PIII - P3 Health Partners: Right Place Right Time Wrong Horse To Back?

2023-09-10 08:31:22 ET

Summary

- P3 Healthcare, operating in the value-based care space, has seen its stock price plummet by ~80% since its Nasdaq listing.

- The company operates within the Medicare Advantage market and provides comprehensive healthcare services to MA plan members on behalf of healthcare payors.

- P3's recent performance has shown some solid revenue growth and a decrease in net losses, but funding is running out and momentum is being checked in several key areas.

- Since my June "Hold" recommendation, P3's stock price is down >50%, after a long bull run. Unfortunately, the challenges of uncertain yet crowded market mean things may get worse before they get better.

Investment Overview

When I last wrote about P3 Health Partners (PIII) for Seeking Alpha back in June , I advised readers that the company was operating in "an intriguing space" - value based care - with "narrowing losses", and that it was "undervalued vs some key peers". I stopped short of making the company a "buy", but advised investors to "keep the company on your watchlist".

I'm glad I didn't advise investors to Buy, because after embarking on a sensational bull run across the second quarter of 2023, with shares climbing from <$1, to >$5 by the beginning of June, the stock price has subsequently gone into free fall, dropping <$1.5 at the end of August, before mounting a slight recovery to trade at $2.1 at the time of writing, giving P3 a market cap valuation of ~$660m.

As I noted in my previous post, P3 achieved its Nasdaq listing thanks to a merger/business combination with Foresight Acquisition Corp, a Special Purpose Acquisition Company ("SPAC") i.e. a blank check company that lists as a shell corporation with the purpose of acquiring a private business and taking it public - in this case P3. SPAC's list with a share price of $10, and have 2 years to find a suitable company or money is returned to investors.

Perhaps Foresight investors regret the decision to merge with P3, as its stock is now down ~80% since listing. That is not at all unusual - SPAC listed companies almost invariably experience heavy share price losses in their early days of trading - and to date, not many have shown that they can claw any of that lost value back.

In my post however I did discuss many aspects of P3's business model and performance that might provide reasons to be confident that longer-term, P3 could be the exception that proves the rule. For a full discussion of Value Based Care and its relationship with Medicare Advantage health insurance plans - the fastest growing and most lucrative market in this industry - I would suggest reading my former note.

In this post I'll briefly recap on P3's business model, recent performance, competition and market opportunities, and speculate on whether the fact that shares are 50% cheaper than 3 months ago makes for an intriguing buy opportunity, or can be interpreted as a red flag and a sign that P3's business model is fundamentally flawed, and the company in trouble.

P3 - Business Model Recap

As I explained in my last note, P3 Healthcare operates within the $829bn Medicare market, which covers 65m eligible lives, with a core focus on the Medicare Advantage ("MA") market, which makes up 48% of the overall Medicare market, or ~28m lives (data from P3 Q223 10Q submission / quarterly report ).

The idea is that Medicare Advantage plan providers - who administer Medicare Advantage on behalf of the Centers for Medicaid and Medicare Services ("CMS"), in exchange for a pre-agreed fee per member, and earn a percentage of whatever money they don't spend taking care of members, plus an additional bonus if their plans earn a 4 star of 5 star rating - pay P3 a per member, per month ("PMPM") fee to provide "holistic, comprehensive healthcare" to their members.

According to P3, "these PMPM fees comprise our capitated revenue and are determined as a percent of the premium (“POP”) payors receive from CMS for these members". This is my first problem with P3's business model - taking a POP from a company this is itself taking a POP surely makes it difficult to drive profit margins?

P3 then takes care of "emergency room and hospital visits, post-acute care admissions, prescription drugs, specialist physician spend and primary care spend", amongst other services. The company then enters into arrangements with local physicians or physician groups who work under P3's auspices, doing the best they can to provide "value based care" and reduce P3 and the healthcare payors' spending - yet another layer of service that eats further into profit margins.

Despite the number of stakeholders ultimately claiming revenues from the same source - CMS and the taxpayer - Medicare Advantage members are the most prized by major health insurers, and value based care is perceived as the optimal way to administer better healthcare, at a lower cost. CVS Health (CVS), for example, has made it a cornerstone of their strategy , paying ~$11bn in December last year to acquire Oak Street Health, whose business model is very similar to P3s.

The issue for P3 is that the marketplace is becoming saturated with Value Based care focused companies. In its 2022 10K , P3 lists competitors as Oak Street, Cano Health ( CANO ), and agilon health ( AGL ), and there are more players besides - Evolent Health ( EVH ), Apollo Medical Holdings ( AMEH ), Addus HomeCare ( ADUS ), CareMax ( CMAX ), Pennant Group ( PNTG ), and Nutex Health ( NUTX ) for example.

Of all of these companies, only Addus - +21%, and Apollo - +102% - have made share price gains over the past 5 years, or since listing. Caremax stock has lost nearly 80% of its value, and Nutex and Cano >95%.

P3 - Recent Performance

Far from being a cash cow, as we can see above most companies are struggling to make the value-based care business model work for the bottom line - as mentioned in my previous note, Oak Street, prior to acquisition, made a net loss of ~$(500m) in 2022, and a net loss of ~$(400m) in 2021.

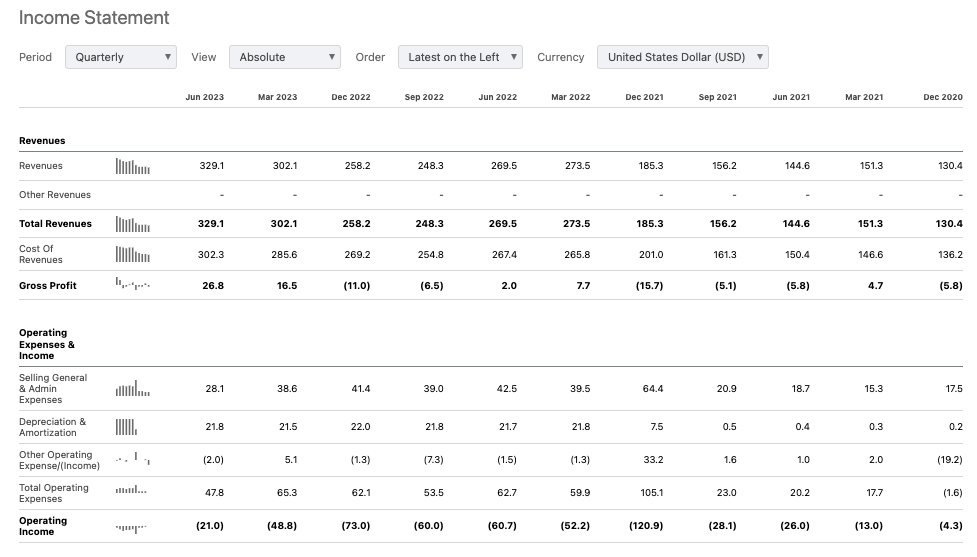

P3 quarterly income statements (Seeking Alpha)

{kind=link}

As we can see above, P3's quarterly income growth has been reasonably solid - revenues have grown in almost every quarter since the final quarter of 2020, and you can just about point to a downward trend in net losses, although with a cash position reported as of Q223 of just $60m, with $104m of receivables, and total current liabilities of $250m, it seems that the funding runway is exhausted, and the company must either start turning a significant profit almost immediately, or raise more funding, which would likely dilute investors if completed via an at-the-market fundraising, and drive down the share price.

Revenues increased 22% year-on-year in Q223, whilst there is barely any comparison between net loss year-on-year, since, owing to a goodwill impairment charge, net loss in Q222 was >$(900m). The adjusted EBITDA comparison is a fairer measure, and that decreased from a loss of $29m in Q222, to just $0.2m last quarter. Medical margin - the amount earned from capitation revenue after medical claims expenses are deducted - was $50.5m - up >130% year-on-year - which works out at $161 per member per month.

For the full year 2023, management has forecasted for total Medicare Advantage members of 115k - 120k, revenues of $1.2bn - $1.25bn, medical margin of $155 - $175, and adjusted EBITDA of $(50m) - $(30m).

During the Q223 earnings call with analysts, P3's CEO Sherif Abdou - a 30-year healthcare services veteran with an impressive track record - compared P3's medical margin favourably with Agilon Health. Agilon - a $7.4bn market cap company - has 4x as many MA members using its services as P3 does, however, is forecasting for nearly 4x higher revenues in FY23, and is just about breaking even. An altogether safer bet for investors looking to gain exposure to the MA / value based care market, albeit with less explosive growth potential.

Looking Ahead - What Is P3's Strategy For Growth?

Explosive growth potential can often also mean that a company is teetering on the brink of failure, as well as success - but which is the case with P3?

The company made a notable hire last quarter, appointing William "Bill" Betterman as Chief Operating Officer. Betterman joined from Optum Care - part of the healthcare giant UnitedHealth ( UNH ), where he was in charge of Pacific NorthWest operations.

P3 is now active in 5 states - Arizona, Nevada, California, Oregon and Florida - and with its experienced management team, the company arguably has the tools and the team at its disposal to drive some strong growth - as Bill Betterman told analysts on the latest earnings call :

In my prior experience, I saw the affiliate model in action in two important ways: First, ability to grow; and second, ability to bend the cost curve. I was drawn to P3 because I believe the model is highly effective and the team has significant experience in helping drive it to optimal outcomes. The affiliate model works across geographies, payers and providers.

If we compare the Arizona market from 2018 to the second quarter of 2023, the trajectory of the P3 model becomes clear. Let's take members, for example, in 2018, it was 10,000. Today, it is approximately 45,500. Revenue PMPM, in 2018, it was $628 PMPM. In the second quarter of 2023, it was $921 PMPM. Medical margin PMPM, in 2018, it was negative $53 PMPM. In the second quarter of 2023, it was positive $163 PMPM. And in the future, we expect continued improvement.

With ~10k Americans becoming eligible for Medicare Advantage plans every day in the US, and that rate set to continue until 2030, it is estimated, there is no shortage of market share up for grabs, and as its business model matures, and patient population adapts to the value based care, P3 is confident it can drive positive EBITDA by 2024, as shown below in a slide from a recent investor presentation.

P3 path to profitable growth (P3 presentation)

{kind=link}

The Right Model, At The Right Time - But Ultimately, The Pitch Is Not Compelling

P3 states in its 2022 10K that:

We believe there is significant white space opportunity. As of December 31, 2022, we have contracted with 2,800 primary care physicians, an increase of 33% from 2,100 at December 31, 2021. This represents less than 1% of the total number of PCPs in the U.S. of approximately 502,000. The industry is primed for a platform like ours, which allows physicians to remain independent while accessing financial resources and infrastructure to support a VBC model.

Whilst I agree the industry is indeed primed for a platform like P3's, there are several reasons why I am sceptical that P3 will show long-term outperformance.

The first is that the value based care industry, being new, is fragmented, with a plethora of companies being set up in both the public and private markets offering a broadly similar business model. In a very minor way, you could compare it to the dot com boom of the early noughties - how many of these of these companies have a genuinely compelling value proposition?

Secondly, P3' route to the public markets, via a SPAC, is not only a historically unsuccessful path, but it also feels as though the company may have been put together too rapidly to try to take advantage of the VBC / MA boom, and although it has had some success, with >100k members, and nearly 3k contracted, it's important to remember these contracts are frequently renegotiated, and the competition is already fierce, and getting fiercer. There are no guarantees the business can retain these contracts.

CVS's purchase of Oak Street can be held us a great example of what can happen if you can scale a VBC business fast enough, but my suspicion is that Oak Street is the exception, rather than the rule. As already mentioned, most listed VBC focused companies have performed poorly for shareholders, and with P3 having already written off ~$1bn via a goodwill impairment charge, and with its funding almost exhausted, expansion feels a long way off.

If you were a healthcare payor looking to partner with a VBC specialist, is P3 the business you'd be hoping to partner with? In my view, healthcare payors, in the long-term, will opt to build VBC franchises in-house, consolidating margins as opposed to farming them out to middle-men.

Finally, although there are plenty of successful "middle man" companies, as I have mentioned above, my sense is that many VBC companies do not provide a significant enough value add to justify their place in the hierarchy. Although P3 has made some good progress with its medical margin, and revenues, my suspicion is that the numbers may not be large enough.

In a fragmented market such as VBC, some smaller companies will emerge as dominant players, growing organically and through M&A. With no funds for M&A, P3 must look to organic growth, as economies of scale are rewarding in this business. On the Q223 earnings call however, management faced questions about a fall in the number of payors it contracts with, as well as flat membership growth.

For investors looking to gain exposure in a fast growth market, it's easy to forget that many companies within that space still face tough challenges and only those displaying the very best execution go on to be successful. Often, the company can do everything right and still see the boom in demand pass them by.

With funding running out, profits elusive, growth slowing, or even shrinking by some measures, and competition fierce, personally - and doubtless many will disagree - I believe P3 may have come to the public markets a little too quickly, and its business model may not be sufficiently robust to compete in a market where the opportunity is clear, but where attempts to harness that opportunity are falling flat more often than not.

For further details see:

P3 Health Partners: Right Place, Right Time, Wrong Horse To Back?