OVID - Ovid Therapeutics: The GABA Gambit In Seizure Wars

2023-10-04 07:14:23 ET

Summary

- Ovid Therapeutics' OV329 shows promise in early Phase 1 data for treating pharmacoresistant epilepsy, boasting superior pharmacokinetics and safety profiles.

- Financials are strong with a robust current ratio of 10.1 and 24-month cash runway, but cash burn and operational expenses remain concerns.

- Investment recommendation: Speculative "Buy" for investors with higher risk tolerance, focusing on the upcoming Phase 1 data release in 2024 as a value inflection point.

At a Glance

In the ever-evolving landscape of antiepileptic drugs, Ovid Therapeutics' (OVID) OV329 represents a pivotal moment in GABA-AT inhibition. With superior pharmacokinetics and a favorable safety profile exhibited in early Phase 1 data, the candidate sets the stage for potentially revolutionizing pharmacoresistant epilepsy treatments. From a financial standpoint, the company's solid liquidity metrics provide a safety net, but they must be weighed against the persistent operational burn. The imminent release of full Phase 1 data in 2024 serves as a critical inflection point that could either vault the company's valuation or send investors scurrying. These clinical and financial contours offer a complex but intriguing narrative for Ovid. While the current financials provide a cushion, any faltering in the clinical trajectory of OV329 could dramatically affect the company's burn rate and necessitate capital infusions. Keep an eye on these pivotal data points as they will provide a comprehensive view of both the drug's clinical prospects and the company's financial health.

Q2 Earnings

To begin my analysis, looking at Ovid Therapeutics' most recent earnings report for Q2 2023, revenue made a jump to $75,000 from virtually nil in the same quarter last year. However, this figure remains inconsequential against operating expenses, which slightly contracted to $14.2M from $14.3M YoY. R&D expenses remained stable at $6M. G&A outlays are still a significant burden at $8.2M. Net loss narrowed to $12.4M from $14.6M YoY. The company continues to dilute shares at a minimal pace, with weighted-average common shares outstanding rising by 0.2% YoY to 70.5M. This indicates a mild but non-negligible impact on shareholder value.

Financial Health

Turning to Ovid Therapeutics' balance sheet , the company holds a sum of $96.5M in highly-liquid assets, broken down as follows: cash and cash equivalents are at $71.6M and marketable securities at $24.9M. The current ratio, calculated as total current assets ($102.2M) divided by total current liabilities ($10.1M), stands at a robust 10.1. For the last six months, the net cash used in operating activities has been $23.8M, resulting in an estimated monthly cash burn of approximately $4M. This implies a cash runway of roughly 24 months. However, it is important to caution that these values are based on historical data and may not be indicative of future performance.

Based on these metrics, the probability of Ovid requiring additional financing within the next twelve months appears to be low. The healthy current ratio and the cash runway of two years provide a comfortable financial buffer for the company. That said, unforeseen developments in clinical trials or strategic investments could alter this outlook. These are my personal observations, and other analysts might interpret the data differently.

Equity Analysis

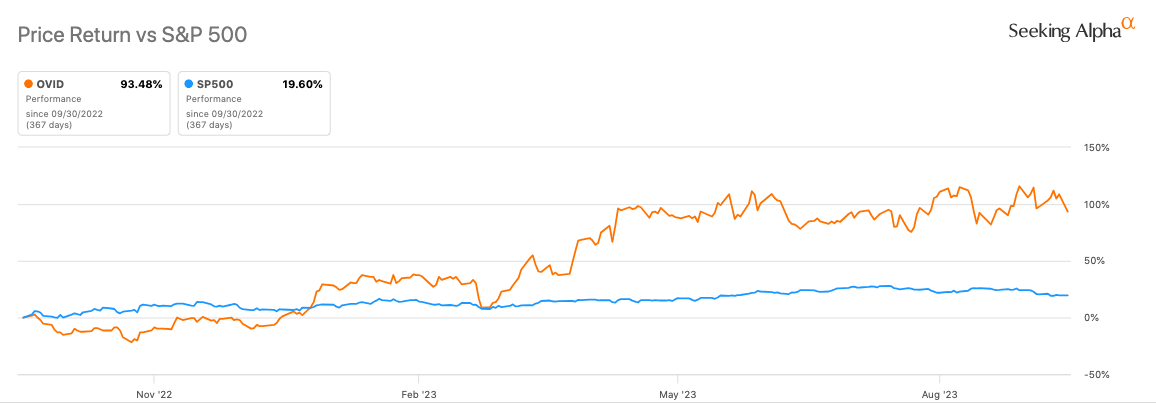

According to Seeking Alpha data, Ovid Therapeutics sports a market cap of $271.11M, a moderate signal of market confidence given the pipeline and partnership with Takeda (TAK). Analyst projections for 2024 revenue leap to $21.4M, a substantial increase, underscored by soticlestat's expected commercialization. Comparing stock momentum, OVID has outperformed SPY in all considered time frames-especially noteworthy is the 91.4% 9-month gain. The 24-month beta of 0.61 suggests lower volatility relative to the market.

{kind=link}

Short interest is at 5.99%, indicating a moderate level of bearish sentiment. Ownership is diverse but leans towards hedge fund managers (31.19%), suggesting that institutional investors find value in the asset. Institutional holdings reveal more increased positions (43) than decreased (28), indicating growing confidence. Lastly, there was no insider trading in the last 12 months.

OV329: A 'Brainy' Solution to Old GABA-AT Problems

Ovid's OV329 is strategically positioned to fill gaps left by previous GABA-aminotransferase (GABA-AT) inhibitors like Sabril (vigabatrin). Sabril's challenges were twofold : it necessitated high dosing due to poor ability to cross the blood-brain barrier, and its use came with significant safety risks, specifically a 25-50% likelihood of causing visual field defects through retinal damage.

OV329 aims to build on the shortcomings of existing options by offering a more targeted and potent GABA-AT inhibition. It is designed to be far more efficient at inactivating GABA-AT compared to its predecessors, providing potential for significantly lower dosing requirements. This is not merely incremental; it is transformative in the quest for balancing efficacy with safety. Specifically, early indications suggest that OV329 could reduce the severity of N-methyl-d-aspartate (NMDA)-induced seizures, which makes it a particularly promising candidate for pharmacoresistant epilepsies.

Moreover, the early Phase 1 data, showing no safety signals, already distinguishes OV329. This builds on the promising outlook that the drug candidate may not only be more efficacious but also safer, potentially eliminating the risks of retinal toxicity that have plagued earlier compounds. While full Phase 1 findings are anticipated in 2024, this novel asset may represent a new paradigm in GABA-AT inhibition, offering a more favorable safety and pharmacokinetic profile.

My Analysis & Recommendation

In light of the recent financials and pipeline developments, Ovid Therapeutics presents an intriguing investment narrative. The financial cushion provided by a robust current ratio of 10.1 and an estimated 24-month cash runway adds a layer of security. Importantly, the company may receive up to $660 million in regulatory and commercial milestones plus royalties for soticlestat (currently in Phase 3 trials for rare epileptic conditions), which could serve as a significant capital inflow to offset R&D expenditures. This is a compelling financial synergy, especially given that Ovid carries no further development obligations for soticlestat.

Transitioning to the drug pipeline, OV329 is what I'd categorize as a "dark horse" candidate for seizure treatments. While incumbent GABA-AT inhibitors like Sabril have proven clinically beneficial, their therapeutic window has been compromised by dosing challenges and severe adverse effects like retinal damage. OV329, by virtue of its enhanced pharmacokinetics and early safety profile, aims to circumvent these hurdles. Its potential for significantly lower dosing could be a game-changer in terms of safety and efficacy. Investors should pay close attention to the full Phase 1 data release in 2024, which could validate or negate this optimism. This data will not only potentially elevate OV329 to a new therapeutic class but also serve as a significant value inflection point for Ovid.

It's critical to understand, however, that OV329 is in early-stage development. While the early findings are promising, the Phase 1 trial completion in 2024 is the immediate milestone that will define its risk profile. Given that most drug failures occur during Phase 2 or 3 due to either safety concerns or lack of efficacy, prudent investors should not discount the inherent risks of early-stage drug development.

On a tactical note, watch for any shifts in institutional holdings and keep an eye on short interest as a barometer for market sentiment. Additionally, keep track of any unexpected escalations in R&D or G&A expenditures, which could necessitate additional financing despite the comfortable cash runway.

In summary, for investors with a higher risk tolerance and a belief in the disruptive potential of OV329, Ovid could be a speculative "Buy." The stock offers a blend of financial stability, potential for significant milestone payments from soticlestat, and a drug candidate that could rewrite treatment paradigms in seizure management. However, it's essential to be cognizant of the early-stage nature of OV329 and the inherent risks that accompany drug development in this complex therapeutic area.

Risks to Thesis

While my overall recommendation is a "Buy," there are nuanced risks that could challenge this stance:

-

Cash Burn: A $4M monthly cash burn is manageable now, but what if OV329 encounters setbacks that elongate the clinical timeline? The runway might not be as lengthy as it appears.

-

Competition: New GABA-AT inhibitors, or any anti-epileptics, could emerge, rendering OV329 less compelling. Furthermore, should OV329 make it to the market, it will face significant competition from existing, well-established drugs marketed by biopharma behemoths.

-

Regulatory Hurdles: Approval pathways are often fraught with delays and unexpected requirements. Any setback here would hit the stock hard.

-

Short Interest: A 5.99% short interest indicates there are parties betting against the stock. It's worth investigating their rationale.

-

Execution Risk: The company has yet to commercialize any product. Until it proves it can effectively do so, this remains a significant risk.

-

Reliance on Partnerships: Ovid's milestone payments from soticlestat are not guaranteed. Any hiccups in the partnership could strain finances.

-

Institutional Holdings: While it leans toward hedge fund managers, any divestment on their part could be a bearish signal.

-

Data Interpretation: Phase 1 data for OV329 might look promising, but the clinical significance remains unclear until larger trials validate these findings.

Finally, investing in micro-cap companies like Ovid comes with unique risks, often amplified compared to larger firms. Liquidity is a prime concern; these stocks are generally less liquid, making it difficult to execute large orders without affecting the stock price. Volatility is often higher, susceptible to market sentiment and news flow. Limited financial resources mean less room for error in R&D or commercialization. Also, these companies often have less diversified revenue streams and may rely on one or two key products or partnerships, making them vulnerable to any setbacks in those areas. Lastly, lower analyst coverage can result in less efficient pricing, creating risks of market manipulation.

For further details see:

Ovid Therapeutics: The GABA Gambit In Seizure Wars