OUT - Outfront: Elevated Debt Leaves Shares Unattractive

2024-01-02 14:18:02 ET

Summary

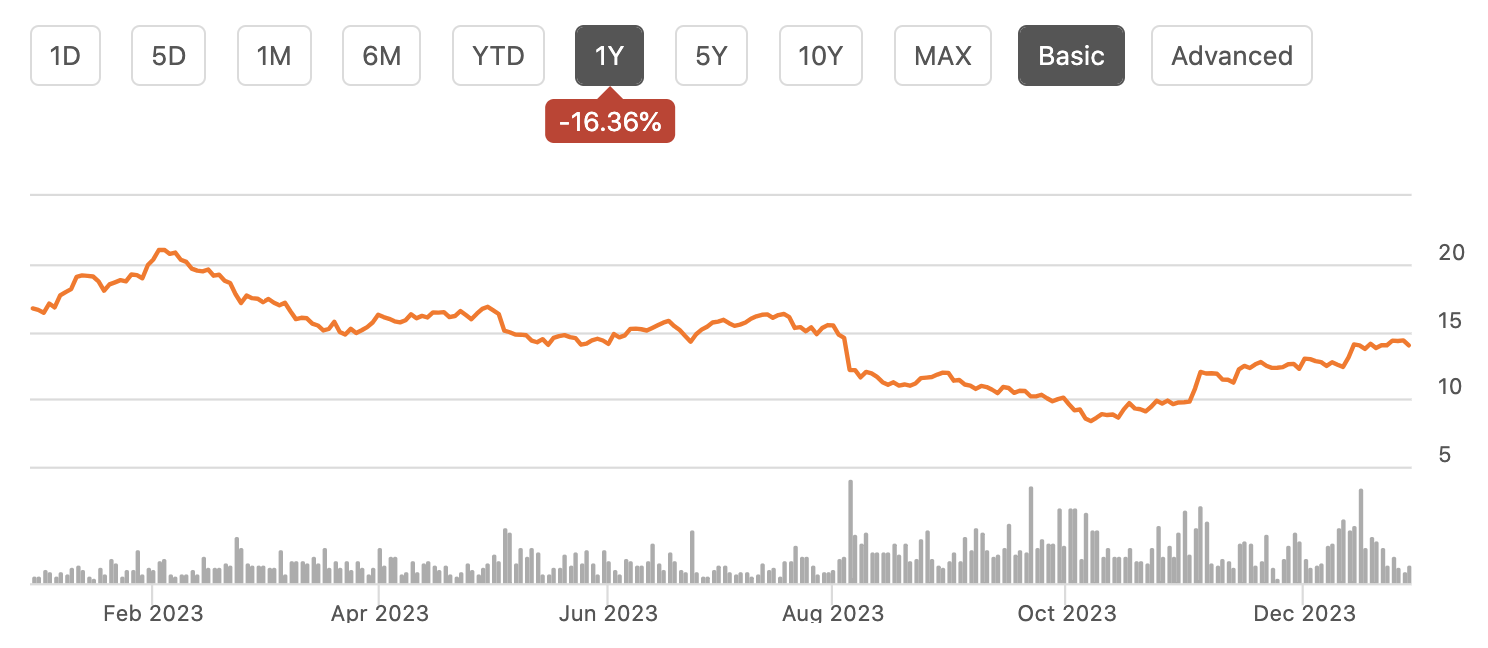

- Outfront Media shares have underperformed this year, losing 16% of their value, due to a weak advertising market and high debt.

- The company's revenue rose slightly in Q3, but lower operating margins and higher interest expense contributed to a decline in adjusted funds from operations.

- Outfront Media's billboard business is performing better than its transit display business, and the company is focused on converting static billboards to digital ones for increased revenue.

- However, elevated debt has led to slower cap-ex spending, and shares are now unattractively valued relative to Lamar.

Shares of Outfront Media ( OUT ) have been a poor performer this year, losing about 16% of their value in what has been a strong year for the stock market. While shares have a large dividend yield, the company is carrying significant debt which has curtailed growth initiatives. While lower rates could help in 2024, I would invest elsewhere in the sector as OUT may be more of a value trap than a value play.

{kind=link}

Outfront Media is an advertising company, primarily through its billboard business. It also has a transit display business. It operates across the United States, which accounts for over 90% of the business with the remainder primarily in Canada, though that business is in the process of being divested. Recently, the company has been struggling with a weak advertising market, rental inflation, and a debt-burdened balance sheet.

In the company’s third quarter , revenue rose by 0.2% to $455 million with adjusted funds from operations of $76 million (FFO), which was down by $11 million from last year. Lower operating margins drove about half of the decline with higher interest expense driving the remainder. Interest expense rose to $40 million from $33 million last year as about one-quarter of its $2.6 billion debt load is floating-rate. If the Federal Reserve begins cutting rates next year as expected, that should provide some relief, though a recent debt issuance will offset this benefit.

Looking into the company’s dynamics, let’s first focus on revenue drivers. US billboard media revenue rose by 2.6% to $344 million while transit revenue fell by 8.6% to $85 million. One challenge for the company has been that entertainment ad spending has been hurt by the strikes, with many movies and TV shows being postponed. About 2/3 of this headwind has been felt by the transit unit, even though it accounts for less than 20% of revenue. This has been a primary driver of the underperformance here, and this pressure should begin to fade by mid-2024.

We are also seeing a large divergence in advertising spending patterns, based on the nature of the advertiser. Local revenue rose by 6%, accounting for nearly 60% of the Outfront’s revenue, while national fell by 7%. As many of the TV media companies have experienced, 2023 was a challenging year for advertising as major national brands pulled back to reduce costs as consumer demand slowed. Local business advertising has proven to be more resilient this year. Fortunately, billboards generate much more of their revenue from local advertisers than cable TV (we have all seen billboards on the side of the highway advertising restaurants near upcoming exits, for instance), helping to insulate the business somewhat.

Daily billboard revenue rose by 3% to $2,800 with digital driving 29% of revenue, up 7% from last year. Digital has been the primary growth engine for billboard companies. Traditionally, billboards housed just one advertiser, usually under a 4-52 week contract. Digital billboards can rotate advertisers every few seconds. This rotation keeps the billboard “fresher,” allowing companies like Outfront to charge substantially more. Outfront has 40,806 US billboards, down 0.4% from last year. Of those, it has 2,105 digital billboards, up 16% from 1,811 last year.

In other words, digital accounts for just about 5% of its total billboards but 29% of billboard revenue, which makes clear how much more revenue these generate. This is why Outfront has been aggressively converting its static billboards to digital ones. Over time, this should greatly enhance the revenue capacity of the business. Unfortunately, with cash flow down from last year, the company has had to temper its growth spending. Cap-ex was down to $19 million in Q3 from $25 million in 2022 with growth spending down by a third. Lower capital spending is likely to slow digital transformation over the next year, which is likely to slow revenue growth somewhat. This is why the company is focused on deleveraging its balance sheet via divestitures.

While billboard revenue has been strong, transit revenue has been weak, partly due to the actors and writers strikes. The other challenge is that with hybrid working fewer Americans are commuting to the office each day. This means less people on subways, buses, and trains. Fewer people on the transit systems means advertisers are unwilling to pay as much for the space. It is similar to how a show with lower TV ratings can charge less for a 30-second commercial than a more popular show. This has been true of Outfront’s large business with the MTA in New York, where it has been lowering its growth estimates from the 6.5% increase initially modeled in the contract. OUT is trying to restructure transit contracts to reflect lower ridership, but unless we see a return to five-day in-the-office work schedules, we are likely to see this unit post slow growth.

Amidst stagnant revenue, OUT has also confronted rising expenses. Expenses rose by 2.2% as last quarter as billboard lease expense rose by 9% to $124 million while SG&A and corporate expenses were held flat. Total expenses rose by 150bp to 74.3% of revenue. While billboard companies typically own the actual billboard, they rent the land it sits on, and OUT has confronted elevated rental inflation as contracts lapsed over the past year and as it acquired costlier billboards. Based on guidance, lease expense growth should moderate, and management expects margin improvement in 2024 . This is aided partially by the fact that Morgan Stanley ( MS ) forecasts 10% advertising spending growth next year, with a 3% tailwind from politics and the Olympics. With its larger local presence which enabled the company to see revenue hold up better this year, I do expect OUT to underperform this 10% benchmark in 2024.

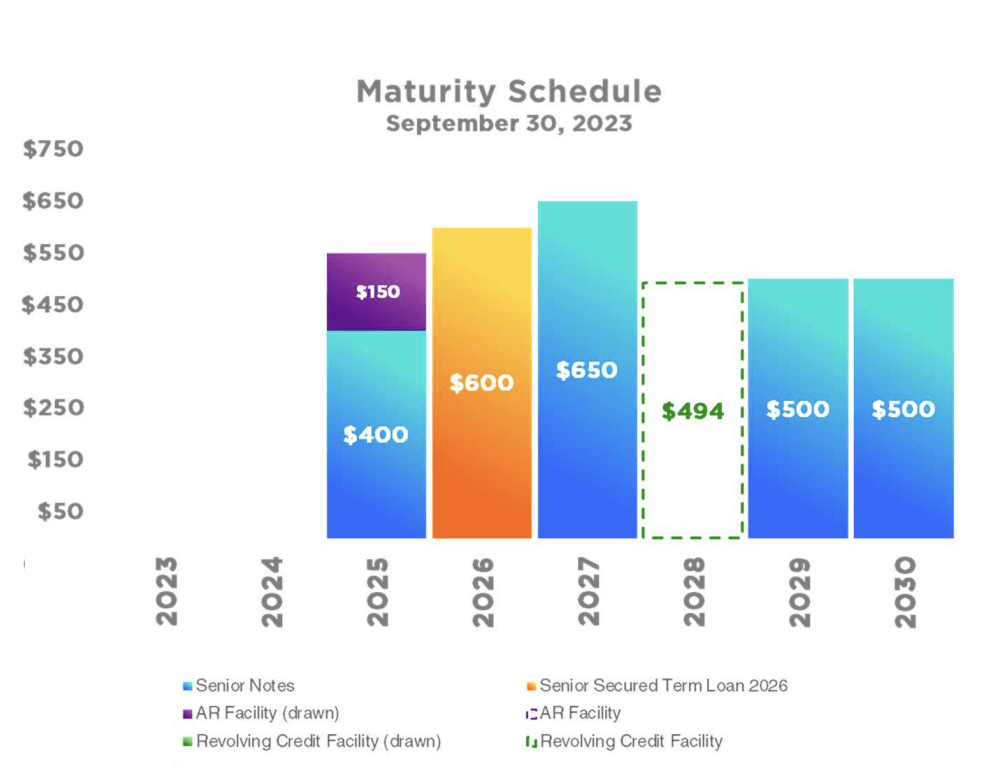

Finally, as noted, OUT carries 5.4x debt/EBITDA leverage. As you can see below, the company has no 2024 maturities and a well-staggered maturity schedule. Subsequent to quarter end, Outfront issued 7.375% 2031 debt to redeem its 6.25% 2025 notes. This will add about $5 million in interest expense. With about one-quarter of its debt load floating rate, this increased interest rate will offset the first three to four cuts the Fed delivers, keeping interest expense elevated for longer.

{kind=link}

Frankly, I was surprised by this debt issuance. Outfront is selling its Canadian business for $410 million CAD , or about $300 million USD. The plan is to use the proceeds to reduce financial leverage, and it should be worth about 0.25x of leverage. I would have expected OUT to use these proceeds expected in early 2024 to pay down most of the 2025 maturity, rather than issue higher cost debt to replace it. I expect proceeds to go towards paying down remaining 2025 and 2026 debt instead. Even after this transaction, leverage will remain above 5x.

When it comes to valuing shares, there are several approaches to take. First, we can begin with this asset sale. Canada accounted for about 5% of the business. At the same valuation, all of Outfront would be worth $6 billion. Today, shares have a $2.3 billion market value while it carries $2.6 billion of debt, for a $4.9 billion enterprise value, about a 20% premium. However, the company also carries $1.6 billion of operating leases, which are debt-like obligations that are assumed in M&A. Factoring some present value to these lease payments, the deal was done closer to OUT’s current value.

I prefer to look at Outfront relative to a peer. For comparison, Lamar ( LAMR ) generated 3% revenue growth last quarter, significantly outpacing Outfront, given less commuter transit exposure. Additionally, aided by its real estate ownership and long-term contracts, it has seen lower rental inflation. Critically, it has a better balance sheet with debt/EBITDA leverage of just 3.5x vs 5.4x for OUT. This has enabled LAMR to continue investing in its digital transformation, rather than significantly curtail growth cap-ex.

Simply put, Lamar has executed better. At first glance, it appears that Lamar is being rewarded with a superior multiple. It has about an 8% 2024 FFO yield while OUT has a 13% FFO yield, based on my expectation for $300-315 million in 2024 FFO. Put another way, LAMR’s equity is valued at 12.5x FFO vs OUT at 7.7x FFO. However, of this 4.8x multiple difference, most is consumed by debt. LAMR’s debt load is 3.9x FFO while OUT is 8.7x FFO, or a 4.8x differential. Their EV/FFO is essentially in-line. The businesses are being valued the same with more of LAMR’s value going to equity holders while more of OUT is consumed by debt.

With more debt comes more risk, which is why OUT pays an 8.6% dividend yield vs a sub-5% yield for LAMR. When things go right, having more leverage can generate stronger returns for equity, but when there are challenges, there is less margin for safety. Given OUT also is posting weaker margins and revenue trends, I view its higher debt load as a clear negative. With shares having rallied over 40% in just a couple of months, now appears like a good time to sell out of OUT and rotate into LAMR at a similar enterprise multiple, as investors can own a superior operator with a better balance sheet.

I would only be a buyer of OUT at a 10% discount to LAMR on an EV/FFO basis, or $11.50-$12. At $14, given its exposure to commuter transit, elevated interest burdens, I see downside and would sell OUT and move into a higher-quality business like Lamar that can more aggressively invest in growth.

For further details see:

Outfront: Elevated Debt Leaves Shares Unattractive