OUT - Outfront: Lamar Actually Looks Better Despite A Higher Multiple

2023-07-24 09:45:18 ET

Summary

- OUTFRONT Media has recovered its pre-COVID-19 revenues, though the price is still depressed.

- Though structured as a REIT, we see the high variability of AFFO as something that flies in the face of the standard REIT model.

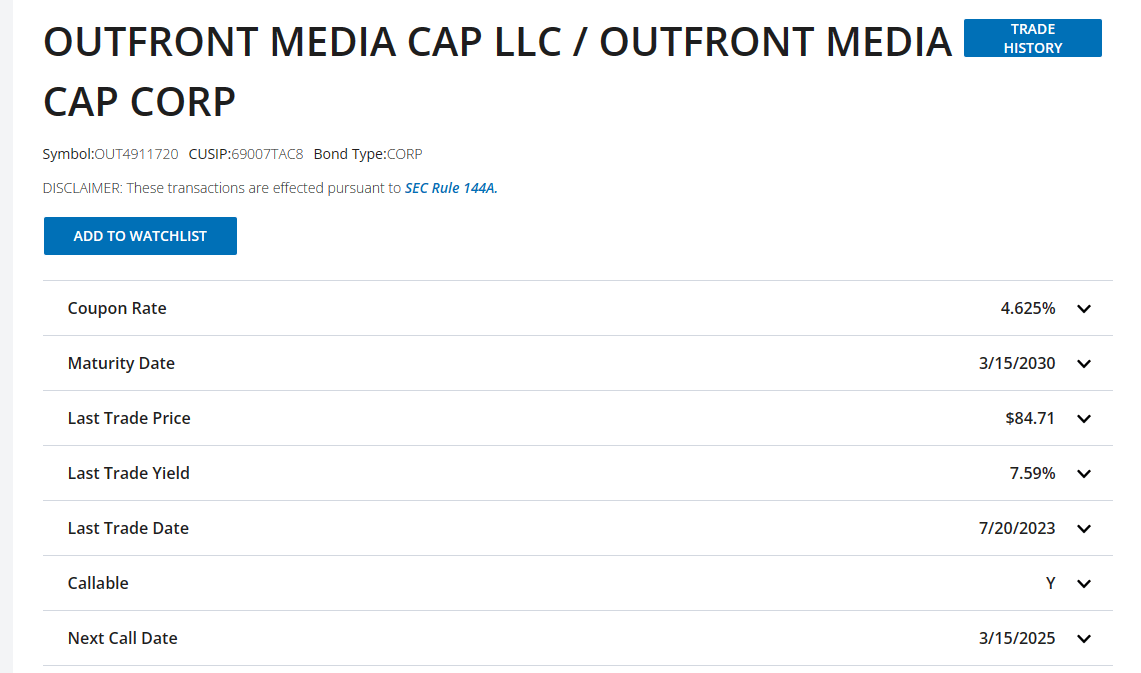

- We tell you why Lamar Advertising looks better and why we even passed on OUTFRONT debt yielding 7.59%.

OUTFRONT Media Inc. ( OUT ) owns billboards, building side art, bus stop posters, transit displays, and subway banners. The company is one of the largest owner-operators of "out-of-home" advertisements and has about a 20% market share. The company is structured as a REIT and was spun off from CBS in 2014 in this form. The stock caught our attention recently as we observed its extremely poor performance since early 2022.

While the COVID-19 related drop (lower outdoor advertising, especially in transit areas) and the subsequent bounce made sense, the giving away of all those gains, was less predictable. We looked to see if this would be a great entry point for a high-yielding stock.

Q1-2023

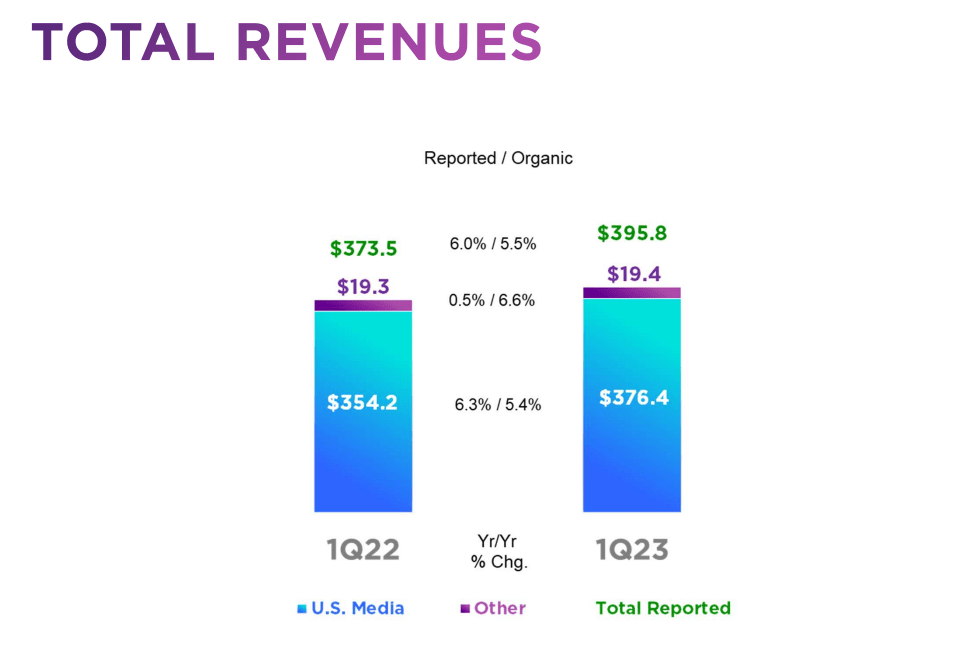

One thing that is immediately apparent while looking at OUT's numbers is that the revenues have indeed recovered from the COVID-19 lows. In fact, we will hit new records in the trailing 12-month metric as the next couple of quarters roll off.

In the most recently reported quarter, revenues were up about 6%.

{kind=link}

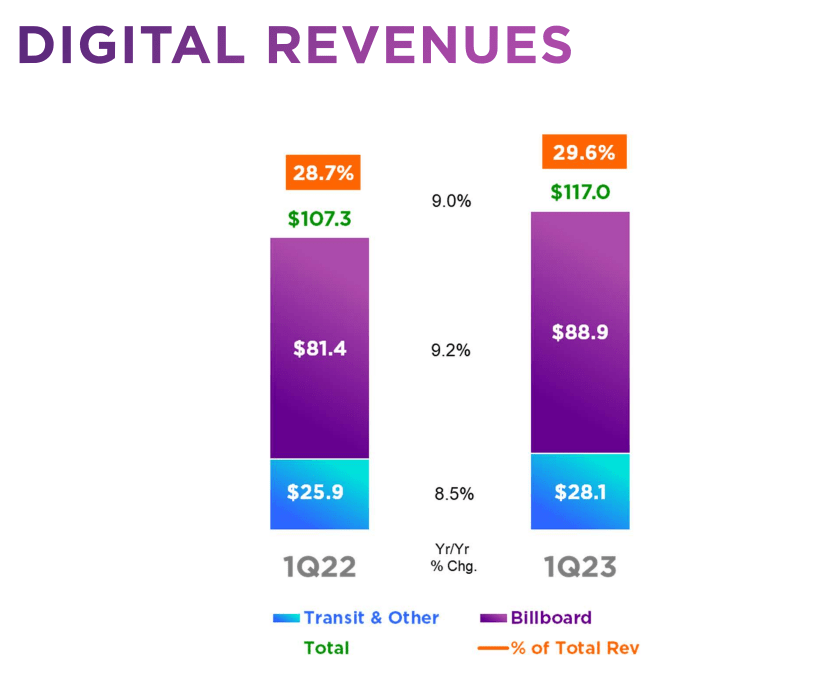

A key facet of OUT's growth strategy has been expanding its digital revenues. What that means is spending more money on digital advertising screens versus static ones. The former allows far more flexibility and creates more revenues per square foot of space. That segment expanded to 29.6% of total revenues in Q1-2023.

{kind=link}

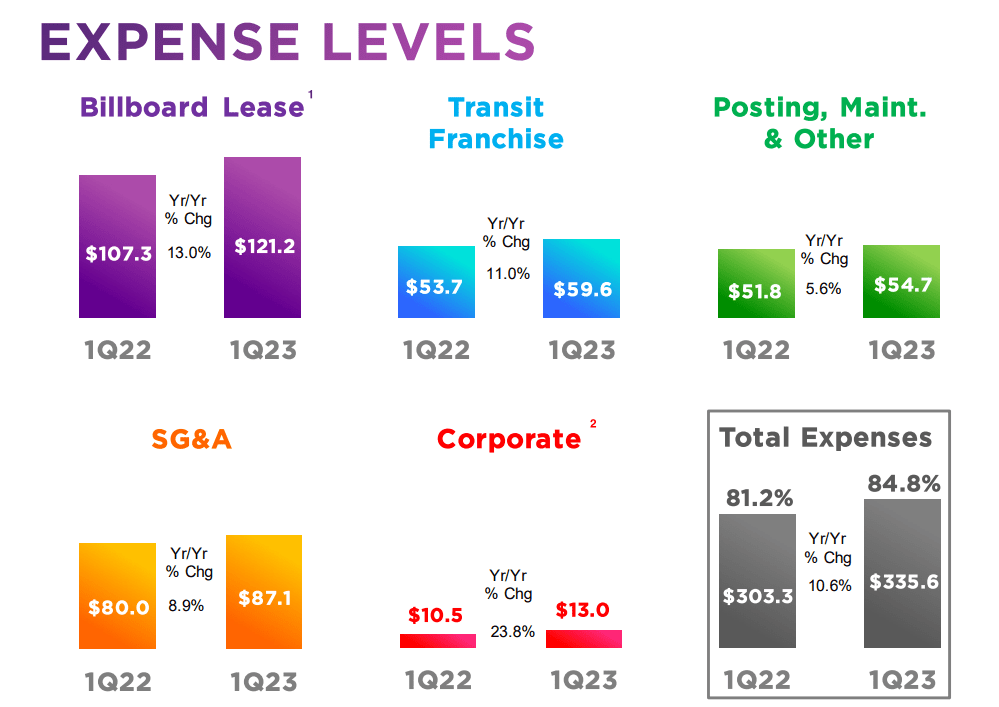

All of that was in line with where the company wanted to go. However, the expense side was not as pleasant. Billboard Leases were up 13%. Out of the six expense categories, only one was about in line with revenue growth. The rest were far higher.

{kind=link}

This is a good point to stop and distinguish the standard REIT model versus the OUT model. OUT, while operating as a REIT, does actually pay operating lease expenses or rent in many cases where it does not own the asset location outright. Not only does it pay lease expenses, but it also has variable lease expenses in many cases which can increase rather briskly.

Billboard property lease expenses represented 38% of billboard revenues in the three months ended March 31, 2023, and 36% in the three months ended March 31, 2022. The increase in billboard property lease expenses as a percentage of billboard revenues is primarily due to an increase in variable billboard property lease expenses.

Source: OUT Q1-2023 10-Q

In fact, we had previously run into OUT when we covered Landmark Infrastructure, which was taken private at a solid premium . Landmark was renting space to OUT.

LMRK Presentation Prior To Being Taken Over

{kind=link}

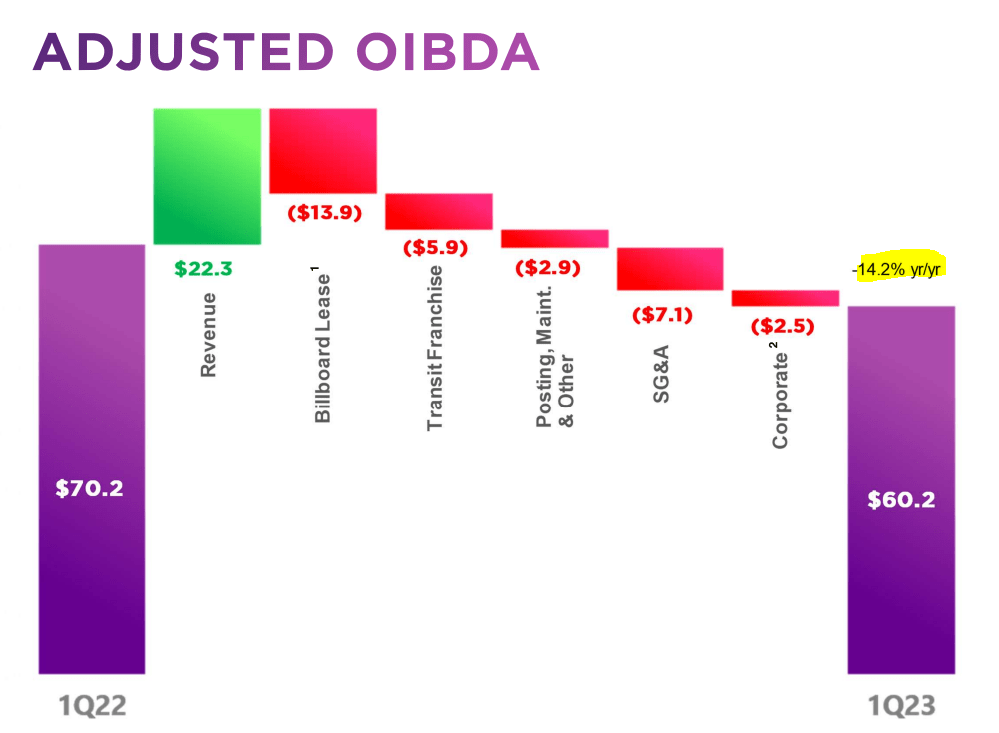

Getting back to the Q1-2023 performance, we saw that the adjusted operating income before depreciation and amortization, or OIBDA, declined by 14% year over year, thanks to expenses growing so strongly.

{kind=link}

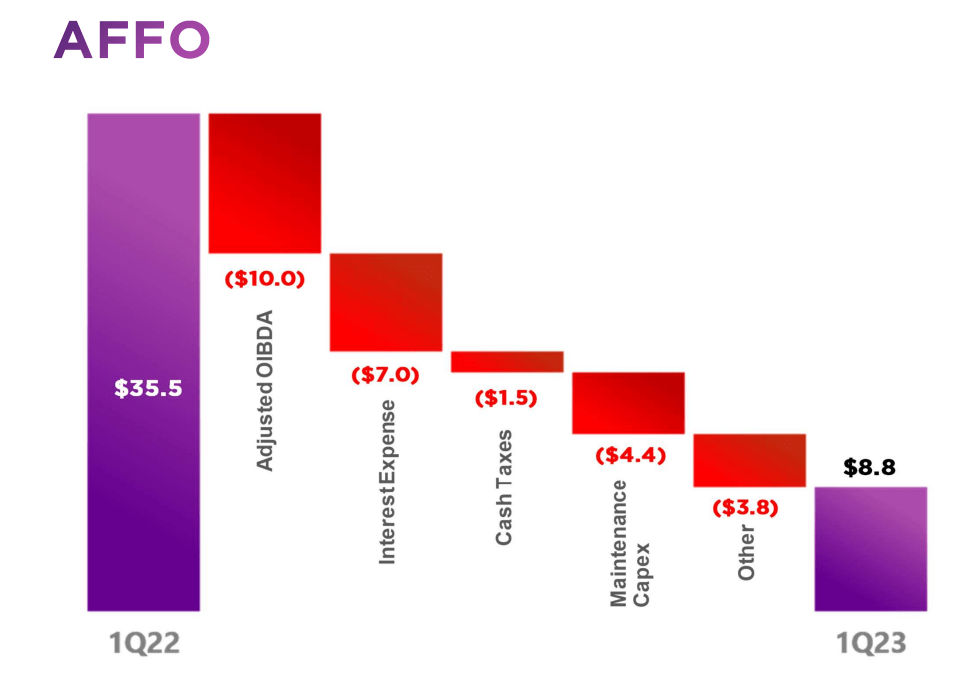

That was not the worst measure we saw the company report. Adjusted funds from operations or AFFO declined by 75% year over year. The primary culprit was of course the OIBDA declining. But beyond that, interest expenses, cash taxes, and maintenance expenses crept up.

{kind=link}

Big Picture Thoughts

One reason we dislike calling companies like OUT as "value plays" even if they sport a low AFFO or adjusted OIBDA multiple, is the sheer variability from quarter to quarter. This is even more true in the REIT sector. In most REITs you have a consistent change of revenues and AFFO tends to remain steady and gently move up. When you have such a high variability, you have to throw out that "It is cheap at 10X AFFO" theory.

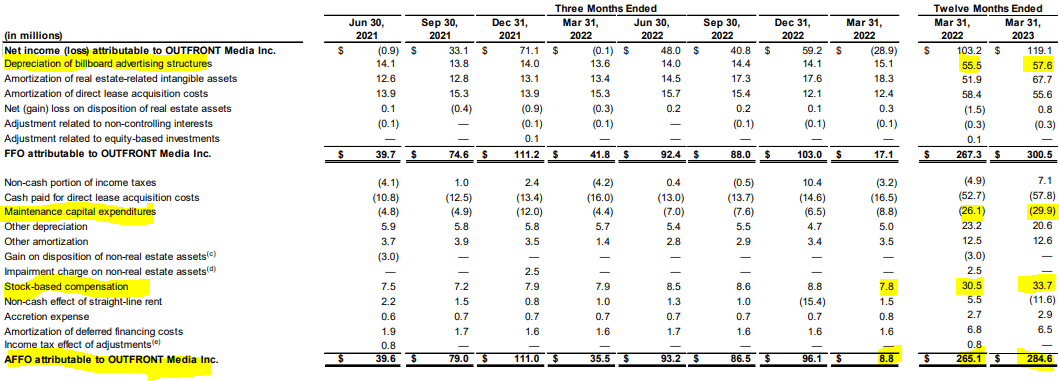

There are a few other points we want to bring up. The first being that depreciation is a very real cost for Billboards, and over time, you would expect to see maintenance capex and depreciation converge on the same number. Stock-based compensation is also a real cost, and it is pretty significant in relation to the total AFFO. In the most recent (and possibly a one-off) quarter, it was even more significant.

{kind=link}

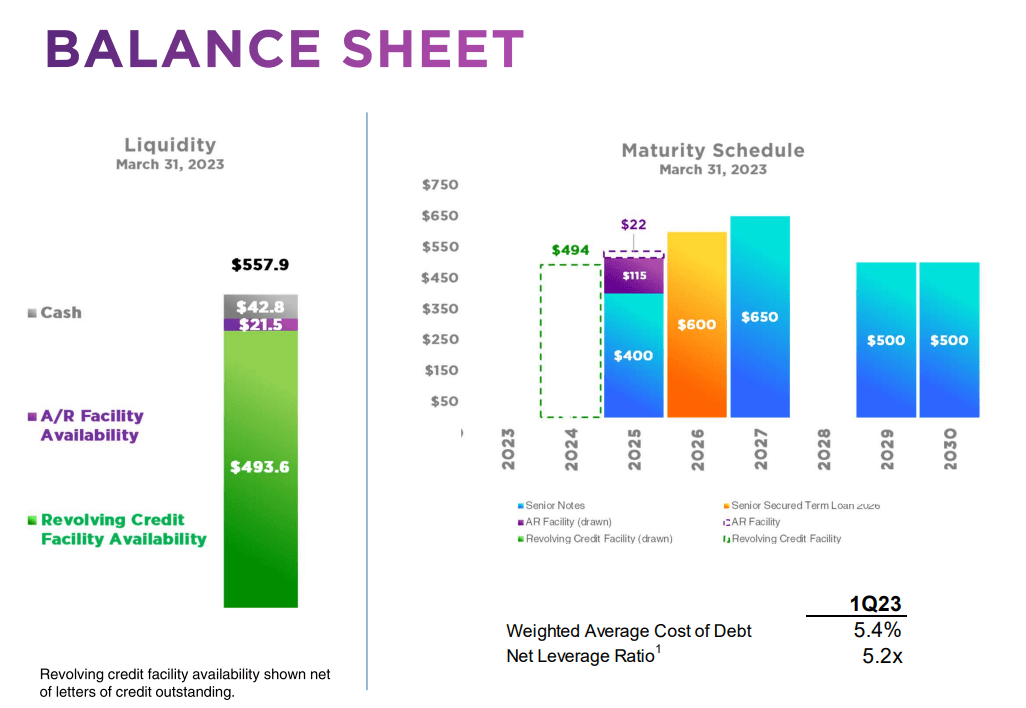

One final concern here is the debt. 5.2X net leverage ratio (read as net debt to adjusted EBITDA) with a weighted average cost of 5.4% is not terrifying by itself. But with a highly variable AFFO, it can be.

{kind=link}

The maturities are well spaced out and there are no immediate threats to the survival, but in the next recession, things may look different. Keep in mind that it has been a long time since we went into a recession with risk-free rates of over 5.25%.

Verdict

The stock's best comparative would be Lamar Advertising Company ( LAMR ) which you can also find on the Landmark Infrastructure slide earlier in the article. The two are at a similar EV to EBITDA ratio currently, but LAMR has a far larger market capitalization (over $10 billion versus $2.5 billion for OUT).

LAMR's debt is also rated at BB by S&P Global versus B- for OUT.

OUT looks incredibly cheap on an AFFO multiple (about 8X versus LAMR's 13X) for 2024. But LAMR's debt to EBITDA is closer to 3.0X, and that is a huge advantage. OUT is not cheap, just a company that is dialing up the leverage on a relative basis. If LAMR used that level of leverage, the market likely would take its AFFO multiple down a peg as well. We think, despite the higher multiple, LAMR is the better bet here. We just cannot see ourselves getting into a company that is this levered with this level of variability in AFFO. The 7.87% dividend yield just does not do it for us. Sometimes the stock does not make sense but bonds do. The longer-dated bonds yielding 7.59% to maturity are certainly a safer option.

{kind=link}

But we are getting investment grade bonds yielding that much today in select cases, and we really don't see the need to reach deep into junk territory for that kind of yield. We won't be buying that, either. We will be keeping an eye on LAMR though for a potential entry point down the line.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Outfront: Lamar Actually Looks Better Despite A Higher Multiple