OXM - Oxford Industries: Undervalued Company With Solid Brand

2023-11-26 01:45:29 ET

Summary

- Oxford Industries is a clothing firm with innovative brands and a stable balance sheet.

- The company pays a safe dividend of 2.75% and has a 34-year streak of payouts.

- Analysts rate Oxford as a "buy" with a 13.44% potential upside and recognize its strong brand image.

- Oxford is currently undervalued assuming my DCF assumptions resulting in a strong buy rating.

Oxford Industries ( OXM ) has seen a recent pullback due to consumer fears in the near future. However, I believe that Oxford Industries is currently a strong buy due to its solid dividend, excellent ROIC, stable balance sheet, resilient earnings, innovative brands, and undervaluation using my DCF figures.

Business Overview

Oxford Industries, Inc. is a clothing firm that finds, develops, promotes, and ships lifestyle and other brand items all over the world. The company's product lines include men's and women's sportswear and accessories under the Tommy Bahama brand; dresses, sportswear, bags, jewelry, and belts for women and girls; children's clothing, swimwear, and licensed items under the Lilly Pulitzer brand; and products for men, women, and children under the Southern Tide brand.

Furthermore, the company holds licenses for a number of products under the Tommy Bahama and Lilly Pulitzer brands, including stationery and gift items, home furnishings, eyewear, bedding and bath linens, as well as fabrics, leather goods and gifts, headwear, hosiery, sleepwear, shampoo, toiletries, fragrances, cigar accessories, and other products.

Oxford Industries, Inc. distributes its goods via department stores, specialty shops, retail locations, off-price retailers, multi-branded online retailers, and e-commerce websites. Tommy Bahama food and beverage outlets, outlet stores, and full-price retail stores dedicated to individual brands are all run by the company.

Oxford

Financials

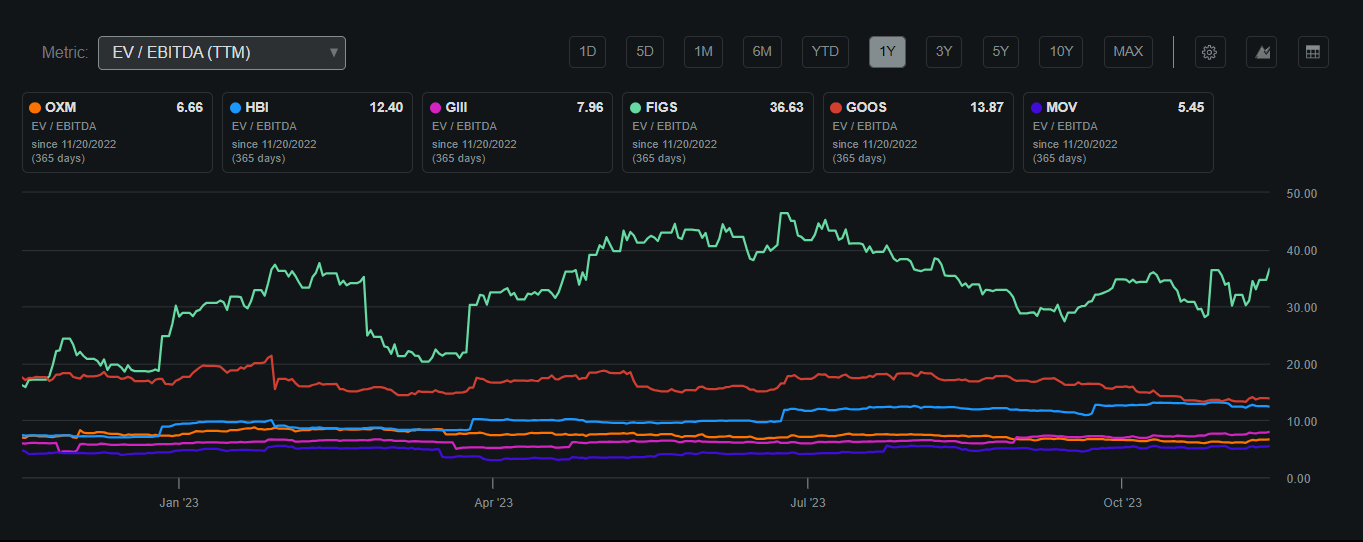

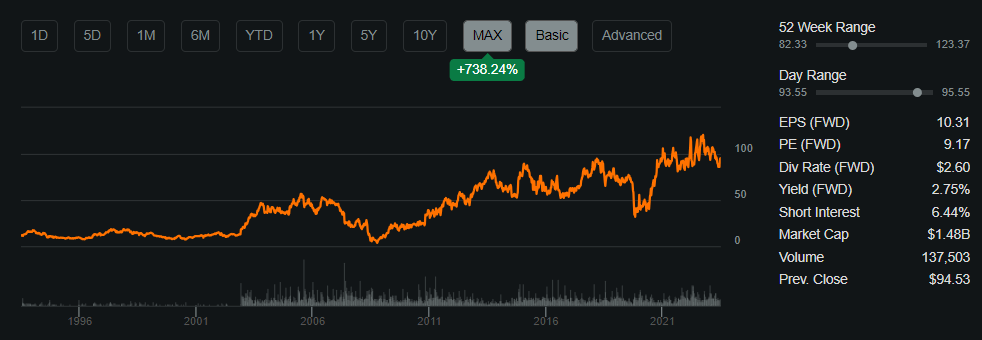

Oxford's current market capitalization is around $1.48 billion, accompanied by a commendable Return on Invested Capital of 19%. The existing stock price is $95.35 per share, slightly below its 200-day moving average of $102.23. The company's EV/EBITDA ratio stands at 6.66, indicating a valuation below the industry average. This suggests that Oxford is trading at a position considered undervalued compared to its peers within the industry.

Oxford EV/EBITDA Compared to Peers (Seeking Alpha)

{kind=link}

Oxford also pays a dividend of 2.75% which represents a payout ratio of 19.25%. This safe dividend allows Oxford to provide value to shareholders through multiple channels and attracts those who are interested in consistent income as it has a 34-year streak of payouts. I believe that this dividend is sufficient at current levels because I believe that capitalizing on the 19% ROIC would be the priority as scalability is critical in retail where brand image is of great importance to sales and relevancy.

Share Performance (Seeking Alpha)

{kind=link}

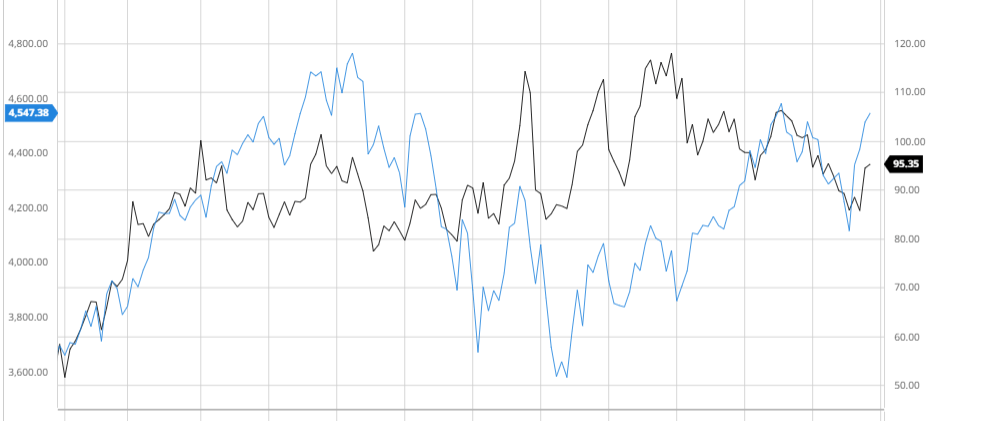

Performance Compared to the Broader Market

Over the past 3 years, Oxford has underperformed the broader market when adjusting for dividends. I believe that this underperformance is attributed to the past year in which macro headwinds of rates and inflation are beginning to chip away at consumer sentiment hurting retail. I believe that as macro headwinds subside, Oxford will begin to outperform due to its solid brand image coupled with its scale.

Oxford Compared to the S&P 500 3Y (Created by author using Barchart.com)

{kind=link}

Earnings

Oxford recently reported mixed Q2 2023 earnings with EPS beating by $0.08 at $3.45 and revenues missing by $3.97 million at $420.3 million indicating a 16% YoY growth. I believe that these earnings demonstrate that although Oxford is experiencing negative sentiment in regard to its consumers, the firm has been able to improve profitability in order to compensate for the sales miss. With earnings estimates being positive in the upcoming years, I believe that if inflation continues to decline and does not remain sticky, Oxford can regain consumer demand and not suffer considerable financial losses leading to a quick rebound to its highs. With an expected EPS of $0.97, which is a decline from last year's $1.46, I believe that outperformance is critical to seeing if consumer sentiment is continuing to hold at estimates which could alter my assumptions in the short term.

Earnings Estimates (Seeking Alpha)

Balance Sheet

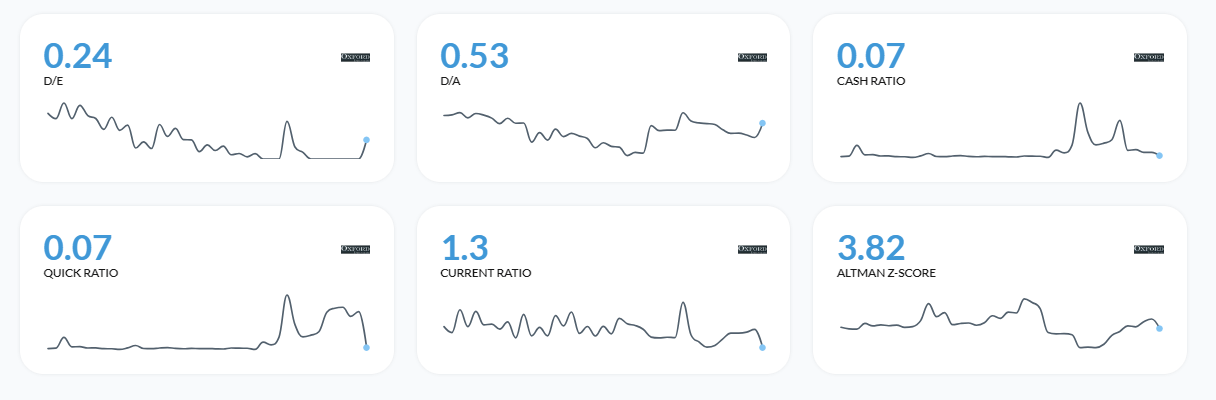

Oxford also holds a solid balance sheet with $335 million of debt along with a Current Ratio of 1.3 and an Altman-Z-Score of 3.82. This demonstrates Oxford's ability to remain solvent in the long term through macro headwinds and shows the safety of the dividend being issued thus far.

Solvency Ratios (Alpha Spread)

{kind=link}

Analyst Consensus

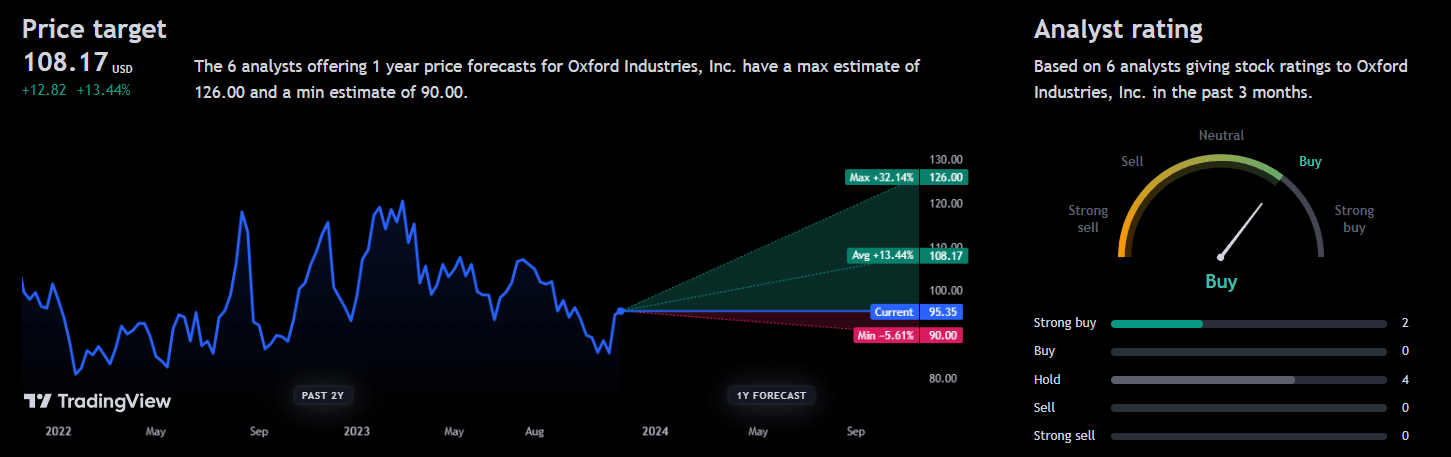

Analysts currently rate Oxford as a "buy" with a 1-year average price target of $108.17 presenting a potential 13.44% upside. I believe that analysts also recognize Oxford's strong brand image and the cooling of inflation leading to solid results in the next year.

Analyst Consensus (TradingView)

{kind=link}

Valuation

Before calculating a fair value for Oxford, I computed the firm's current Cost of Equity using the Capital Asset Pricing Model. For this, I used a risk-free rate of 4.46% which is in line with the current 10-year treasury yield which got me a Cost of Equity of 7.85%.

Cost of Equity (Created by author using Alpha Spread)

{kind=link}

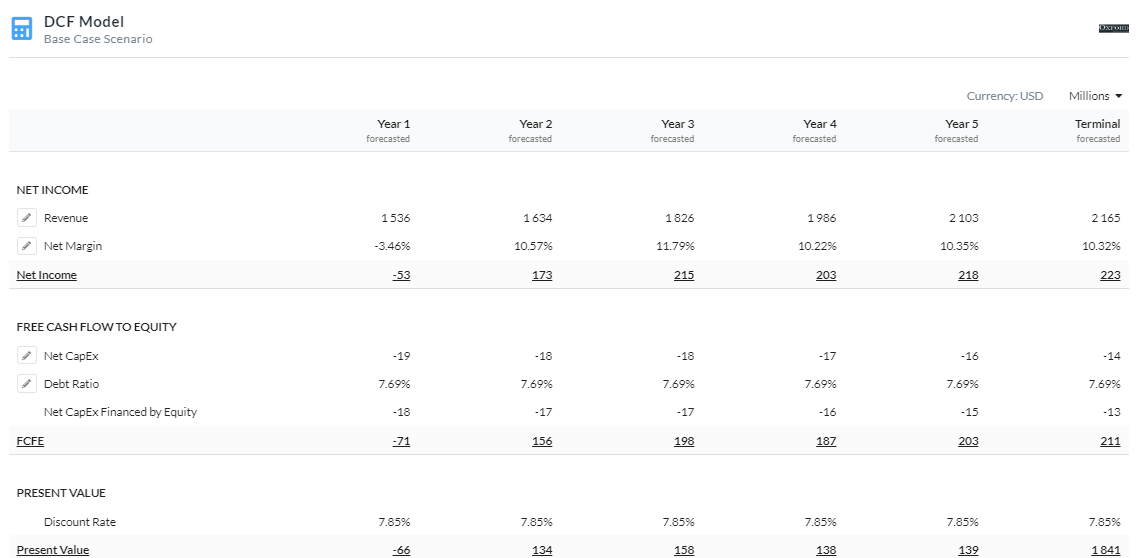

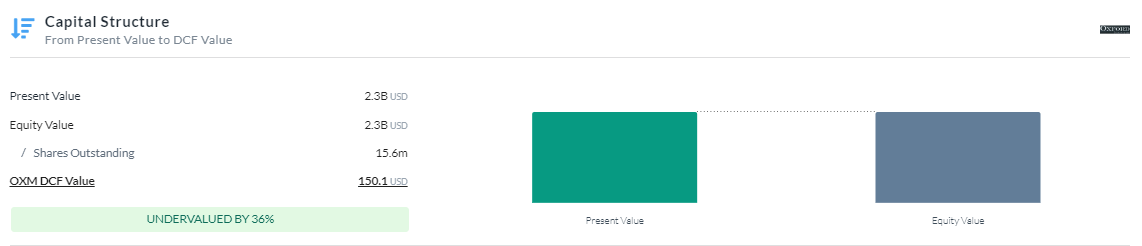

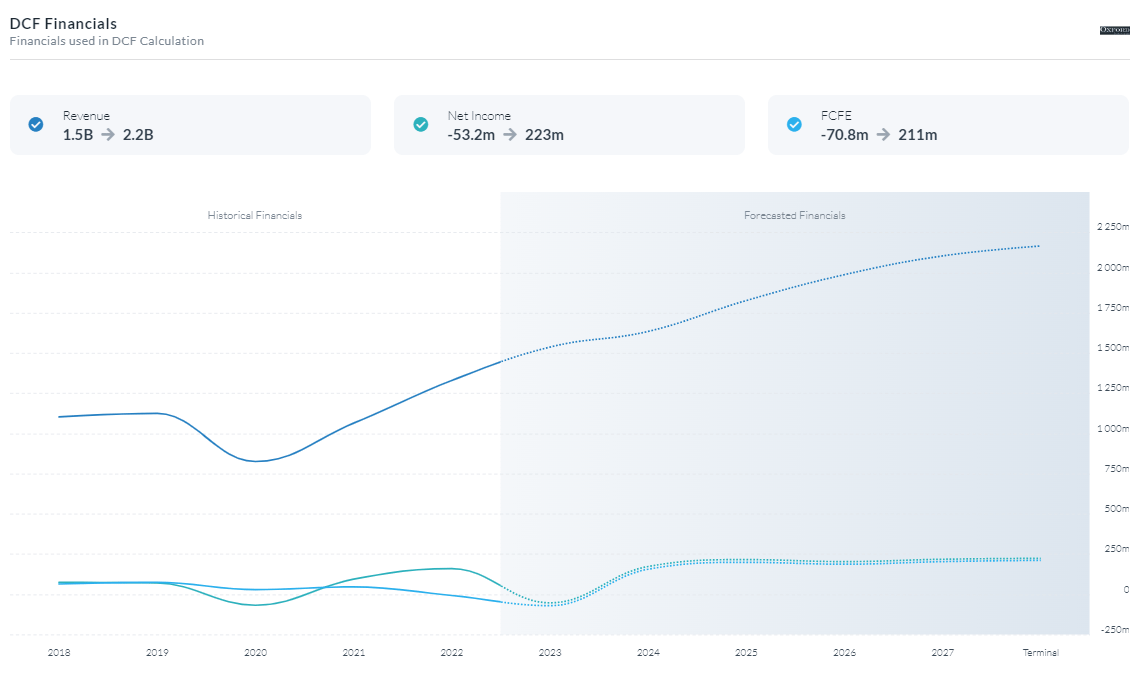

Using the previously calculated Cost of Equity as my discount rate, I calculated Oxford's fair value using a 5-year Equity Model DCF using FCFE. I decided to keep the discount rate in line with my Cost of Equity because Oxford holds a solid balance sheet and brand which they can leverage in order to improve their financial position during these headwinds. I also estimated revenues and margins to continue growing in line with analyst expectations, which has been very accurate in the long run due to Oxford's stable nature. This resulted in a fair value of ~$150.1 presenting a potential 36% upside.

5Y Equity Model DCF Using FCFE (Created by author using Alpha Spread) Capital Structure (Created by author using Alpha Spread) DCF Financials (Created by author using Alpha Spread)

{kind=link}

{kind=link}

{kind=link}

Constant Product Innovation Resulting in Solid Growth

Oxford Industries' dedication to product innovation is demonstrated by the Southern Tide brand, which not only strengthens the company's position in the market but also generates significant financial gains. Oxford Industries satisfies the increasing demand for performance-driven and environmentally responsible design by bringing cutting-edge fabric innovations, such as moisture-wicking fabrics or sustainable fabric alternatives, into Southern Tide's clothing. This tactical move increases the brand's market share and fosters consumer loyalty by drawing in eco-aware customers and establishing it as a fashion leader.

Oxford Industries has proven again that it can adapt its goods to meet changing consumer needs by including cutting-edge technologies like UV protection into Southern Tide's apparel. This leads to improved profit margins and revenue growth in addition to fostering brand distinctiveness and allowing the firm to charge premium pricing for its creative services. Beyond only increasing sales, Southern Tide's innovative reputation will favorably impact brand perception, drawing in a larger consumer base and fostering long-term financial success.

Oxford Industries offers options for income diversification through its limited-edition collections and strategic collaborations under the Southern Tide brand. These efforts, which are motivated by a desire to remain at the forefront of fashion trends, allow the business to take advantage of the buzz around exclusive releases, which will lead to higher sales and a feeling of exclusivity that appeals to customers.

These innovative strategies will lead to solid improved cash flows which will foster growth through its 19% ROIC or provide shareholders with improved income which will create value one way or another.

Risks

Economic Conditions: Recessions and downturns in the economy can result in lower consumer spending on discretionary goods, which can impact the market for clothing and fashion items.

Supply Chain Disruptions: Oxford Industries is dependent upon an intricate worldwide supply network. Natural catastrophes, geopolitical upheavals, and other events can cause disruptions that affect raw material prices and availability, manufacturing, and distribution.

Conclusion

To summarize, I believe that Oxford Industries is currently a strong buy due to its solid dividend, excellent ROIC, stable balance sheet, resilient earnings, innovative brands, and undervaluation assuming my DCF figures. I believe that monitoring inflation would be important as several more unexpected rate hikes would alter my thesis due to consumer sentiment being further damaged.

For further details see:

Oxford Industries: Undervalued Company With Solid Brand