PPBI - Pacific Premier Bancorp: Over 7% Dividend Yield But Risks Are Too High

2023-05-15 13:17:20 ET

Summary

- Both the loan balance and the net interest margin will likely remain somewhat stable for the remainder of the year following poor performance in the first quarter.

- PPBI is currently offering a dividend yield of 7.4%. The dividend appears secure.

- The risk level is high mostly because of California markets.

Earnings of Pacific Premier Bancorp, Inc. ( PPBI ) will most likely dip this year because both the average loan balance and the average margin will be lower this year relative to last year. I’m expecting the company to report earnings of $2.56 per share for 2023, down 14% year-over-year. The year-end target price suggests a very high upside from the current market price. Further, Pacific Premier is offering a very high dividend yield of over 7%. Unfortunately, the company’s risk level is also high. Considering these factors, I’m adopting a Buy rating on Pacific Premier Bancorp.

Loan Trend Likely to Turn Positive but Remain Close to Zero

The declining loan trend that started in the third quarter of 2022 worsened during the first quarter of 2023. The loan portfolio declined by 3.5% during the first quarter as originations were unable to keep up with pay downs and payoffs. There is another $1.3 billion of scheduled loan paydowns for the last three quarters of 2023, as mentioned in the conference call. To put this number in perspective, $1.3 billion is a sizable 9% of total loans outstanding at the end of March 2023. Therefore, these paydowns will continue to exert pressure on the total loan portfolio size.

Further, funding constraints amid a declining deposit trend can also restrict loan growth. Pacific Premier is headquartered in California, which has seen deposit runs that tanked SVB Financial ( SIVBQ ) and First Republic Bank ( FRCB ). Pacific Premier’s deposit decline was quite small during the first quarter, so I’m not worried that it will experience a full-fledged deposit run. However, it’s likely that deposit growth will remain under pressure, which will also hurt loan growth.

Moreover, the higher costs for borrowers amid the rising-rate environment will dampen credit demand in Pacific Premier Bancorp’s markets.

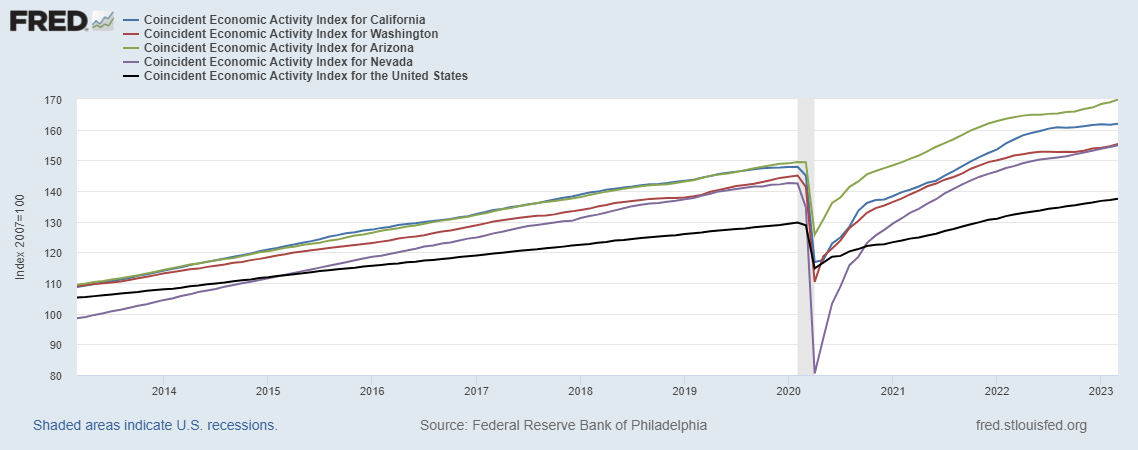

Nevertheless, I’m hopeful the declining loan trend will turn around because of strength in local markets. Pacific Premier operates in major metropolitan markets of California, Washington, Arizona, and Nevada. With the exception of California, all of the states Pacific Premier Bancorp operates in currently have steeper trend lines for economic activity than the national average.

{kind=link}

Considering these factors, I’m expecting the loan portfolio to grow by 0.5% in each of the last three quarters of 2023, leading to a full-year loan decline of 2%. The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 393 |

| 447 |

| 574 |

| 662 |

| 697 |

| 674 |

| Provision for loan losses |

| 8 |

| 6 |

| 192 |

| (71) |

| 5 |

| 8 |

| Non-interest income |

| 31 |

| 35 |

| 71 |

| 108 |

| 89 |

| 82 |

| Non-interest expense |

| 250 |

| 259 |

| 381 |

| 380 |

| 397 |

| 418 |

| Net income - Common Sh. |

| 123 |

| 160 |

| 60 |

| 336 |

| 280 |

| 241 |

| EPS - Diluted ($) |

| 2.26 |

| 2.60 |

| 0.75 |

| 3.58 |

| 2.98 |

| 2.56 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD million unless otherwise specified) |

Risks Appear High Due to the Location

The biggest source of risk for Pacific Premier Bancorp is its California location. The three U.S. banks that have failed so far, SVB Financial, First Republic Bank, and Signature Bank ( SBNY ), all had sizable exposure to California markets. The deposit runs that plagued SIVBQ and FRCB could also potentially spread to other banks in the area, including Pacific Premier Bancorp.

Apart from the contagion risk, the company’s risk level is satisfactory. Unlike other banks, Pacific Premier has NOT racked up large unrealized mark-to-market losses on its Available-for-Sale securities portfolio amid the rising rate environment. Gross unrealized losses totaled $253 million at the end of March 2023, which is around 9% of total equity. As 9% is a manageable level, these losses are not worrisome.

Moreover, uninsured and uncollateralized deposits made up 35% of total deposits at the end of March 2023, which isn’t too bad.

Overall, I believe Pacific Premier Bancorp’s risk level is high.

Dividend Yield of 7.4%, Over 27% Upside

Pacific Premier Bancorp’s stock price has plunged by 41% since March 8, 2023, when the Silvergate Capital ( SICP ) case sent ripples of panic across the banking sector. As a result of the price rout, Pacific Premier is now offering a very high dividend yield of 7.4% at the current quarterly dividend rate of $0.33 per share. The earnings estimate and current dividend imply a payout ratio of 52% for 2023, which is above the four-year (ex-2020) average of 42%, but still easily manageable. Therefore, I think the dividend is secure despite the earnings outlook.

I’m using the peer average price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value Pacific Premier Bancorp. Peers are trading at an average P/TB ratio of 1.30 and an average P/E ratio of 7.79, as shown below.

| PPBI |

| FFBC |

| WAFD |

| AUB |

| PRK |

| FULT |

| Peer Average |

| TBVPS - Dec 2023 ($) |

| 19.8 |

| 19.8 |

| 19.8 |

| 19.8 |

| 19.8 |

| Target Price ($) |

| 21.8 |

| 23.7 |

| 25.7 |

| 27.7 |

| 29.7 |

| Market Price ($) |

| 17.9 |

| 17.9 |

| 17.9 |

| 17.9 |

| 17.9 |

| Upside/(Downside) |

| 21.6% |

| 32.7% |

| 43.8% |

| 54.8% |

| 65.9% |

| Source: Author's Estimates |

Multiplying the average P/E multiple with the forecast earnings per share of $2.56 gives a target price of $19.90 for the end of 2023. This price target implies an 11.3% upside from the May 12 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple |

| 5.8x |

| 6.8x |

| 7.8x |

| 8.8x |

| 9.8x |

| EPS 2023 ($) |

| 2.56 |

| 2.56 |

| 2.56 |

| 2.56 |

| 2.56 |

| Target Price ($) |

| 14.8 |

| 17.4 |

| 19.9 |

| 22.5 |

| 25.0 |

| Market Price ($) |

| 17.9 |

| 17.9 |

| 17.9 |

| 17.9 |

| 17.9 |

| Upside/(Downside) |

| (17.3)% |

| (3.0)% |

| 11.3% |

| 25.6% |

| 39.9% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $22.80 , which implies a 27.5% upside from the current market price. Adding the forward dividend yield gives a total expected return of 34.9%.

I normally adopt a Strong Buy rating when the total expected return is this high. However, due to the risk level, I believe a Buy rating is more appropriate. Moreover, because of the riskiness, I believe Pacific Premier Bancorp is unsuitable for risk averse investors.

For further details see:

Pacific Premier Bancorp: Over 7% Dividend Yield But Risks Are Too High