PKG - Packaging Corporation Of America: Finally Time For An Update

Summary

- It's been some time since I reviewed Packaging Corporation of America. Given that I'm a fairly heavy investor in things like packaging, timber and cardboard/paper, this is warranted now.

- I've looked at PKG a number of times in the past, and my latest stance at least outperformed the overall market - if still negative.

- Here is my 2023 stance for Packaging Corporation of America.

Dear readers/followers,

I've been looking at Packaging Corporation of America ( PKG ) for a number of years at this point, and I remain invested, albeit at a small stake, in the business. The company as of my last thesis has mostly outperformed the market, though I don't view "red numbers" as desirable, of course...

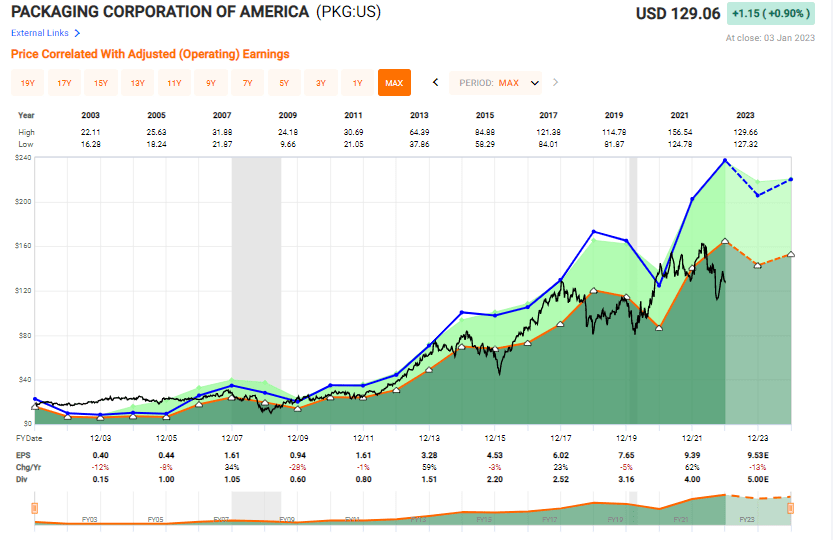

Packaging Corporation of America (Seeking Alpha)

Still, the company has upside and interest going into the next few years - and that is what I am going to take a look at here.

Let's revisit PKG.

Revisiting Packaging Corporation of America

The fundamental attractiveness of packaging companies and the sort of business that PKG has remains. It produces basic materials and products that are needed - no matter what sector you're in.

When it comes to corrugated products and containerboard in the US, this company is the third-largest producer in the nation. Compared to its two peers and direct competitors, International Paper ( IP ) and WestRock ( WRK ), the company has certain advantages that have led to higher profitability historically speaking.

The company reports in three segments, each fairly self-explanatory.

- Packaging

- Paper

- Corporate & other

Its facilities and plants are found in the following areas in the US.

PKG IR (PKG IR)

The company is almost fully vertically integrated. What this means is that PKG handles every aspect of the manufacturing process, saving the supply of timber and pulp. The company designs its packaging at company offices/locations, produces the containerboard at one of six mills, and assembles it at one of its many locations across the USA.

The only aspect where the company is not self-sufficient is fiber, which is consumed both in the form of wood fiber and recycled paper/cardboard fiber.

PKG sells through direct sales to end-users, independent brokers in the field, various marketing, and sales organizations, as well as national and regional distribution partners. PKG also has sales representatives that travel the nation to push products and has a sales force that focuses on larger accounts. Transporting is handled mostly by rail, or truck.

{kind=link}

The current 2022-2023 state of the operations include six containerboard mills, one containerboard machine at its Jackson, Alabama, white paper mill, and 89 converting operations.

In 2021, the latest fiscal we do have, PKG produced about 4.9M tons of containerboard and shipped about 65.7 billion square feet of corrugated products. The company also has a paper segment that works under the "Boise Paper" brand name, which is a division that still sells legacy white paper at two mills currently remaining.

The company employs over 15,000 people as of late 2022, and sells around $8B worth of products per year, with headquarters 30 miles north of downtown Chicago, IL.

That's pretty much what the company is and does today - packaging and paper, with paper a mostly declining segment that over time seems likely to decline further.

PKG managed the pandemic well - and has managed inflation acceptably as well. For the early periods of 2022, the company reported record sales revenues, EBITDA, operating profits, margins, and EPS. In short, the company fired on all cylinders in the 2021 fiscal, and while we're likely to see a double-digit EPS decline in 2022, that decline probably isn't going to be 40-60%, it's going to be around the low teens, at 11-14% according to most recent forecasts.

This is a testament to the company's operational efficiencies, savings, and cost discipline as well as taking advantage of a very interesting market. PKG remains a volatile business in terms of its share price, and not one that I believe should be bought at a premium at any point.

{kind=link}

The company returned to shareholders both in the form of dividends as well as stock repurchases and delivered a record ROIC despite massive global problems. It refinanced its debt to 3.5% despite the current interest rate situation and currently has an average maturity of 16.3 years. This company took the concept of preparation for trouble to heart and did the equivalent of building a doomsday bunker around its finances, with that debt situation and liquidity of $1.1B - almost 10% of its current market cap.

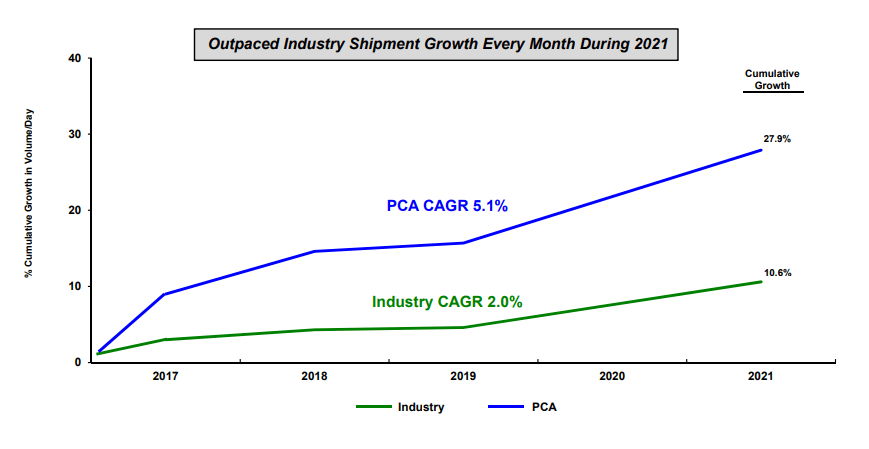

PKG outperforms the industry and has for some time.

{kind=link}

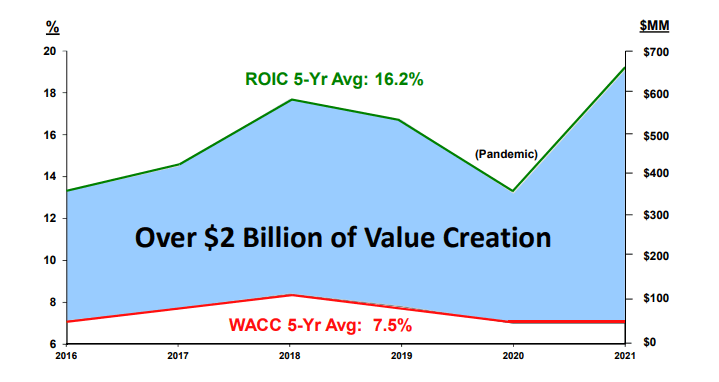

Despite inflation and cost increases, the company has maintained a very solid EBITDA margin of upwards of 25%, with an average integration rate of 91.4% for its containerboard production - among class-leading in truth, and again, the ever-important ROIC for a company like this in relation to its weighted average cost of capital is amazing.

{kind=link}

Taking a replacement value calculation to the company confirms the same thing. Its assets cannot be replaced at effective prices in today's market, even if market entrants were interested in doing so. It's this that keeps me interested in companies like this, not only in the USA but in Sweden and other countries as well.

My firm stance is that paper, cardboard, timber, and fiber/wood products are going to be a bigger part of our economic global future, not a smaller one, and that's why I go for companies that are market leaders in these respective segments.

As for the ROIC thing in companies like these, there's a very high correlation between a basic materials company's ROIC and its share price, usually. When one goes up - the other follows. PKG is no different, even if it's more volatile.

Also, with a 20-year RoR of 800%, or 11% per year, PKG has firmly outperformed the average of the market here.

So, it's a great business with a BBB credit rating and a dividend that's currently close to 3.9%. Not high-yield, but respectable, and one that's growing as well.

Speaking of dividends, the company's approach to them is very conservative. It has a 10-year average yield of below 3% (note today's yield), and a 10-year average EPS payout of 46%, leaving ample room for investments, buybacks, raised interest rates, inflation and other considerations.

PKG is, simply, a very conservative sort of business deserving of your undivided attention.

3Q22 results are the latest we have - and these were positive. The company once exceeded guidance despite massive inflation and cost headwinds, managing to generate earnings of $2.83 for the quarter, a full $0.14 above YoY results. Price increases contributed to this development, as demand in packaging was actually significantly below the company's expectations. However, like many companies, there is a current focus on pricing above volumes in terms of results, and PKG is reaping the rewards of this.

At the same time, mills across the company's portfolio are reducing their costs through process efficiency and cost cuts in terms of both materials and labor. Containerboard is a very good example, which was handled in a very balanced manner for the quarter, focusing on demand to match the supply and with expertly-managed mill outages.

There is no massive difference for the upcoming 4Q22 period. The company is expecting more headwinds in terms of inflation, but demand for paper and cardboard is stable, with continuing to run the containerboard system in accordance with demand. I've been through the quarterly P&Ls and the various items affecting comps, and there wasn't anything that drew my attention - just remember that costs are indeed a thing here. PKG is rare because it managed to lower interest expenses - but higher operating costs, logistical expenses, outage expenses, D&A, and converting costs are still affecting the bottom line. Operating costs alone were a $0.77 per-share impact, with logistics another 20 cents.

Volatility is here and certainly isn't going anywhere in the near future.

Let's look at the valuation impact of this.

Packaging Corporation of America - Valuation

I am still unwilling to consider any significant premium valuation for the company. Buying PKG at a high premium has always been a good way to get your negative returns handed to you, so to speak. So that 5-year premium of 16.5x P/E, that's an average I very much ignore, focusing instead on the 15x standard.

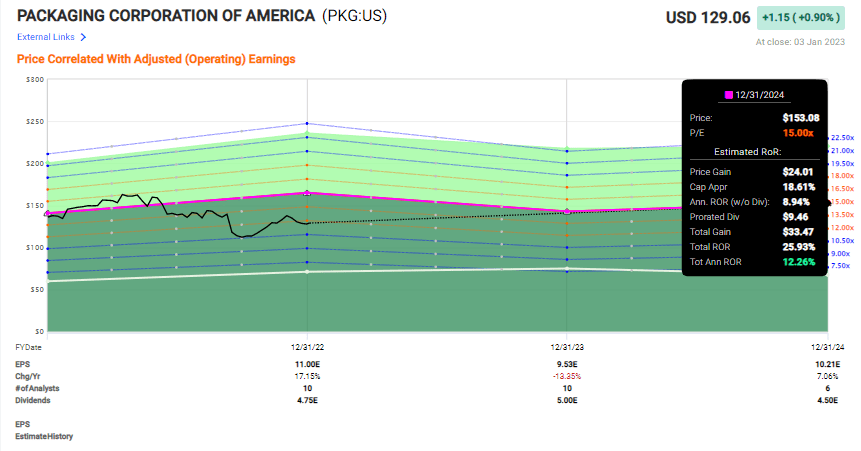

To that end, PKG does have a good upside, if not the best one we've ever seen. It's close to its 20-year average performance.

{kind=link}

The company currently sports an EPS yield of 8.51%, or a P/E of around 11.7x, which is very low for this company. It's low enough to make me interested in potentially increasing my position.

S&P Global doesn't believe the company to be worth more than this. Due to cost increases and demand opaqueness, S&P Global analyst averages are down to around $129 from $143 about a year back, with only 3 at "BUY" out of 10 analysts. I go against the grain here. I believe PKG is worth long-term 15x P/E, which if we average it out for the next couple of years including the 2023E numbers comes to around $145/share. That's a few dollars above my last target, which I believe to be a good one for the next few years. Any time the company drops below $130/share, the value for its assets, its revenues, its earnings, and the potential as well as the sheer replacement value for what the company has starts to look attractive from a purely supply/demand perspective.

That's not even mentioning the fact that there's a higher focus on domestic manufacturing and supplies, and paper and cardboard like other commodities not really being something you want to "ship" great distances.

For those reasons, here is my thesis on PKG.

Thesis for the common shares

- PKG Is a great business with great fundamentals and a good market share of NA containerboard. It should be considered attractive at the right valuation, and management is proactively managing the current inflation/logistical/cost headwinds to stay ahead of the curve and improve margins. For now, this strategy has been working out for the company, and I don't see a fundamental reason why this would change materially in the near term.

- A price target that I would consider attractive for investment based on my goals would be around $142/share - though every investor of course needs to look at their own targets, goals, and strategies. I would also always consult with a finance professional before making investment decisions such as this. My own goal calls for an annualized rate of return of at least 8.5%, and PKG currently delivers almost 13% until 2024E.

- Because of that, I view PKG as a "BUY" here.

Remember, I'm all about:

1. Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation but hovers within a fair value or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

PKG fulfills every single one of my investment criteria.

Thesis for options

PKG is a non-trivial/uninteresting option potential. The combination of volatility and fundamental safety usually makes for some potentially lucrative contracts, if you pay attention and are clear on your goals. While we haven't seen massive declines in selling cash-secured puts, I can guide to the following Put at this time.

PKG Option (Author's Data)

Not the most impressive RoR, but I went through history and saw that in a day in the red for PKG, that premium is likely to go up over $3/share, meaning you're getting a 9%+ annualized RoR to wait for PKG to drop below a share price it hasn't seen in over 1.5 years.

That is not a bad deal as I see it. $10,000 is a lot, but it shouldn't be prohibitive to someone in the "options game".

I'll keep an eye on both the February and the April puts for this one.

For further details see:

Packaging Corporation Of America: Finally Time For An Update