PKG - Packaging Corporation of America: Q2 Beat Vs. Lower Q3 Estimates

2023-07-26 15:03:49 ET

Summary

- Packaging Corporation of America's Q2 adjusted earnings per share reached $2.31, exceeding our $1.99 estimate.

- Despite a challenging demand environment, the company managed operations efficiently and cost-effectively.

- Although optimistic about the containerboard sector, the company expects higher logistic costs in Q3 and predicts a lower EPS of $1.88.

- Valuing the company using its historical average, we are now moving our rating to a neutral 12-month view.

Our latest publication released at June-end was called: " Approaching The Bottom, Time To Re-Enter ." No title was more effective, and today, we hope our followers/readers/PKG investors are enjoying a plus 10% in stock price appreciation. Packaging Corporation of America ( PKG ) released its quarterly figure, exceeding Wall Street numbers and internal estimates. Paper valuation multiples bottomed in Q4 2022, and we are not surprised to see a positive reaction. In addition, we believe that analysts will focus on profitability targets and cost improvements in H2 2023, and this week, International Paper is also reporting. As a reminder, we have a long-standing buy rating on PKG. This is supported by 1) a higher ROCE vs. its peers, 2) best-in-class EBITDA thanks to competitive advantages on clients' proximity and lower logistic costs, 3) centralized procurement with a focus in the US (not like International Paper and WestRock with earnings and industrial facility in Europe (Fig below) and Mexico respectively), 4) lower energy cost thanks to self-sufficient production, and 5) operating cash flow generation sufficient to deploy CAPEX and pay a recurring and increasing dividend .

{kind=link}

Source: International Paper Corporate Website

Q2 results

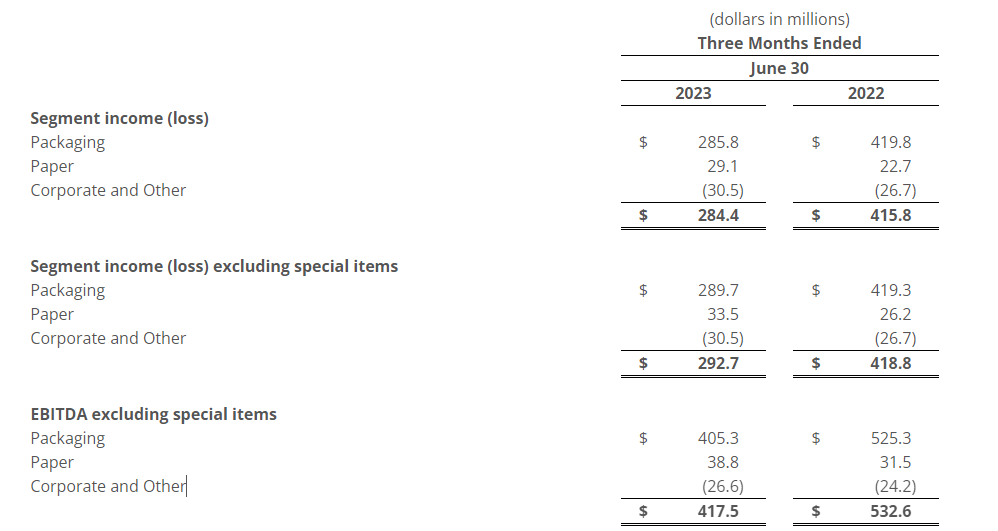

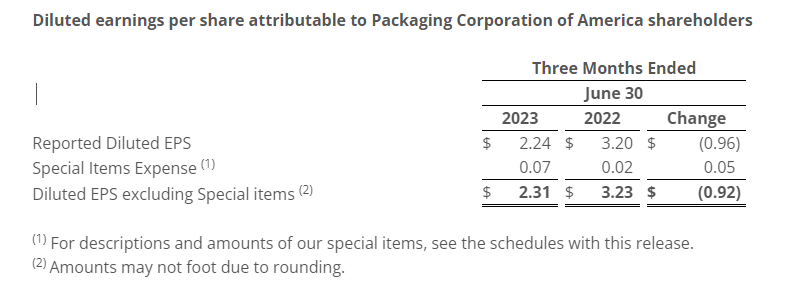

Q2 adjusted earnings per share reached $2.31, well above the Wall Street estimate at $1.93 and the company's guidance of $1.96. Q2 top-line sales reached $2.0 billion compared to the $2.2 billion achieved last year. The company delivered an adj. EBITDA of $417 million represents an 11% outperformance compared to the average consensus set at $375 million. This beat was due to lower operating expenses and lower freight costs. The CEO also confirmed this positive outcome, reporting that " logistics and distribution personnel did a great job minimizing the effect of higher freight rates in certain regions and optimizing freight routes and transportation modes." Well, this is very much in line with our buy rating thesis supported by our point 2. On a positive note, corrugated shipments per day declined by 9.8% on a yearly basis but grew by 2.7% on a quarterly basis. This is the reason for PKG's stock price today's upside. In addition, the CEO explained how Packaging Corporation of America is managing " operations efficiently and cost-effectively as we continued to operate both our Packaging and Paper segments against a challenging demand environment ." Looking at the details, the company cited a 49k-ton inventory decline on a yearly comparison.

{kind=link}

Source: Packaging Corporation of America press release

For Q3, despite one less shipping day, the CEO expects higher packaging volume but offset due to lower price/mix evolution. Packaging Corporation of America guided Q3 with an EPS of $1.88, and Wall Street is at $1.94. Despite that, the company is usually very conservative, and PKG's track record is additional proof to be above their internal estimates.

{kind=link}

Conclusion and Valuation

Here at the Lab, we are more optimistic about the containerboard sector; however, pricing developments will likely decrease faster than expected. The company is more confident about clients destocking, but the US has an oversupply current capacity issue. In addition, the CEO emphasized higher rail rates for the second time in the analyst call. So, we might forecast higher logistic costs in Q3, which is probably why the company's EPS is predicted to be down quarterly. Last time, we were already above the company EPS guidance and set quarterly earnings per share of $1.99 in our internal estimate. The company has usually traded at a premium valuation compared to its peers at the P/E level and EV/EBITDA. Flattening demand at a low level is not resolving the oversupply issue. In our estimate, despite a supportive Q2, we are lowering Q3 numbers, arriving at a 2023 EBITDA of $1.6 billion. Valuing PKG in line with its historical average (8.2x), we arrive at a valuation of $150, providing a neutral rating. In our paper coverage, we prefer WestRock for its cheaper valuation and because it has a higher boxboard mix.

For further details see:

Packaging Corporation of America: Q2 Beat Vs. Lower Q3 Estimates