PX - P10: I Expect Shares To Double Over The Next 3 Years

2024-01-07 10:22:58 ET

Summary

- P10 shares have underperformed the market due to a slowdown in organic growth, decline in EBITDA margins, and lack of acquisitions.

- P10's stability of revenue and free cash flow, niche focus on small and mid-market private equity, and an improved outlook for private equity fundraising make the company an attractive business.

- P10 shares trade at less than 11x my estimate of current free cash flow and I believe shares can double looking out three years.

P10 ( PX ) shares have meaningfully underperformed the broader market over the past year, falling 18% while the Russell 2000 small cap index ( IWM ) has increased 11%. Weakness in the stock is attributable to:

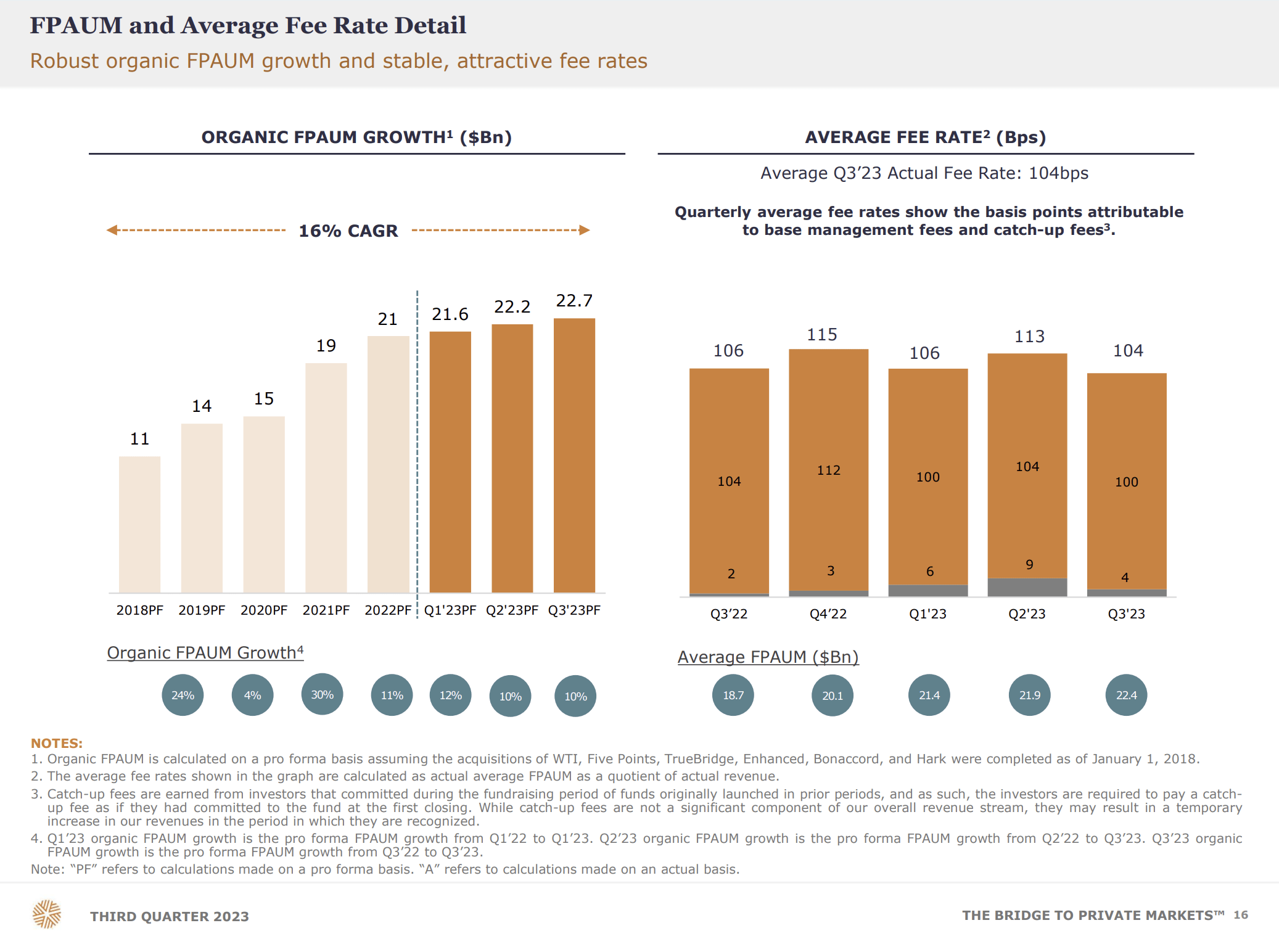

- Slowdown in organic growth in assets under management (sub 10% in 2023 versus 16% CAGR since 2018 as shown below) as investor appetite for new private equity offerings in 2023 was below what we've seen over the past 5 years. Some of this is due to the denominator effect - throughout much of 2023 the value of public equity and fixed income securities was below 2021 levels while reported values of private assets were relatively steady. As such, the percentage allocation of private assets as a percentage of total invested assets for many investors was at or above their target range. Given the strong rally in public debt and equity markets over the past two months, allocation to private assets has mechanically shrunk suggesting a potentially more favorable outlook for new fund raising.

Organic growth in AUM (P10 Investor presentation)

{kind=link}

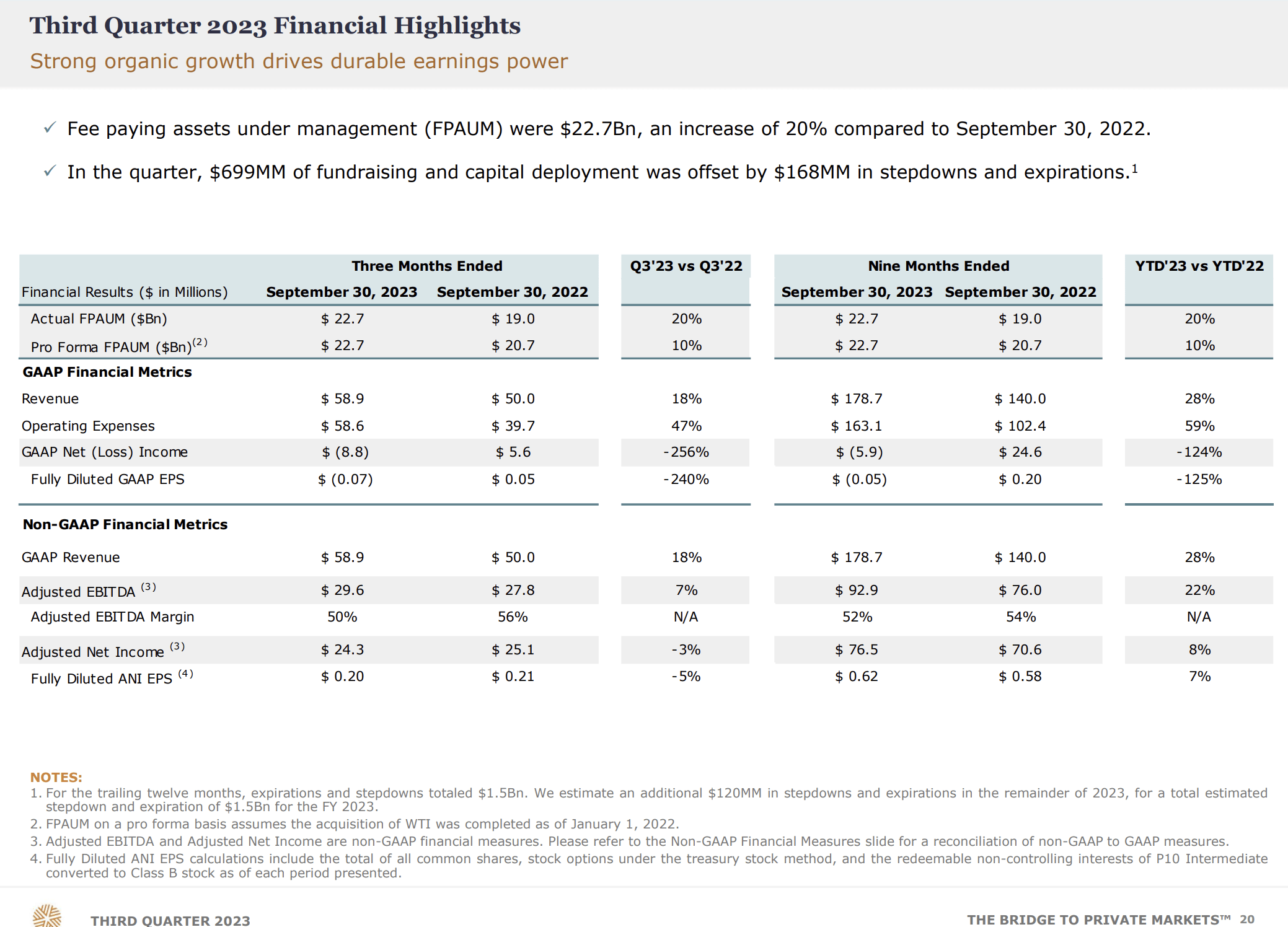

- As shown below, P10 has experienced a slight year-over-year decline in EBITDA margins. While assets under management/revenue have continued to grow, albeit at a slower pace than in years past, expenses have increased faster which has pressured margins. Given the company's rapid growth over the years, management had reinvested into the business to expand infrastructure, product breadth, and distribution capabilities. It is also worth noting that some of this is due to P10 founders stepping back from day-to-day management and bringing in a new CEO (increased compensation expense).

Current Results (3Q23 Investor Presentation)

{kind=link}

- Lack of acquisitions - P10 made several acquisitions from 2017-2022 but has not made a deal since the third quarter of 2022. With acquisition driven growth having been a key tenet of the P10 investment case, the lack of new deals has disappointed investors. The underperformance in P10's shares has made it more difficult to do accretive acquisitions, as P10 has historically used its shares as an acquisition currency. With shares trading at such a low valuation (less than 11x 2024e FCF per share), structuring a deal using equity has become more challenging. That said, I believe it is wise for management to maintain price discipline in pursuing deals. Further, given its strong balance sheet and ample free cash flow, P10 still has plenty of capacity to make acquisitions without issuing shares.

Despite these headwinds, I see P10 as being a very attractive investment at current prices given:

- Stability of revenue and free cash flow - Unlike large private equity firms Apollo ( APO ), Blackstone ( BX ), and KKR ( KKR ), P10 does not share in incentive fees (known as 'carry' - at P10 all 'carry' is paid to division management/investment teams) - it's revenue is comprised solely of management fees. Management fees are very stable and predictable given that fees are paid as a percentage of invested assets (not subject to mark to market) on assets which are locked up for nearly a decade. For the large private equity firms, public markets have placed much higher multiples on management fees (17-25x pre-tax fee related earnings) than earnings from carry which tends to be quite lumpy (very low in 2023 given dearth of IPO activity).

- Niche focus on small and mid-market private equity should allow P10 to continue to generate meaningful excess returns for investors across the cycle. Moreover, smaller deals tend to use lower levels of financial leverage (less reliance on low interest rates/appetite of junk bond investors). P10 and the managers on its fund-of-funds platform are able to invest in smaller deals which while attractive are in many cases too small to move the needle for the private equity behemoths.

For further details see:

P10: I Expect Shares To Double Over The Next 3 Years