PCAR - Paccar: Q3 Earnings Preview Of An Industry Leader

2023-10-11 10:38:31 ET

Summary

- Paccar outperformed competitors Daimler Truck and The Volvo Group this year, attracting investors during a market sell-off.

- Paccar's consistent management and strong service business contribute to its profitability and high margins.

- Q2 sales were up 24.4% YoY, and Paccar Parts is experiencing significant growth and profitability.

- In this article we go through the latest financials to see what we can expect from the upcoming earnings report.

Introduction

Let's face it: this year Paccar ( PCAR ) performed much better than its two main competitors Daimler Truck ( DTRUY ) and The Volvo Group ( VLVLY ).

What is even more interesting, is that it decoupled from trading in line with the other two since May, when the AI-frenzy started pausing and the general market saw its bull run slow down and then retrace, as it is doing right now.

What has caused Paccar to attract investors during the late part of the last bull-run and in the midst of a sell-off? In this article, I will give a preview of the upcoming earnings report and, the meantime, I will give my take regarding this question. More in depth, we will see why I expect the upcoming earnings report to be rather strong, but this is mainly the effect of past price hikes together with pent-up demand that was still to be fulfilled. As 2024 approaches, there is enough data to believe we will see a more normal environment where sales will see a slowdown.

Summary of previous coverage

For those who are unfamiliar with the company, Paccar is a North-American truck manufacturer of light, medium and heavy duty commercial vehicles. Its main brands are Kenworth, Peterbilt and DAF. In my previous articles , I highlighted how Paccar has achieved excellent financial performance throughout every business cycle, suffering briefly during severe recession, but coming out of each one of them with stronger and growing results. Considering the decline in orders its peers have reported, I gave Paccar a hold rating, assuming a neutral stance at the current share price. In fact, I believe we are in a situation where tailwinds and headwinds will more or less offset one another in the next few months, giving the stock less strength to keep pushing upwards.

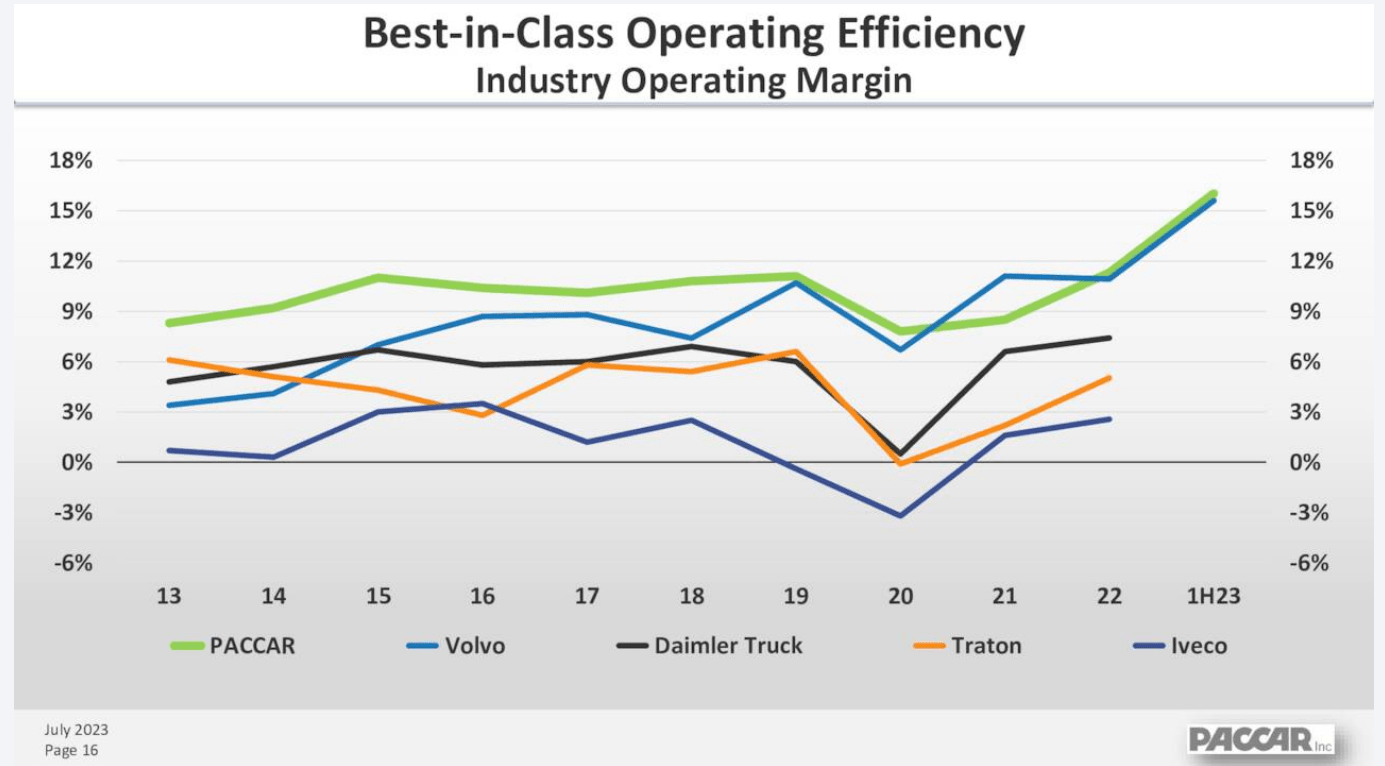

The company has been managed with consistency and, unlike many other companies, it is proud to show its growing results over the past 20 years (usually we see reported results of the last 3 to 5 years). Since the beginning the millennium, Paccar's operating cash flow has compounded at a 6% CAGR. Its operating efficiency has always been fighting with Volvo's for the first spot in the industry.

Paccar 2Q 2023 Results Presentation

{kind=link}

Not by chance, Paccar has reached the 84th consecutive year of profitability, and it has been able to pay a dividend every year since 1941.

But its real secret won't be found in its ordinary manufacturing operations. Investors should be aware that no other player in the industry has invested and has thus built a service business as good as Paccar's that accounts for 25% of total revenues. This is what gives the company a real hedge against downturns . From my rough calculations, we can estimate Paccar has an average revenue per truck around $155k. But then each truck, whose average life should be around 15 years, usually generates something like $2,000 per year in service revenue. This adds another 30,000$ plus inflation over the lifecycle. Of course, these $30+k have very high margins (30% vs. manufacturing whose gross margins are around 14%) and do help fatten the bottom line.

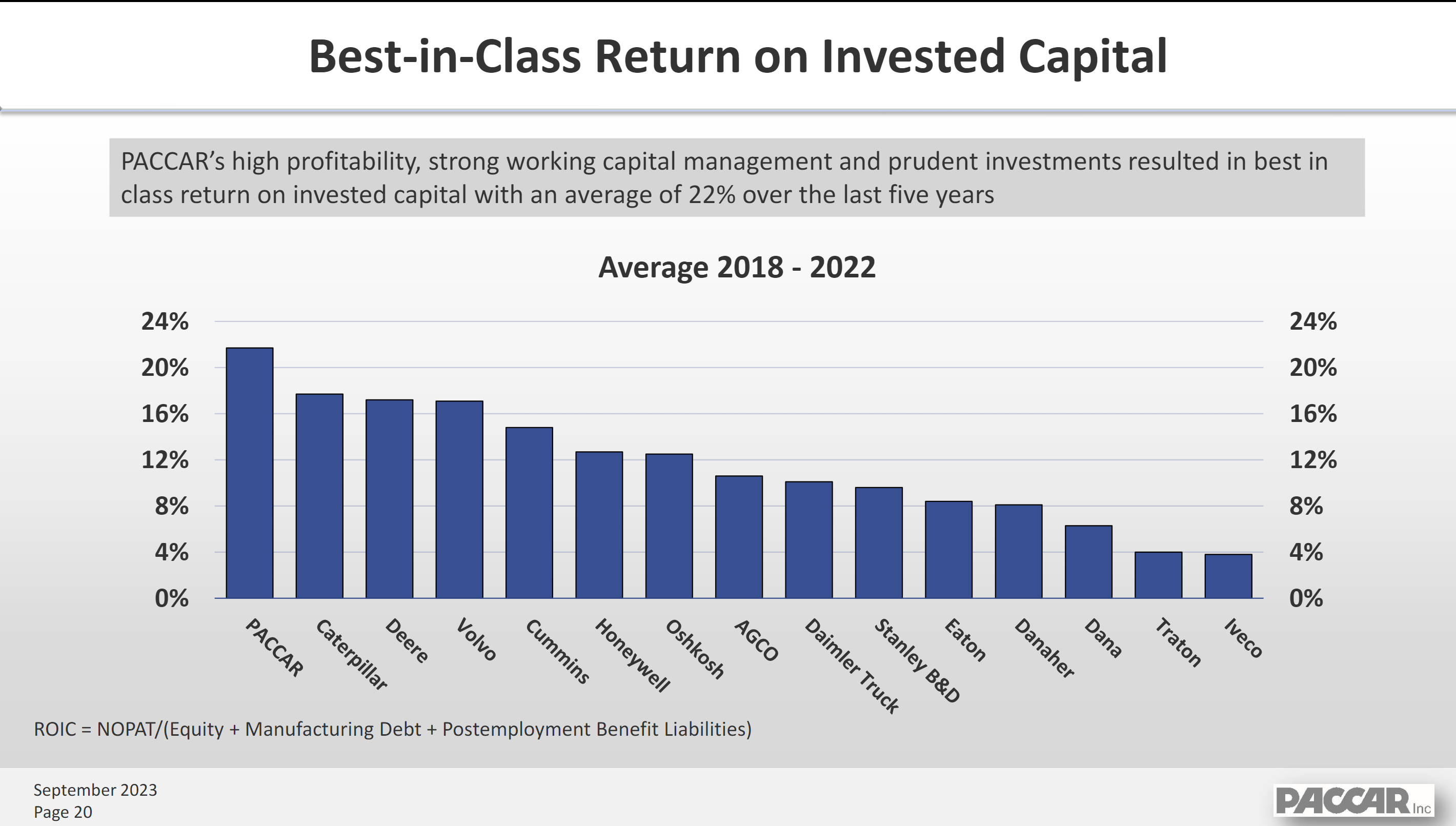

Paccar has proven to employ its capital at high rates of return , even higher than machinery giants such as Deere ( DE ) and Caterpillar ( CAT ).

Paccar Q2 Results Presentation

{kind=link}

With a recession always looming on the horizon (at least in many investors' minds), Paccar could for sure take a hit, but it is in the right position to weather it better than many other manufacturing companies.

Earnings preview

Unlike some of its peers, Paccar doesn't disclose the performance of its order books. However, looking at what its peers have reported, we may assume order intake is slowing for Paccar as well.

However, as far as sales go, 2023 is being a rather good year because supply chain issues are easing and manufacturing companies are able to deliver their finished products. Just in Q2, sales were up 24.4% YoY to $8.44 billion. This is why, in the last earnings call , Paccar disclosed the industry build has been gradually increasing during this year and the Class 8 market is performing well.

In Q2, Paccar delivered 51,000 trucks. In Q3 I expect this to be flat because, on one side, production is speeding up; on the other, Europe shuts down for three weeks during summer.

In Q2 Paccar achieved a whopping gross margin of 18.8%, quite incredible for a company in this business. Yet, with deliveries of trucks sold at high prices (pricing was up 15% in Q2), it would be a large surprise to see a margin below 18%.

I also expect Paccar Parts to reach a gross margin of 32%, a few basis points above the 31.6% achieved in Q2. Paccar Parts is a fast-growing high-margin business, considering that in Q2 alone its sales grew 11% and its profits 19%. If we zoom out and look at the past 5 years, this segment has grown by 73% and its profits have gone up by 136%.

In Q2, Paccar Parts did $1.6 billion in revenue. In Q3, many are forecasting a 6% growth, which would lead to $1.7 billion, at a pretax profit around $450 million. Preston Feight, Paccar's CEO, during the last earnings call, explained why this segment is so successful.

I think the Parts business is growing for several reasons. One is it’s because our ability to get parts to our customers in the same day or next day has changed a lot. So we are the desired place to go for parts for people. I think the application of technology by our team has been an enabler as well, like we make sure that our dealers have the right parts that they need and support. And I think that understanding our customers’ needs is how we think about it. So, Parts is really a transportation solutions provider, which makes them the go-to source for customers. And we think we’re the leader in that space, and that helps us grow the business through all parts of the coming years.

In Q2 Paccar's after tax return on invested capital was a considerable 35%, up from 22% in the same period last year. Given the strong year and a better management of working capital, Q3 should be at least in line with this result.

As usual, Paccar carries no manufacturing debt and I am not expecting any in the upcoming report.

Considering these numbers, as said, I am expecting a top-line around $8.3 billion. Since Paccar has not been repurchasing its shares in the past quarters, as we can see from its balance sheet history on Seeking Alpha, we can expect the number of outstanding shares to be still at 522 million.

Assuming a net income margin of 13%, we should have $1.08 billion in net income. Dividing it by the number of outstanding shares, I am expecting EPS of $2.06. The current consensus sees Q3 EPS come in at $2.12, a bit above my estimate.

Valuation

Paccar currently trades at a fwd PE of 11.4, and a fwd EV/EBITDA of 10.7. According to Seeking Alpha Quant Grades, its valuation is rated with a C+. This goes along with a C as its growth grade and an A in profitability.

Seeking Alpha

Now, I believe these multiples to be fair. In fact, compared to the general market, Paccar trades at a discount. But so do its peers. In fact, the market has always discounted this industry because of its cyclicality and its lack of recurring revenue. Of course, Paccar has built an outstanding spare parts business line that partially offsets these issues. However, the recent bid up in price has made the stock come close to its fair value, which is in the range between $80 and $90.

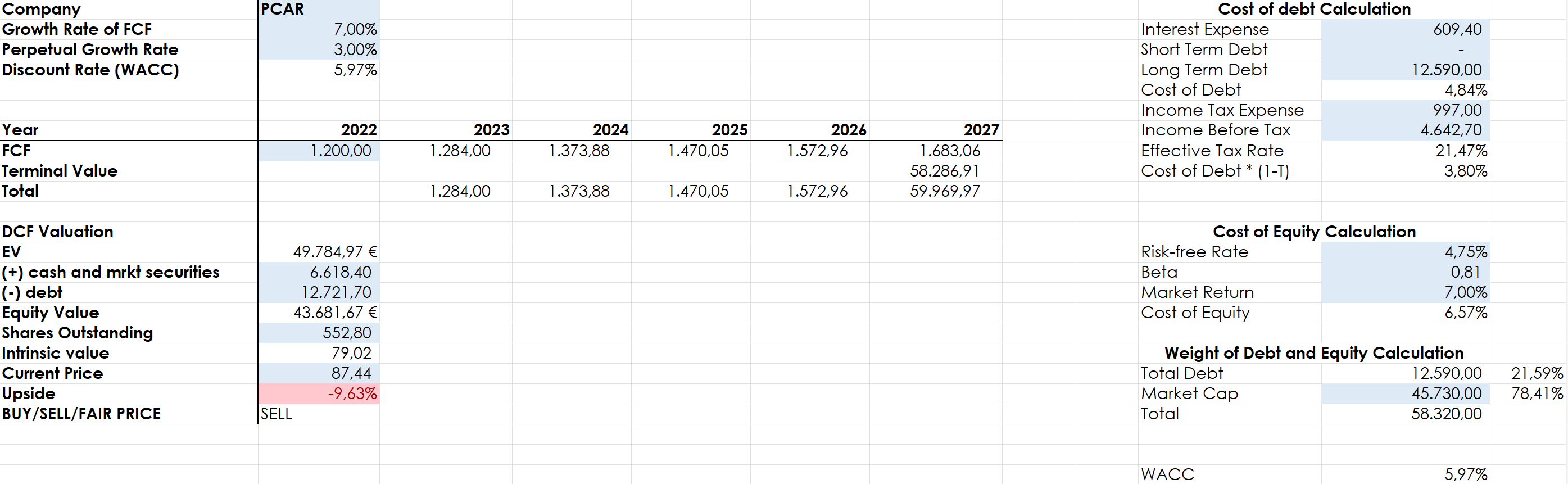

I got this value through my discounted cash flow model. Here, I assumed Paccar will be able to grow its FCF by 7% for the next five years. The reason to expect this comes from its spare parts business growth, which, as we have seen, is growing fast. Of course, this year Paccar is achieving higher-than-expected margins and this will probably impact positively its FCF. Yet, since 2023 is nearing to its close together with its exceptional results in sales, I am not willing to bake in higher FCF expectations. As things normalize and the economy slows down, Paccar will still need to fund its operations and to spend on capex, but it might see its net income flatten a bit, with a direct consequence on FCF.

As a perpetual growth rate I am using 3%. Some may think this is too high and that I should use 2%, in line with the expected inflation. Yet, are we so sure inflation will return to 2%? I actually expect inflation to stay around 3% for some time.

As the risk-free rate I used the 10 year treasury (4.75%) and to calculate the cost of equity I used an expected market return of 7%, more or less in line with the long-term yearly return we can expect from the S&P500.

Running these assumptions into the model, the intrinsic value comes in at $79. Considering the quality of this industry leader, we can award it a 10% premium, which positions the fair price in the range said above.

{kind=link}

Now, if Paccar reports a big beat (10% or more above my estimates) we will need to revise this model, assuming an increased FCF generation for the year. Currently, Paccar's FCF conversion rate is around 33%. So, if net income comes in for the quarter well above $1 billion, we might end Q3 with $330 million in FCF. This could make as think that the company will reach a yearly net income around $4 billion, which translate into an EPS of $7.66, assuming no reduction is share count. Clearly, I am not totally aligned with the current consensus, which sees CSX EPS come in at $8.59 per share. If FCF goes up 10% as well, then my new fair price becomes $88, which is exactly the current price the stock is trading at.

A big surprise could be also to the downside. Here, there might be some risks for investors. In fact, depending on how big of a surprise we will be talking about, the stock could trade down a bit after the current surge. However, if a miss will come, it should be very slight. In fact, the company is organically in good shape and the only hit could actually come from slower sales, which should not be the case in Q3. My model is more sensitive to this event, since I had to bake in a way to award Paccar a premium. If in 2023 FCF comes in, for whatever reason, 10% lower than expected, then the new intrinsic value would be $70, showing how almost no margin of safety is currently baked in the share price.

Paccar is a great company with a superb balance sheet and very healthy economics and financials. Yet, I would not buy the stock near ATHs because there is not a large enough margin of safety. I would suggest adding on any weakness that brings the stock back into the low $70s.

For further details see:

Paccar: Q3 Earnings Preview Of An Industry Leader