OXSQ - Oxford Square Capital: Staying Away From This 14.5% Yielding BDC

2024-01-04 10:27:17 ET

Summary

- Oxford Square Capital Corp. is a small BDC with a market cap of just over $150 million.

- The company's asset allocation strategy heavily emphasizes collateralized loan obligation (CLO) structured finance investments, which introduce different risk factors.

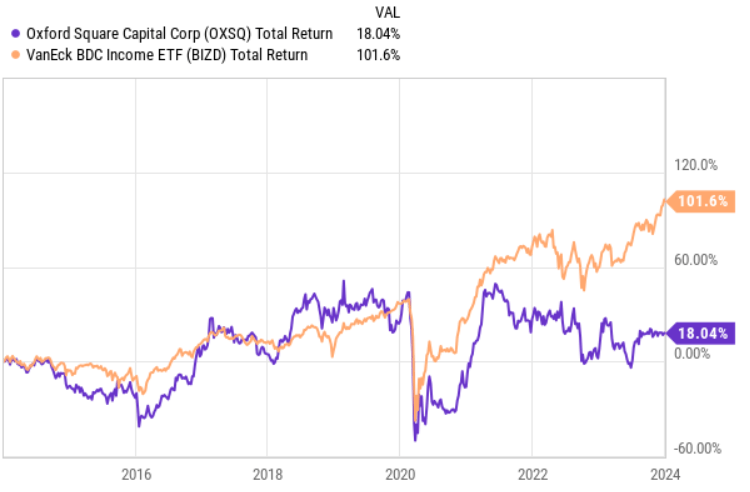

- The company's historical performance has diverged from the overall BDC market, and its share price has been negatively impacted (on a relative basis) by higher interest rates.

- In this article, I elaborate on the key elements within OXSQ's portfolio that substantiate the thesis of avoiding this BDC.

Oxford Square Capital Corp. ( OXSQ ) is a small size BDC with a current market of cap of just above $150 million.

From the underlying structure perspective and how the focus is put on distributing dividends from debt-like investments, OXSQ is quite similar to any standard BDC out there.

However, there are notable points of difference when it comes to the asset allocation strategy and overarching investment criteria. Namely, OXSQ puts a heavy emphasis on collateralized loan obligation (“CLO”) structured finance investments, which introduce totally different risk and return factors than we are used to in the BDC universe. To make things more complex, these CLOs themselves in OXSQ are not that conventional since according to the Fund's policy, CLO investments may also include warehouse facilities (financing structures, which aggregate loans that may be used to form the basis of a CLO body).

Having said that, the element of CLOs does not necessarily render the investment case unattractive.

{kind=link}

Yet, if we look back at the historical performance and compare OXSQ with the overall BDC market, we can clearly notice how consistent the divergence has been since early 2020 (i.e., outbreak of a wider Covid-19 pandemic). Even more, it is quite evident how the higher interest rate regime has actually introduced downward pressure on OXSQ's share price - a complete opposite to the rest of BDC players, which currently thrive from a higher SOFR and the ability to capture higher yields.

With this relatively negative backdrop in mind, let's explore in a bit more detail whether OXSQ might be an interesting investment pick going forward, when the consensus signals of gradually falling interest rates and the recessionary risks seem to be on the rise.

Thesis

In terms of the overall portfolio structure, OXSQ rather diversified across three investments types: first lien, second lien and CLO equity with each of these positions assuming more or less equal chunks of the total AuM figure.

OXSQ Investor Presentation

However, a major issue or an area of concern in this context is that the exposure to first liens is only ~30% with the remaining portfolio placed in inherently riskier and unpredictable assets (i.e., second lien and CLO equity).

Typically, you would see first lien accounting for 70-85% of the BDC portfolio and then the rest spread across other types of assets such as second lien, preferred shares, asset finance or equity.

OXSQ Investor Presentation

The underlying asset or investment quality serves as a testament of the aggressively structured portfolio. In other words, the pie chart above classifies the portions of investments, which are currently performing fine (as expected) and which are either on the brink of default or close to that.

Again, for context, most BDCs in this environment have a maximum of 3% of their assets registered as non-performing and then really depending on the case but on average ~5-15% that are placed on a watchlist.

In OXSQ's case, however, we see that ~10% of the portfolio is already labeled as non-performing (i.e., grade 5, which per OXSQ's definition implied the following: Full repayment of the outstanding amount of OXSQ’s cost basis is not expected for the specific tranche and the investment is placed on non-accrual status ).

Then there is a huge component that is attributable to grade 3, which means that OXSQ has to monitor these investments more carefully as there are already some early signs of potential struggles to service the payments.

Now, if we look at how all of this has translated to the financial performance, we can notice only logical consequences.

{kind=link}

The most important takeaways from this are the following:

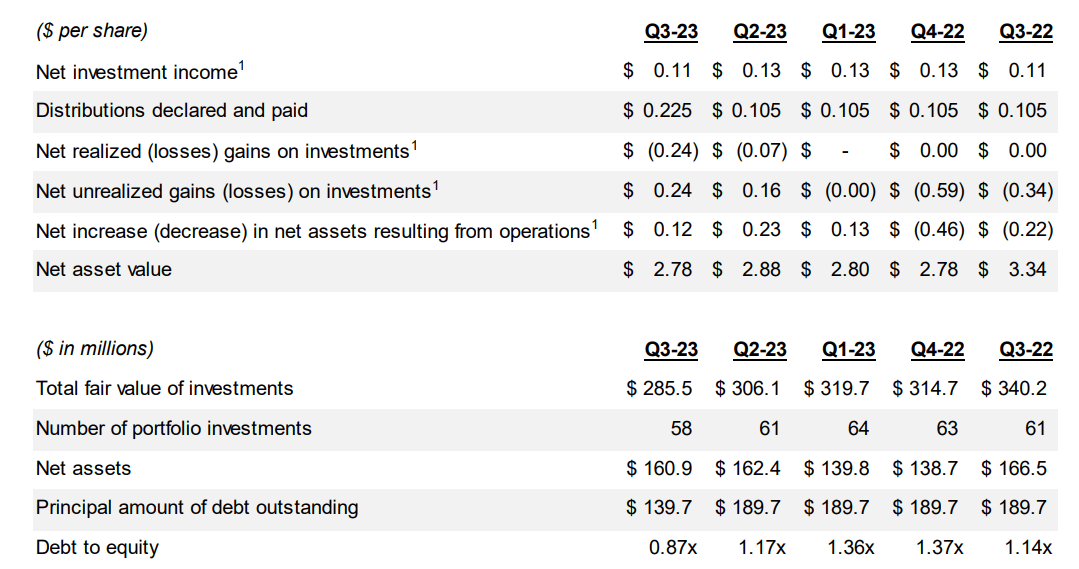

- Core net investment income just barely covers the dividend payments.

- Net unrealized gains and losses tend to swing considerably, going from negative $0.59 per share in Q4'22 to positive $0.24 per share in Q3'23.

- Net asset value has been on a constant decline since Q3'23, which to a large extent could also be explained by the de-leveraging of OXSQ's balance sheet.

So, the essence is that there is too small margin of safety for covering the underlying dividend in a sustainable manner given the volatility in the net unrealized gains and losses element and the lower quality of OXSQ's investments.

Granted, we have to appreciate the fact that OXSQ has considerably deleveraged its balance sheet, reaching a debt to equity level that is way below its historical average and the average of BDC players (~117%).

Yet, there are again two issues in this context:

- The process of de-leveraging has been carried out partially at the expense of net asset value, which makes this story inherently less attractive and successful.

- The leverage itself embodies quite unfavorable refinancing dynamics, as already next year the fund will be forced to refinance portions of its fixed rate debt, which will be repriced to much higher interest rates taking into account the current SOFR and credit risk premiums levels for OXSQ.

The bottom line

Considering the combination of elevated risk profile, which is associated with OXSQ's investments and a very thin margin of safety for current dividend coverage, OXSQ seems an overly speculative bet for me.

At the same time, I would not short this fund since as a BDC it still enjoys some of the sector-level tailwinds, which provide a structural support to OXSQ's share price.

All in all, while the current dividend yield of 14.5% is indeed attractive and ~200-300 basis points above what we could access in the overall BDC sector (on average), it does not justify the additional risk exposures that are embedded in OXSQ's portfolio.

For further details see:

Oxford Square Capital: Staying Away From This 14.5% Yielding BDC