PCRX - Pacira BioSciences: More Evidence Needed To Advocate Entry At Current Valuations

Summary

- Reluctancy of management to provide forward estimates points to challenges in end-markets, and a key risk by estimation.

- Sequential sales growth looks to have stalled based on the monthly earnings releases, but we'll have to wait and see.

- Investor reaction to commentary on previous earnings resulted in violent selloff in PCRX equity at the back end of FY22.

- Net-net, there are too many unanswered questions at present, leading us to rate PCRX a hold.

Investment summary

Many healthcare and med-tech equities peaked in early FY22, setting up the stage for a broad-market selloff within these sectors. The pace of deceleration continued into the final stages of the year, leaving many equity investors having to pick up the pieces of their portfolios.

One case in point we'd allude investors to is Pacira BioSciences, Inc. (PCRX). Following its rapid selloff in Q4 FY22, we wanted to see if this presented as either an alpha or turnaround opportunity. After rigorous analysis of the available data, we believe there are more selective opportunities to allocate capital elsewhere. Hence, I'm here today to explain why we rate PCRX a hold, noting the company's reluctance to provide forward guidance, combined with unsupportive valuations. Net-net, we see PCRX fairly valued at $36 until the company can demonstrate its propensity to return former levels of growth.

PCRX equity selloff in the back end of FY22' was violent and resulted in shares diving to 2-year lows into the new year.

{kind=link}

Various headwinds observed in PCRX's latest numbers

We would start here by noting PCRX's Zilretta segment continues to be the main driver for growth and value creation for the company, in our opinion. As a reminder, Zilretta is a triamcinolone acetonide extended-release injectable suspension indicated for treating pain in osteoarthritis ("OA"). Third quarter sales for Zilretta reached $26.5mm, a decent contribution since the company started booking sales in this segment after its acquisition from Flexion Therapeutics in November of FY21'. Management also mentioned its intentions to expand Zilretta into adjacent markets by demonstrating its efficacy in priority population groups such as in diabetics. Turning to the November 2022 numbers , Zilretta generated net product sales of $10.0mm, ~38% of the Q3 total. It should be noted that a portion of Zilretta's sales in November 2021 occurred prior to PCRX's acquisition of Flexion in the same month, as mentioned.

Looking ahead, the company plans to initiate two label expansion studies for Zilretta this year, including one evaluating the drug's effectiveness in diabetics with knee OA in comparison to immediate-release triamcinolone acetonide, and another studying its use in shoulder OA. The study on Zilretta's use in shoulder OA, if successful, could make it the only approved corticosteroid for shoulder treatment specifically, so says management. The knee and shoulder studies are expected to be completed in H2 FY23' and the H2 FY24', respectively. The advantage of treating these areas with Zilretta, if successful, is that it would generate a higher reimbursement opportunity with the wider treatment application.

We'd also highlight that product sales for its Exparel label reached $46mm in November of 2022, a slight decrease from the $46.5mm in November of the previous year. Despite a stagnant market for surgical procedures, Exparel saw a 400bps increase in unit volumes compared to the same month in the previous year. However, the net selling price was lower due to the company's implementation of the 340B Drug Pricing program, but also the fact that several customers received a discount on purchase orders during the quarter. On this, the average daily sales for Exparel in November of 2022 were 99% of those in November of the previous year, [both months had 20 selling days].

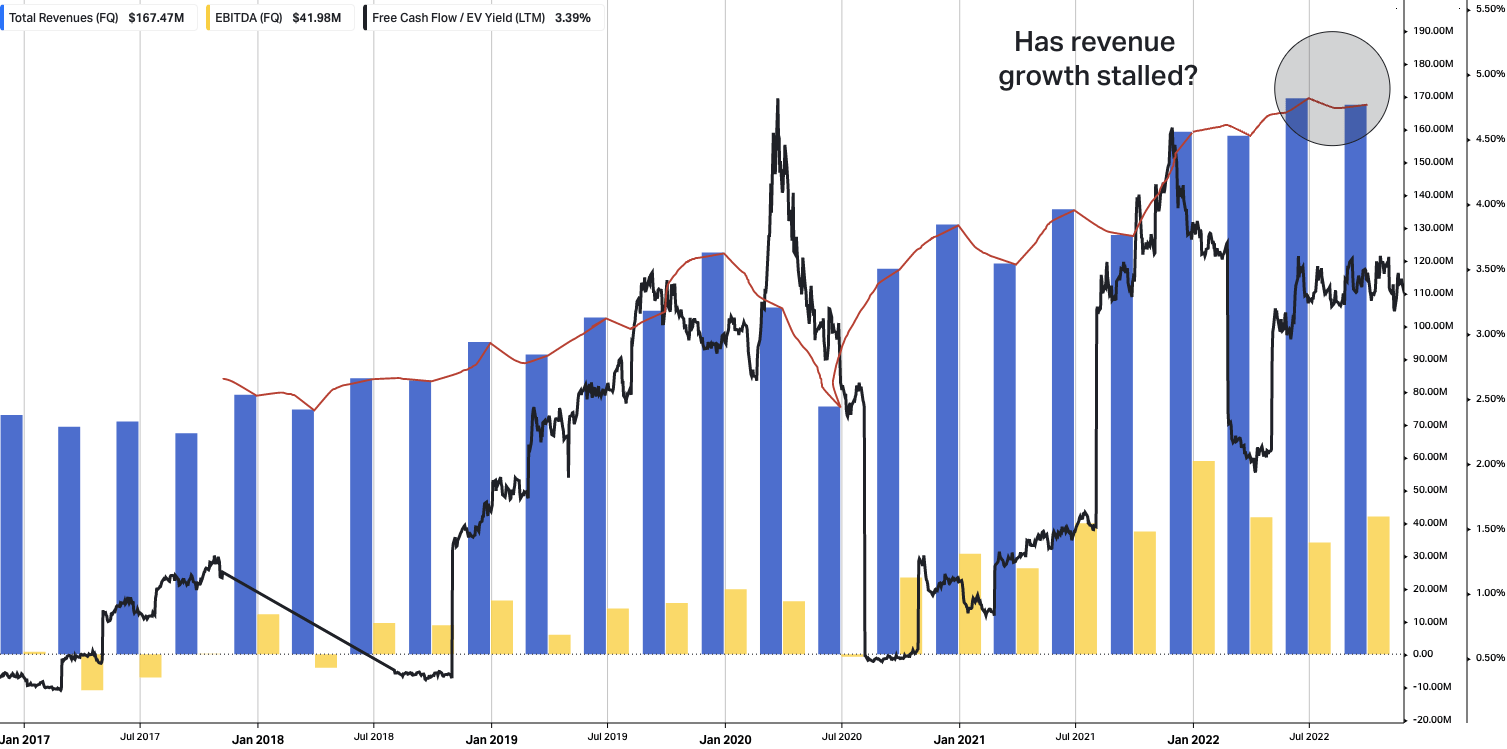

With the monthly earnings releases, revenue growth looks to have stalled on a sequential basis

Data: HBI, Refinitiv Datastream

{kind=link}

Meanwhile, the company's iovera ° ("iovera") net product sales for both November FY22' and November FY21' were $1.5mm. With the rollout of the 2nd generation device and the transition to this improved version underway, PCRX has baked in a steeper demand and growth curve for the coming 12 months. Its FY22 numbers will provide better clarity on this, by estimation.

The company also remains focused on growing the potential of iovera in new indications such as spasticity and medial branch blocks. In September, PCRX met with the FDA and gained clarity on the study design and pathway for approving iovera as a treatment for spasticity. If you weren't aware, spasticity is a manifestation of upper motor neuron dysfunction, characterized by an increase in muscle tone, reflexes, and resistance to passive movement. It has a clinical presentation that produces rapid onset of pulsating/intermittent muscle function, in response to velocity of movement.

Hence, it makes biomechanical functions [ambulation, upper limb movements] inherently difficult by impairing weight-bearing/anti-gravity musculature. It is commonly observed in individuals with central nervous system injuries or disorders, such as multiple sclerosis, spinal cord injury, stroke, or cerebral palsy. The severity of spasticity can range from mild to severe, with symptoms including difficulty with movements such as walking, writing, or grasping objects, as well as abnormal posturing or curvature of the spine. Thus, there's scope for PCRX to make a difference to this population group, should its iovera label pull through in efficacy testing in its upcoming study to launch early this year.

The study, which will compare iovera to a sham treatment in adult patients, is set to concluding enrollment by the end of the year to support a 510(k) marketing approval. It should be noted that the pain associated with spasticity is already on the label for iovera, so this would be an extended application of the compound should it convert successfully from the clinical trial.

Additionally, the company recently finalized enrollment in another iovera study examining its use to treat low back pain, with plans to report data and launch its new Smart Tips segment sometime in FY23.

No guidance secondary to "continued market uncertainties"

PCRX management declined to provide full-year guidance on the last call, opting to provide monthly revenue updates instead. It said this was due to "continued market uncertainties". Specifically, quoting from the latest press release from its November FY22 update:

"The company is not providing 2022 revenue or gross margin guidance at this time given the continued uncertainty around labor shortages, COVID-19, and the pace of recovery for the elective surgery market. To provide greater transparency, the company is reporting monthly intra-quarter unaudited net product sales for Exparel, Zilretta, and iovera until it has gained enough visibility around the impacts of COVID-19."

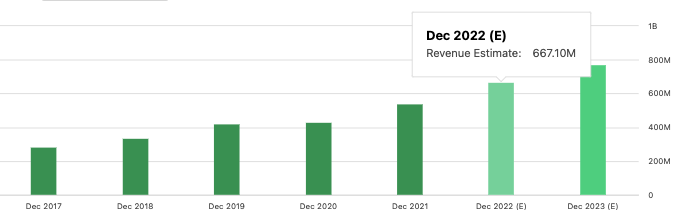

You'll see in Exhibit 1 that consensus has PCRX to print $667mm in FY22 revenue, calling for 23.2% YoY growth at the top-line. This would be a steady ramp from the previous year, hence, the numbers PCRX prints for FY22 are sure to be a key inflection point for investors to benchmark against the consensus estimates.

Further from the above, whilst revenue upsides are forecast for the full-year, this doesn't appear to carry through to the bottom-line. Broker analyst forecasts for PCRX's FY22 EPS [non-GAAP] pull to $2.60, down from a $3 actual the year prior. This is a key risk for the stock re-rating to the downside in the first half of FY23, by estimation. Especially when the macro pressures continue to mount for U.S. equities, with a higher cost of capital and therefore discount rate. It also sets the stage for PCRX to surprise to the upside come FY22 earnings, which could see its stock catch a bid.

Exhibit 1. PCRX consensus revenue estimates, FY22-FY23

Data: Seeking Alpha PCRX quote page, see "Revenue".

{kind=link}

Valuation and conclusion

There are mixed results when looking at PCRX's factors of corporate and equity value. First, the stock trades at 14.5x forward earnings [non-GAAP], which is a respective 23% discount to the sector and 60% off its 5-year average. This corresponds to ~14x trailing earnings, similar discounts as listed above. Those hunting for a bargain might be interested here.

However, the forward 14.5x multiple is also below the S&P 500's ~18.18x forward P/E estimate, implying that investors expect the stock to underperform the benchmark. It also trades at 2.3x book value, and at a trailing ROE of 2.8%, the investor ROE at this multiple is just 1.22%.

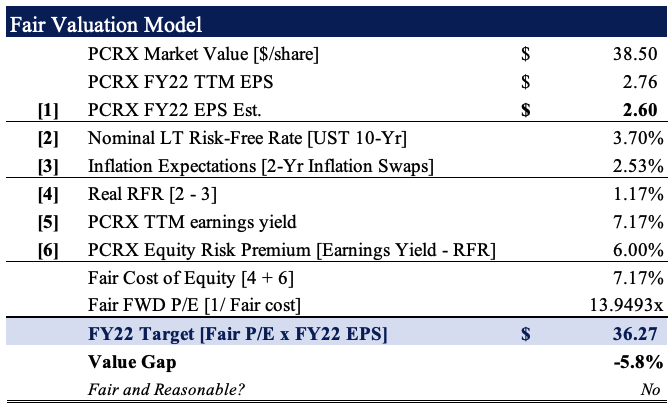

Assigning the forward estimates into our model below we believe the stock trades fairly at 13.95x forward earnings, below consensus estimates, and deriving a price target of $36. We've also got multiple downside targets to $28 and $24.5, after the stock has taken out its $38.5 target shown in Exhibit 3. These factors combined confirm our neutral thesis.

Exhibit 2. Fair valuation of $36 based on 13.95x forward P/E

{kind=link}

Exhibit 3. Downside targets to $28 with multiple resistance lines shown on point and figure studies

Data: Updata

Net-net, there's a number of unclarified data points with the PCRX story at present. It's concerning that the company isn't confident enough within its own position in its end-markets to provide forward-looking guidance. This was also seen in the last set of earnings, where it posted a wider than expected loss. It should be no surprise that we advocate investors to benchmark the company's Q4 FY22 and FY22 full-year results as a key performance indicator to assess its growth prospects looking ahead. Still, there's a lack of valuation upside from our assessment, and we see the stock fairly valued around its current market levels at a ~$36 price target. With shares trading within the scope of this valuation, we rate PCRX a hold.

For further details see:

Pacira BioSciences: More Evidence Needed To Advocate Entry At Current Valuations