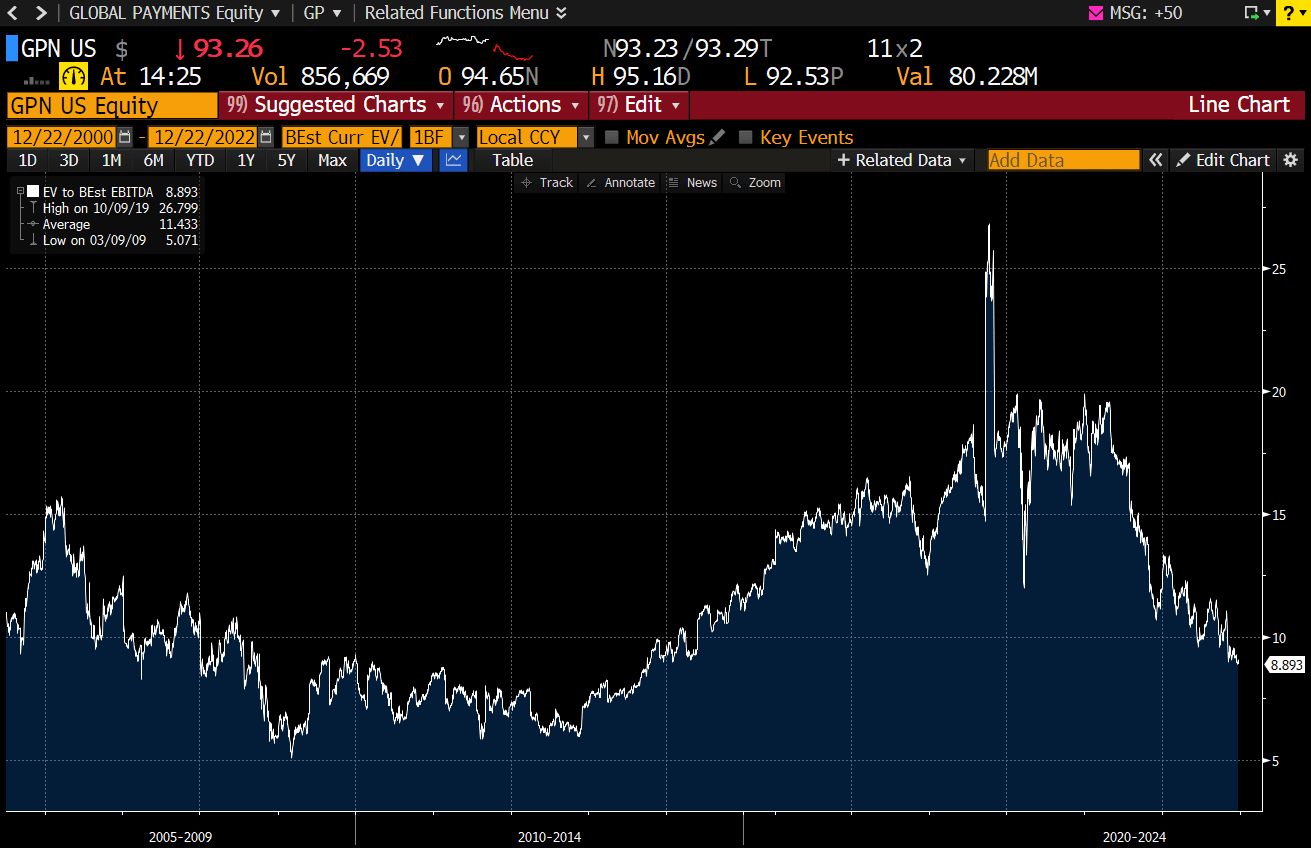

Below is GPN on a blended forward EV/EBITDA basis.

{kind=link}

Bloomberg

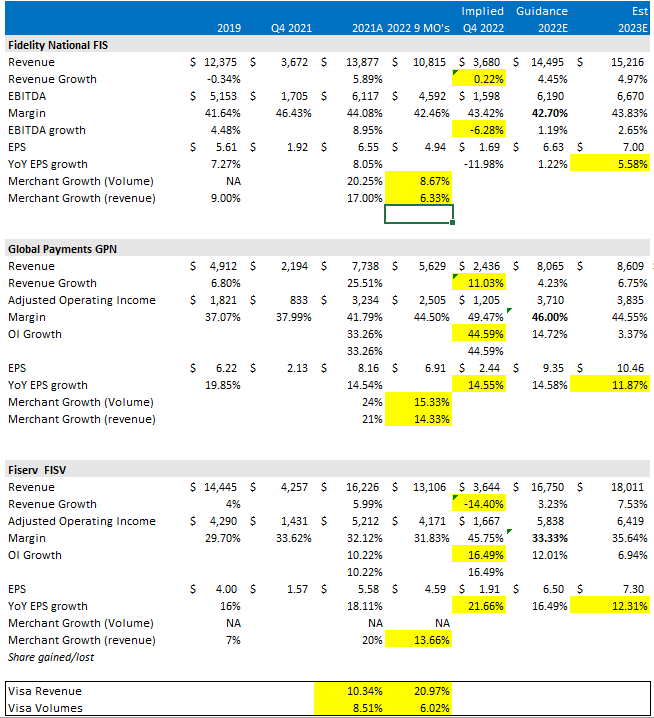

We think the best comp is Fiserv ( FISV ), who has similar market share figures and similar EPS growth.

FISV trades today at 10.8x EBITDA and 13.5x earnings.

For those who like to dive deep into the numbers, here is market share data for the big three legacy players.

{kind=link}

Company financials / author spreadsheet

Overall, FIS is struggling share wise, with 9-month growth in merchant revenues of 6.3%. FISV has grown merchant revenue by 13.7% and GPN at 14.3%.

We know the Clover branded point of sale system at FISV is growing quite rapidly (and is notably popular among investors in the space who think it can be hived off for a big multiple). But that would just expose the weakness in Fiserv’s other merchant operations, probably leading to a collapse in the remaining business.

In short, we see zero reason for any discount in GPN shares to FISV.

Here are our valuation scenarios.

EV/EBITDA Valuation (Author spreadsheet and estimates)

Conclusion

It could be a rough few months in 2023 should a recession begin to impact earnings. That said, in our down 25% scenario, EPS could drop to $7 and implies a stock trading at 13.3x today. That is still a discount to FISV and well below its long term average 18x multiple. But leverage is higher today (3.9x proforma for the EVOP deal) and investors have been shooting this stock first and then asking questions.

We view Global Payments as a far higher than average quality company. It has a broken stock but not a broken business model. Risks related to fintech competition also seem misplaced. As Bank of America pointed out recently, fintech private capital investing is down 68% so far in 2022. Higher rates and a business that requires massive scale in order to generate profits means that it will be tough if not impossible for new entrants.

Even well established disruptors like Block generated negative $50 million EBITDA on a trailing twelve month basis (including stock based comp). It has been around since 2009, so we wonder, when will they actually begin to make money?

Looking past a recession and a normal/conservative 13-15x multiple on 2025 figures suggests 70% to possibly 100% upside. The event path looks tough, but we view this quality name as having a big margin of safety at current levels, and our top growth pick for 2023.

Editor's Note: This article was submitted as part of Seeking Alpha’s Top 2023 Pick competition, which runs through December 25. This competition is open to all users and contributors; click here to find out more and submit your article today!

For further details see:

Our Top Growth Idea For 2023: Global Payments