OB - Outbrain Faces Softening Advertising Market

2023-05-15 13:45:54 ET

Summary

- Outbrain published its Q1 2023 financial results on May 9, 2023.

- The company provides online advertising recommendation services to companies worldwide.

- OB has produced declining revenue and increasing operating losses amid an advertising demand drop.

- My outlook for OB is Bearish [Sell] in the near term.

A Quick Take On Outbrain

Outbrain ( OB ) reported its Q1 2023 financial results on May 9, 2023, beating revenue and earnings per share consensus estimates.

The firm operates a recommendation platform for websites on the open Internet.

OB is producing lower revenue, increasing operating losses and negative earnings.

I’m Bearish [Sell] on OB for the near term.

Outbrain Overview

New York, NY-based Outbrain was founded to develop a system to provide recommendations of stories, products and videos that are relevant to the content it is displayed next to and relevant to readers' potential interests.

Management is headed by co-founder, Chairman and CEO Yaron Galai, who was previously the co-founder of Quigo Technologies, a provider of performance-based marketing solutions for advertisers and publishers.

The company’s primary offerings include:

-

Engage

-

Smartfeed

-

Native Ads

The firm seeks relationships with media agencies and brand advertisers.

Outbrain’s Market & Competition

According to a 2020 market research report by Transparency Market Research, the market for digital ad spending is estimated to reach $1.4 trillion in 2031.

If achieved, this would represent a CAGR (Compound Annual Growth Rate) of approximately 14% from 2021 to 2031.

The main drivers for this expected growth are a shifting consumer preference toward social media and digital video are increasing the demand for display advertising.

Additionally, after the pandemic, travel, hospitality and automotive industries are likely to represent significant demand growth opportunities.

Major competitive or other industry participants include:

-

Facebook (META)

-

Google (GOOG)

-

LinkedIn

-

Twitter

-

Amazon (AMZN)

-

Criteo (CRTO)

-

Magnite (MGNI)

-

PubMatic (PUBM)

-

Taboola (TBLA)

-

The Trade Desk (TTD)

-

Viant (DSP)

-

Xandr

Outbrain’s Recent Financial Trends

-

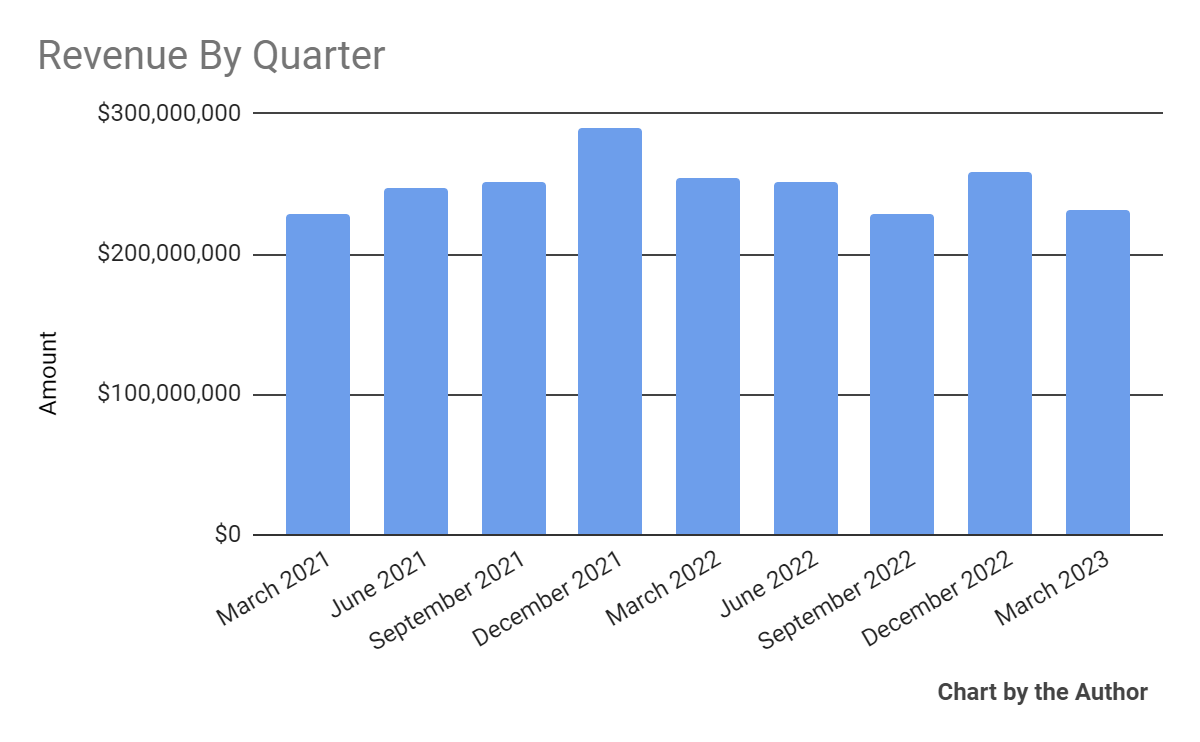

Total revenue by quarter has trended lower in recent quarters:

{kind=link}

-

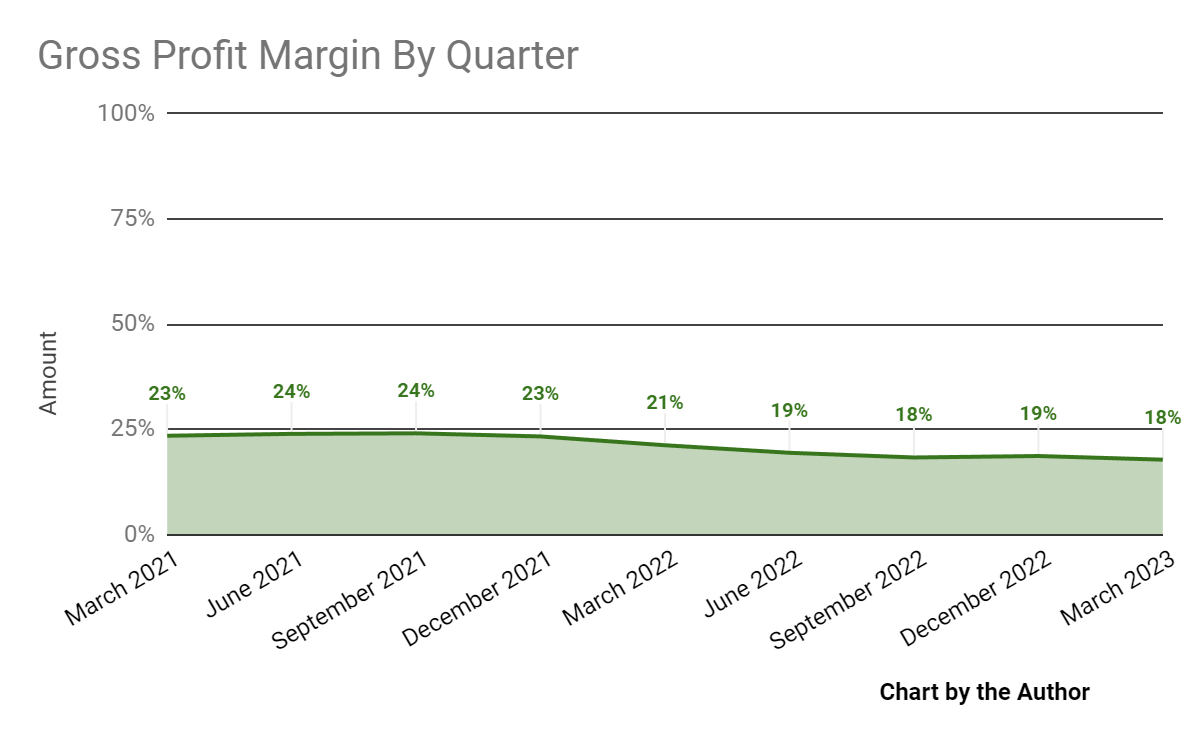

Gross profit margin by quarter has also trended lower more recently:

{kind=link}

-

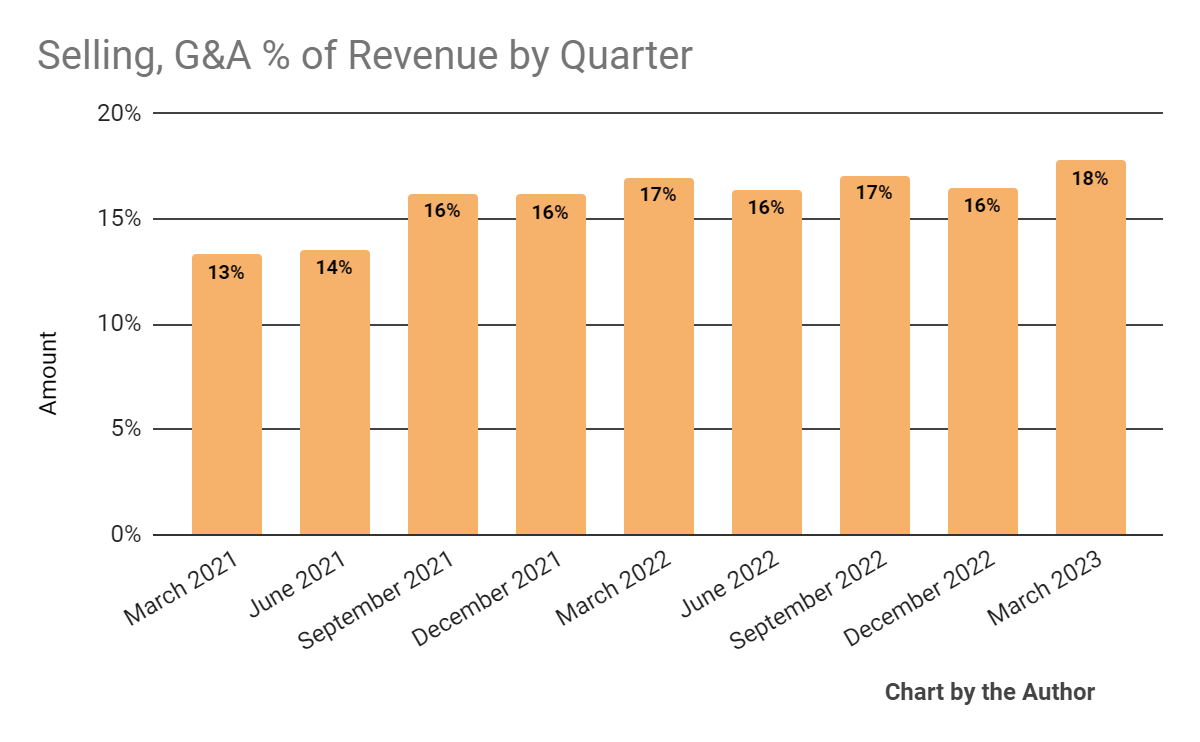

Selling, G&A expenses as a percentage of total revenue by quarter have grown in recent quarters:

{kind=link}

-

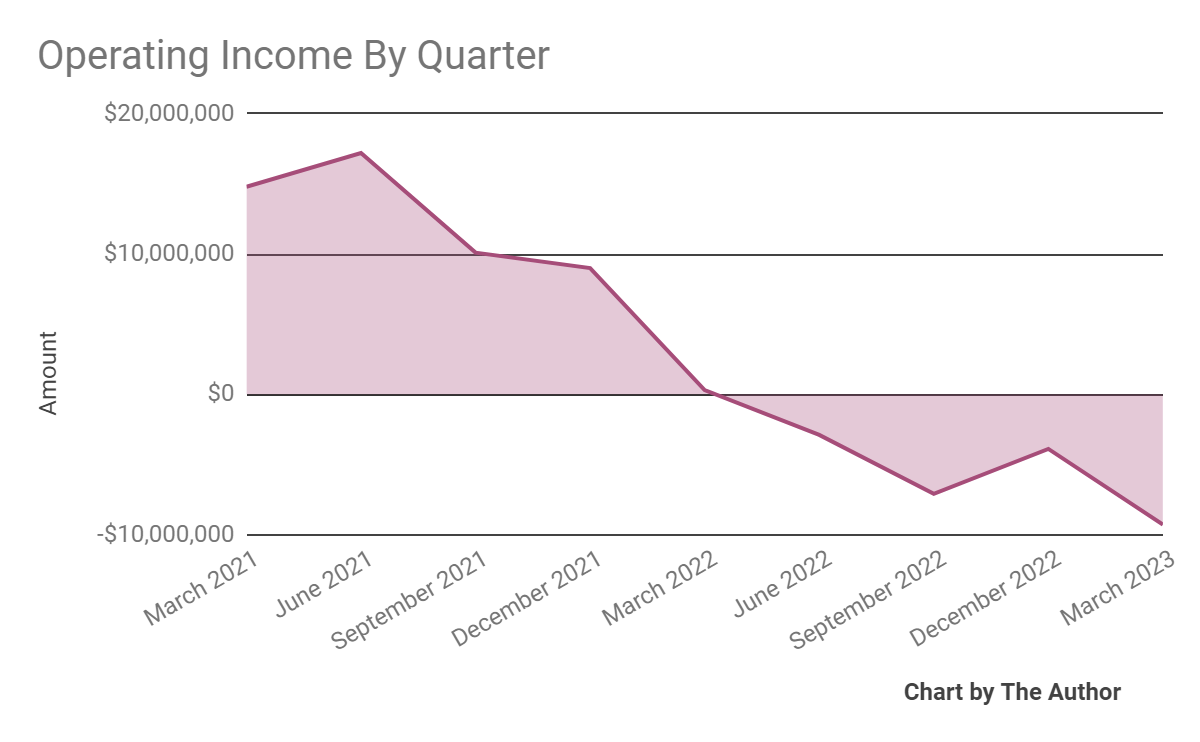

Operating income by quarter has worsened further into negative territory:

{kind=link}

-

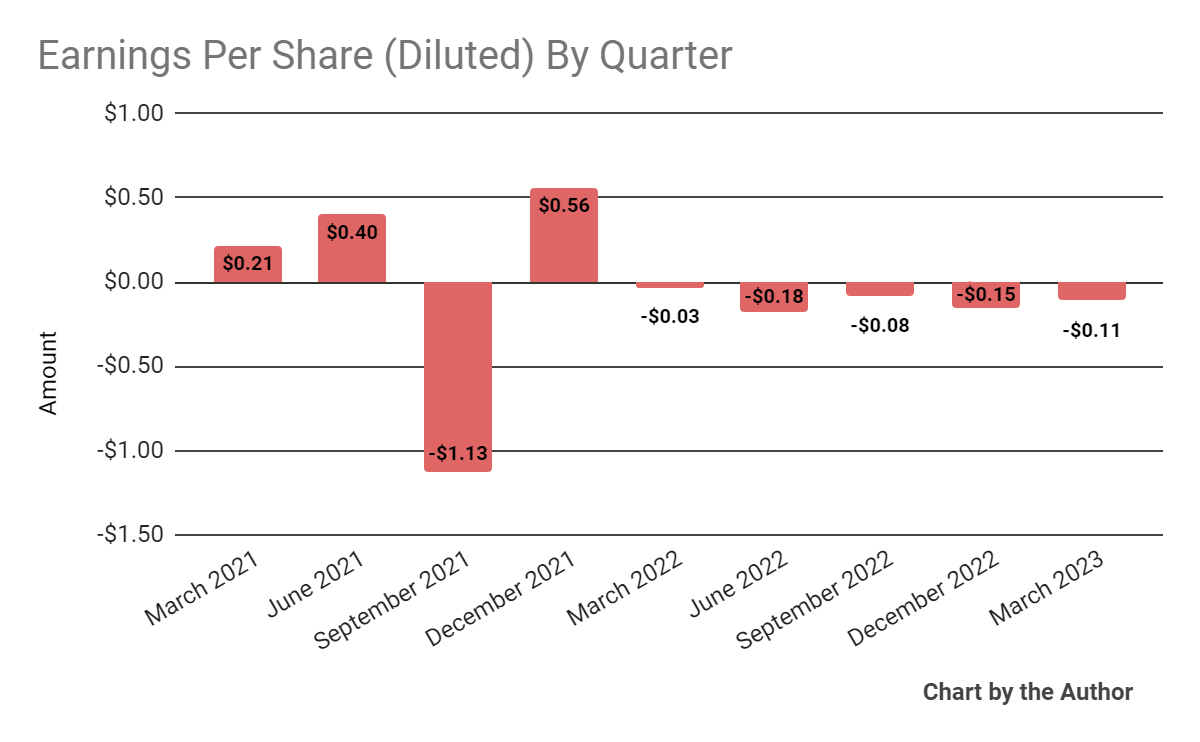

Earnings per share (Diluted) have remained negative in each of the past five quarters:

{kind=link}

(All data in the above charts is GAAP)

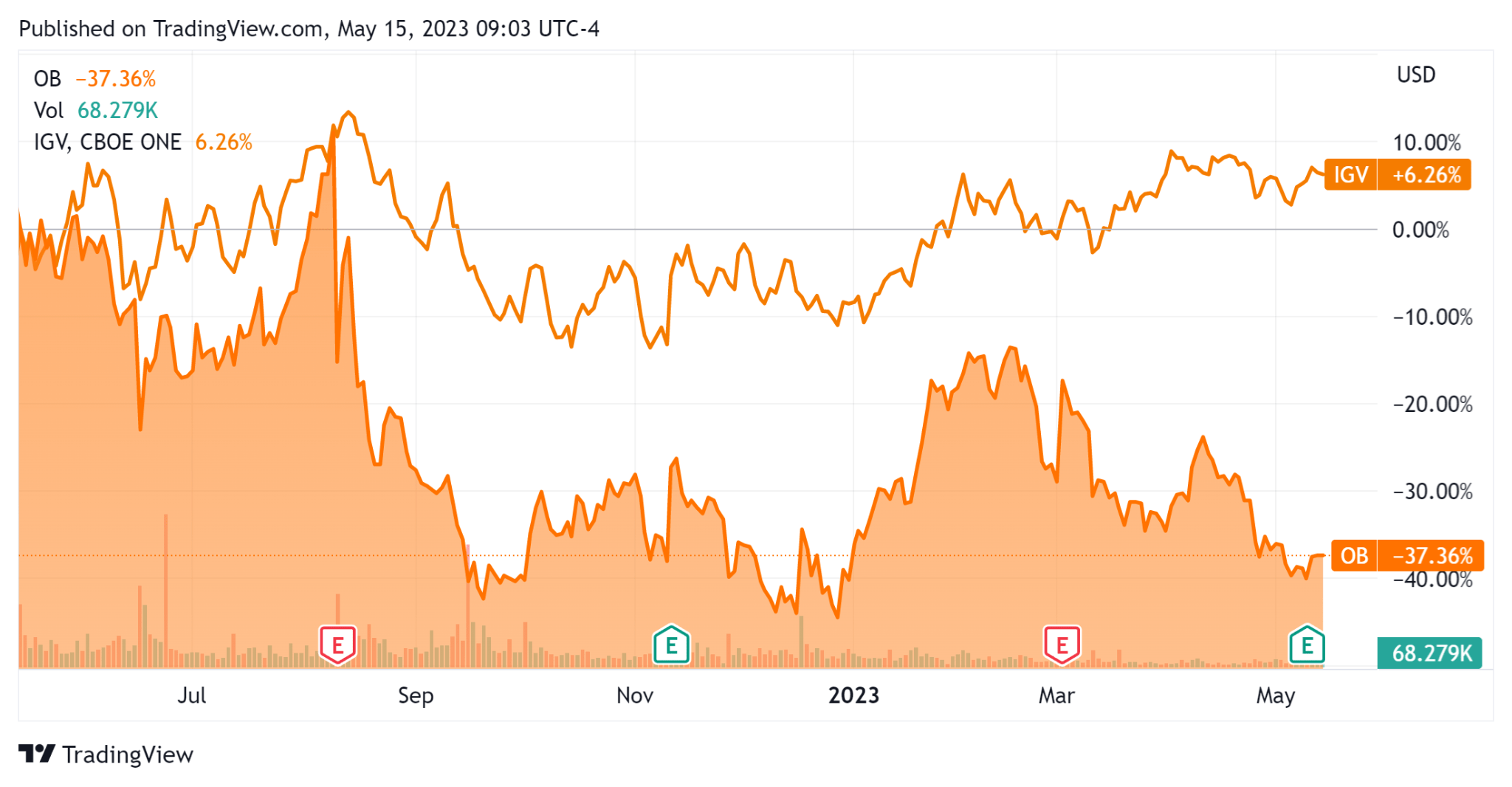

In the past 12 months, Outbrain’s stock price has fallen 37.36% vs. that of the iShares Expanded Tech-Software Sector ETF’s ( IGV ) rise of 6.26%, as the chart indicates below:

{kind=link}

For the balance sheet, the firm ended the quarter with $251.7 million in cash, equivalents and short-term investments and $236.0 million in total debt, none of which was categorized as the current portion due within 12 months.

Over the trailing twelve months, free cash used was $28.3 million, of which capital expenditures accounted for $14.3 million. The company paid $11.5 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Outbrain

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 0.1 |

| Enterprise Value / EBITDA |

| NM |

| Price / Sales |

| 0.2 |

| Revenue Growth Rate |

| -6.9% |

| Net Income Margin |

| -2.9% |

| EBITDA % |

| -0.6% |

| Market Capitalization |

| $193,830,000 |

| Enterprise Value |

| $121,020,000 |

| Operating Cash Flow |

| -$14,020,000 |

| Earnings Per Share (Fully Diluted) |

| -$0.52 |

(Source - Seeking Alpha)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

OB’s most recent Rule of 40 calculation was negative (7.5%) as of Q1 2023’s results, so the firm has performed poorly in this regard, per the table below:

| Rule of 40 Performance |

| Calculation |

| Recent Rev. Growth % |

| -6.9% |

| EBITDA % |

| -0.6% |

| Total |

| -7.5% |

(Source - Seeking Alpha)

Commentary On Outbrain

In its last earnings call (Source - Seeking Alpha), covering Q1 2023’s results, management highlighted the uncertain macro environment where customer budgets are under negative pressure, especially in the United States.

The European region has been somewhat more favorable to the firm’s offerings.

Management is seeking to increase its focus on further integrating AI machine learning technologies into its recommendation engine.

The company’s publisher net revenue retention rate was 80%, indicating sales & marketing efficiency in need of significant improvement.

Total revenue for Q1 2023 fell 8.8% year-over-year and gross profit margin also fell, by 3.4 percentage points.

SG&A as a percentage of revenue rose 0.8 percentage points, while operating income continued its clearly negative trend, with the firm generating an operating loss of $9.3 million.

Looking ahead, management reiterated its previous full-year 2023 guidance.

The company's financial position is reasonably strong, with ample liquidity and relatively minor free cash use in the last twelve-month period.

Regarding valuation, the market is valuing OB at an EV/Revenue multiple of only 0.1x, an extremely low multiple.

The primary risk to the company’s outlook is continued softness in advertising spend as macroeconomic conditions appear to be slowing down.

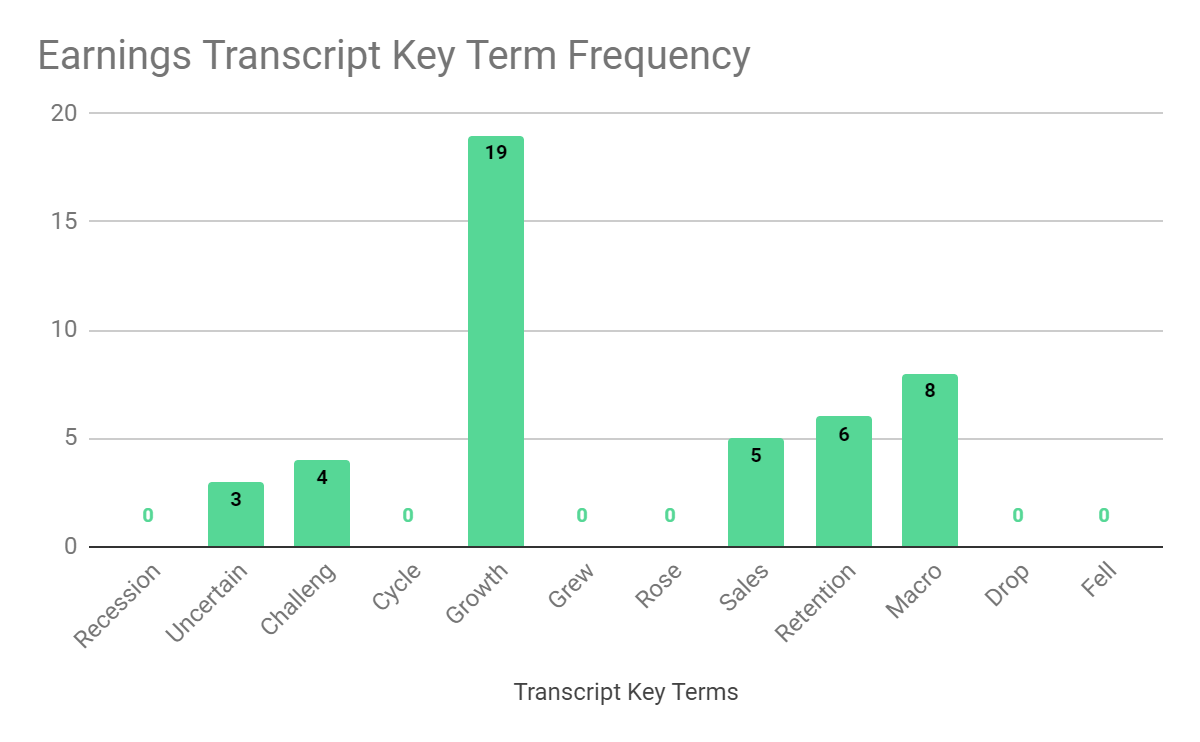

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I’m most interested in the frequency of potentially negative terms, so management cited ‘Uncertain’ three times, ‘Challeng[es][ing]’ four times, and ‘Macro’ eight times in various contexts.

The negative terms refer to the difficulties the company is facing with a dropping customer spending dynamic.

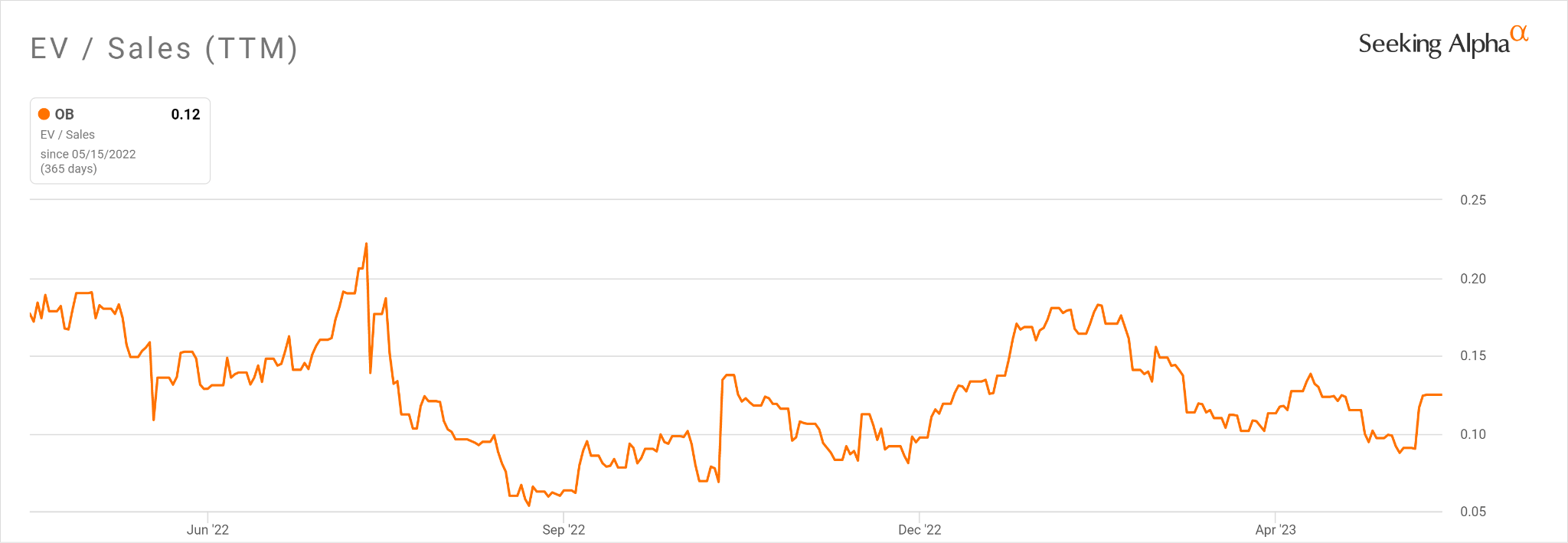

In the past twelve months, the firm's EV/Sales valuation multiple has dropped by 33%, as the chart from Seeking Alpha shows below:

{kind=link}

A potential upside catalyst to the stock could include an improvement in advertising spending in the U.S., although I don’t expect that to occur.

Outbrain is simply producing lower revenue, greater operating losses and negative earnings.

Until management can turn those three metrics around, I’m Bearish [Sell] on OB.

For further details see:

Outbrain Faces Softening Advertising Market