OB - Outbrain: Capital-Intensive Ad Business That's Faltering

Summary

- Outbrain posted a significant decrease in its revenues last quarter, albeit still outperforming analyst consensus.

- The company has a capital-intensive business as it has to bid on-screen space for advertisements. This, along with its operating costs, make it frequently swing into a loss.

- To deal with the volatility inherent in its business, Outbrain has taken on debt that it doesn't appear to be paying off.

- Finally, global growth in digital ad spend hasn't translated into the top line for Outbrain.

- As such, I think investors should look elsewhere for exposure to digital/programmatic advertising.

Overview

Outbrain ( OB ) is a programmatic advertising company. The company's core technology is an advertising platform that integrates across publishers (media companies) and advertisers in order to deliver targeted advertisements across both desktop and mobile. As always in programmatic advertising, the firm bids on media 'real estate' and then places advertisements there if it is able to 'win the auction'.

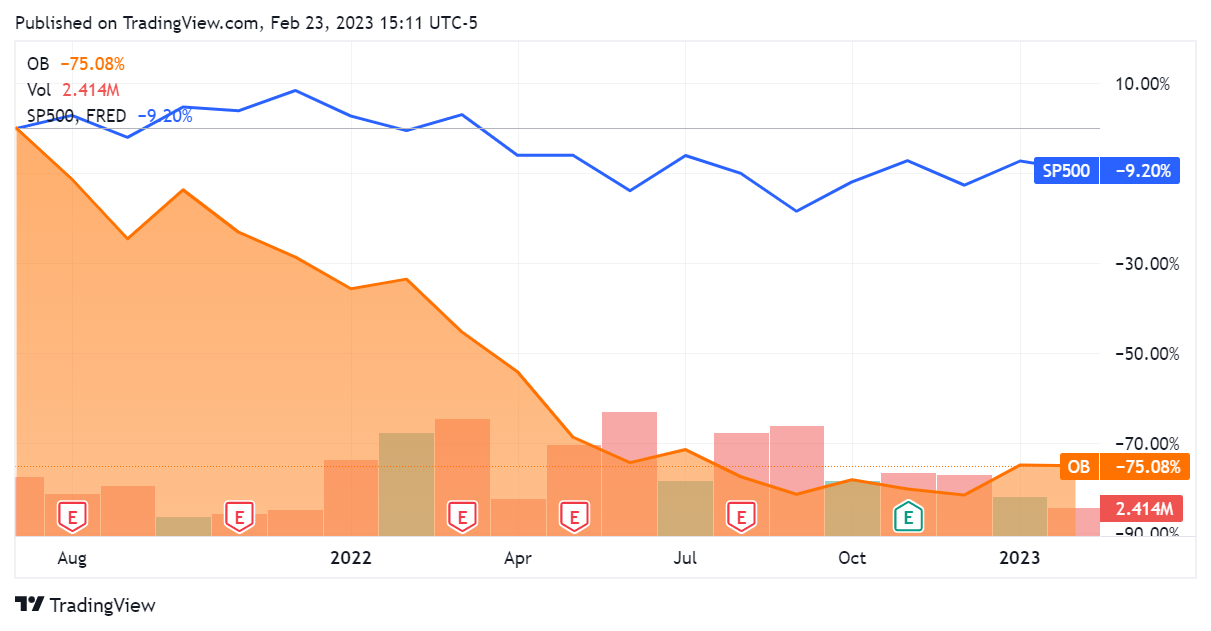

The company was founded in 2006 and entered the public markets via initial public offering in Q2 2021, at $20 per share. Since then, the stock has depreciated significantly while to its current price of under $5 per share, all the while materially underperforming the S&P500 index.

{kind=link}

While the increasing difficulties of the digital advertising landscape are well-known, Outbrain is certainly a known entity and scale player in the space. As such, it's worth evaluating its stock to see if it may have become cheap relative to its fundamentals.

Financials

Outbrain has generally been a growing firm over the last 10 quarters, although the most recent quarter saw its top line degrade for the first time in recent memory. Worth noting is that analysts had actually expected a decrease in revenues, and that this performance constituted a beat against consensus by $19.5M.

SeekingAlpha.com OB 2.23.23 SeekingAlpha.com OB 2.23.23

{kind=link}

{kind=link}

Management made clear on the earnings call for that period that this decrease was due to lower yields (cost per mile, cost per click) on digital advertisements. Currency movements, namely the strength of the US Dollar, also appeared to shave off 6% from the top line.

SeekingAlpha.com OB Q3 2022 Earnings Transcript 2.23.23

{kind=link}

The rising US dollar throughout this period ended up being a material factor due to Outbrain's business being primarily (60%) outside of the US.

SeekingAlpha.com OB Q3 2022 Earnings Transcript 2.23.23

{kind=link}

This factor is less numerically significant now, as the US Dollar Index ( DXY ) has seen a 9.5% decrease since Q3 2022; upcoming earnings for Q4 2022 could be marginally less impacted by this.

{kind=link}

Nonetheless, a revenue decline isn't something that any investor likes to see. The company expects this trend to reverse as the macroeconomic situation improves and ad-buying recovers. This could take a year or longer, however, in my view, as we don't appear to be out of the woods yet on inflation or a return to baseline GDP growth as of yet.

SeekingAlpha.com OB Q3 2022 Earnings Transcript 2.23.23

{kind=link}

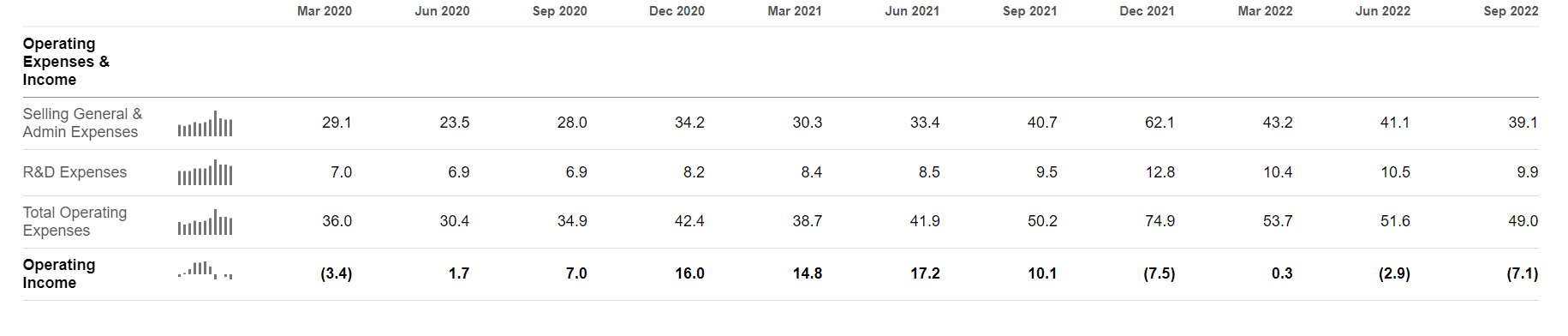

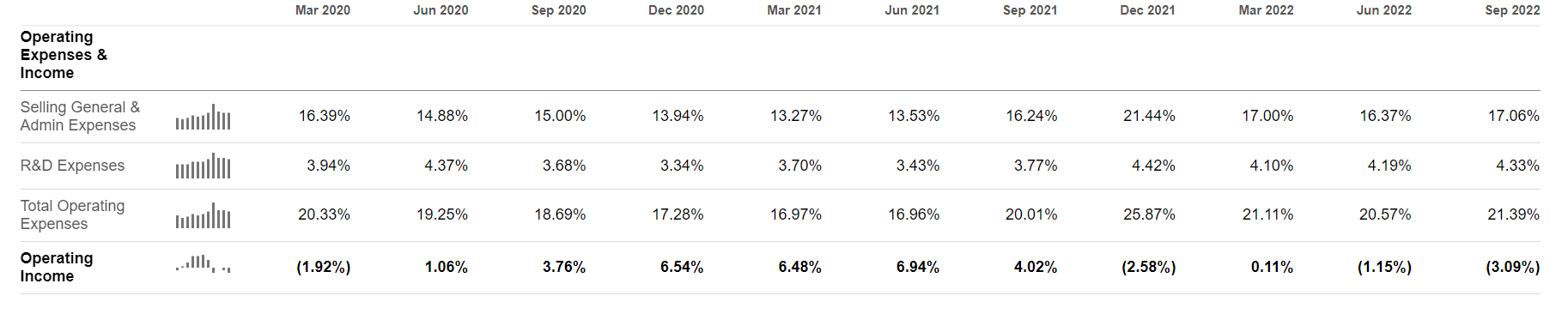

Looking towards profitability, we see that Outbrain presents a relatively volatile picture on earnings. While it has been able to post a profit during some quarters, it just as often posts a loss; Q3 2021 was particularly negative in this regard. Additionally, the company has not been profitable for 3 quarters running.

{kind=link}

The company also appears to have an operating cycle that can readily swing into a loss; this has happened the last 3 quarters out of 5. Since its operating expenses as a percentage of revenue are relatively low, hovering around 20%, this means that it is being forced to expend significant amounts of capital to generate its revenues.

SeekingAlpha.com OB 2.23.23 SeekingAlpha.com OB 2.23.23

{kind=link}

{kind=link}

The firm's management states that this is due to investments in technology, namely 'serving capacity' and algorithmic optimization.

SeekingAlpha.com OB Q3 2022 Earnings Transcript 2.23.23

{kind=link}

Yet, we can see that Outbrain generally has quite high costs of revenue - particularly for a technology entity. This can be partly due to their accounting philosophy, wherein they bill technology expenditures as a cost of revenue. The main reason that this is the case, however, is because Outbrain's business in digital advertisements includes 'bidding' for screen space. The way that an algorithmic digital advertising company such as this one works is in some respects similar to a liquidity seeking algorithm. The firm must bid on digital 'real estate' in order to place ads there, through an auction. This occurs through ad networks such as Google's DoubleClick. Clearly, Outbrain has to spend roughly 80 cents for every dollar of revenue that it ends up generating; this is the norm. With another 20 or so percent of revenues for operating expenses, the different between profit and loss ends up being quite thin - and volatile. I wouldn't have too much confidence in any projected growth rate for this company as a result of the variance within these figures.

{kind=link}

Owing to the variable nature of its business and operating cycle, Outbrain is thus forced to leverage debt for its operations. This has become particularly prominent as the digital advertising landscape has encountered weakness. Starting in Q3 2021, the firm took on $236M of long-term debt - and hasn't yet paid back any of it.

{kind=link}

Debt, of course, comes with interest. The company is now servicing this debt without actually cutting into the principal. This debt appears to be structured such that payments are made every half-year. While the interest itself doesn't appear to be overly significant - 1.6% of revenues last quarter - I am concerned that they haven't paid back any of the principal. The number is much more significant when we calculate that the debt service of $3.6M was a significant 78.3% of its net loss for the last quarter. An ongoing situation like this, along with the thin margins and volatility inherent in the digital media business, will make it difficult for the company to generate a profit unless conditions noticeably improve.

{kind=link}

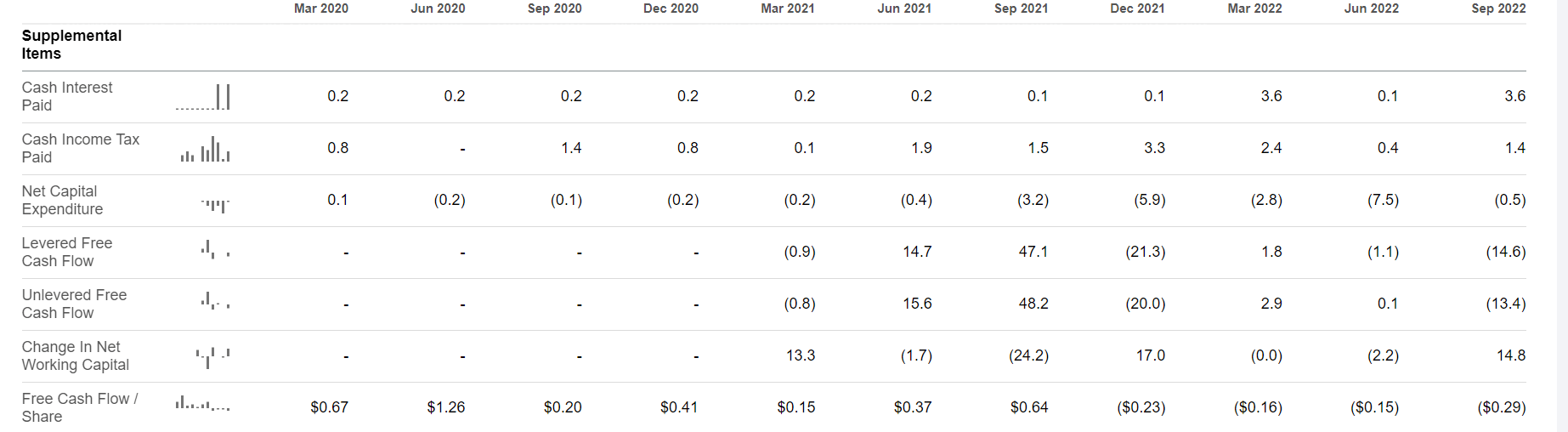

Expanding our lens to cash flow, it shouldn't be too surprising to see that the firm posted negative FCF for the last quarter. The picture here again reflects the variance that they encounter in their business. I wouldn't have comfort that this company can generate consistent cash flows for its shareholders. Its free cash flow loss last quarter came in at a relatively significant 5.99% of its share price.

{kind=link}

Valuation

On the valuation side, Outbrain presents a much better picture. This indicates that the market is pricing the firm such that it will continue to underperform in the manner that it has been. This presents a potential opportunity for alpha generation in case we can get in at the right time - although that time does not appear to be now.

Notably, the company only reports GAAP earnings - something quite unique indeed for software companies. Here, we see that it is trading at a 7.9% discount to the Communication Services GICS sector.

{kind=link}

On a sales basis, things look even better. The firm is quite cheap relative to its peers, with a 79% discount at its current price.

{kind=link}

Of course, the company has been losing cash so we can't really look into that valuation.

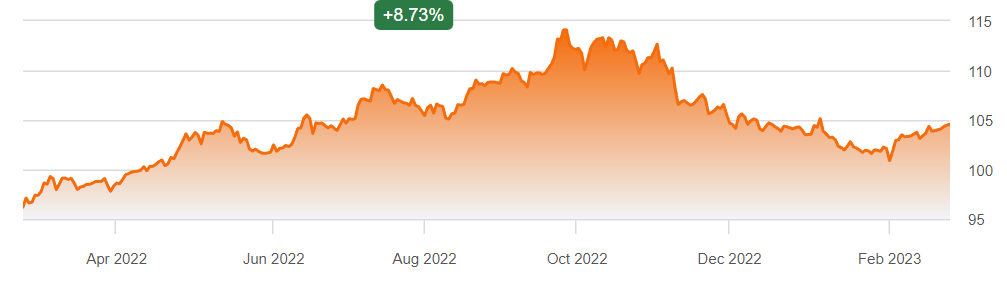

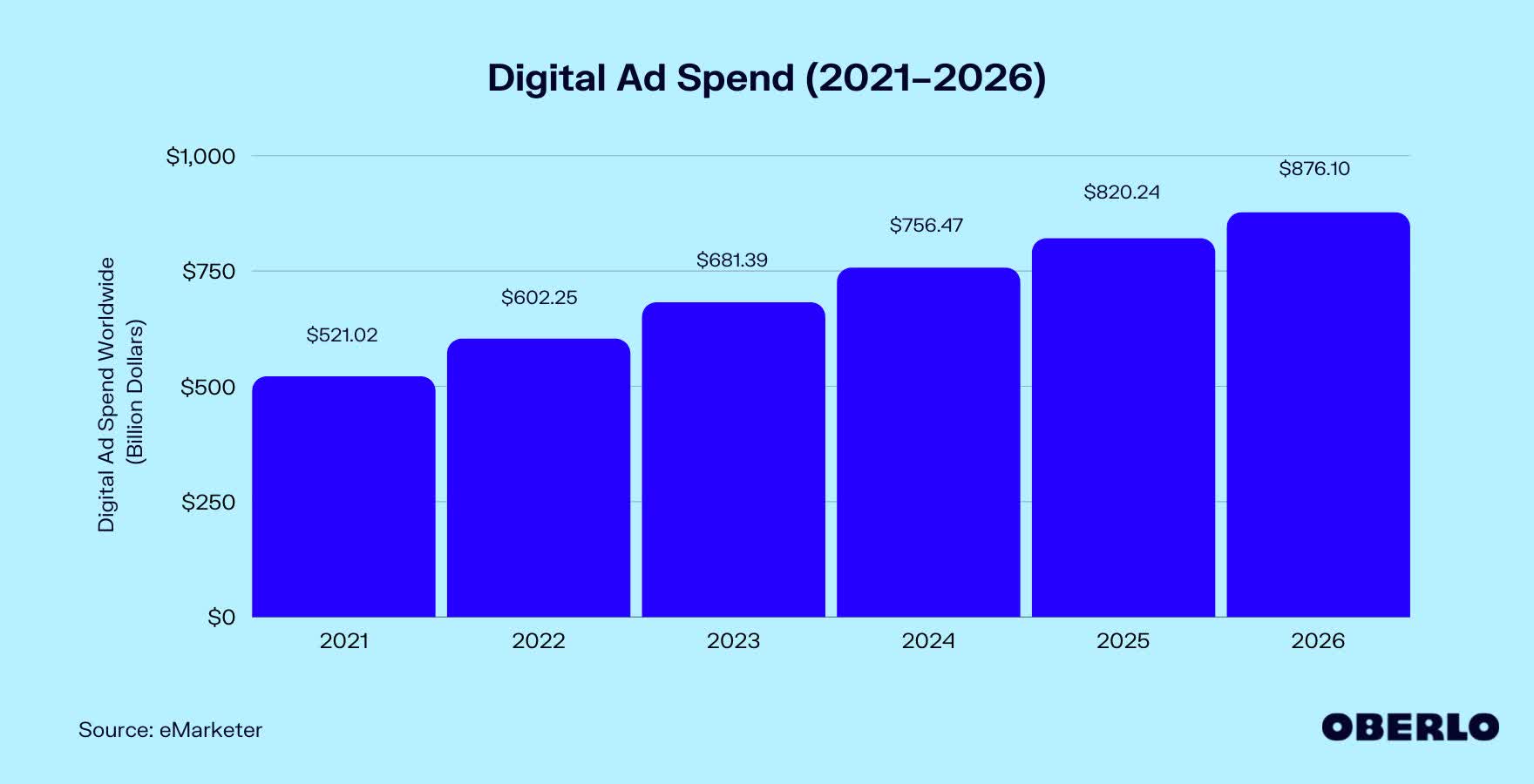

The coda to all this is digital advertising growth globally has actually been rising. The chart below shows results for 2021 and 2022, with projections thereafter. Outbrain has seen a decline in its business performance even as its been part of a 'rising tide'. This makes me skeptical that it can regain its footing even as macroeconomic conditions improve. Ultimately, there are heavy hitters in the digital advertising space that it has to go up against.

eMarketer via Oberlo.com 2.23.23

{kind=link}

Conclusion

There are better stocks for an investor that wants exposure to the digital advertising space. Even though US spend on digital ads has faltered over the last several years, this hasn't been the case internationally. Nonetheless, Outbrain failed to capture this growth in 2022. It appears that the business has difficulties beyond its target market - I would certainly chalk up competition and a capital-intensive business as significant factors.

This is a company that has to spend very significant amounts of capital (80 cents per dollar) to generate revenues. The debt it has taken on, and the overall negative cash flow picture, make me all the more pessimistic. If this stock wasn't already discounted by the market, then I would call it a sell. The market seems to have priced all of this already, however, so I will call it a hold. Current owners should think carefully as to whether they want to hold on, and individuals considering a purchase should look elsewhere for this kind of exposure.

For further details see:

Outbrain: Capital-Intensive Ad Business That's Faltering