AGL - P3 Health Partners On Solid Path To Profitability

2023-06-15 07:00:00 ET

Summary

- Big losses have plagued P3 Health Partners in the fast-growing sector of population health management and have resulted in severely depressed share prices.

- On the positive side, P3 losses continue to improve and share prices are climbing again.

- P3 CEO announced that recent $90 million funding and cost-cutting measures will help reach Adjusted EBITDA profitability in 2024.

- Insiders are buying P3 stock in the open market and M&A activity in healthcare is robust.

- Recent share prices have rallied to reflect these improvements, but may have several multiples go if management continues to deliver.

As a 20-year veteran serving doctors, P3 Health Partners (PIII) is a population health management company that supports providers with administrative services and care coordination for Medicare Advantage patients. P3’s model aggregates and supports the community’s existing healthcare resources to build a network of community providers working together to deliver highly coordinated and integrated care to patients with a shared commitment to improving patient outcomes, lowering cost, and delivering a better experience for all.

In February 2023, I covered P3 Health Partners in an article titled, “P3 Health Partners Reaffirms 2022 Growth Over 61% and Path to Profitability” . My view at that time was that there are cost-cutting measures and powerful Digital Healthcare platforms that can help greatly reduce labor costs which could have an enormous positive impact on P3 income. P3 shares were then trading at $1.03. Today, they are trading at about $4.50 for a very impressive gain of over 400% in under 4 months. The big question I ask now is, “Will P3 shares continue to perform well?”

In an attempt to answer this question, it would be helpful to have an understanding of what the 2023 and 2024 landscape is surrounding projected sales, margins, cost-cutting measures, and capital availability. The overall general stock market environment is also a big factor that can greatly impact share price performance, but that is one that nobody can predict with any degree of certainty. My personal opinion is that we may be entering a time when the Fed is likely to begin loosening its grip on the money supply and the cost of money which should be good for stocks and for metal prices. Time will tell.

Sales have not been the problem. The big problem for investors is the very large losses that the company has continued to report. P3 Growth has been rapid and is expected to continue at high rates because there are over 938,000 practicing doctors in the United States and so far, P3 Health Partners is serving close to only 2,500 which means there is the potential of gaining meaningful numbers of the remaining 935,500.

There is only one road to profitability for population health and that is the one of lower costs because claim limits are set by Medicare and payors. This means that P3 must be confident of their ability to manage their patients with decreasing costs. If you do the P3 math, 100,000 patients and 2,500 doctors, P3 is only handling about 40 patients per doctor and each doctor typically has between 1,000 and 4,000 patients . The 40 patients that P3 is serving are most likely the more chronically ill and more difficult to manage patients that are over burdening the physicians. Just imagine how many patients P3 can attain if they show efficacy and profitably on the first 40 patients of a case load that is over a thousand and where over 50% of all patients have at least one chronic medical indication. Chronically ill patients are exactly the ones that P3 wants to provide healthcare to and the numbers are staggering.

If P3 can substantially reduce costs, they could enjoy enormous growth and profit potential because they have barely scratched the surface of available patients and there are about 938,000 doctors and about 60 million people on Medicare.

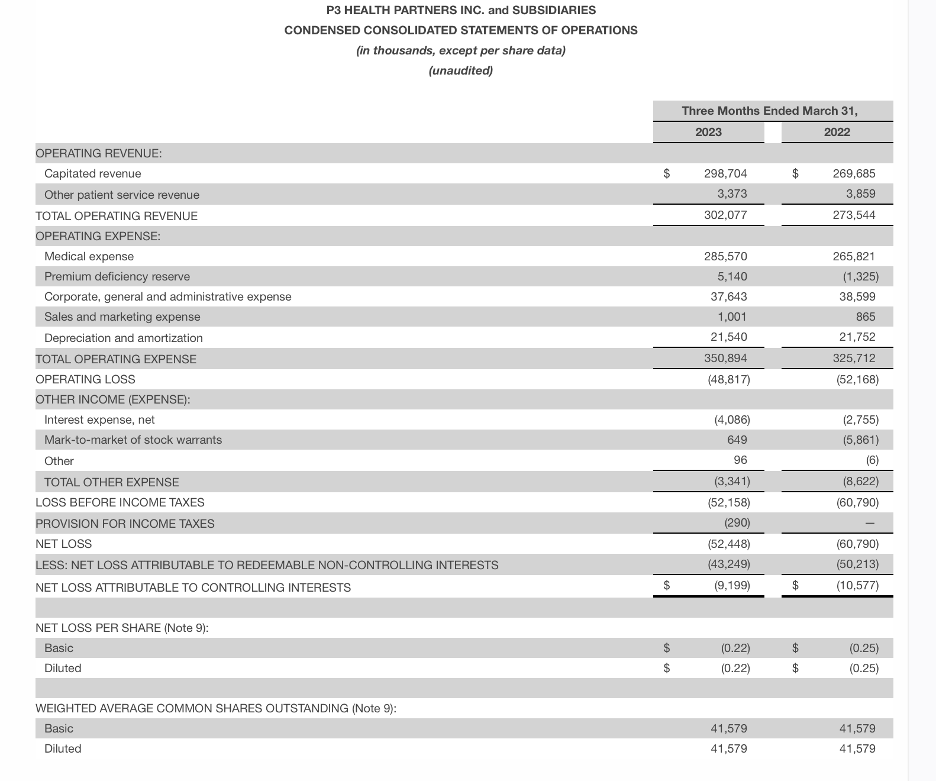

P3 has been steadily reducing losses and recently announced a very significant quarter with revenues continuing to increase and a very healthy improvement in reducing losses by 14% quarter over quarter for Q1 '23 versus Q1 '22.

P3 recently announced the following First-Quarter 2023 Results and 2023 guidance:

- Capitated revenue was $298.7 million, an increase of 11% compared to $269.7 million in the first quarter of the prior year, and an increase of 18% compared to the fourth quarter of 2022

- Net loss was $52.4 million, an improvement of 14% compared to a net loss of $60.8 million in the first quarter of the prior year, and an improvement compared to a loss of $532.3 million in the fourth quarter of the prior year.

- Net loss PMPM was $169 compared to a net loss PMPM of $203 in the first quarter of the prior year, and a net loss PMPM of $1,766 in fourth quarter of 2022

- Adjusted EBITDA loss was $19.1 million, compared to an Adjusted EBITDA loss of $18.9 million in the first quarter of the prior year, and an Adjusted EBITDA loss of $40.1 million in fourth quarter of the prior year. Adjusted EBITDA loss in the first quarter of 2023 includes the impact of approximately $3 million in consulting and other cost which are not expected to be a part of the ongoing expenses

- Adjusted EBITDA PMPM loss was $62, compared to an Adjusted EBITDA loss of $63 PMPM in the first quarter of the prior year, and an Adjusted EBITDA loss of $133 PMPM in the fourth quarter of 2022

- Operating loss was $48.8 million, compared to $52.2 million in the first quarter of the prior year, and an improvement compared to $537 million in the fourth quarter of 2022.

- Medical margin was $39.2 million, an increase of 58% compared to $24.8 million in the first quarter of the prior year, and $6.6 million in the fourth quarter of 2022

- Network contribution was $16.5 million, an improvement of 114% compared to $7.7 million in the first quarter of the prior year, and an improvement of 250% compared to fourth quarter of 2022

Comparison to Agilon Health (AGL)

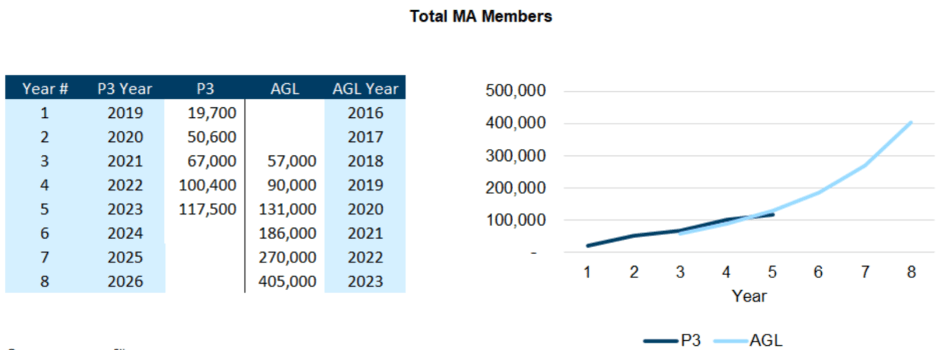

Analysis of Agilon Health’s growth model suggests a bright future for P3 Health Partners. During the company’s first-quarter earnings call, P3’s executive team suggested that the organization is on a fairly similar growth and margin trajectory as Agilon Health. The following charts indicate that P3’s positioning and performance, at present, aligns closely to that of Agilon Health’s from a few years ago when Agilon’s membership base was of a similar size to that of P3.

P3 Health Partners appears to have similar results to the early days (30 months ago) of Agilon Health and appears to be on the right path to profitable long-term growth. Agilon Health trades at about $21 with a market cap of about $8.7 billion. P3 has 103,000 Medicare Advantage members compared to Agilon's 131,000 in 2020.

{kind=link}

Agilon MA growth chart (Agilon web site)

{kind=link}

Recent $90 million financing expected to provide bridge to profitability

The recent funding of $90 million sends a comforting signal to shareholders that big money is friendly and is there for P3 needs. P3 has a good history of being able to raise whatever they need at favorable terms to all shareholders.

“We announced today that we have secured financing of approximately $90 million and believe this provides a solid path to profitability,” said Dr. Sherif Abdou, CEO of P3. “The new financing, along with our expected shift to a higher percentage of persistent lives, a focused reduction in operating expenses, and measured and disciplined growth in 2023 make us confident that we will have the resources necessary to reach Adjusted EBITDA profitability in 2024.”

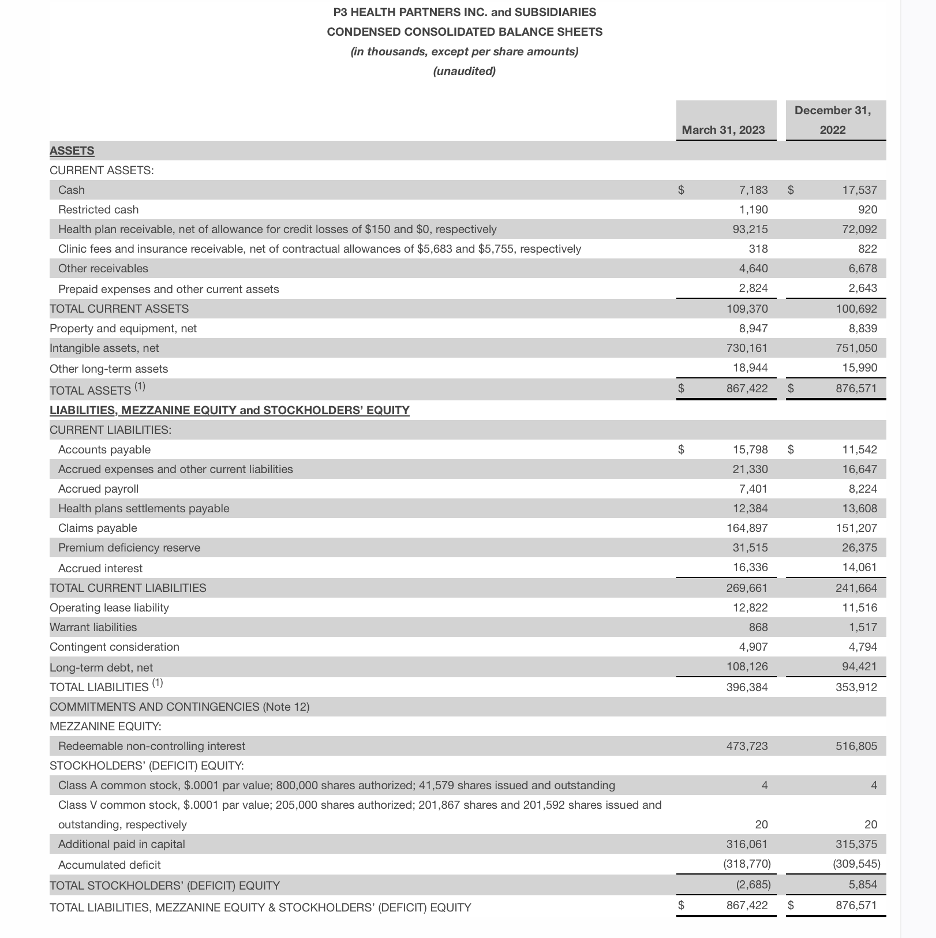

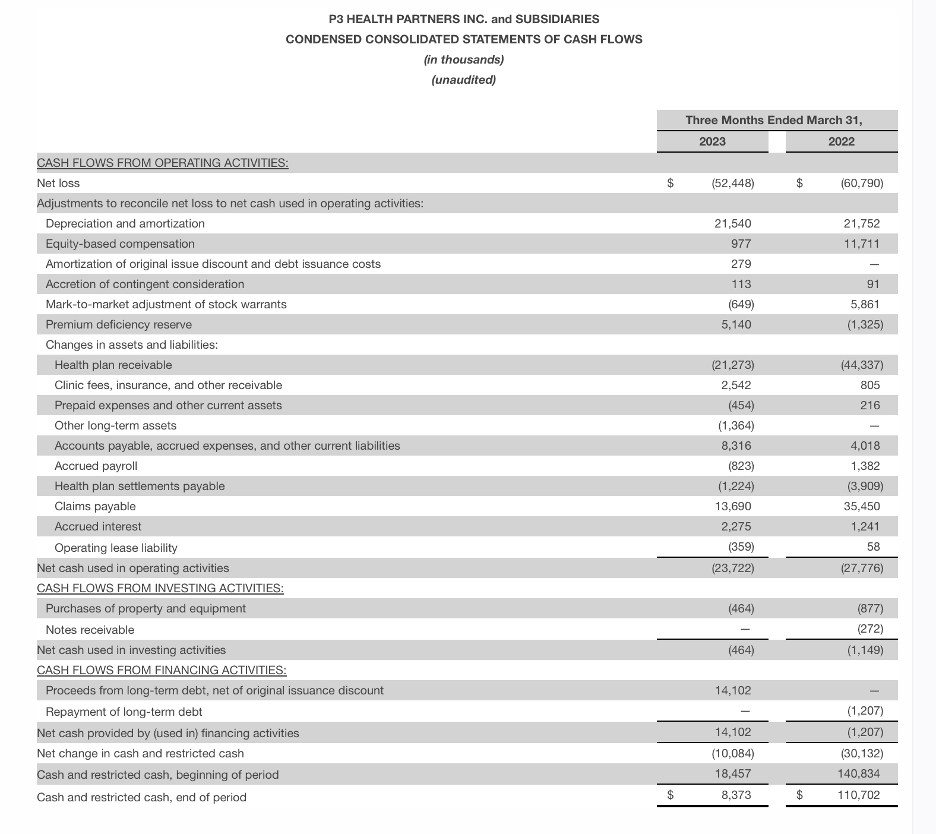

Recent Financials

P3 Balance Sheet - March 31, 2023 (SEC Edgar) Income Statement Quarter March 31, 2023 (SEC Edgar) P3 Cash Flows March 31, 2023 qtr (SEC Edgar)

{kind=link}

{kind=link}

{kind=link}

M&A activity in this sector is robust and P3 insiders are buying

Investors never know when they might be pleasantly surprised with a buyout offer for their company. It may never happen, or perhaps they might wake up to a big surprise one day. M&A activity in healthcare remains very active.

On February 8, 2023, CVS Health (CVS) announced it entered into a definitive agreement to acquire Oak Street Health in an all-cash transaction for $39 per share, representing an enterprise value of approximately $10.6 billion or 3.5 times forward revenue. Amazon (AMZN) bought OneMed for $3.9 billion. Kaiser Permanente is acquiring Geisinger Health and will combine the entity under Risant Health. Kaiser will seek out another four to five health systems to form a national network of health systems in VBC contracts, which should generate about $30 billion in revenue over the next five years, according to management.

Option Care Health (OPCH), a leader in the home infusion services industry, also announced its acquisition of Amedisys (AMED), a leading healthcare-at-home company focused on hospice and high-acuity care services.

Vytalize Health, a risk-bearing provider enablement platform, recently announced that it acquired a majority interest in Independent Physician Association of New York, one of the largest multi-state independent physician associations in the United States and employs more than 3,000 providers. commercial plans, and Medicaid, and we view it as a highly strategic acquisition for the organization.

In 2022, there were 2,277 deals valued at $127 billion and so far, 2023 looks like it will exceed 2022 levels.

A recent report by Nasdaq indicates that P3 insiders are buying substantial amounts of shares on the open market.

Risk factors

One of the greatest risk factors is a company running out of money and P3 Health Partners has recently met this challenge with the announcement of $90 million in new funding. So far, it appears that investors continue to favor P3. While the company labels their risk factor as high, it is best to review the regulatory filings for detailed information.

Conclusion

I am even more bullish on P3 shares since my first article. I believe shares of P3 Health Partners are beginning to recognize some of the early results of cost-cutting measures and shares could be poised for even greater growth which we are seeing in loss reductions and profitability forecast for 2024. P3 is fast becoming a success and with such a large potential market in need of their services, the future looks very bright. In just a few short years, P3 achieved 2022 sales over the billion-dollar mark. Just imagine what the next few years holds in store if revenues continue to expand and if costs continue to be dramatically reduced. If success continues, thousands of physicians and investors could find their services attractive.

I personally believe P3 should do close to $1.25 billion in revenue this year and close to $1.5 billion next year. Even at 3x forward revenue and assuming full dilution for all shares (which doesn’t reflect cash that will come into the company with the exercise of options and warrants), would fetch between $11.5 - 12/share. There is certainly a lot of strategic interest and the fact that Chicago Pacific Ventures owns a lot and has bought more recently, they would not likely be a seller unless the price was significantly higher.

Dr. Sherif Abdou, co-founder and CEO of P3 Health Partners says: “If you have a happy patient and a healthy patient, you will have more patients, you will have lower costs, and you will have created more value for the patient and the system. Dr. Abdou is building a great team and is performing according to plan.

For further details see:

P3 Health Partners On Solid Path To Profitability