TRATF - Paccar: Overvalued Momentum Stock Worth Holding Onto

2023-07-14 09:51:01 ET

Summary

- Paccar, up 66% over the past year, is among a group of hot truck manufacturing stocks whose prices have boomed along with sales and profits.

- As great as this momentum has been for investors, Paccar might be running too hot and is looking overvalued.

- However, the stock is worth holding onto given Paccar's market position, reliable dividend, consistent record of profitable growth, and knack for beating estimates.

Investment Thesis

PACCAR Inc (PCAR) is among five truck manufacturing giants that have seen their stock soar over the past 12 months, in line with explosive growth in EBITDA and sales. Although the stock has great momentum, it is simply too expensive, potentially trading at 30% over its intrinsic value. The stock, however, is worthy of holding onto because the company is well-equipped to maintain a strong position in the global truck making industry, has a strong record of delivering profitable growth, a steady and reliable dividend, in addition to a knack for beating earnings targets.

Hot Truckmakers Might See Engines Cool

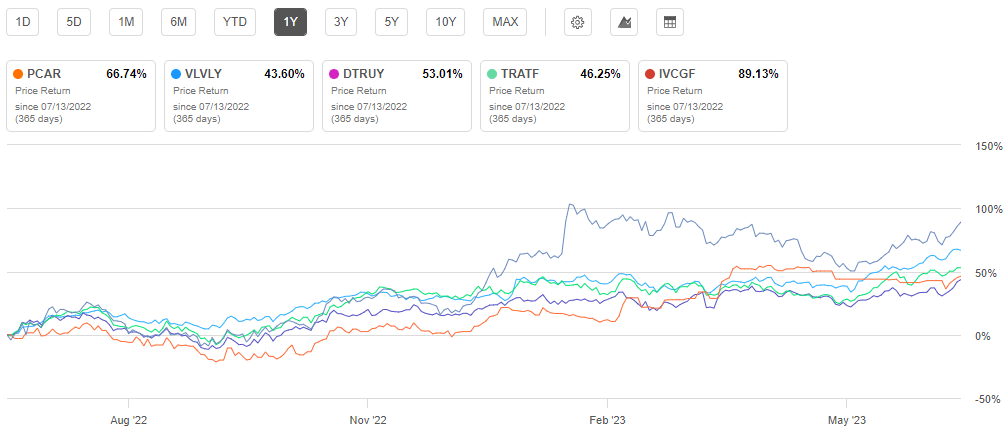

Truck manufacturing giants have been hot stocks over the past year, which makes sense in light of the explosive growth they've seen across the board from sales to EBITDA to EPS. Paccar's stock price soared 66.7% in the past 12 months, and the four companies it identifies as its chief rivals are also up big. Volvo (VLVLY) rose 43.6%, Daimler Truck (DTRUY) 53%, Traton (TRATF) 46.2%, and Iveco Group N.V. (IVCGF) is up nearly 90% since mid-July of 2022.

PACCAR vs. peers stock price performance (Seeking Alpha)

{kind=link}

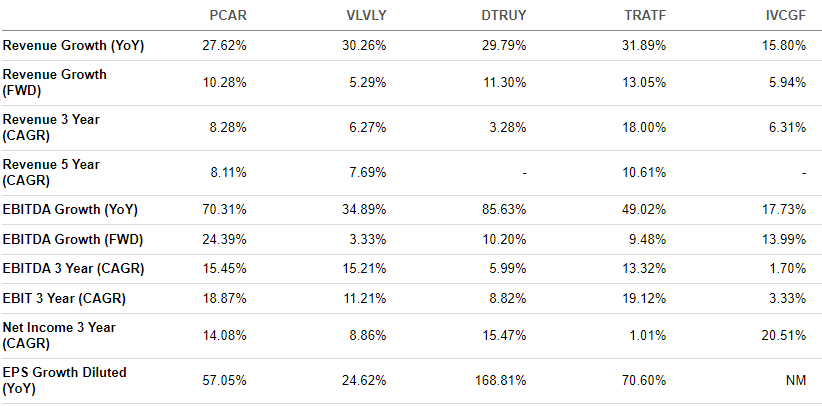

The five companies saw revenue rise by an average of 27% year-over-year while EBITDA grew by an average of 51%.

PACCAR vs. peers growth metrics (Seeking Alpha)

{kind=link}

However, despite strong long-term growth projections, the truckmakers may face a slowdown in 2024. Freight forecasting firm FTR is predicting U.S. Class 8 truck production levels will drop 23% next year - from 320,000 to 245,000 units. S&P forecast a similar slowdown in a note last week, and in fact seemed surprised by the truck markets strength in 2023. The agency cited "stoic" spending on the part of consumers and the fact recession talk was not as pervasive.

Present demand is still strong, owing to the muted risk of recession compared to the previous two quarters, combined with surprisingly resilient consumer activity. Production is expected to sustain its surge in the short term, while remaining constrained by supply chain and labor issues, before levelling off and even declining in 2024.

However, after the slowdown in 2024, S&P painted a positive long-term outlook, saying that electrification will drive accelerating growth as the next tier of greenhouse regulations arrives in 2027 timed with the fleet replacement cycle.

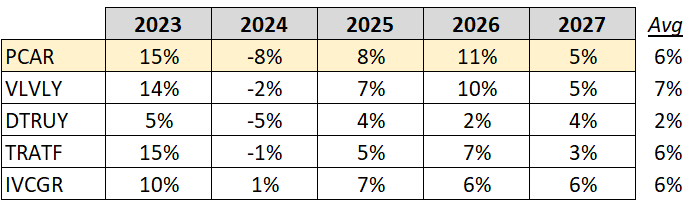

Analysts are forecasting double-digit growth in 2023 for all five truck making giants, except Daimler, which is expected to grow sales by only 5%. However, analysts have roundly estimated a slowdown in 2024, although not as severe as FTR's projection.

Paccar's revenue, forecast to grow 15% this year, is expected to drop by 8 percent in 2024. From 2023-2027, analysts have Paccar, Traton, and Iveco growing by an annualized growth rate of 6%. Volvo over the next five years is expected to grow by an annual average of 7% and Daimler by 2%.

Heavy Truckmaker Sales - Analyst Estimates (Data: Seeking Alpha)

{kind=link}

Valuation

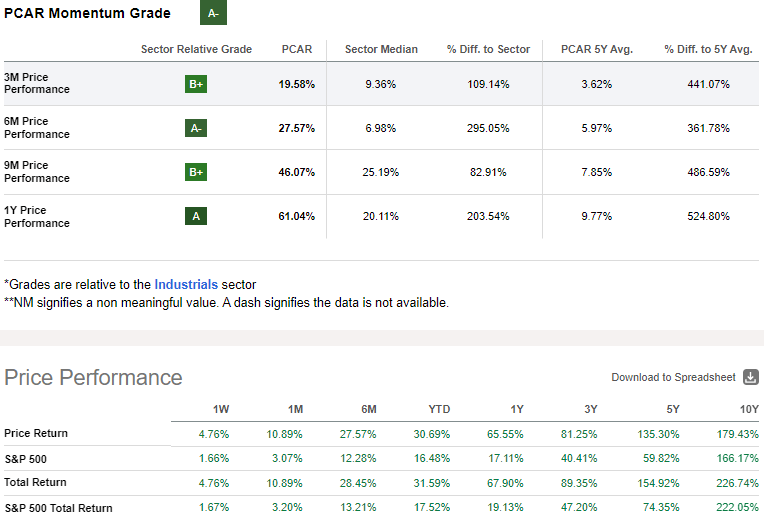

Paccar has certainly been a solid stock for investors in terms of total returns over the past five years, soundly beating the market, and continues to have strong momentum.

PACCAR Momentum Grade (Seeking Alpha)

{kind=link}

And one cannot complain about the company's fundamentals, including profitability performance. In the previous quarter, PACCAR's quarterly operating margin exceeded 17%, marking the highest in at least ten years.

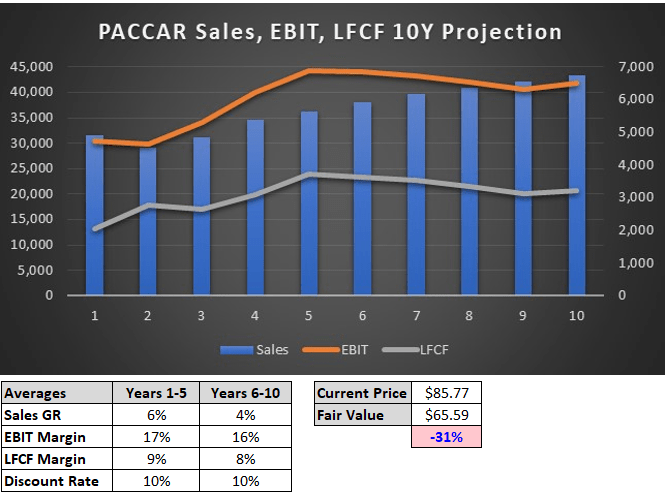

Despite all this, the bottom line is that the stock price is just too high when compared to its intrinsic valuation, based on a discounted cash flow analysis. And this is even under the assumption the company sustains a 17% average in the next five years, the input I used for the base case. For the top line, I relied on the analyst estimates for years 1-5. Capex spending was set at only 2% of sales per the guidance on year one and the tax rate set at 23%. When it is all said and done, I found the stock overvalued by 30%.

Author's PACCAR DCF analysis (MH Analytics)

{kind=link}

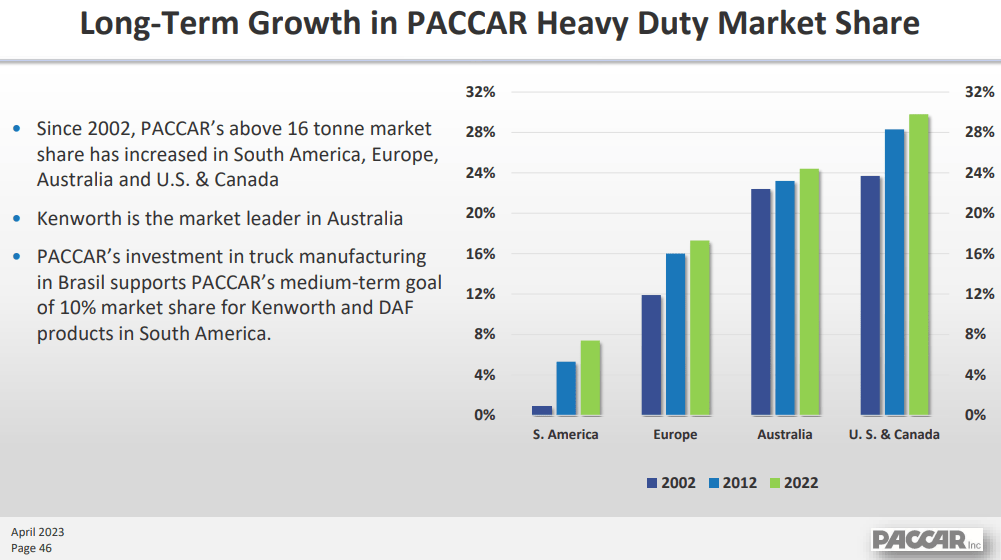

I stopped short of recommending a sell because the company is a major player in the global truck manufacturing industry and its market share has grown substantially over the past two decades. It also has significant upside opportunity to grow market share in South America.

PACCAR Market Share (PACCAR Q123 Presentation)

{kind=link}

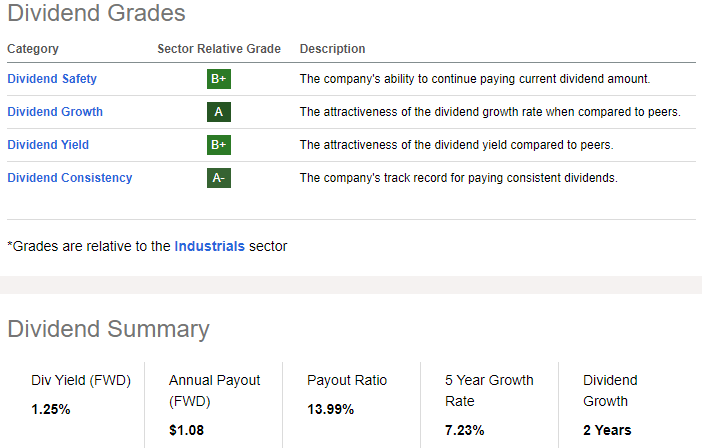

Paccar also has a solid dividend - which is always a good incentive for holding onto a stock, especially when the company delivers strong financial results consistently. Paccar has garnered strong relative grades in every one of Seeking Alpha's dividend categories: safety, growth, yield, and consistency.

PACCAR Dividend Grades (Seeking Alpha)

{kind=link}

Another strength is its analyst revision grades, which suggests to me it is highly like to hit its EPS and revenue targets when it reports earnings on or around July 25. Paccar beat EPS estimates ten times in the past 12 quarters and revenue 9 times.

Risks

Paccar's debt/equity ratio of 86% is a bit high compared to the industry average, although much lower than its four main rivals, and it has steadily dropped over the past five years. Paccar's interest coverage ratio of 7x is much lower than its peers, and it has a net debt of $6 billion.

However, investors should also consider the company has a stellar A+/A1 credit rating and an Altman Z Score of 3.50. In addition, Paccar's short-term assets exceed short-term liabilities and long-term assets exceed long-term liabilities.

Conclusion

Truckmaker stocks are among the hottest in the industrials sector, with Paccar among the leaders, rising 66% over the past year. However, despite great momentum and profitability metrics, the stock appears overvalued by about 30%, although I think it is worth holding onto for a number of reasons. For starters, Paccar is well-equipped to remain a key player in the heavy duty truck market, especially in North America, where it has a 30% market share, with opportunity to grow in South America. Not to mention, the company has strong fundamentals, a solid dividend, and a consistent record in delivering profitable growth and beating earnings targets.

For further details see:

Paccar: Overvalued Momentum Stock Worth Holding Onto