PIII - P3 Health Partners: Just Another SPAC-Listed 'Value-Based Care' Company?

2023-06-09 14:36:41 ET

Summary

- P3 Health Partners went public in December 2021 via a SPAC merger.

- The company is a "value-based care specialist", focused on providing holistic, localised care, for Medicare Advantage patients.

- Shares sank in value after listing, reaching a low of $4.

- Value-Based Care is a crowded space and not every company can succeed - but CVS recent acquisition of Oak Street shows that those that do succeed can richly reward shareholders.

- P3 has promised to be EBITDA-positive in 2024 and will turnover >$1.2bn in FY23 if guidance is met. Losses are narrowing, but cash is scarce. I'm maintaining a watching brief for now.

Investment Overview - Why Value Based Care, & Why P3 Health Partners

The emergence of a new type of approach to healthcare, known as "Value Based Care" as a long-term replacement for the traditional "Fee For Service" approach has led to a spate of recently listed companies attempting to cash in on the trend.

What is value based care, and how does it compare to fee for service? In a fee for service model, doctors, hospitals and medical practices charge for each service they perform, and a patient's healthcare insurer is then responsible for settling those bills.

Conversely, in a value based care model, reimbursement is based on quality of care provided, as well as patient outcome. According to MHA online , "in 2015, the US Department of Health and Human Services set a goal of having 50 percent of Medicare reimbursements tied to value-based care by 2018".

Whilst it's "unclear" if that goal is anywhere close to being met, one of the areas where value based care has had the most impact to date is within the Medicare Advantage model. According to the Centers for Medicare and Medicaid Services ("CMS"):

Medicare Advantage (also known as "Part C") is a type of Medicare health plan offered by a private company that contracts with Medicare. These plans include Part A, Part B, and usually Part D. Plans may offer some extra benefits that Original Medicare doesn't cover.

Medicare Advantage is big business for health insurers, who generally view it as their fastest growing and most lucrative business model. According to the private healthcare insurer funded Better Medicare Alliance:

The Better Medicare Alliance :

Medicare Advantage is built on a value-based system in which Medicare Advantage health plans receive a per-member, per-month payment for each beneficiary's care, and are tasked with using those dollars most effectively - incentivizing high quality, high-value care for the 24.2 million enrollees who trust Medicare Advantage with their health care needs.

In other words, the CMS pays private health care insurers a flat fee for administering the health care plan, and if the overall costs funded by the health insurer are lower than the flat fee, the health insurer pockets a percentage of that difference.

Medicare Advantage ("MA") is available for seniors over 65-years of age - a massive growth market given 10k "baby boomers" turn 65 every day in the US. MA offers additional benefits that traditional Medicare plans do not, such as vision, hearing and dental services.

In order for the Medicare Advantage/Value Based Care model to work, however, clearly, private healthcare insurers need to keep costs down, while ensuring the care administered to patients remains high - the CMS has a Star Rating system in place that rewards 5-star plans with additional bonuses.

This is where a company like P3 Health Partners (PIII) comes in. Private healthcare insurers essentially want to keep their members out of hospitals and away from doctors, because these are the most substantial costs they can incur. A Physicians' salary in the US is ~$200k per annum, therefore their time is expensive, especially compared to e.g. a nursing assistant, on ~$35k per annum. Likewise, hospital visits are expensive, and so is using hospital equipment, and staying overnight.

This may not sound great for the patient - but the idea is that by providing better care for patients at the outset, companies like P3 - who contract directly with private health insurers - can ensure that patients' health problems can be treated earlier, negating the need for expensive treatment further down the line. Most MA plan providers specify that patients can only use doctors and other providers who are in the plan's network and service area as an additional cost cutting measure. Theoretically at least, it is a virtuous circle.

The Rise Of Value Based Care Company Listings

Plenty of companies have recently opted to become public and build out their Value Based care networks, sensing a gap in the market to offer the type of holistic, localised care that private healthcare insurers believe can keep patients' healthy, and ultimately reduce the costs of administering their plans.

The most significant of these companies may be Oak Street Health, which has been acquired by CVS Health ( CVS ) in an all-cash deal for $39 per share, representing an enterprise value of $10.6bn. The deal completed last month. CVS commented:

The acquisition will broaden CVS Health's value-based primary care platform and significantly benefit patients' long-term health by improving outcomes and reducing costs - particularly for those in underserved communities.

I have listed a number of other listed Value Based Care companies in the table below, in order of market cap.

Listed companies focused on Value Based Care (Google Finance, TradingView )

{kind=link}

Whilst GE Healthcare is somewhat anomalous, being a provider of medical devices and an established healthcare giant already (although its pivot into VBC does speak to the attractiveness of the market), the other companies are primarily focused on this sector, and range in size from $8.3bn market cap agilon health ( AGL ), to troubled Nutex Health ( NUTX ).

As we can see, five companies have been listed for less than three years, and overall, share price performance has been decidedly mixed. Six of the nine companies are earning revenues >$1bn, or very close to $1bn - price to sales ratios across the board are very low - although profit margins are low to non-existent - perhaps not too surprising given the industry is relatively new, and companies are speculating to accumulate.

P3 Health Partners - Company Overview

What, if anything, makes P3 Health stand out in its field? In its Q321 10Q, the company discusses its business as follows:

We operate in the $829 billion Medicare market, which covers approximately 65 million eligible lives as of 2021. Our core focus is the MA market, which makes up approximately 48% of the overall Medicare market, or nearly 28 million Medicare eligible lives in 2022.

We predominantly enter into capitated contracts with the nation's largest health plans to provide holistic, comprehensive healthcare to MA members. Under the typical capitation arrangement, we are entitled to per member per month ("PMPM") fees from payors to provide a defined range of healthcare services for MA health plan members attributed to our primary care physicians ("PCPs"). These PMPM fees comprise our capitated revenue and are determined as a percent of the premium ("POP") payors receive from CMS for these members.

Under this capitated contract structure, we are generally responsible for all members' medical costs across the care continuum, including, but not limited to emergency room and hospital visits, post-acute care admissions, prescription drugs, specialist physician spend and primary care spend. Keeping members healthy is our primary objective. When they need medical care, delivery of the right care in the right setting can greatly impact outcomes.

Since being founded in 2017, P3 has expanded its network of 2,800 PCP's into 15 markets, across five states, and serving 103,400 MA members - up from ~60,000 members at the end of 2021. In a corporate presentation, P3 notes that its 75% CAGR growth in PCPs since 2018 significantly outpaces rival agilon's 19% CAGR over the same period, to 1,600 PCPs, despite agilon's enjoying a market cap valuation of >$8bn, compared to P3's $1.5bn at the time of writing.

P3 achieved its Nasdaq listing thanks to a merger/business combination with Foresight Acquisition Corp, a Special Purpose Acquisition Company ("SPAC"). Wikipedia defines a SPAC as follows:

A special purpose acquisition company, also known as a "blank check company", is a shell corporation listed on a stock exchange with the purpose of acquiring a private company, thus making it public without going through the traditional initial public offering process and the associated regulations thereof

SPAC's list with a share price of $10 and have two years to find and merge with a target company, or money is returned to investors. Typically, in recent years, companies that have listed via a SPAC have seen their valuations decline, often drastically - much like the value based care industry, it is still early days for the SPAC model, but for anyone considering investing in P3, this can be considered a potential red flag.

Recent Performance

In Q123, P3 outperformed analyst's expectations on both EPS of $(0.22) per share, and revenues of $302m. Overall net loss was $52.4m, versus a $(60.8m) loss in the prior year, and net loss per member per month $($169). Company CEO Sherif Abdou noted that:

We are off to a strong start in 2023. We achieved a medical margin of $39.2 million or 13.1% as a percentage of capitated revenue for the quarter, a key metric for validating the effectiveness of P3's model. As a result of the first quarter strength, we are increasing our Adjusted EBITDA guidance today.

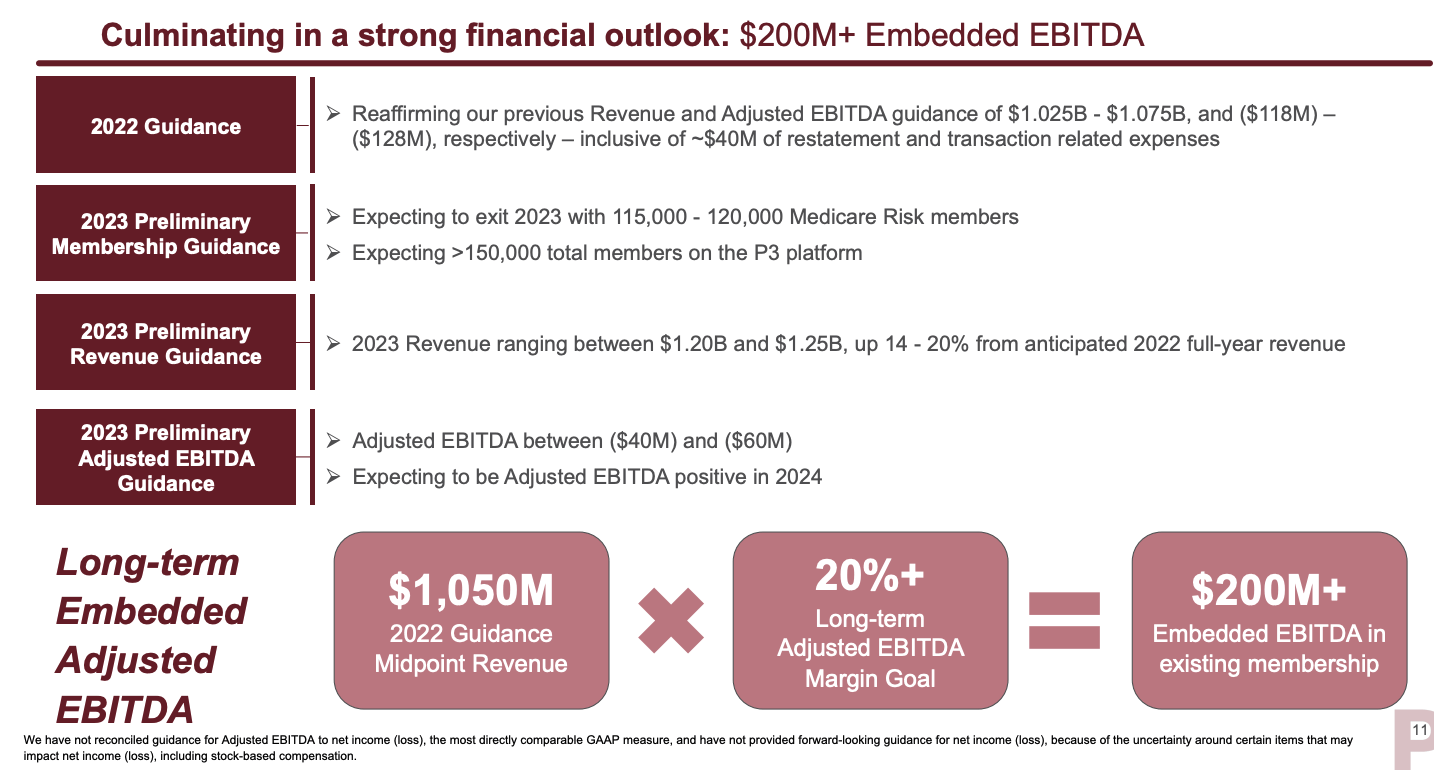

FY23 guidance is shown below as per a slide from a company presentation :

P3 Health FY23 guidance (company presentation)

{kind=link}

For a company like P3, to be generating >$1bn in revenues is an encouraging sign, and the 14-20% uplift now expected in 2023, to $1.2 - $1.25bn, is also a strong positive, as is the narrowing EBITDA losses, now expected to be $(40m)-$(60m). Management has promised that the company will be EBITDA positive by 2024, which is important, in my view, as one accusation that can be levelled at Value Based Care companies is a lack of profitability to prove the business model is working. Oak Street, for example, made a net loss of >$(500m) in 2022, and a net loss of >$(400m) in 2021, before its acquisition by CVS.

Although some metrics around the value based care industry are somewhat confusing, management was keen to provide plenty of evidence that it is delivering on its promises to shareholders and investors during its Q123 earnings call . In its various regions, new market Oregon is said to be "moving towards profitability", California delivered "positive adjusted EBITDA", and in Arizona, "performance is strong", suggested CEO Abdou. Summing up overall progress and measurement against deliverables, Abdou summed up as follows:

I just wanted to remind you all that our key promises to our shareholders and investors that we will work hard on improving the funding and we have improved that from $899 PMPM last year first quarter to $963 per member per month first quarter 2023. That's about 9.3% improvement. We have promised and committed to improve our medical margin.

First quarter 2022 was $82 PMPM. And as we promised we increased the medical margin to $127 per member per month. That is constituted about 13.1% margin from our revenue. And medical cost ratio had improved from 91% 92% first quarter 2022 to 87% first quarter of 2023. We promised we said it we did it.

And network contribution was $7.7 million first quarter last year or $26 PMPM or 2.8%. This year first quarter, as we promised, it's more than doubled $17 million network contribution positive $53 per member per month, that's 5.5% of the revenue.

It should be noted that P3 is still making a net loss per member per month, of >$100, although it is narrowing, and "patient persistence", which I assume means how long the same patients have been cared for, is growing, which is another important factor in P3's progress, assuming it implies contracts with insurers are being renewed, and patients are happy.

Concluding Thoughts - An Intriguing Space, A Growing Company With Narrowing Losses, Undervalued vs Some Key Peers - Keep It On Your Watchlist

P3 is not a cash rich company, with total current assets of $109m reported as of Q123, enough to last just two more quarters based on net loss for last quarter of $52m, which means management has very little leeway and needs to keep delivering progress.

The recent progress has resulted in P3's share price posting some spectacular recent gains, however - the stock price is +126% so far this year, although trading at $4.30 at the time of writing, it remains down >50% since listing.

P3 - as management is keen to point out - also stacks up well against some rivals, although it lacks the financial funding of some, and it should also be noted that key rival Cano Health apparently generates twice the revenues of P3, and has half the market cap valuation - although its debt to equity ratio suggests Cano may have some crippling debt to contend with.

Personally, I have not quite made up my mind about value based care. The grand plan to transition from Fee For Service to VBC has not quite materialised, amid accusations that health insurers may be trying to "game the system", implying patients are more unwell than in reality, to secure more funding, and making difficult for patients to access care outside of a specific network.

Another issue with a company like P3 is that it expects to take a further chunk out of a health insurers profit margin, without necessarily being able to guarantee it can reduce a health insurer's cost burden, and its business model may be relatively easy for a large private health insurer to copy and establish in-house - although clearly, CVS did not seem to think so, opting to pay >2x the traded share price of the very unprofitable Oak Street rather than set up a similar business itself.

I recently covered The Pennant Group (PNTG) for Seeking Alpha, a company which I felt was a good buy opportunity with a market cap >4x lower than P3's, and I remain concerned by the dismal general performance of companies that list via SPAC's - the "light touch" route to market potentially hiding a multitude of sins.

Nevertheless, the recent rise in P3's share price can be considered very encouraging in my view, after a pretty poor start to life as a traded entity. I will assign P3 a "Hold" recommendation for now, as after such a strong bull run the share price could dip on profit taking.

I plan to study Q2 and Q3 results closely, however, and if I could buy shares at <$4.5 ahead of FY23 earnings, and still expect management to hit their guidance, I'd be tempted to buy the stock, as the VBC model has been to some extent validated by the Oak Street buyout, and although I'd expect some consolidation within the industry, and some companies to fail, P3 appears to be building a business that is improving every quarter and it is not too hard for an outsider to assess progress within this immensely lucrative and exceptionally fast growing Medicare Advantage market.

For further details see:

P3 Health Partners: Just Another SPAC-Listed 'Value-Based Care' Company?