PKG - Packaging Corporation of America: Strong Fundamentals And Growth A Choice For Dividend Investors

2023-05-04 01:49:18 ET

Summary

- Strong growth over time is exceptional, especially for a company of this size and age.

- They have a commitment to return value to shareholders and have been holding that up with a good dividend and generous share buybacks.

- An impressive balance sheet and cash flow statement back up the fundamentals of this company to make it a solid buy.

Company Overview

Founded in 1867, Packaging Corporation of America (PKG) is one of the country's largest producers of container board products, paper, and packaging material for a large range of items. It currently reports sales in three segments consisting of Packaging (making up the bulk of their business), Paper, and Corporate and Other.

They operate 8 mills and 89 corrugated products plants and related facilities spread across the United States, along with a single facility abroad in Hong Kong.

Their customers are businesses of all sizes, purchasing all manners of corrugated packing materials - including packaging for food and other consumer products. Their paper segment typically sells both commodity and specialty paper products.

Now let's get started with this "bird's eye view" of PKG: This is intended to give you, a potential investor, an overview of the company and its financial prospects. Hopefully this will help you get a good sense of whether or not you're interested in this company.

Revenue

PKG has precisely the "upward and to the right" revenue curve that I want to see. Going back to 2000 they've continued to grow steadily over time. If we are looking for a long-term investment, then this is what we want.

In their latest conference call they discussed their latest estimates and forward guidance. One of the concerns from the call regarding revenue was that they were going to actually have a lower Q2 than Q1 this year, something that had only happened one time in the company's history.

George Staphos: Thanks for the details. Mark, a question for you. Normally 2Q is up sequentially from 1Q. And when we look back historically over time, the only time that we saw a down 2Q, if we're correct, was the COVID second quarter, even if we went back to the, the great recession in '08 and '09, you had up 2Q versus 1Q.

Their response was a bit of a mixed bag, discussing price declines as noted in the previous conference call. So it looks like this was expected. They then went on to show some promising information for future guidance:

The good news is, is that there's been a big turnaround starting in April. And so we've got a good look 13 days into the month. And our bookings right now just over March alone are up 11%, and they're up 10% over the first quarter. Still down 6% compared to April of '22, but April of '22 was our all-time record. So just to calibrate everybody, the volume continued to increase significantly because of COVID all the way through April and then finally started to turn the other way. So we've still got that really tough comp coming in the month of April. But given the fact that we're double digits ahead of where we are in March is a huge improvement.

Overall I don't see much to worry about there. Next, let's break down the company's segments and take a look at their charts.

{kind=link}

{kind=link}

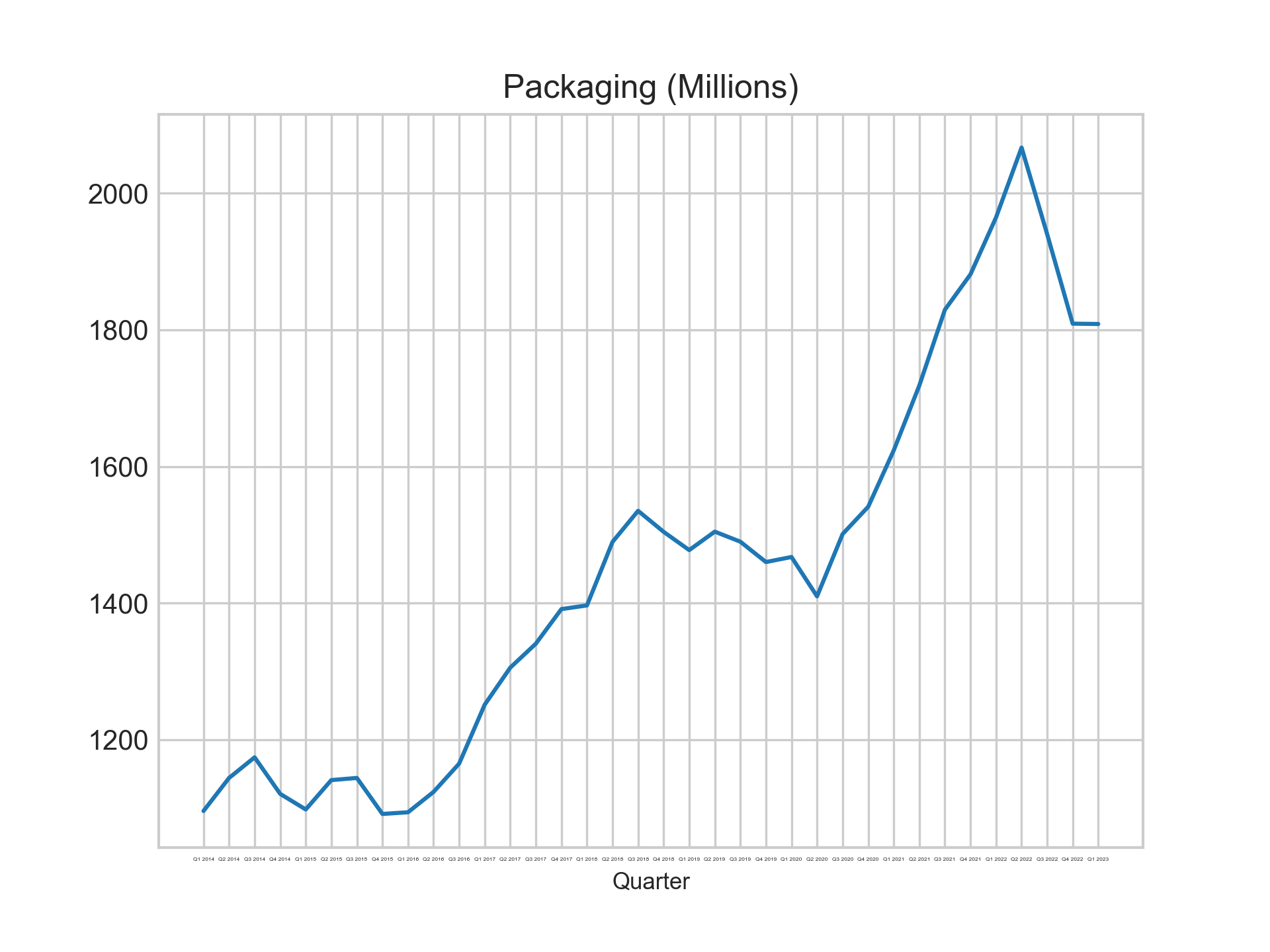

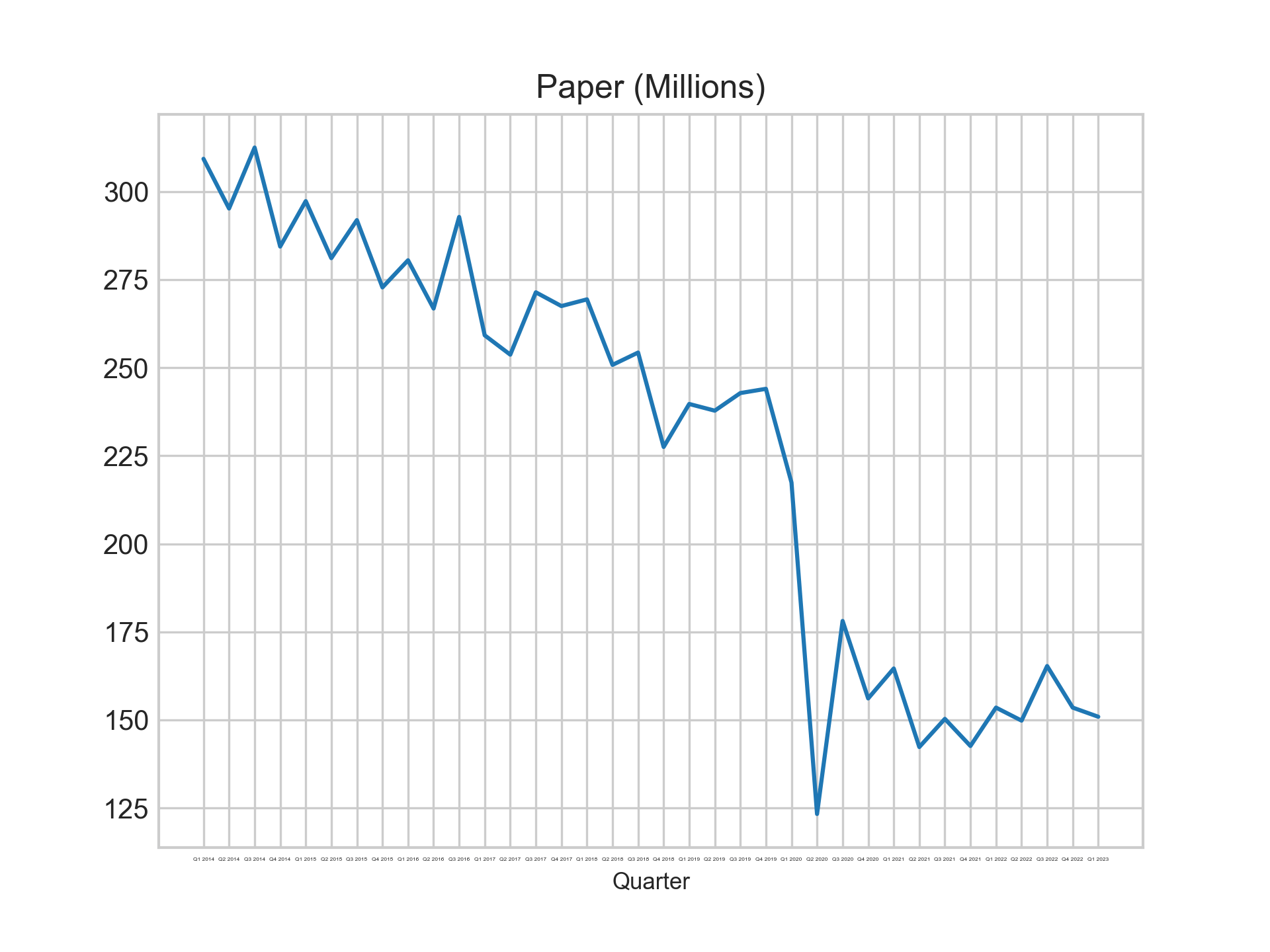

The company clearly has exceptional growth in the Packaging segment, which is really what we want to see here since it's the cash cow. The other segment, Paper, is giving us a bit of trouble. The third segment, Corporate and Other, only accounts for $20M in revenue and isn't worth discussing.

The Paper segment plunged heavily in COVID, and hasn't recovered, just holding steady at $150M. Although it's worth noting that the trajectory that it was on prior to COVID seems like it would have ended up in this territory anyway.

Declines in Paper revenue are to be expected however, as our world moves further and further away from any sort of print and towards digital information transfer - even in offices. Overall the decreases are more than offset by the large increases in the Packaging segment, so it's clear the company is taking them in stride and making up those losses elsewhere. I don't really have any concerns over this.

Debt

At the end of Q1 2023 PKG reported a total of $2.4B in total long-term debt consisting of fixed-rate senior notes. They've more or less kept it stable since 2014, and haven't paid it down over time.

They do a good job of keeping their current liabilities low compared to revenue as well, and their interest expenses into EBIT finds an interest coverage ratio of 21x. They should have no problem servicing their debt levels, although I'd like to see them declining.

Valuation

PKG is coming in at the top of the list here compared to its comps (according to SA and a little bit of research by me). It's not a huge difference, but it's significant that it's at the top of the pack. Investors are definitely more optimistic about it than its peers, and the revenue curve is certainly a reason why. Let's compare it to its historical valuation to get a better picture.

Looking back at their valuation over time, they're at the lower end of their range back to 2012 or so. The blue line behind is the price, so we can see even with recent increases in stock price they're at a very favorable valuation compared to where they were in the past.

I'd have to say the company is likely fairly valued here, but it has plenty of runway to move to that overvalued level so the savvy investor can take some profits off the table.

Looking at their CF/CapEx ratio, it is more or less sideways. The gross value of CapEx has risen broadly along with their revenue, giving them that nice upward curve to their operating cashflow. I like that they've achieved that growth, while keeping their CF/CapEx consistent (if you put a moving average on it, anyway), although I'd like to see the ratio rising over time.

Overall, I have no concerns with their valuation and an entry at this area seems appropriate.

Dividend

PKG has the fantastic "stair-stepper" pattern that I like to see for dividend paying stocks, showing an increase year after year and returning that value to shareholders. Currently we have an annual payout of $5.00, giving us a forward yield of 3.74% at today's price.

The yield isn't incredibly high, but it's not bad when you consider that the company has plenty of room to keep growing it. Over the last 10 years we've never seen them much over a 60% payout ratio, and the majority of the time it's below 50%. That's perfectly sustainable and leaves room for growth given the year of year increases in revenue.

The dividend here is a big plus for this company, and I'm a fan of where they're at with it.

Shares Outstanding

This is exactly what we want to see with a profitable company like this. Over time they buy back stocks, returning value back to shareholders. We want to see the opposite of the dividend graph here, with a downwards stair stepper pattern.

Looking through previous earnings call transcripts they have spoken repeatedly about share buybacks, and in their latest one they addressed it again. Mark Kowlzan, CEO, mentioned that the company is paying an attractive dividend and they remain flexible on any and all opportunities in terms of dividends and share repurchases. They have the flexibility to take advantage of all these opportunities as they present themselves.

I think that's accurate, looking at their revenue and cashflow. They have plenty of room for both the dividend and continuing share buybacks.

Leadership

{kind=link}

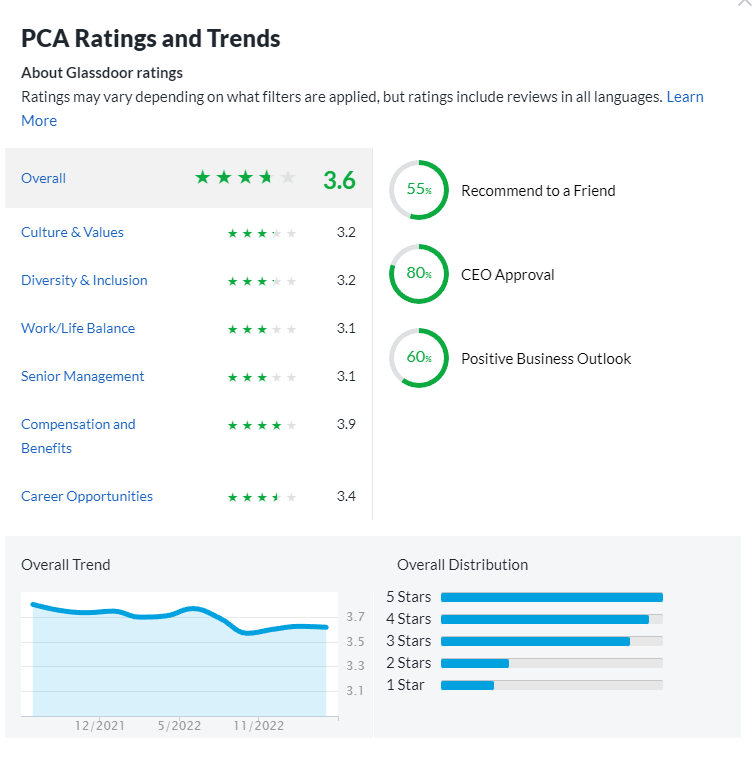

PKG has generally good reviews on Glassdoor , with most employee ratings clustering around 3, 4, and 5 stars. It's important to note that it is on a downward trend however over the last few years.

Most of the positive and negative reviews mention the same things. They're pleased with the company's benefits and pay, but dislike local management. After having read through the reviews of a great many companies I can say that nothing is unusual there at all.

What is interesting here is an 80% approval of the CEO. That means, in my opinion, overall employees are pleased with upper leadership. Generally employees are very brutal towards a CEO, so an 80% approval is pretty high marks.

Overall it looks like employee morale is fine, and on par with a very large company. Employees like the CEO more than average which is a good sign.

Conclusion

PKG is coming in with a strong revenue curve, and solid fundamentals. They're well positioned in their industry with a large stable of products, clients, and contracts. They're one of the largest and oldest players in their game.

They pay a decent dividend, and they've continually shown that they're willing to return value to shareholders. This is what I really want to see out of companies. When you combine with the really solid foundation that I've went through in this article, I've got to recommend a buy for the dividend focused investor. I think this is a solid company that can remain in your portfolio for years to come, generating income for you.

About this article: When I research stocks I start with a "bird's eye view" of the target company. Many of the things I went through in this article are what I'll look at first. I want to make sure the company grows year over year with a nice revenue curve. I want to make sure their debt is serviceable and preferably getting paid down. I want to make sure shareholders get a return on their investment through a good ROE. I want to see how the company is handling its dividends and are they sustainable. I want to look at the share float and make sure they aren't decreasing share value by inflating it. And finally, I want to look at the leadership and see what employees think about them.

When this bird's eye view is complete, I'll decide if I want to avoid the company for the time being or if it's a potential candidate for investment. This article that you are reading is the result of my bird's eye view examination. It is designed to be an overall high level view of the company that you can read to determine if this company is something that you might consider as a candidate for investment. You should not take my final conclusion on the company as your sole recommendation for investment, and you should conduct further in-depth research on your own to come to your final conclusions.

As a result of this, my "buy" recommendations come with an asterisk. And that asterisk is that this is only a high-level examination, and in-depth research that can take many hours, or days, of your time is still required. This is why my articles are short and to the point, with no fluff or filler. Just the facts that you need to know to move forward.

For further details see:

Packaging Corporation of America: Strong Fundamentals And Growth, A Choice For Dividend Investors