OXSQ - Oxford Square Capital: Not A Place To Generate High Quality Income

2023-10-16 17:09:37 ET

Summary

- Oxford Square Capital Corp.'s main business is investing in collateralized loan obligations, but I believe its business model is unlikely to result in strong returns for investors.

- Collateralized debt may not be fully secured as corporate assets can lose significant value if a company defaults on its debt or goes bankrupt.

- The company's stock performance has been poor, with a decline of close to -70% in the last 10 years, matching decline in its book value.

- Its dividends have been slashed by more than two thirds in the last decade and this was during a strong bull market.

Oxford Square Capital Corp. ( OXSQ ) is a business development company that invests into a variety of debt instruments including secured and unsecured senior debt, subordinated debt, junior subordinated debt, preferred stock and syndicated bank loans for companies in the technology sector; but the company's main business is CLOs (collateralized loan obligations). The company's history shows what I believe is a broken business model which is unlikely to result in strong returns for investors in the long run.

At first, one might hear the words "collateralized loan obligations" and think this is a great idea and safe investment because it implies that the debt is fully secured by assets similar to how a mortgage would be secured by a house which means if the debtor isn't able to service their debt, the issuer of the debt could take that asset and cover their losses - but it's not that simple when it comes to corporations. When taking on collateralized debt, a company's assets could be worth a certain amount but if the company defaults on its debt and goes bankrupt, those assets will be worth only a fraction of that amount. For example, if a company has a factory producing goods which is assessed to be worth $50 million and this company were to go bankrupt and the factory was put on liquidation sale, it could only get about $15-20 million because it's not operational anymore. Unlike mortgaged houses which tend to protect most of their value in default (with the exception of 2009) corporate assets can lose so much value if the company holding them defaults on their debt or goes bankrupt. So a collateralized debt might not be fully collateralized after all because those assets backing them might not be worth that much if the company is unable to service that debt.

The company appears to be fully aware of this and tries to minimize the effects of this by establishing itself as either first or second priority position in those companies' debt structure. What this means is, when a company goes bankrupt, the bankruptcy court will look at all kinds of different debts owed by the company and put them in a priority order in which they must be paid by liquidating the company's assets. This means that debt owners who are not on top of this list might get very little or no compensation for the debt they are holding because assets are distributed based on priority. By contractually establishing itself as one of the top priority creditors, Oxford Square Capital makes sure that it will get paid before others are getting paid but this doesn't always guarantee that the company will get 100% of its money back since a troubled company's assets might cover only a fraction of their debt obligations. What makes the matters worse is if the debtor company is highly leveraged, which a lot of them are since they are unable to get good loan deals from established banks and they are willing to pay a premium interest for services of a BDC company. Typically, companies that borrow from BDCs tend to have either bad credit rating or no credit rating at all and have trouble accessing liquidity otherwise. Many of them could also be start-up companies that have yet to make a profit.

Historically speaking, this stock hasn't delivered the goods for investors even though it has a generous dividend yield of 13%. In the last 10 years the company's stock has been down close to -70% and its total return was only 31.6% which comes down to less than 3% annualized which is a fraction of the company's dividend yield. If a company offers 13% dividend yield but its annual total return is less than 3%, something is going terribly wrong. Also this performance came during one of the strongest bull markets in history where the Fed was extremely accommodative for the most part and access to liquidity was better than any time in history. If the company performs this poorly when everything was going great, how will it perform when things actually get tough?

Just to give you a hint, the stock dropped 65% in a matter of 3 weeks during the COVID crash of 2020 which I think can give you a preview of how this stock might perform when things get tough.

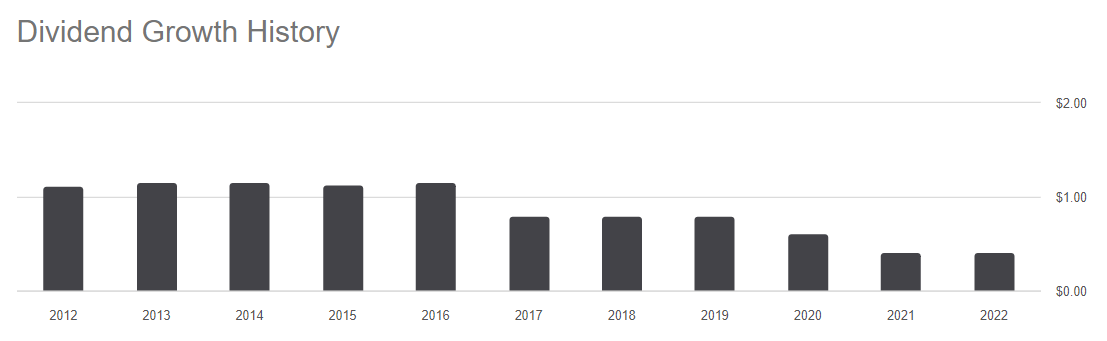

One thing I hate to see in a high-yielding stock is declining dividends over time. At the end of the day, people buy high-yielding stocks not for capital appreciation but for income potential. Preferably, you want your dividends to grow, or at least stay stable, year after year so that you can make a budget and live comfortably without worrying too much about your income declining. Well, if you bought this stock 10 years ago, you would have enjoyed a dividend of $1.12 per share in your first year but it would gradually decline to its current dividend of $0.42 per share. This is not good. Your income shouldn't drop by two thirds in 10 years (more like three fourths after accounting for inflation). This is why it's important for investors to look at a company's dividend distribution history before being lured in by high yields.

{kind=link}

In the last 10 years, the company's book value declined by close to 70%. Meanwhile, it currently trades at an 8% premium against its book value. Just a few years ago it was trading for only 0.6 of its book value where it enjoyed a deep discount of 40% against its book value but it is pretty much gone now.

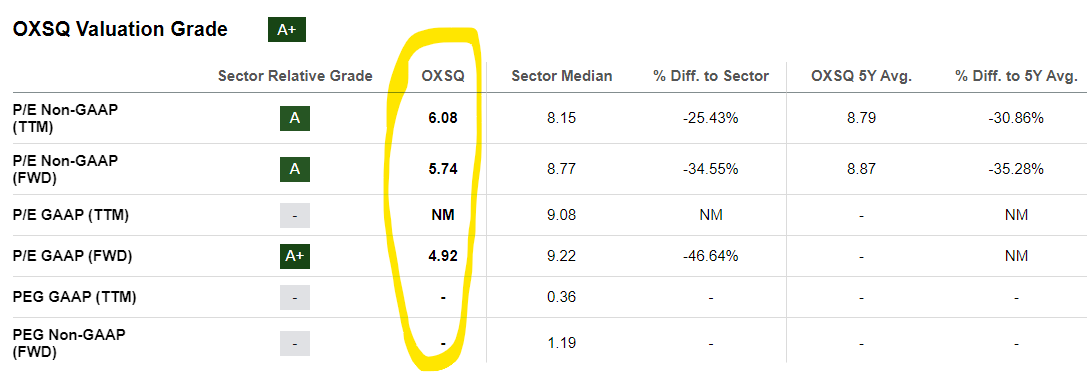

When you look at the company's valuation from a traditional standpoint, it looks fairly cheap at a trailing P/E of 6 and forward P/E of 5.7 (based on non-GAAP earnings) as compared to the sector median of 8, but it is probably cheap for a good reason considering all the risks associated with it.

{kind=link}

Another issue with this company is its high reliance on leverage in order to sustain that high dividend yield. Investing into risky companies is one thing but doing it with leverage is even worse. The Fed has been tightening money supplies for the last year and half and these things tend to have a lagging effect. We've yet to feel the full effects of the Fed's tightening activities in my opinion, and if liquidity levels in the economy start shrinking, this will affect companies like OXSQ quite severely because a lot of its customers likely won't be able to roll their debt and may even risk defaulting on their existing debt. A few isolated incidents might be ok but if a chain reaction were to occur, I believe in a worst case scenario it could put this company's entire existence in jeopardy. Lately it is automatically assumed that the Fed will always come to the rescue of the market and save all troubled companies by printing unlimited amounts of money every single time but this is a very dangerous assumption that can cost you in my view.

Retirees and income-oriented investors should be very careful about where they put their money and where their income comes from. Safety and sustainability should come before everything even if it means a lower yield. There are better places where you can generate healthy levels of income without taking this much risk.

For further details see:

Oxford Square Capital: Not A Place To Generate High Quality Income