OXSQ - Oxford Lane Capital: 19% Yield With Only Implied Risk

2024-01-05 14:42:48 ET

Summary

- Oxford Lane Capital carries a pure-play exposure to CLO debt and equity products.

- Since the exposure to CLO equity tranche dominates, there are huge risks embedded in OXLC that render this BDC very speculative per definition.

- If we look deeper into OXLC, we notice several levers that quite clearly de-risk the overall investment case, thereby making the 19% dividend more sustainable than would be implied.

- In this article, I elaborate on the main drivers behind this thesis and provide my opinion on the overall investment case.

Very recently I issued an article on Oxford Square Capital Corp. ( OXSQ ) - Oxford Square Capital: Staying Away From This 14.5% Yielding BDC - highlighting several elements, which render this BDC a subpar investment. Namely, the combination of clear signs of deteriorating portfolio quality and the exposure to second-lien and CLO equity introduced too much of risk relative to the return potential (including the dividend).

Now I am trying to explore a closely related BDC - Oxford Lane Capital Corporation ( OXLC ) - which carries rather similar investment allocation characteristics to OXSQ.

Just like OXSQ, OXLC allocates heavily into CLO structured finance investments, which come with totally different risk and return patterns compared to those, which we can see in the overall BDC space.

Yet, the key difference here is that OXLC has pure-play exposure to CLO debt and equity products, while for OXSQ this category accounts "only" for ~30% of the total portfolio.

What this means is that OXLC has a higher risk profile and that at least theoretically the returns prospects are way more unpredictable relative to those of OXSQ (which already are skewed to the more aggressive end of the risk spectrum).

A confirmation of this observation is the current yield of OXLS, which is ~500 basis points above what OXSQ can offer and in absolute terms implies a truly elevated risk exposure (i.e., yield of ~19%).

With that being said, let's explore whether a 19% yield (from which the lion's share of OXLS returns comes from) is sufficient in the context of the underlying risk.

Thesis

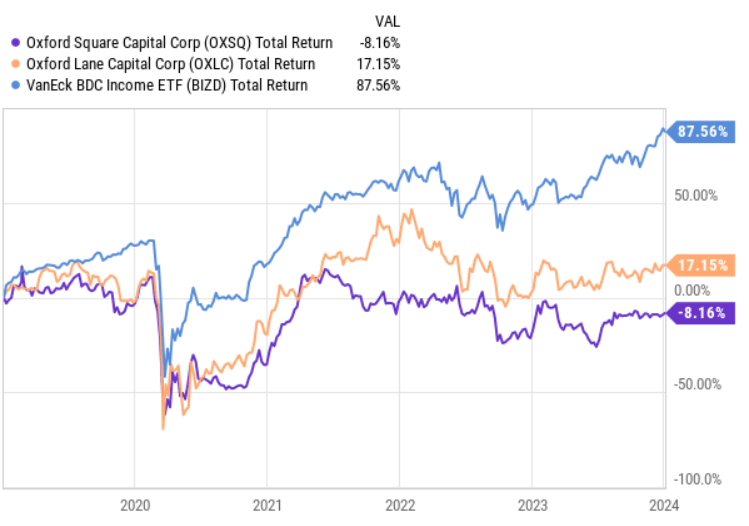

If we look at the historical 5-year total return chart of OXSQ, OXLC and the broader BDC market, we notice some interesting dynamics.

{kind=link}

Just like OXSQ, OXLC has underperformed the BDC market in a quite notable fashion. At the same time, OXLC has delivered more attractive returns compared to OXSQ despite carrying higher risk in its structure. In fact, if we zoomed the picture back and looked at the historical 10-year total return data, we would notice a rather similar pattern, where OXLC performs consistently above OXSQ.

From the historical return perspective, we do not see signs or appealing evidence which would indicate an ability to generate alpha over the BDC market.

Nevertheless, as we know, past performance is not indicative of future results. Plus, the current dividend yield of 19% still provides an interesting option for yield-seeking investors to consider in their portfolios.

{kind=link}

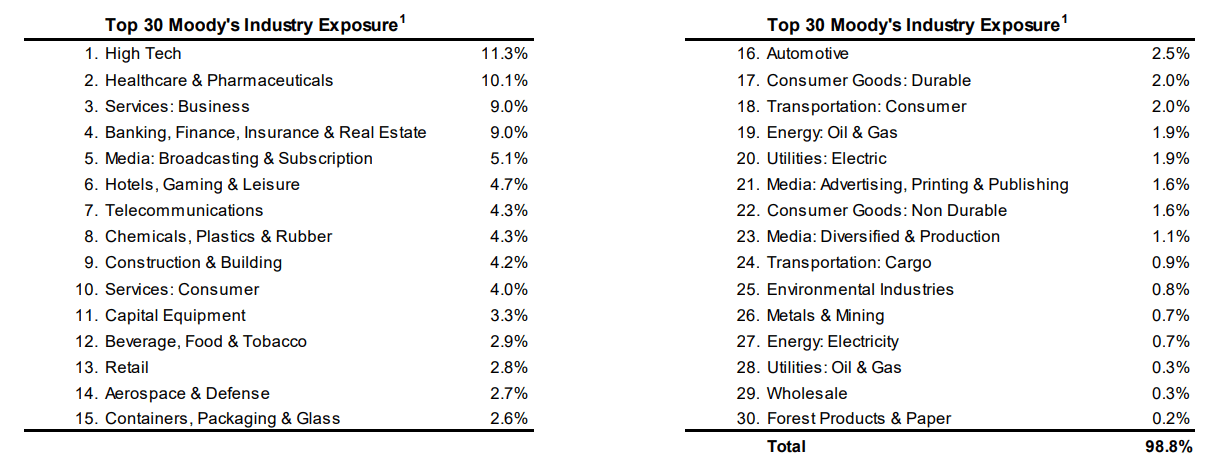

As mentioned a bit earlier, OXLC invests only in CLO structures, which is visible in the table above. Yet, I have to underscore the fact that ~95% of the total AUM amount is channeled towards CLO equity, which is even riskier than the CLO debt category.

Although CLO equity is ultimately composed of debt-like instruments (e.g., bonds, loans), the fact that CLOs come with their own tranches starting from rated debt and ending with unrated equity introduces complexity. Here, obviously, as the name implies, CLO equity is located well at the bottom of the total CLO structure, which acts as a first line of defense.

To put it simply, if underlying loans or bonds start to default, CLO equity holders (e.g., OXLC) are the ones, which absorb the first losses.

However, from a portfolio perspective or how it is constructed beyond the CLO equity vs. debt level, things look rather solid.

{kind=link}

OXLC is well-diversified across many industries, thereby neutralizing single-industry concentration risk. This is critical to avoid assuming additional risk in the portfolio.

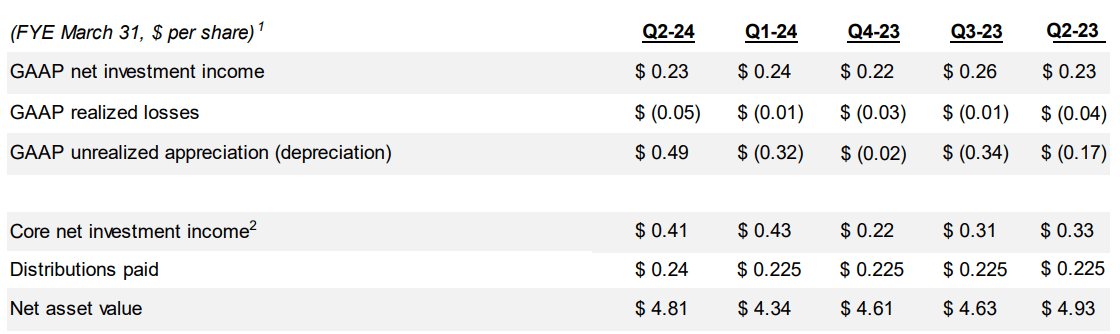

Then, if we look at the recent results and how the underlying numbers come together in the context of cash generation versus OXLC's ability to service the attractive dividend payments, the story is actually not that bad.

{kind=link}

Here are two critical takeaways to note:

- The net investment income component, which is the most critical one as it reflects the cash income generated by the fund and avoids factoring in net unrealized gains and losses (i.e., swing in the asset prices), has been stable in the past five quarters.

- The net investment income component itself has been sufficient to cover the dividend payments without tapping into the NAV base (with very immaterial exceptions).

Having said that, the issue in the dividend coverage context is that there is a very thin margin of safety when it comes to fully covering the current yield as the dividend coverage ratio is already at ~100%. This, in turn, means that in case of several major asset write-downs and/or underlying loan defaults, OXLC would be forced to immediately revise the dividend to make the fund sustainable.

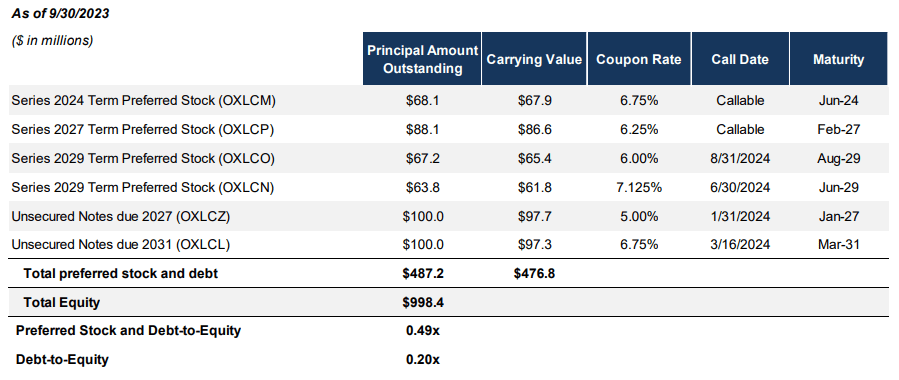

Finally, it is worth paying attention to OXLC's debt structure.

{kind=link}

There are also two elements I would like to underscore.

First, is OXLC's debt-to-equity level of 0.2x, which is considerably below the sector average of 116% . Having this tiny load of external leverage helps decrease the risk of being subject to magnified losses in case of investment write-downs. Plus, it does not really make sense from the yield perspective either as the current weighted average cash yield of OXLC is already high enough (~24%) to satisfy most investor expectations.

Second, while the external leverage is minimal indeed, it is still structured in a very favorable fashion, where low fixed rate loans carry distant maturity profiles allowing OXLC to avoid expensive repricing of the debt.

The bottom line

OXLC is inherently a speculative vehicle due to its pure-play skew towards CLO-type structures, where the underlying risk profile is made worse given that ~95% of total AUM lies in the most risky lever of CLO products (i.e., CLO equity). Plus, the fact that OXLC has fully exhausted the net investment income component in terms of the dividend coverage leaving no space for any error in the portfolio, brings additional risk to the equation.

Yet, the remaining aspects of OXLC are actually quite solid - i.e., great diversification across various industries, low debt, locked-in borrowings at attractive interest rates and distant maturities, and the stability of net investment income. So even if OXLC was forced to decrease the dividend, it still would not be a major cut considering these layers of protection.

In my view, OXLC is an interesting investment to consider for yield-chasing investors, who are not afraid of notable volatility. However, it should not consume too large a chunk of the portfolio since the CLO equity exposure per definition opens up a greater risk of a permanent impairment of capital.

For further details see:

Oxford Lane Capital: 19% Yield With Only Implied Risk