PCRX - Pacira BioSciences: Economic Returns Languish Required Growth Rates

2023-08-05 12:28:15 ET

Summary

- Pacira BioSciences posted mixed Q2 FY'23 earnings, with $34mm in quarterly FCF on $42mm pre-tax earnings.

- The company's EXPAREL unit sales were down YoY due to pricing issues from the 340B drug pricing program.

- Capital deployment and business returns are lagging, and the softer FY'23 outlook suggests challenges for future growth in my view.

- Net-net, reiterate hold.

Investment briefing

Pacira BioSciences, Inc. (NASDAQ: PCRX ) posted Q2 FY'23 earnings this week with a mixed set of numbers throughout the P&L and balance sheet. Notably, it pulled in ~$34mm in FCF on pre-tax earnings of $42mm, quite a reasonable conversion.

Picking apart the company's capital deployment, profitability, and incremental business returns, reveals there are visible headwinds to PCRX re-rating to the upside in my opinion. I won't waste too much time boring you with the details (you can read these extensively below), but the point is I continue to reiterate PCRX a hold from my last PCRX publication in May.

On my FY'23 assumptions, I estimate the market has the company's equity stock fairly valued as I write. Net-net, reiterate hold.

Figure 1.

{kind=link}

Q2 breakdown—clear headwinds remain

The critical takeouts from PCRX's latest numbers reveal visible headwinds to the company's growth plans. I'll discuss each of these below, but the point is we had expected to see better performance in the company's EXPAREL unit by now. Instead, it has languished, much like its stock price this YTD.

(1). Financials well behind schedule

It was a mixed quarter, no sugar coating it. PCRX pulled in revenues of $169.5mm—a whole $0.1mm on Q2 last year. There's a few key reasons for this.

One, EXPAREL sales were down ~$2mm YoY to $135m. What's concerning is it sold $2mm less on 400bps greater volume compared to this time last year. Principally, this is a pricing issue. The 340B drug pricing program is a challenging one for PCRX. It is a price reduction on drugs for regions and entities where opioid-related issues are most prolific. It was a 28% discount last quarter, and may or may-not reduce to 25% by yearend. Still, the risk is real for PCRX's top line, because its government tenders run with a two-quarter lag on any 340B changes. It added 350 first-time accounts in Q2 and this still wasn't enough to get on top of last year's numbers. Management didn't add any conviction on the call:

April was very soft...and actually, one of the worst months that we've seen in since the pandemic...I don't believe that there's any issues in the marketplace related to how we're being viewed. I think the marketplace continues to be financially strained, especially in the hospital marketplace. " —David Stack, Pacira BioSciences CEO

Aside from the EXPAREL saga, breakdown of the top-line was as follows:

- ZILRETTA sales came to $29.3mm and were up ~$2mm YoY. It now has ~200 reps in the field, leading to a quarterly revenue per rep pf $0.147mm. It pulled this to 82% gross, quite promising in my opinion.

- Iovera sales were up ~$1mm YoY as well to $4.4mm, but the company booked a $300K loss in its Bupiacaine segment.

It pulled these revenues to $24.5mm in operating income on earnings of $0.78 per share. Both of these numbers are up substantially but on weak comps from last year. Therefore, in my opinion, growth vertically down the P&L was weak for PCRX, and didn't evidence any reason to expect different into the medium-term either.

(2). Capital deployment at not so-attractive returns

Looking at the quarter briefly, PCRX disposed a portion of its available-for-sale marketable securities and realized ~$90mm in cash flow from this. It put ~$10mm of this to work towards its EXPAREL project in San Diego. Management said the facility is " now outperforming volume targets" and pulled in 76% gross during the 3-months. This is likely a testament to its 200-litre process, something I commented on at lengths in my last two PCRX publications. Hence, it is good to see this pulling through at the margin.

Business returns lagging market returns

Zooming out, the economic benefits to PCRX's capital deployment initiatives have yet to be realized these past 3 years. You'll note below [Figure 2] the company's return on existing capital from Q4 FY'20—Q2 FY'23 on a rolling TTM basis. It is titled "return on capital at risk".

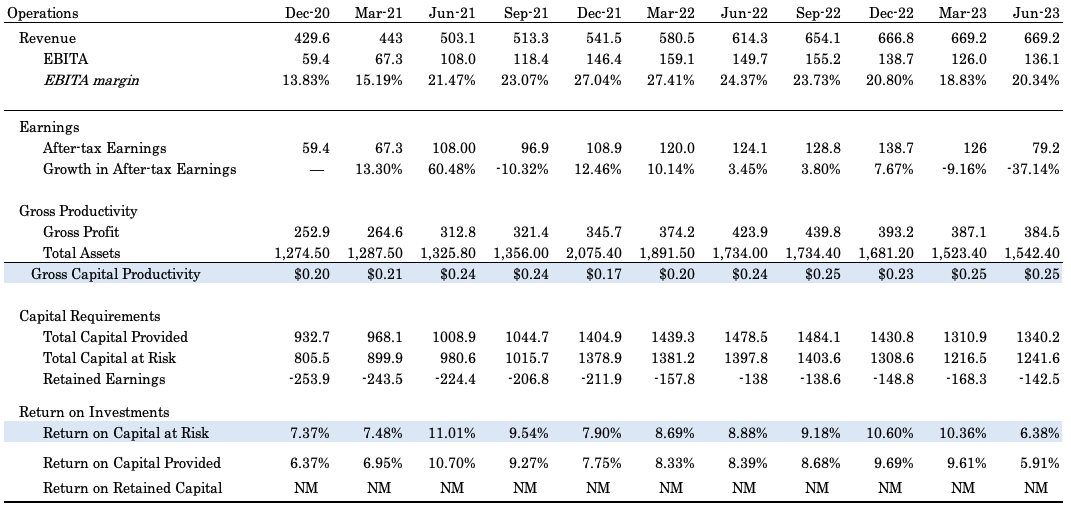

PCRX hasn't beaten the market return on capital (at 12% for the long-term average here) in any of these periods. Hence, the business returns on offer are well behind benchmark returns on capital, that investors could reasonably expect to receive without doing a thing (by simply riding the benchmark).

Figure 2.

Data: Author, PCRX SEC Filings

{kind=link}

It is essential to realize that, over time, market returns on any corporate equity security will typically mirror that corporation's business rates of return—i.e., their returns on existing and new capital deployed. Moreover, intelligent investors always consider the opportunity cost of any investment, thereby creating the 12% hurdle rate described earlier (I'd put it in the range of ~10—12%).

If a firm doesn't beat the market return on capital on its own business returns, it in no way creates value for its shareholders—no matter what the earnings growth was for that period. Growth can actually be destructive in that regard. You can see this in full action for PCRX in the series above and below [Figure 2 and Figure 3]. Note, despite the incremental growth in post-tax earnings, these weren't sufficiently above the opportunity cost of capital of 12%. The economic earnings— those profits above/below the hurdle rate—have been negative the entire testing period.

Several concerns I have from these statistics:

- Despite the growth in post-tax earnings, and, owner earnings throughout several periods [defined as NOPAT less reinvestment to growth capital], the economic earnings suggest that PCRX has added little to no shareholder value.

- This, due to the fact returns on incremental capital deployed to achieve said growth have languished, combined with returns on its existing capital base not meeting the hurdle rate.

- Moreover, at points where ROIC was high, the firm reinvested basically little to no additional capital to beef up the dollar returns.

- Similarly, in times when returns on capital were low, PCRX over-invested, thereby committing funds to risk without the adequate return.

These certainly aren't the hallmarks of a firm creating value for its shareholders in my opinion.

Figure 3.

Data: Author, PCRX SEC Filings

{kind=link}

By all measures, these trends look set to continue

Moreover, it would appear we can expect more of the same moving forward. For one, I mentioned the heavy investment into its 200-litre production capacities. This will continue into the near future, as confirmed by management.

Secondly, the cash and liquidity it has on hand, and likely, the additional profits to be generated this year, will be put towards retiring its term loan A and convertible issues that come due end of this month. This was confirmed on the call as well.

To me this confirms an already bleak picture:

- Sub-par returns on capital deployed (below the 12% hurdle rate benchmarked here);

- Earnings growth at the detriment to compounding shareholder value, therefore;

- The pattern of reinvestment trends to fuel intrinsic value are equally as bleak, suggesting that:

- There are either no additional high-return opportunities for the company to put money to work; or

- Its current growth programs do not offer the kind of reward to allocate more capital towards.

This language from the CFO adds weight to these assumptions:

As you know, Pacira leadership team is constantly assessing the best use of capital and ways to optimize our balance sheet. To that end, last week, we made a $25mm principal prepayment on the term loan A and we continue to fully expect our significant cash flow outlook will enable early retirement of the remaining term loan A balance of approximately $122mm. For modeling purposes that $25mm prepayment and will result in interest expense savings of roughly $1mm in the second half of the year."

Retiring debt is the best use of capital , really? That to me is a tad worrying. And it talks to the points I raised just above—that there appear to be no new profitable avenues of growth for PCRX. Why not buyback stock instead? Special dividend? Fold into existing operations? And so on. Again, this isn't the kind of economic features I want to position against.

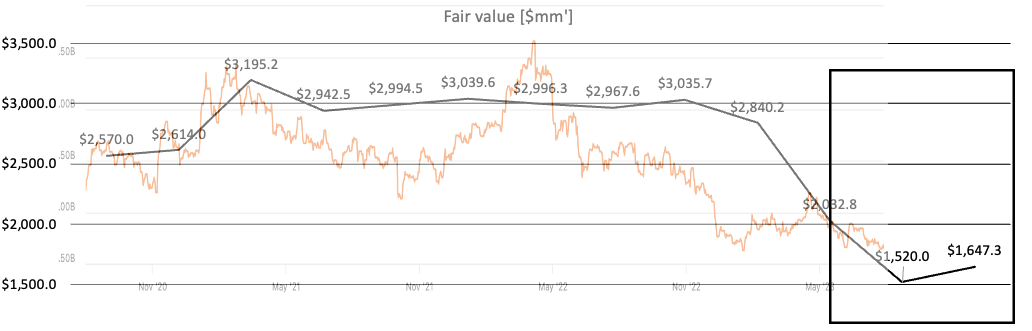

Either way, I don't see PCRX spiking back to its FY'21 highs based on what I've uncovered here, not in the medium-term, and, not relative to many of its peers. I would also opine that the market has PCRX around fairly valued as I write. You can see below, the implied intrinsic value of the firm from 2020. There have been periods of under/overvalued, but the latest economic performances have dragged this toward the floor.

Figure 4.

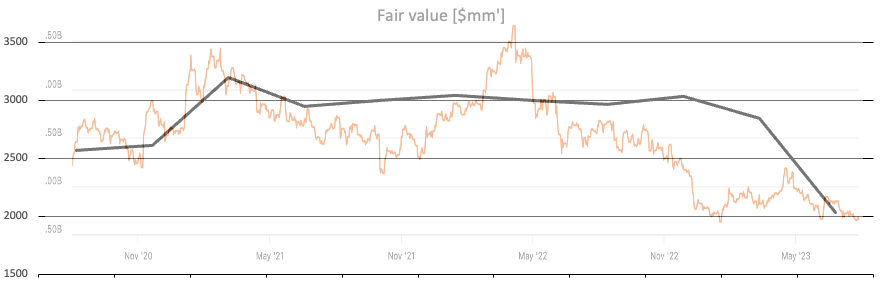

Note: The image is the market cap line [orange], retrieved from Seeking Alpha, superimposed over the implied intrinsic value line [black]. This is why the image is slightly faded.

Note: Implied intrinsic value assumptions calculated as the Return on incremental capital multiplied by the reinvestment rate, plus/minus the economic profits produced each period. Each are in TTM values. (Data: Seeking Alpha, Author)

{kind=link}

(3). Softer FY'23 outlook

Findings from section (2) above appear to be vindicated in the softer FY'23 outlook management detailed on the earnings call. It has reduced full-year guidance across all product lines.

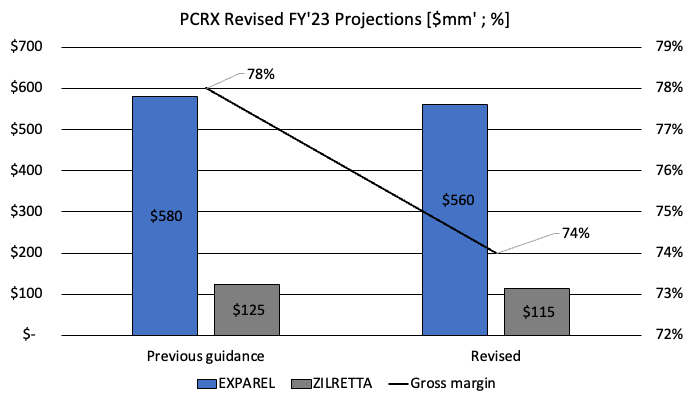

It now projects ~380bps growth at the top line, calling for $695mm at the upper end of range. This is down on previous estimates, and stems from downgrades across the entire portfolio. Specifically:

- EXPAREL projections revised down to $550mm—$560mm from $570mm—$580mm;

- ZILRETTA to $110mm—$115mm versus $115mm—$125mm;

- Iovera sales projected to reach $17—$20mm;

- Gross margin on these to ~74% from 76—78%.

The softer outlook is another challenge to PCRX repricing higher over the medium-term in my opinion. Obviously, the significant upside risk is that PCRX comes in with earnings that completely blow these estimates out of the water. On the bounce of probabilities, I am on the 'less than likely' side of this occurring.

Figure 5.

Data: PCRX Q2 FY'23 Press Release,

{kind=link}

Valuation and conclusion

Investors are selling PCRX at 12.7x forward earnings (38x GAAP earnings) and ~9.6x forward EBITDA. These are attractive numbers on a relative sense—37% and 29% below the sector, respectively.

Question is, why the discount? Is it justified, or do we have a mispricing on our hands? To answer, you've got to think in first principles:

- PCRX is pulling returns on its capital employed less than the hurdle rate.

- Thus, a lack of economic earnings and value-add. My assumptions have these trends to continue moving forward.

- Questionable capital budgeting, with no apparent avenues for growth capital to be deployed (free cash allocated to retiring debt instead).

- Softer FY'23 guidance (and potentially FY'24), with EXPAREL sales well behind where we expected them to be.

- Management's pessimism on the underlying market's outlook.

These are 5 points related to asset factors and earnings power that don't suggest PCRX deserves to trade near the sector multiple. In my opinion, the discount is therefore justified. Even using the sector multiple of 20x forward, I get to $1.46Bn in projected value, $31.7 per share. Compounding the company's implied market value at the function of my ROIC, reinvestment and economic profit assumptions, I get to $1.65Bn in intrinsic value by FY'23 yearend. This is below the current market value, and thus does not support a buy rating at this stage.

Figure 6.

Note: Refer to "Figure 4".

{kind=link}

Net-net, I continue to rate PCRX a hold for the reasons outlined in this report. With equity markets at the helm of macro-economic drivers, a higher cost of capital, more lucrative opportunities in income-producing assets and quality corporate securities, any buy rating must be accompanied by a robust set of economic characteristics. On my examination, that simply isn't the case for PCRX. There are visible challenges it must overcome in order to earn a spot within the risk budget of my equity holdings. The key upside risk is a strong earnings beat across H2 FY'23, as the company's equity stock has priced this not happening. As such, reiterate hold.

For further details see:

Pacira BioSciences: Economic Returns Languish Required Growth Rates