PCAR - Paccar: Slightly Expensive If Margins Don't Improve Significantly

2023-04-19 11:03:13 ET

Summary

- Great Paccar Inc FY22 results show pent-up demand in many regions.

- Paccar stock seems to be cheap in P/E terms, however, digging in further, the lack of margin expansion makes the company slightly overpriced currently.

- The Paccar balance sheet is strong to withstand a slight economic downturn.

- An optimistic, yet conservative, discounted cash flow model with good revenue increases over the next decade and margin expansions suggests Paccar is still too expensive.

Investment Thesis

Paccar Inc ( PCAR ) recently reported Q4 and full-year results that beat estimates. With around 13x earnings, I wanted to see if the company could be a good long-term investment at these prices. Digging further into the company’s growth prospects and margin expansions, the company, according to a conservative discounted cash flow ("DCF") model is slightly overvalued currently, and I would wait for the company to come back down, as I would like to see some substantial margin improvements in the upcoming quarters.

Even with a decent growth assumption, and some margin expansion over the next decade, the company is still trading at a premium, and I would wait for the company to come back down slightly before looking into initiating a position.

Briefly on FY22 Results

Total revenues were up around 23% y-o-y to $28.8B. EBIT increased by 59% while net income was 61% y-o-y. Gross margins also saw an increase from the previous year, mostly due to the company's higher-margin Parts segment.

Overall, very good results I thought, and maybe the company is a good investment. However, when I went deeper into the company’s financials, I saw something that isn’t very attractive right now, and that is the company’s margin situation. Furthermore, the upcoming slowdown of the global economies predicted may weigh on the company’s revenue growth in the short run. So, let’s talk about those.

Outlook

Paccar Inc management still projects strong growth in the U.S. for the first quarter of ’23 and a modest expansion in the U.S. economy overall for the whole year. That is a good sign for the company's growth prospects because, in the last 3 years, there has been a lot of pent-up demand for their new trucks because of COVID restrictions. Customers right now are still wanting to replace their old fleets with the newer and much more superior Kenworth and Peterbilt trucks that are currently on the market.

This pent-up demand will help the company to avoid a decrease in revenues for the periods that economists are predicting we are going to see an economic downturn. All the regions the company serves are showing pent-up demand for the trucks, so, in terms of revenue growth, I don't see an issue here. My issues come from the lack of margin improvements.

Over the last 5 years, the company's gross margins according to my model have ranged from 16.6% to 18.8%. As of the most recent annual report, the company's gross margin was sitting at 18.1%, which is an improvement from the prior year of about 150bps. That is great, however, it doesn't look like it is enough of an improvement to warrant the stock price in my opinion even if Paccar Inc is trading at around 13x earnings.

If we do see some downturn in the economies, I would guess the demand for the trucks will fall as customers decide to push back these purchases because either they are waiting for the prices or interest rates on loans to come down. The Fed and the European Union are still hiking interest rates because inflation is not where they want it to be. Revenue might decrease or come in flat for those tough times, but it is hard to tell right now as it’s already mid-April and we haven't seen anything developing in terms of that downturn, with markets rallying for a while now as has the company’s stock, which is up over 11% YTD.

Financials

The Paccar Inc outlook is a bit of a mixed bag in my opinion. Let’s check what the balance sheet looks like. Maybe it’ll show me why the company has been performing so strongly over the last year.

The company had around $6.3B in cash and short-term investments on the books as of Dec 31 st ’22. These do not cover the long-term debt, which stood at $8.2B, however, it doesn't seem to me that the leverage the company has would be worrying, because EBIT and cash from operations more than cover the interest expense.

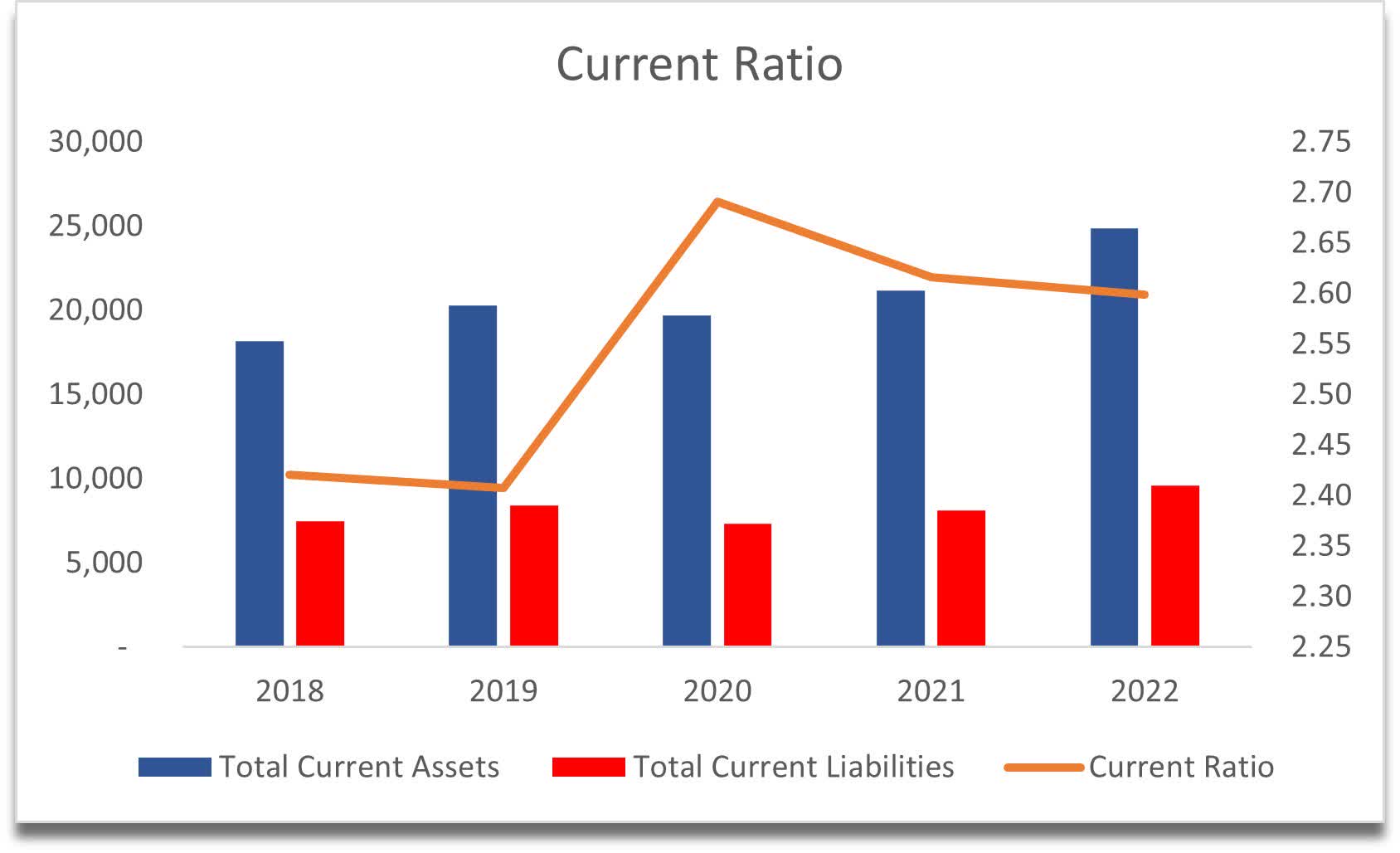

In terms of other liquidity metrics, the company's current ratio is extremely healthy and has been at these levels for at least 5 years. The company can cover its short-term obligation 2.6 times over, which is above my threshold of at least 1.5-2.0.

{kind=link}

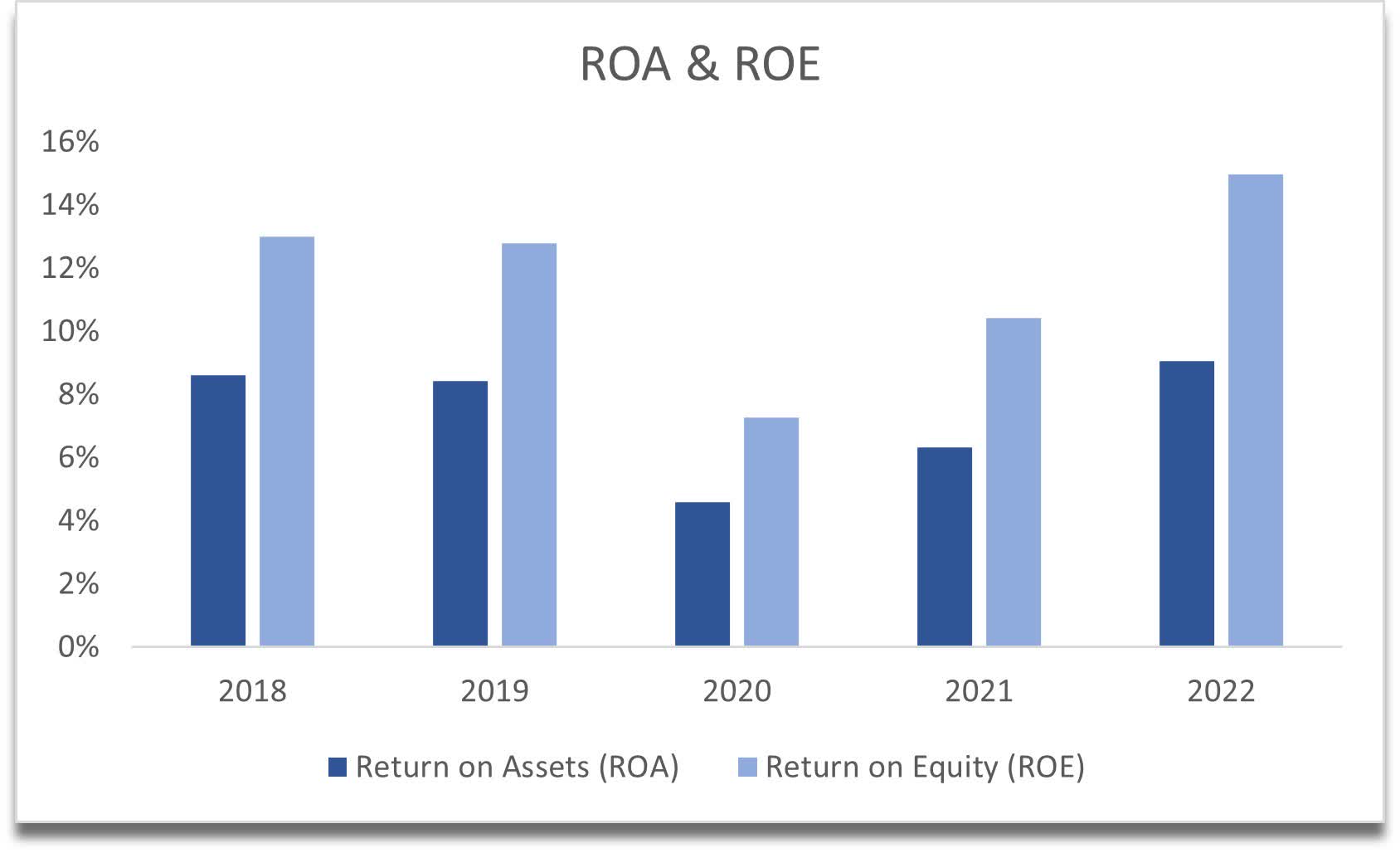

In terms of efficiency and profitability, the management's doing a decent job. ROE and ROA are decent, but nothing too outstanding. Nevertheless, they still have acceptable returns.

{kind=link}

The company’s ROIC is also pretty good, which shows that the Paccar Inc has a decent moat and some competitive advantage against its competition, currently at around 10%, which if compared to other companies is sitting somewhere in the middle.

ROIC vs Competitors (Seeking Alpha)

Overall, the balance sheet also provided a mixed bag of numbers. Some are good, some are not-so-great, but the company seems to be in good shape.

Valuation

In terms of revenue assumptions, I was thinking of implementing a decrease in revenues in '23 and a slight rebound in '24. However, I decided against that because of the pent-up demand for the trucks and because I wanted to be more optimistic, yet still conservative. My reasoning for that is I don't think the company would achieve very high revenue growth which could push its valuation over what it currently trades, without improving its margins significantly.

For the base case, I went with 15% in '23 and '24 revenue growth. After that, the company will see linear revenue decline to around 4% by '32. These assumptions turn FY22 revenues from $28.8B to $70.3B, which is quite an increase in my opinion. The growth of the revenues for the model is around 9% per year on average.

For the conservative case, I went with 200bps worse in every period in the model, and vice versa for the optimistic case.

The revenue assumptions will have some effect on the valuation of the company; however, the valuation will be much lower than what the company trades at currently if it cannot improve its gross margins significantly. I decided to be a little more optimistic for this analysis because recently my models included a downturn in the economy, however, we haven’t seen anything substantial yet so I will model that the margins will improve over the next decade by around 300bps, which I think is more than optimistic as the company has not seen such an improvement in at least 5 years.

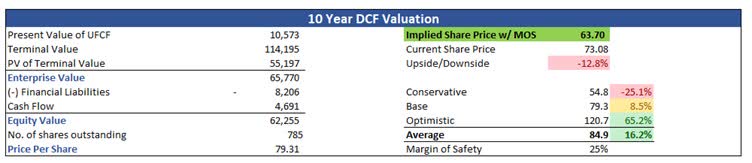

Since Paccar Inc does have a decent balance sheet, I will include a 25% margin of safety in my calculations, as I believe that is sufficient for this company and that is the minimum I would like to use. With that said, the company’s implied intrinsic value is $63.70, which means there is around a 13% downside to current valuations.

{kind=link}

Closing Comments

Paccar Inc has seen a decent rise in its share price, which I believe doesn't reflect the upcoming downturn in the economy. The share price is slightly over what I believe the company is worth right now and, in my opinion, is due for a correction in the next couple of quarters. Personally, I would like to see Paccar Inc coming back below 60, as I believe then the company has a decent risk/reward ratio.

Even with what I believe is decent revenue growth over the next decade, Paccar Inc is overvalued currently if it cannot improve gross margins in a significant manner.

I think volatility will persist in the markets and will bring a better entry point for the long-term, patient investor, as I do believe Paccar Inc is a good candidate for a long-term hold once it comes down a bit more in my opinion.

For further details see:

Paccar: Slightly Expensive If Margins Don't Improve Significantly