PPBI - Pacific Premier Bancorp: CRE Overexposure But Currently The Situation Is Stable

2023-08-14 17:58:52 ET

Summary

- Pacific Premier's stock is far from its 5-year-high, with concerns about its loan portfolio and high concentration ratio.

- The bank is holding more cash than historical levels to increase financial flexibility and cover unexpected expenses.

- The bank has slowed its loan growth because of competition from peers.

Despite the recent uptick driven by increased confidence in the banking sector, Pacific Premier ( PPBI ) is still far from its 5-year high of $47 per share. Concerns about this bank's loan portfolio persist, but at the same time NIM remains high, albeit declining.

Overall, Q2 2023 was rather positive, but the concentration ratio is above the precautionary threshold. On the doorstep of a potential recession, this may make Pacific Premier's future less rosy.

Loans and liquidity

Although the bank failures of SVB and First Republic Bank are behind us, Pacific Premier is still keeping its guard up about any new issues that may plague the banking sector in the future. For this reason, management is working to make the financial structure more flexible by holding more cash than historical levels.

Pacific Premier Q2 2023

Compared to last year, cash accounts for 7.1% of total assets, about $1.46 billion. Adding this figure to the unused borrowing capacity of $8.52 billion, Pacific Premier is able to cover 1.9 times its uninsured and uncollateralized deposits.

This liquidity will be used to cover any unexpected expenses or to take advantage of new investment opportunities. In any case, regarding the latter, at the moment CEO Steven Gardner expressed his concerns during the conference call about new lending:

I think as we've started to see a bit more stabilization in the deposit market, that we're becoming incrementally more comfortable around lending, but it's got to have the kind of returns that we expect. And frankly, we just haven't seen that at this point, given that there are some lenders out there that are still lending at what we consider just unacceptable risk-adjusted rates. So we'll see how it plays out.

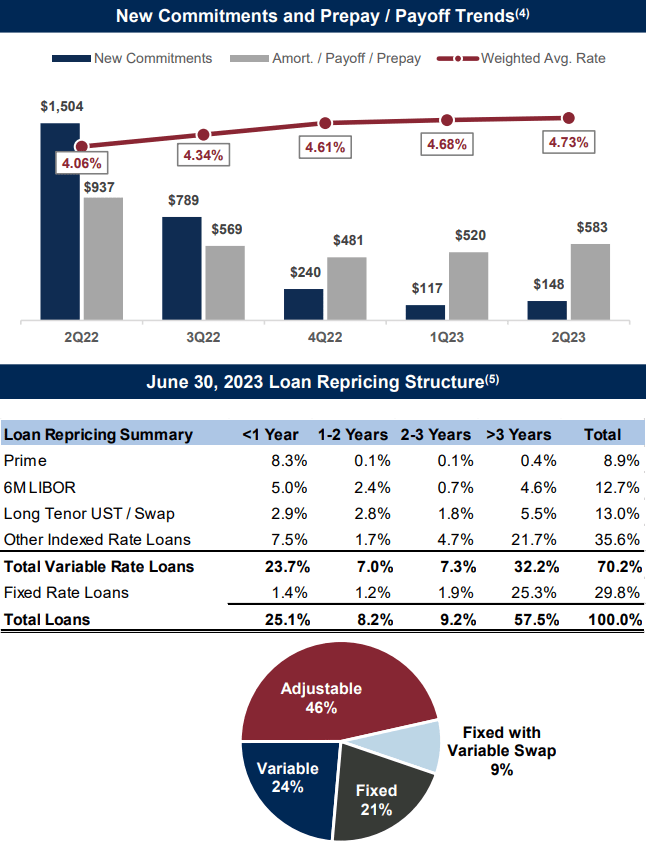

Basically, it would appear that there are some banks willing to offer loans at an interest that is not commensurate with the degree of risk taken, and this makes issuing new loans rather complicated for Pacific Premier. Management wants to issue new loans, but at interest rates that are not competitive for the time being. As a result, considering the maturity and amortization of previously issued loans, the overall effect is a reduction in the loan portfolio as a whole.

{kind=link}

Pacific Premier Q2 2023

Since Q4 2022, new commitments fail to exceed payoffs and amortization.

At the moment, this situation is not a problem in my view, as priority is simply being given to a more flexible financial structure rather than lending at questionable interest rates. As we will see later, this bank cannot even afford to make risky loans since its CRE concentration ratio is already far too high.

In addition, since 25.1% of loans will be subject to repricing within 12 months, Pacific Premier could increase its yield on loans without necessarily making new ones. Let us now come to the crucial point.

{kind=link}

Pacific Premier Q2 2023

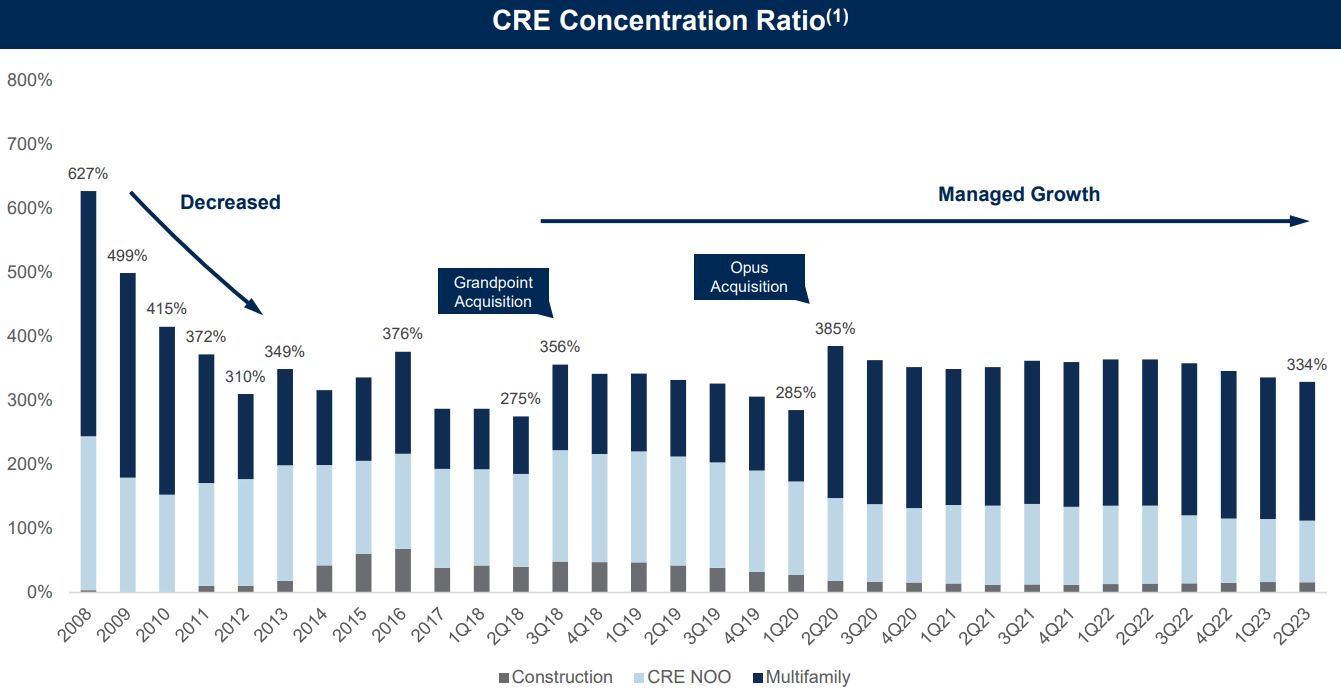

The CRE concentration ratio is above 300%, the maximum threshold set by the supervisory authority. It is possible to exceed it, as indeed has been the case in recent years, however one faces a more stringent set of controls as the bank in question may not have enough funds should a large portion of CRE loans default.

The largest component is multifamily loans, which account for 42% of total loans. This is a huge exposure, where the weighted average loan-to-value is 59%.

Such overexposure is certainly a risk, but at the moment the situation remains stable since Pacific Premier is both well capitalized and very careful about the deterioration of its loans.

{kind=link}

Pacific Premier Q2 2023

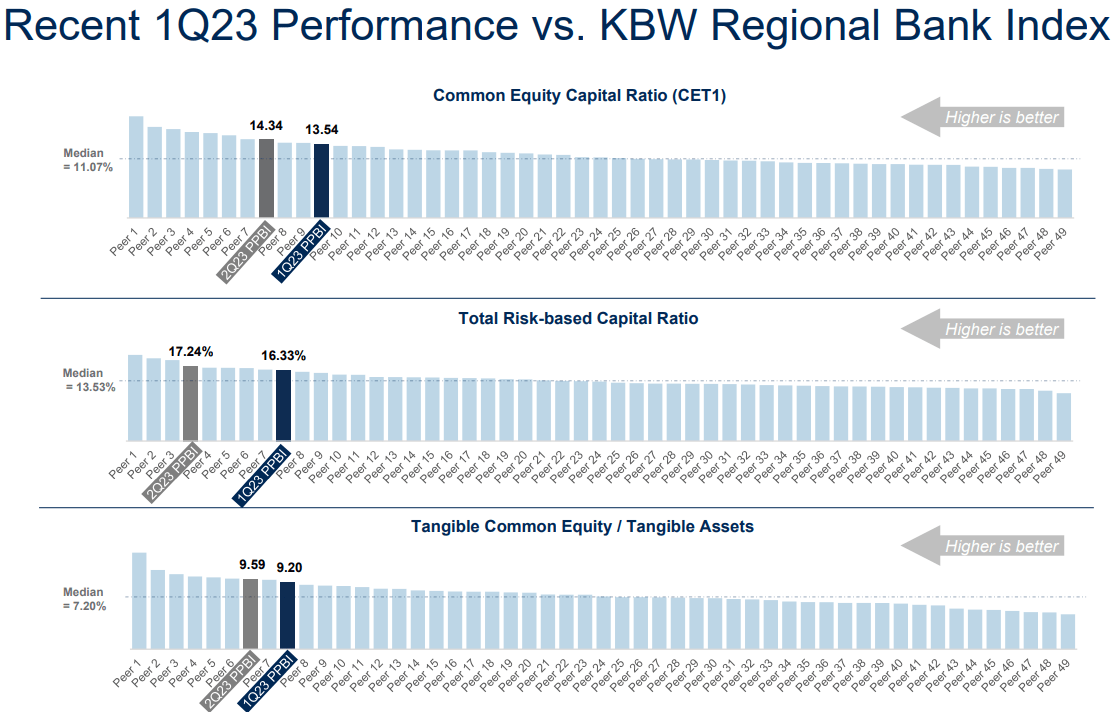

Compared to its peers, this bank has a CET1 well above the median of 11.07%, and the same is also true for Total-Risk based Capital Ratio and TCE/Tangible Assets. A similar argument can be made with non-performing assets.

{kind=link}

Pacific Premier Q2 2023

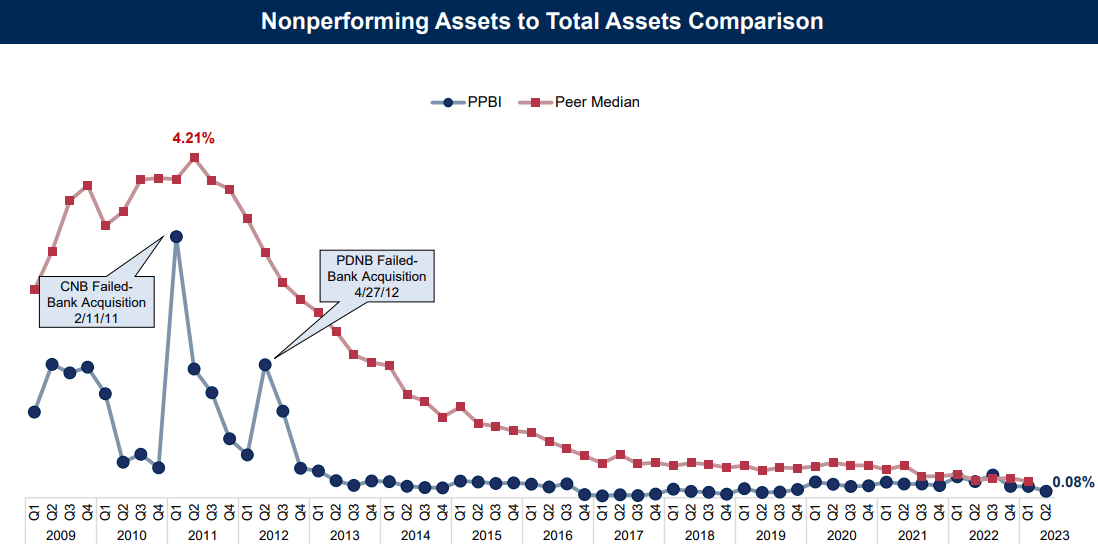

Historically, Pacific Premier has almost always performed better than peers in this area, and today the NPAs/Total Assets is only 0.08%. In other words, overexposure to CRE loans is evident, but default levels are at historic lows.

Anyway, although the situation is stable for the time being, I always remain doubtful about banks with such a high CRE concentration ratio. In the event of a recession, it is very unlikely that this bank will perform better than the market; indeed, I would not be surprised if it were to fall significantly.

{kind=link}

TradingView

During the subprime mortgage crisis the CRE concentration ratio was even over 600% and the collapse of Pacific Premier was catastrophic. Today this ratio is about half that, and continuing new banking regulations are increasingly pushing for better capitalization levels, yet one can never completely rule out banking risk. Frankly, in the event of a major recession, I would not be comfortable having a bank with these characteristics in my portfolio: it does not reflect my risk aversion criteria.

Deposits and margins

The cost of deposits is the sore point for many banks in the current macroeconomic environment, since money market rates are much more attractive than one year ago. Banks have been forced to give a higher yield on their deposits in order to retain customers, and this is negatively affecting NIM.

{kind=link}

Pacific Premier Q2 2023

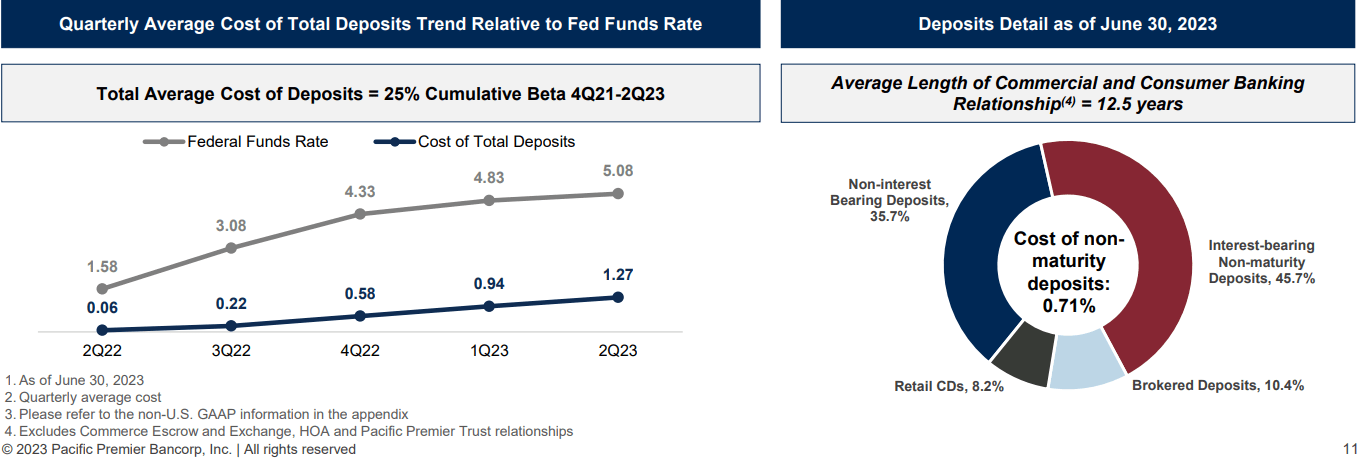

In the case of Pacific Premier, the increase in the cost of total deposits has been there, but not so evident compared to the Fed Funds Rate: as of today it is 1.27%. Moreover, as much as 35.70% of total deposits are non-interest bearing deposits.

{kind=link}

Pacific Premier Q2 2023

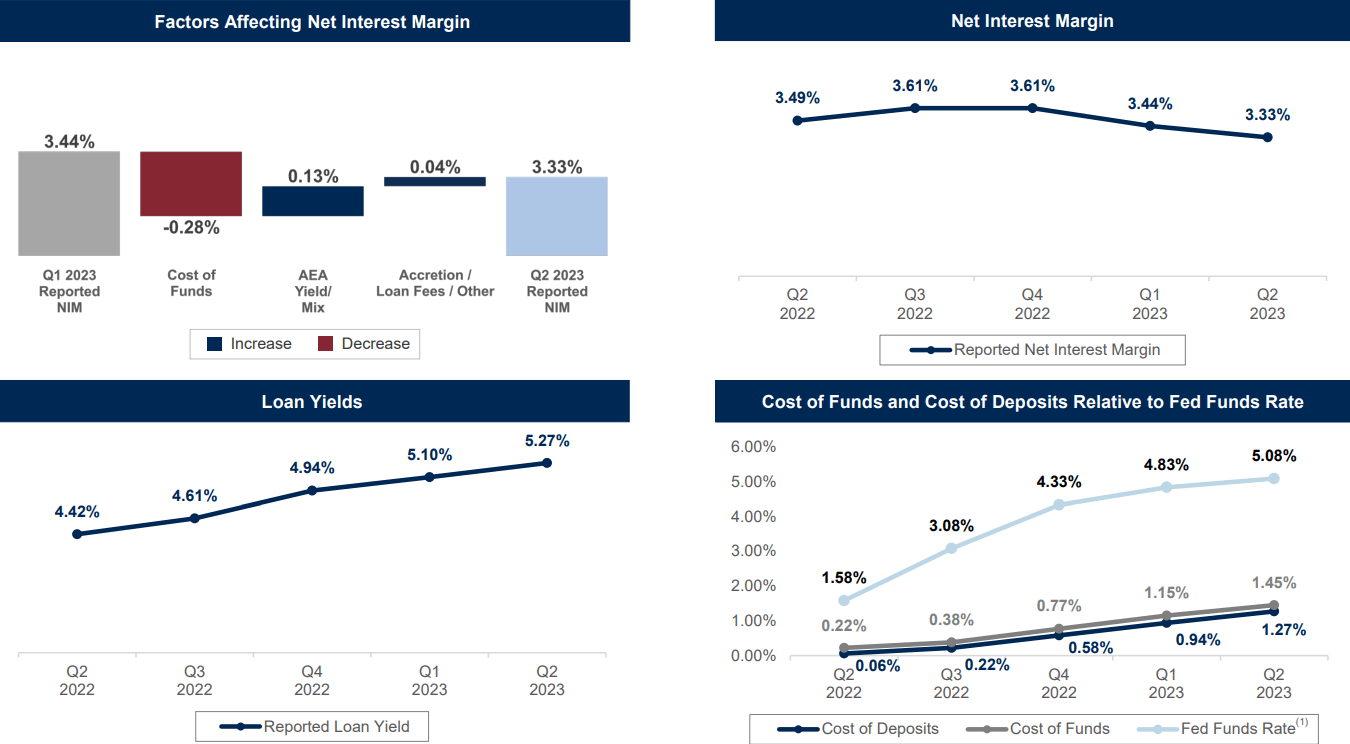

Higher interest on deposits necessarily means downward pressure on NIM, and in fact the current 3.33% is the lowest figure since Q2 2022. The loan yield has increased quarter by quarter, but not at the same pace as the cost of funds. In any case, it remains a good net interest margin that is not far off from that achieved in a much easier economic environment than the current one.

Finally, regarding the dividend, in my opinion the current dividend yield of 5.27% is sustainable. EPS ((TTM)) is $2.80 while the dividend per share is not even half that, only $1.32. Should the CRE loan segment begin to show signs of deterioration, the dividend could be cut, but as of today there is no reason to think so.

Conclusion

Pacific Premier is a bank with quality deposits and a fairly high net interest margin. The current dividend yield above 5% provides shareholders with good dividend income and given the low Price/Book Value of 0.84x, I would not be surprised if this bank's rally continues.

The main concern is the CRE concentration ratio above 300% even though the bank is well capitalized now. The loan portfolio is not sufficiently diversified and in the event of a recession this bank could suffer much more than its peers. For those who are positive about the future of the U.S. economy, the overexposure to CRE loans might not be a problem after all; but for those who are more pessimistic, this might be a plausible reason to avoid investing in Pacific Premier. Personally, I belong to the second category, so I do not consider this bank a buy despite its valuation multiples being at a discount.

For further details see:

Pacific Premier Bancorp: CRE Overexposure But Currently The Situation Is Stable