PIII - P3 Health Partners Reaffirms 2022 Growth Over 61% And Path To Profitability

Summary

- P3 Health Partners’ guidance breaks the billion-dollar mark in 2022 revenues.

- P3 Health Partners anticipates that its Adjusted EBITDA will be positive in 2024.

- P3 Telehealth and more advanced Digital Health and Telehealth support platforms coming to market can substantially accelerate growth and profits as they are implemented.

- At the current share price of $1.03, P3 Health Partners share price is undervalued compared to industry comps based on competitors' price to sales ratios, growth rates, and cost containment.

Revenues of population health management company, P3 Health Partners (PIII) have been climbing fast, but large losses have sent shares falling in the past 12 months from $8.19 per share to $1.04 per share. Population health stocks have been in a tailspin from heavy losses but recently, P3 management reported guidance for smaller losses and believes those losses will continue to narrow in 2023 and that the company will actually achieve profitability in 2024.

In addition to P3's narrowing losses that are expected to turn profitable by 2024, P3 Health Partners valuation is 9 times lower than competitors. See calculations and table below.

There is only one road to profitability for population health and that is the one of lower costs because claim limits are set by Medicare and payors. This means that P3 must be confident of their ability to manage their patients with decreasing costs. If you do the P3 math, 100,000 patients and 2,500 doctors, P3 is only handling about 40 patients per doctor and each doctor typically has between 1,000 and 4,000 patients . The 40 patients that P3 is serving are most likely the more chronically ill and more difficult to manage patients that are over burdening the physicians. Just imagine how many patients P3 can attain if they show efficacy and profitably on the first 40 patients of a case load that is over a thousand.

My conclusion is that if P3 can substantially reduce costs as they claim, they could enjoy enormous growth and profit potential because they have barely scratched the surface of available patients and there are over 60 million people on Medicare and very few population health companies, if any, have figured out how to do this yet.

Telehealth may have been slow to adopt, but Covid clearly accelerated its use and it is now becoming commonplace and ripe for mass adoption. Digital Health solutions are in their infancy and there is an abundance of individual solutions that is becoming available every day.

P3 Partners is already using Telehealth encounters to increase effectiveness and to decrease costs and in my opinion, it is only a matter of a short time before they implement far-reaching Digital Health solutions that can catapult revenues and profits.

At more than $4T per year , healthcare is one of the largest sectors in the market and offers some of the biggest investment opportunities because it continues to be plagued by inefficiencies, misalignments, and high costs.

These problems affect most Americans and include inadequate access to care , poor patient literacy , low patient adherence to the doctor’s treatment regimen, far too many hospital readmissions and avoidable episodes of care, excessive costs, over-burdened physicians with too many patients and not enough time, too much time-consuming paperwork for billing , and the list goes on and on.

On January 11, 2023, P3 Health Partners, Inc., reaffirmed full-year 2022 financial guidance and announced financial guidance for the full-year 2023. Judging by the low price of P3 shares, readers would have expected bad news, but instead, the news was very positive and confirmed record growth. The company announced:

- For the full-year 2022, P3 is reaffirming the revenue guidance range given on the third quarter earnings call of between $1.025 billion and $1.075 billion, representing a 61% to 69% increase over 2021.

- The at-risk Medicare Advantage membership is expected to be greater than 100,000 for the full-year 2022, representing a roughly 35% increase over prior year.

- Adjusted EBITDA loss is expected to be between $118 million and $128 million, as previously announced.

For full-year 2023, the Company’s preliminary guidance is as follows:

- At-risk Medicare Advantage membership is expected to be in a range of 115,000 to 120,000

- Revenue is expected to be in a range of $1.20 billion to $1.25 billion

- The Company expects that 2023 Adjusted EBITDA loss will be between $40 million and $60 million.

- The Company anticipates that its Adjusted EBITDA will be positive in 2024.

Revenue growth is strong and Per Member Per Month cost is declining

P3 Health Partners and competing population management companies are using every means possible to help reduce costs and improve efficiencies and are constantly searching the marketplace for ways to reduce cost. The most obvious place to look for cost-cutting is in using automation to reduce staff, decrease the avoidable episodes of care, decrease hospital readmissions, utilize telehealth in newer and more efficient ways, train and certify patient family members to provide the patient care. It is important to note that over 90% of care is provided in the home by non-professionals. This appears to be one of the standout places where the wheels fall off the bus.

Digital Health platforms that include and go beyond Telehealth

As more efficient Digital Health platforms come into the marketplace to help population management companies, patients, providers, and payers, costs will come down and profit will rise.

Digital Health solutions using AI and closely networked to connect the patients with their caregivers are the most likely solutions to improve patient outcomes and reduce avoidable episodes of care. Digital Health solutions have been slow to materialize, but with the recent explosion of Telehealth that was fostered by Covid, it is only a matter of time when they will be available to improve patient outcomes, cut costs dramatically, and contribute to profitability.

Imagine a population health company like P3 Health Partners integrated in a partnership with state-of-the-art automated care management systems that utilize trained and certified family members and trained and certified AI ChatBots. These trained and certified family members and AI ChatBots are always available, they are fully trained to properly manage to patient's specific diagnosis . . . and they are free at no charge, thereby slashing healthcare costs almost overnight.

P3 is a leader in population health and as such expects to be among the first to employ new automated Digital Health technologies to increase revenues and dramatically improve the care they provide. Better patient outcomes, fewer avoidable episodes of care, and expanding the efficiency of the physician’s staff with automation and "no fee" non-professional family members that are trained and certified for their task is exactly what the doctor ordered.

Market comparisons

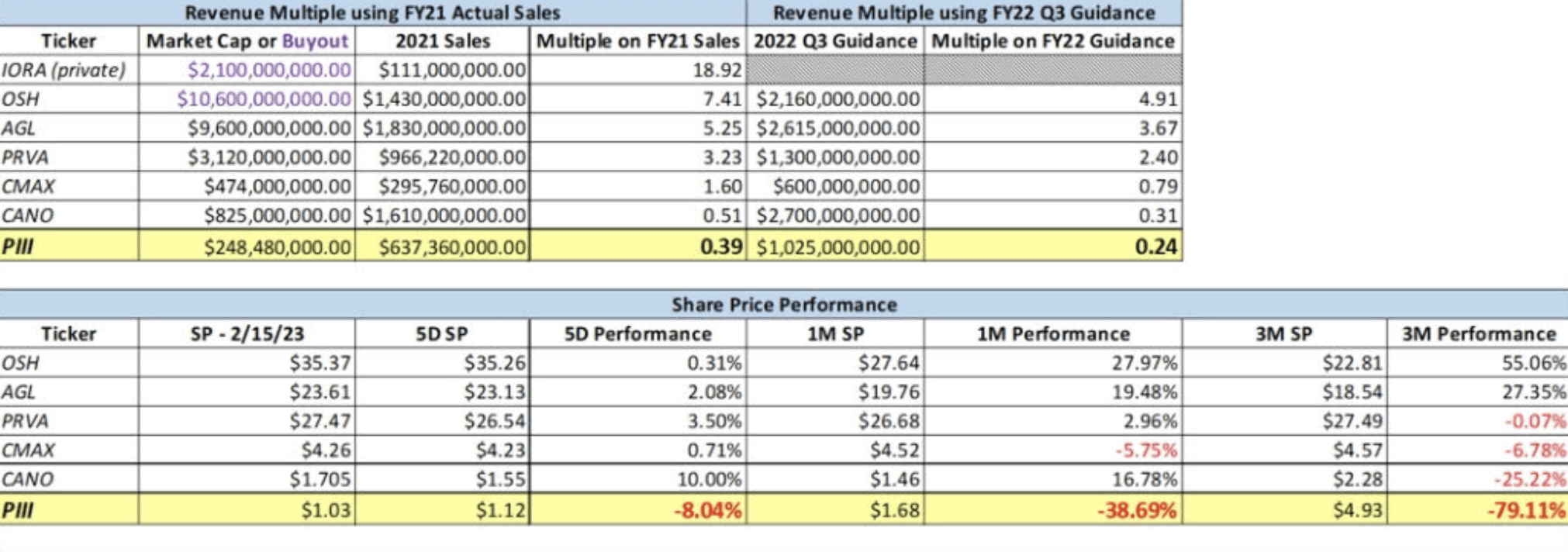

I believe P3 Health Partners shares are undervalued for a number of reasons: First, take a look at this chart of share price to sales ratios of P3 and several competitors. It’s not often when an investor can buy a stock at 25% of its annual revenues. What happens if the company turns profitable? The share price will rise dramatically and based on their comments about lowering costs to achieve profitability, I believe P3 Health Partners is positioning to do exactly that.

A few noteworthy competitors reporting significant losses are Cano Health (CANO): reported a loss of $113,259,000 for the quarter ending September 30, 2022, Oak Street Health (OSH) reported a loss of $130,700,000 for the quarter ending September 30, 2022, agilon health, Inc., (AGL) reported a loss of $30,668,000 for the quarter ending September 30, 2022, Privia Health Group, Inc. (PRVA), reported a loss of $1,624,000 for the quarter ending September 30, 2022, and CareMax, Inc., (CMAX) reported $22,053,000 for the quarter ending September 30, 2022.

Valuations based on Revenue/share price ratio

The following chart shows an average share price to sales ratio of 3.6 to 1. P3 Health Partners has an exceptionally low ratio of .39 which is 9 times cheaper than the competition. This is an important comp when attempting to demonstrate valuations.

{kind=link}

{kind=link}

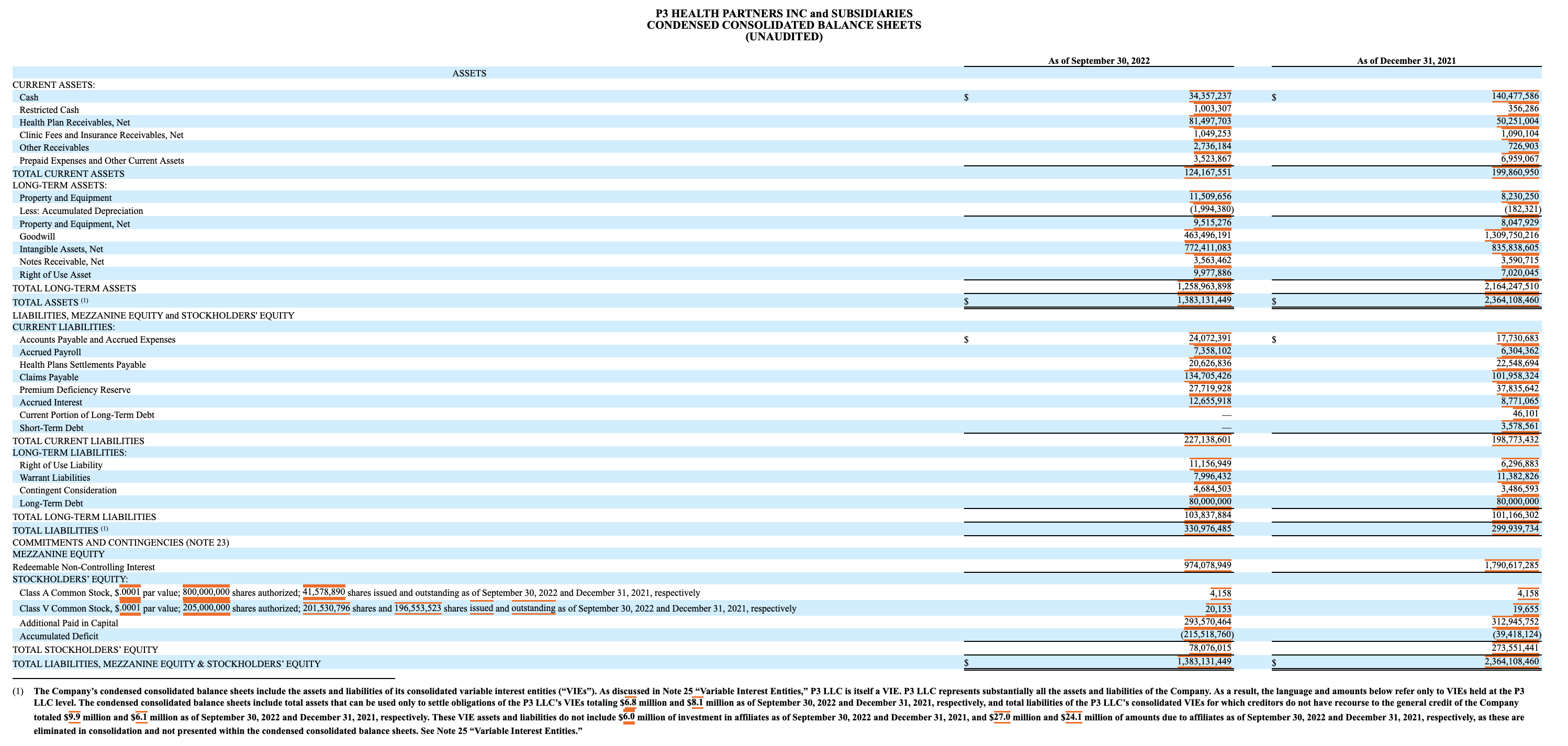

P3 HEALTH PARTNERS BALANCE SHEET (SEC EDGAR)

{kind=link}

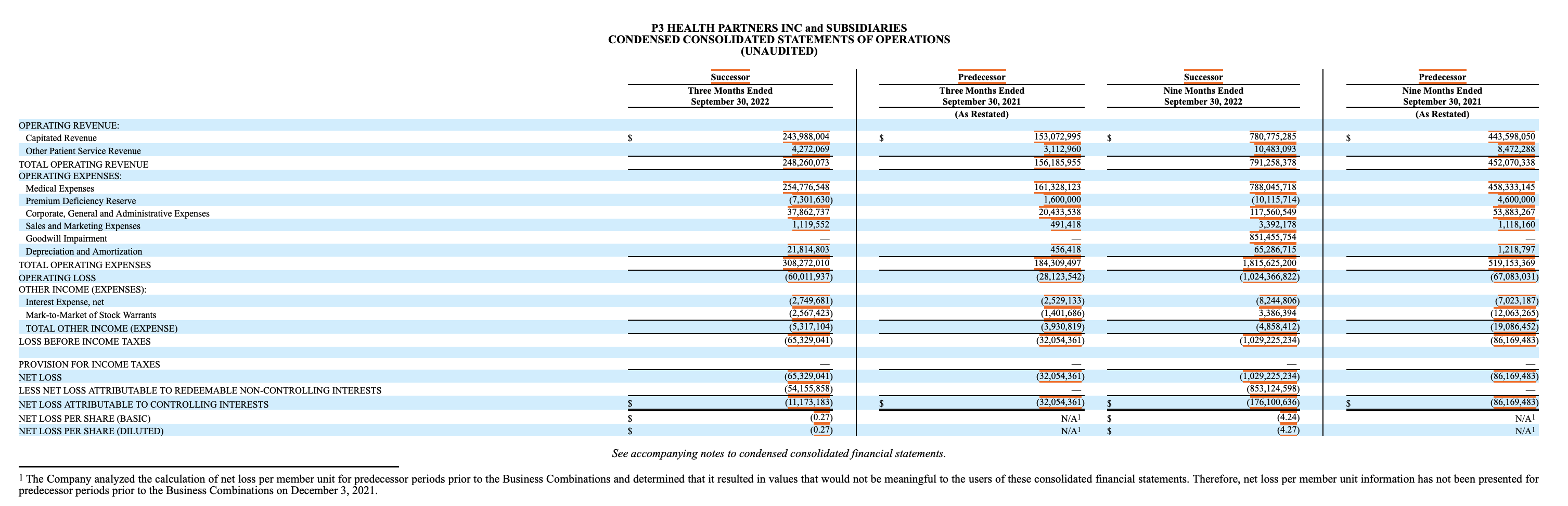

P3 HEALTH PARTNERS INCOME STATEMENT (SEC EDGAR)

Risk factors

One of the greatest risk factors is a company running out of money and P3 Health Partners clearly has big and growing revenues to negotiate with. While the company labels their risk factor as high, it is best to review the regulatory filings .

Conclusion

I believe shares of P3 Health Partners are selling at exceptionally low prices that are indicative of failure when in fact P3 is fast becoming a roaring success. In just a few short years, P3 achieved 2022 sales over the billion-dollar mark. Just imagine what the next few years holds in store as revenues continue to expand and as costs are dramatically reduced.

Dr. Sherif Abdou, co-founder and CEO of P3 Health Partners says:

If you have a happy patient and a healthy patient, you will have more patients, you will have lower costs, and you will have created more value for the patient and the system.

Dr. Abdou knows the healthcare system well and is a proven problem solver.

For further details see:

P3 Health Partners Reaffirms 2022 Growth Over 61% And Path To Profitability