OSG - Overseas Shipholding Group: Creating Shareholder Value

Summary

- OSG has performed handsomely this year, up ~51% year-to-date.

- Despite the stock's appreciation, future guidance suggests OSG could move higher over the coming quarters.

- Therefore, the company is a Buy with a reiterated $3.10/sh price target.

To hold, or not to hold, that is the question. This mockery of Shakespeare's famous epigram suits my present rumination whether to maintain a position in Overseas Shipholding Group, Inc. ( OSG ). The stock has performed handsomely this year, up ~51% YTD, but its ascension may have run its course. After a steady climb starting in July, OSG sputtered in late September on news of insider selling. Interest has remained tepid ever since.

With that said, future guidance suggests the stock could move higher over the coming quarters. Management foresees a promising '23 driven by ample free cash generation and opportunities to expand into new markets. This forecast is bolstered by bold insider buying from the company's CEO. There has been, however, an equal amount of institutional selling, which suggests management's outlook might be overly optimistic.

Overall, OSG's fundamentals remain solid, with an exceptional managerial outlook, and the company appears undervalued relative to peers. Nevertheless, this year's price appreciation suggests that at least some of the outlook is already baked in. Therefore, OSG is recommended as a Buy and the previous price target of $3.10/sh remains intact

Stock Appreciation

OSG experienced strong price appreciation earlier this year, with the stock up 50%-plus year-to-date. It hit a multi-year intraday high of $3.39/sh in September:

The stock's run was poised to continue until it was interrupted by the news that Anja Manuel, an OSG independent director, sold 54% of her position at $3.17/sh. The stock sold off subsequently and has traded narrowly since.

Guidance

Forward guidance contravenes recent price action. In the Q3'22 conference call , management guided for FY'22 TCE revenues "at about $420 million and adjusted EBITDA should exceed $133 million." Furthermore, OSG anticipates, after share repurchases, year-end cash balances between $90 million and $100 million. The cash balance puts OSG in a marvelous position to return capital to shareholders in the near-term.

Additionally, OSG is expecting FY'23 to be as good, if not better, as FY'22 despite returning three vessels to American Shipping Company ( OTCQX:ASCJF ) earlier this month. Redelivery of the ASC vessels will reduce annual fixed payment obligations by ~$27m/year yet the company expects to maintain similar operational performance as FY'22. FY'23 TCE revenues for 2023 are expected to be ~$400m with adj. EBITDA between $100m and $135m.

To this end, management stated "OSG vessels are essentially fully committed well into the middle of next year" with "92% of available (Jones Act) vessel operating days [] covered for all of 2023." The company also is making inroads into the renewable diesel trade. On the call, management noted OSG has:

... negotiated time charters with four different charters engaged in renewable diesel trade with the result that by the middle of next year, 50% of (the company's) conventional tanker fleet will be employed in trades related to renewable diesel, with several of these contracts extending beyond the end of 2023.

As for '23 cash flow, OSG anticipates FY'23 FCF, after debt service and capex, between $50m and $55m. Adding that to '22 year-end balance, OSG is on course to have ~$140m-$155m in cash at the close of '23. With that amount, the company could easily retire a substantial chunk of debt, acquire a new vessels, or potentially return a portion to shareholders.

Share Ownership

OSG's rosy outlook has made its CEO, Samuel Norton, bullish on the company's stock. Earlier this month, he announced purchasing 350k @$2.92/sh from Cyrus Capital Partners - OSG's second largest outside shareholder. The purchase put Mr. Norton's total position in OSG at 2.45m shares (~3.1% of OSG). Cyrus' divestiture is the second sale the firm has made of OSG's shares in the last two months. In November, Cyrus sold 5m @$2.86/share to OSG in a private transaction. While there are several reasons why one sells, there's only one reason for buying. Mr. Norton's purchase inspires confidence that OSG will continue to create shareholder value despite this year's capital appreciation.

Valuation

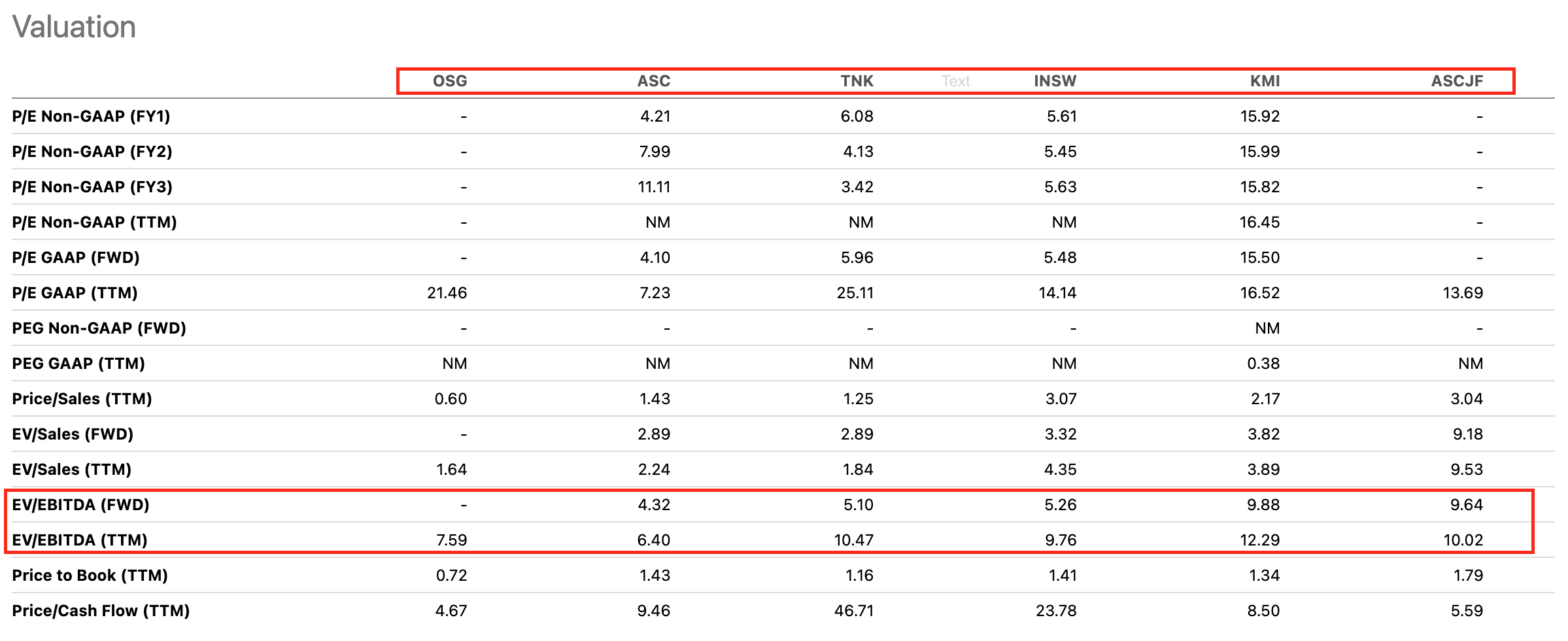

OSG currently has an enterprise value of ~$685m (inclusive of its marketable securities and operating and financial leases, at fair market). OSG's FY'23 Adj. EBITDA between $100 - $135m implies the company trades 5.1x - 6.8x FWD EBITDA, with a midpoint of 6.0x. This compares to an average 6.8x for OSG's peers:

{kind=link}

However, Kinder Morgan ( KMI ) and American Shipping Company - OSG's Jones Act competitors - trade at ~9.8x FWD EBITDA. Whether or not OSG could fetch a similar multiple as its Jones Act peers is speculative, although not unrealistic. But even if it were to trade at 7x FWD EBITDA, still a substantial discount to Jones Act peers, the stock could trade north of $4/sh.

All things considered, OSG remains a Buy and is one to watch over the coming quarters.

For further details see:

Overseas Shipholding Group: Creating Shareholder Value