PCRX - Pacira Biosciences: Sell-Off On Pain Relief Specialist - But Recovery Not Guaranteed

2023-10-30 17:17:47 ET

Summary

- Pacira Biosciences' stock has reached its lowest value since the pandemic-induced market crash in March 2020, trading at just $27.

- The company's recent Q2 2023 earnings report showed a decline in EXPAREL revenues and downgraded FY23 guidance.

- Pacira faces challenges such as patent expiration, generic competition, and uncertain revenue growth potential, making it difficult to make a convincing bull case for the stock.

Investment Overview

It has been more than three years since I last covered Pacira Biosciences ( PCRX ), the company that styles itself as "the industry leader in our commitment to non-opioid pain management and providing a non-opioid option to as many patients as possible to redefine the role of opioids as rescue therapy only."

Back in February 2020 , I gave Pacira stock a "buy" recommendation when shares traded ~$45, suggesting they ought to trade closer to $60. This was largely based on the growing sales of Pacira's lead product, EXPAREL, a long-acting, local analgesic (bupivacaine liposome injectable suspension), which the company describes as:

The only opioid-free, long-acting local and regional analgesic approved for infiltration, field blocks and interscalene brachial plexus nerve block to produce local or regional postsurgical analgesia.

In September 2020 , after Pacira stock had reached a price of $60 per share, I again gave the stock a "Buy" recommendation based on Pacira's assertion that EXPAREL could generate blockbuster (>$1bn per annum) revenues by 2025, and also based on the potential of its cold-therapy treatment Iovera, acquired via the buyout of Myoscience in 2019.

If the company could extract $200m of annual revenues from Iovera, on top of the blockbuster revenues from EXPAREL, and increase profitability by growing net profit margins slightly, my discounted cash flow analysis suggested the company's true value was closer to ~$100 per share.

After sliding to <$50 per share 12 months later, Pacira stock embarked on a bull run, reaching $84 per share in April 2022. In late 2021 the company had acquired Flexion Therapeutics and its lead product ZILRETT A (triamcinolone acetonide extended-release injectable suspension), the first and only FDA-approved treatment for osteoarthritis ("OA") knee pain utilizing extended-release microsphere technology, in a deal worth $450m, or $630m including debt, that paid $8 per share plus a contingent value right ("CVR") paying up to $8 based on certain sales milestones for ZILRETTA, and commercial approvals for two pipeline candidates.

ZILRETTA generated $106m of revenues in FY22 for Pacira, while EXPAREL generated $537m of revenues - up 6% year-on-year, with IOVERA revenues down 6% year-on-year, to $15m. The company earned $667m of revenues in total, but net income, which had been $146m in 2020, and $42m in 2021, slipped to just $16m, and earnings per share ("EPS") to $0.35, or $0.8 per share on a non-GAAP basis. Announcing 2022 earnings, Pacira also provided FY23 guidance as follows:

- EXPAREL net product sales of $570 million to $580 million;

- ZILRETTA net product sales of $115 million to $125 million;

- iovera° net product sales of $17 million to $20 million;

Pacira also added it expected a non-GAAP gross margin of 76%-78%, R&D expenses of $70 - $80m, SG&A expense of $220m - $230m and stock based compensation of $51 - $54m. That seems to imply that profits before tax may fall <$200m, and if we assume a tax rate of ~20%, a forward earnings per share figure ~$3.5.

Clearly, the market does not seem to have been impressed with these figures - whether the flat top line revenue growth, or the slightly underwhelming bottom line figures implied by guidance, or the earnings and forecast downgrades that occurred through 2022 - and began selling off Pacira heavily, so that today, the stock price has sunk to its lowest value since the pandemic induced market crash of March 2020, with shares trading at just $27 - a long way below my optimistic forecast back In September 2020.

Nevertheless, analysts at TD Cowen upgraded their rating on Pacira, setting a price target of $50, in August, suggesting that "negative sentiment is bottoming out." The company also has a supplementary New Drug Application ("sNDA") pending with the FDA for EXPAREL in the new indication of lower extremity nerve block, with a "PDUFA" action date of Nov. 13, and multiple other opportunities to expand its existing product portfolio into new indications, as well as several pipeline assets.

With the company set to announce its third quarter earnings on No. 2, and shares trading at historic lows, could this be a good time to think about acquiring some Pacira stock, or is the company - which also recently announced the departure of its 16-year veteran CEO and President David Stack headed for further trouble?

In the remainder of this post I'll analyze the company's strengths, weaknesses, opportunities and threats to try to answer this question, beginning with Q223 earnings.

Pacira - Recent Performance Fails To Offer Reassurance As Problems Become Evident

Pacira released its Q2 2023 earnings on Aug. 2, triggering a slide in the company's share price from ~$37, to $27. Of $169.5m of revenues reported, Exparel earned $135m, ZILRETTA $29.3m, and Iovera $4.4m. Net income was $25.8 million, or $0.56 per share (basic) and $0.51 per share (diluted).

EXPAREL revenues fell year-on-year, from $137m in Q222, which management explained as follows:

Second quarter volume growth of 4 percent was offset by a lower net selling price primarily due to the implementation of 340B Drug Pricing and other contracted relationships

Meanwhile, ZILRETTA sales increased only slightly, by ~7%, and Iovera revenues are clearly a long way off the $200m per annum management once felt was achievable. Meanwhile, the company downgraded its FY23 guidance, albeit only narrowly, guiding for EXPAREL revenues of $550 - $560m, ZILRETTA revenues of $110 - $115m, no change to Iovera revenues, but a fall in non-GAAP gross margin to 73% - 74%.

A cash position of $87m plus $134m of short-term investments was reported, alongside current liabilities of $109m, and $397m of convertible senior notes of £397m, and long term debt of $135m. To add to Pacira's worries, GAAP net income recorded across the first six months of 2023 amounts to just $6.2m, compared to $26.7m in the prior year period, and GAAP EPS was just $0.14, compared to $0.59 in the prior year.

In short, at this point it seems easier to identify the flaws in Pacira's business model - products struggling for revenue growth, a lack of profits, sizable debt, dwindling cash reserves, and lower net selling prices for its lead assets - than the strengths.

These are not necessarily the only problems affecting Pacira either. In its 2022 annual report / 10K submission, Pacira mentions the fact that:

The active ingredient in EXPAREL is bupivacaine. Patent protection for the bupivacaine molecules themselves has expired and generic immediate-release products are available. As a result, competitors who obtain the requisite regulatory approval can offer products with the same active ingredient as EXPAREL so long as the competitors do not infringe any process, use or formulation patents that we have developed for drugs encapsulated in our pMVL drug delivery technology.

For example, we are aware of at least one FDA-approved long-acting instillable bupivacaine product on the market which utilizes an alternative delivery system to EXPAREL. Such a product is similar to EXPAREL in that it also extends the duration of effect of bupivacaine, but achieves this clinical outcome using a completely different drug delivery system as compared to our pMVL drug delivery technology.

Patent protection is immensely important in the pharmaceuticals industry, as when it is in place, a company can charge the price it sees fit, i.e. a price that ensures the company is rewarded handsomely for the millions of dollars of R&D investment that have gone into developing the product.

Once that protection expires, however, generic versions of a product can be launched cheaply, and the company finds itself forced to drop the price of the original drug or risk selling volumes declining too steeply. It's a vicious circle that tends to see products revenues falling by >25% per annum. With the price of EXPAREL already affected by 340B drug pricing, can Pacira afford to see EXPAREL revenues fall when they are barely over half way to reaching the company's stated $1bn per annum target?

Although non-opioid pain relief is clearly preferable to use of opiates, for patient health reasons, the safety of drug delivery devices has recently been brought into focus, and it may be questionable if Pacira has brought about enough goodwill with patients and physicians to ensure the long-term viability of EXPAREL in the marketplace, and indeed, perhaps ZILRETTA and IOVERA also.

Although Pacira insists EXPAREL, IOVERA and ZILRETTA are unique and innovative products, in the case of the former the company admits in its annual report that the drug:

... Competes with currently marketed non-opioid products such as bupivacaine, marcaine, ropivacaine and other anesthetics/analgesics, all of which are also used in the treatment of postsurgical pain and are available as either oral tablets, injectable dosage forms or administered using novel delivery systems.

Iovera has fewer competitors, arguably, while ZILRETTA competes against "immediate-release steroids and HA injections."

Reasons To Be Cheerful? New Product Approvals, Pipeline, New Management, Historical Performance

It's not necessarily all doom and gloom at Pacira, however - it's shouldn't be forgotten that the company has delivered 25 consecutive quarters of positive adjusted EBITDA (would it be more impressive if that were positive GAAP EBITDA - arguably, yes it would), and the addition of Zilretta to the product portfolio has arguably been a success, bringing in triple-digit million revenues.

There are also multiple expansion opportunities for Pacira to explore. The company cites (in a recent investor presentation ) 340B drug pricing as a potential plus point for the company, as despite dragging down the average selling price ("ASP") there is potential to reach some 10m patients undergoing surgical procedures, plus the NO PAIN act, which mandates CMS reimbursement for non-opioid pain therapeutics, covers ~20m procedures, Pacira believes.

Then there's the upcoming sNDA decision from the FDA, which is backed by data showing EXPAREL proved superior to bupivacaine, which may help expand EXPAREL's addressable market to >2m patients, the company believes, while ZILRETTA's addresable market may cover up to ~8m potential procedures. Arguably, the promise of IOVERA - a hand-held cryogenic devices that can provide up to three months of pain relief, with an addressable market of 31m procedures, management believes, has not yet been fully unlocked.

In theory, patent issues aside, the longer Pacira's products are on the market, the greater the awareness amongst patients and physicians grows, and the more product Pacira can sell.

{kind=link}

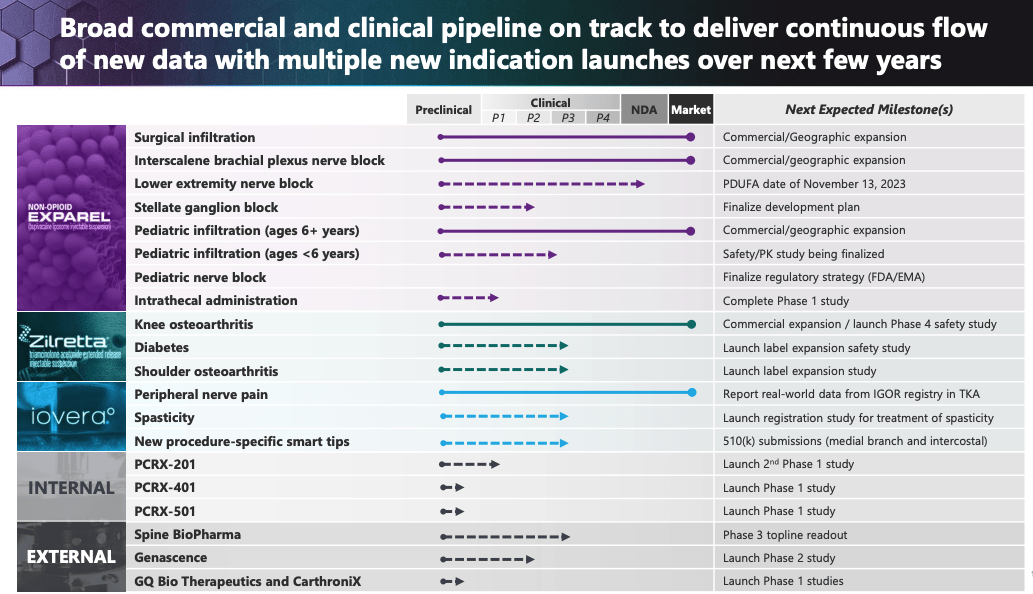

As we can see above, Pacira has an extensive pipeline of opportunities for both approved and pipeline products. ZILRETTA in diabetes and shoulder osteoarthritis strike me as intriguing opportunities, while PCRX201, a novel intra-articular gene therapy for knee OA, PCRX401, dexamethasome for back pain, and PCRX-501, 20mg bupivacaine, designed for longer lasting or chronic pain, all have the potential to open new revenue streams for the company, although I would be slightly concerned about the costs of R&D escalating beyond the company's somewhat limited resources.

Concluding Thoughts - Steady Q3 And New Approval Can End Pacira's Bear Run - But Is There Long-Term Value In Prospect?

Coming back to review Pacira after a three-year hiatus has been intriguing, and clearly, after my last post posited a share price target of $100, I'm disappointed to find the share where it is today, especially when 18 months ago, a peak of >$80 had been achieved.

The non-performance of IOVERA has clearly been a difficult issue for the company to overcome, and perhaps that is why Pacira felt it needed to grow inorganically via the acquisition of Flexion Therapeutics and ZILRETTA.

Back in February 2020 I gave a "sell" rating to a company considered Pacira's rival at the time, Heron Therapeutics ( HRTX ), which was struggling to secure an approval for a non-opioid pain relief therapy HTX-011. The drug was initially rejected, but eventually approved by the FDA under the brand name Zynrelef, but I note the company's shares have lost >95% of their value since my bearish note, and trade <$0.

To me, that underlines what a tricky market non-opioid pain relief can be, and how well Pacira has done to generate strong revenues, within it. The key question in relation to Pacira is whether EXPAREL, ZILRETTA and IOVERA genuinely have further revenue growth potential, or whether a ceiling has been hit.

Unfortunately, although I do agree with analysts that the non-opioid pain relief market can keep expanding through Q4 and into 2024, and that there's potential for Pacira's share price to recover, I almost feel as if Pacira has attempted to establish a foothold in this market too early. While Pacira has done much of the "dirty work" making the case for non-opioid pain therapeutics with patients and physicians across the US, the problematic patent issues, uncertain revenue growth outlook, costs of R&D - without a cast iron guarantee pipeline products can be successful - downward pressure on pricing, and increasing competition means that I struggle to make a convincing bull case at this time.

I do think Pacira's share price can grow in 2023, perhaps to traded within a $40 - $50 range, provided there are no further earnings downgrades in 2023 and the upcoming sNDA is successful. I would be slightly concerned around what next year's guidance will bring, however, and how the market will react to that.

For me, the risk of backing Pacira to be a long-term growth story is a little too high at present, and I wonder if, now that the long-term CEO has departed, if the new management will view its best exit strategy as an M&A deal, perhaps with a pharma - AbbVie ( ABBV ) for example, that has an interest in entering the pain relief market long term, and would be prepared to pay a premium for Pacira's business and products.

In six month's time, it may be much clearer in which direction Pacira's business is heading, and that will provide a better basis for making "buy" or "sell" decisions. I would give the stock a "hold" rating for the time being.

For further details see:

Pacira Biosciences: Sell-Off On Pain Relief Specialist - But Recovery Not Guaranteed