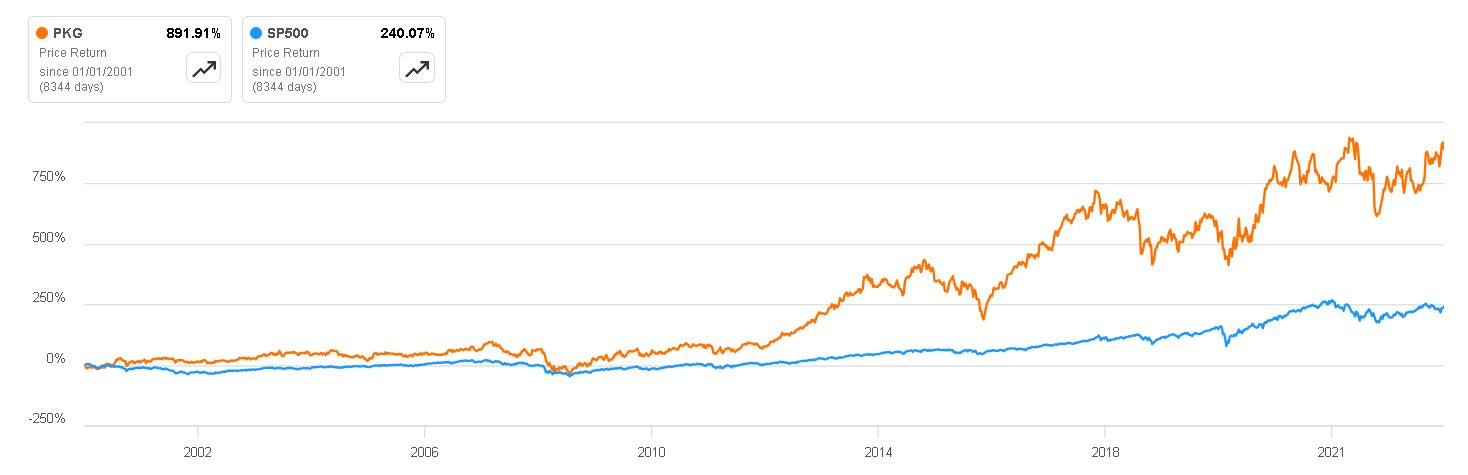

PKG - Packaging Corporation of America: Valuation Is Justified By Its Quality

2023-11-16 18:02:04 ET

Summary

- Packaging Corporation of America specializes in the production of containerboard and corrugated packaging.

- The sector is stable and expects growth in the coming years, primarily driven by the expanding e-commerce market.

- The company has better ROIC, margins and financial position than its peers, but trades at average multiples.

- Although I do not expect returns greater than 15% on this investment, I find it an attractive company to strengthen a portfolio.

Investment Thesis

The packaging sector stands out as one of my preferred areas to explore for investment opportunities. Renowned for its stability and resilience during economic downturns, this sector features consolidated businesses with significant growth potential, exemplified by Packaging Corporation Of America (PKG).

This article will provide an in-depth examination of the company's business model, backed by a numerical comparison with some industry competitors. Despite the initial impression of it not being particularly cheap, a closer look within the sector suggests it trades at reasonable multiples. These multiples are arguably justified by the company's superior quality, leading me to consider a ' buy ' rating.

{kind=link}

Business Overview

Packaging Corporation of America (I will refer to it as PKG or PCA) specializes in the production of containerboard and corrugated packaging.

PCA's products are used for a variety of packaging applications, including corrugated boxes, containerboard, and specialty packaging. The company serves a diverse range of stable industries, including food and beverage, automotive, agricultural, and consumer goods.

{kind=link}

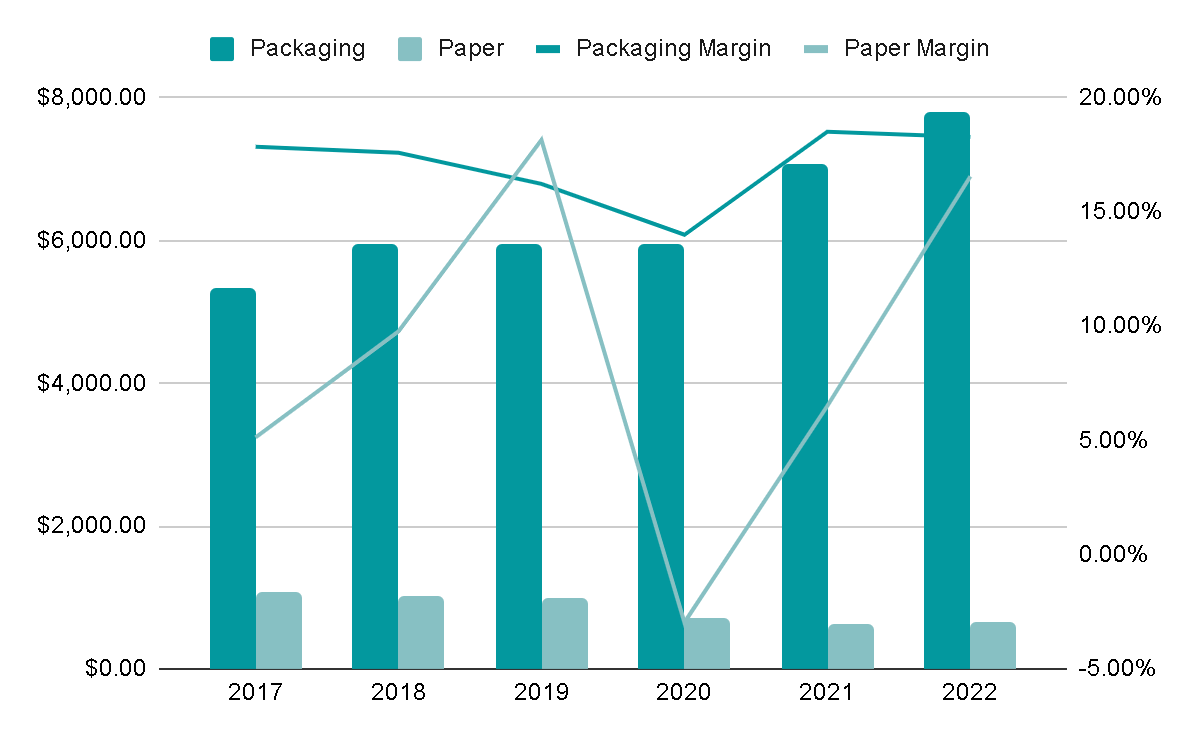

The company primarily operates in two segments, which collectively contribute to 97% of its revenues: Packaging and Paper.

Within the Packaging segment, the company is engaged in the manufacturing and sale of a diverse range of containerboard and corrugated packaging products, constituting 90% of total revenues. Conversely, the Paper segment represents 7% of revenues and is considered a less favorable business. In this segment, the company manufactures and sells consumer-brand office and business papers. However, this segment is experiencing a decline at an annual rate of 10%, attributed to the increasing trend of companies shifting to digital environments, resulting in less demand for paper, and margins in this segment are less predictable.

{kind=link}

This is in stark contrast to the Packaging segment, where the market exhibits favorable trends . Various studies anticipate global growth of approximately 4-6% annually in the next decade. This growth is primarily driven by the expanding e-commerce market, which consistently requires cardboard for product packaging, as well as the increasing demand for sustainable packaging and alternatives to plastics.

While it may not be a high-growth industry, the Packaging segment is characterized by stability . This stability arises from the essential nature of packaging in various consumer products, including basic necessities like food and beverages. As a result, clients of PCA typically maintain stable incomes and, consequently, tend to sustain orders even during economic downturns.

Market Expected Growth (Grand View Research)

Key Ratios

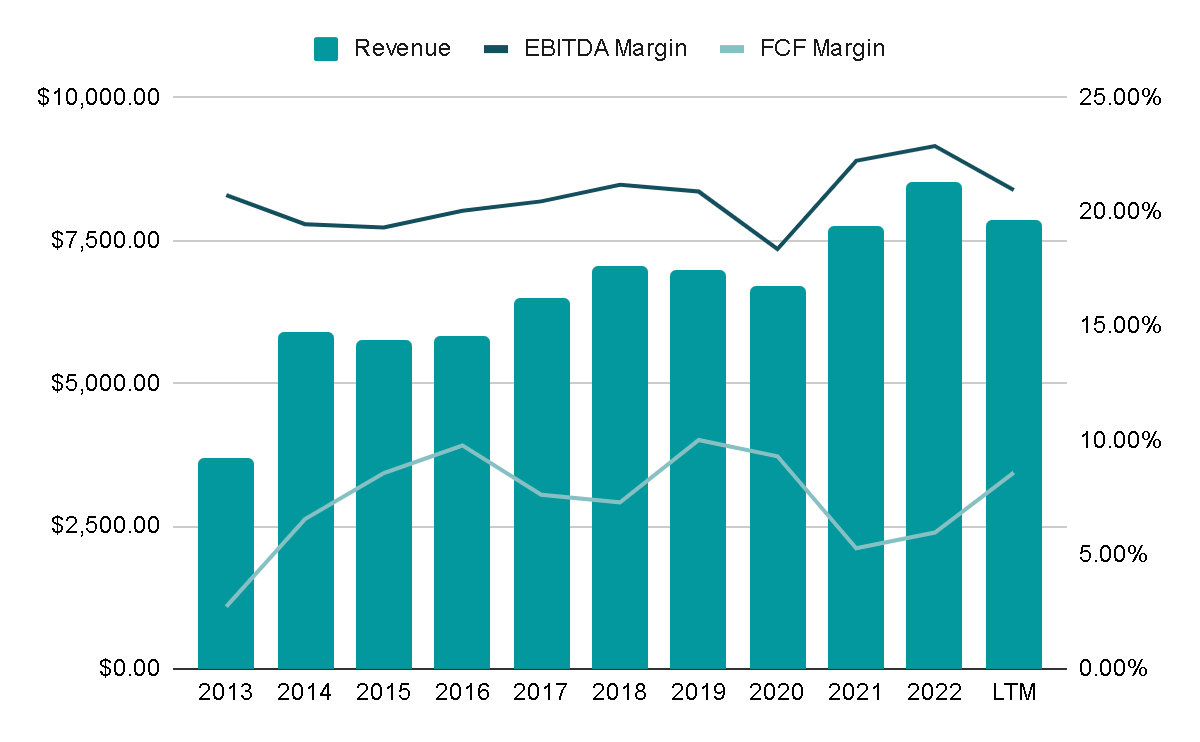

Revenues have grown at rates of 10% annually in the last decade, maintaining very stable EBITDA margins of 20%.

In the valuation section we will go into more detail about the growth and margins of each line of business, but for now the set of profits shows us a very defensive and predictable business with moderate growth.

{kind=link}

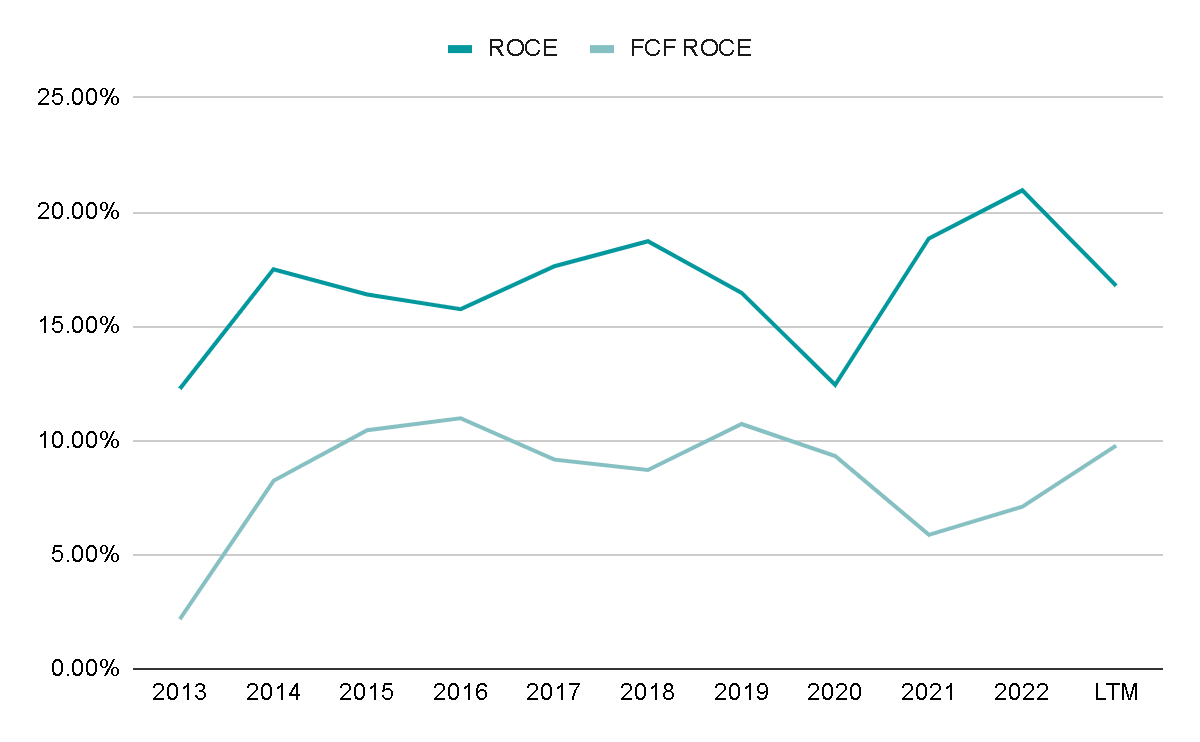

The company consistently maintains a Return on Capital Employed ((ROCE)) of around 17%, a metric regularly considered by management. This is particularly advantageous for shareholders, indicating that the company actively seeks investments that generate value surpassing the cost of the capital employed.

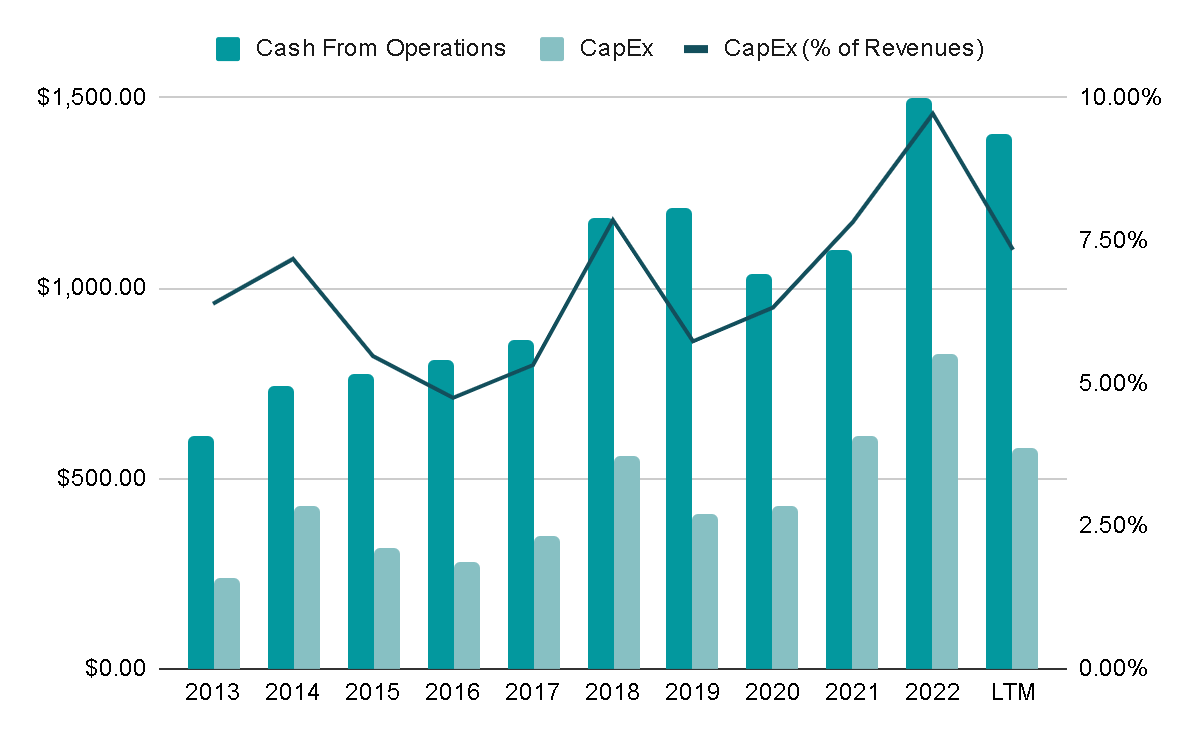

Typically, capital allocation involves reinvestment in the business through capital expenditures (CapEx). Over the last five years, only a modest 3% of capital has been directed toward acquisitions, while 24% has been allocated to debt repayment. Moreover, 32% has been utilized to reward shareholders through dividends, coupled with occasional buybacks during opportune periods of favorable stock prices.

{kind=link}

In the provided image, a substantial investment in CapEx is evident, representing 10% of Revenue during FY2022. These businesses are inherently capital-intensive , necessitating continuous investment to expand the number or capacity of their factories, which is a costly endeavor. Furthermore, the company has been proactive in investing to comply with environmental rules and regulations. While these investments may not yield extraordinary returns, they are essential and temporary obligations.

Contrary to initial perceptions, the capital-intensive nature of these businesses serves as a barrier to entry for potential competitors. The significant investment required acts as a deterrent, particularly for new entrants attempting to compete at the scale of well-established entities such as PCA.

{kind=link}

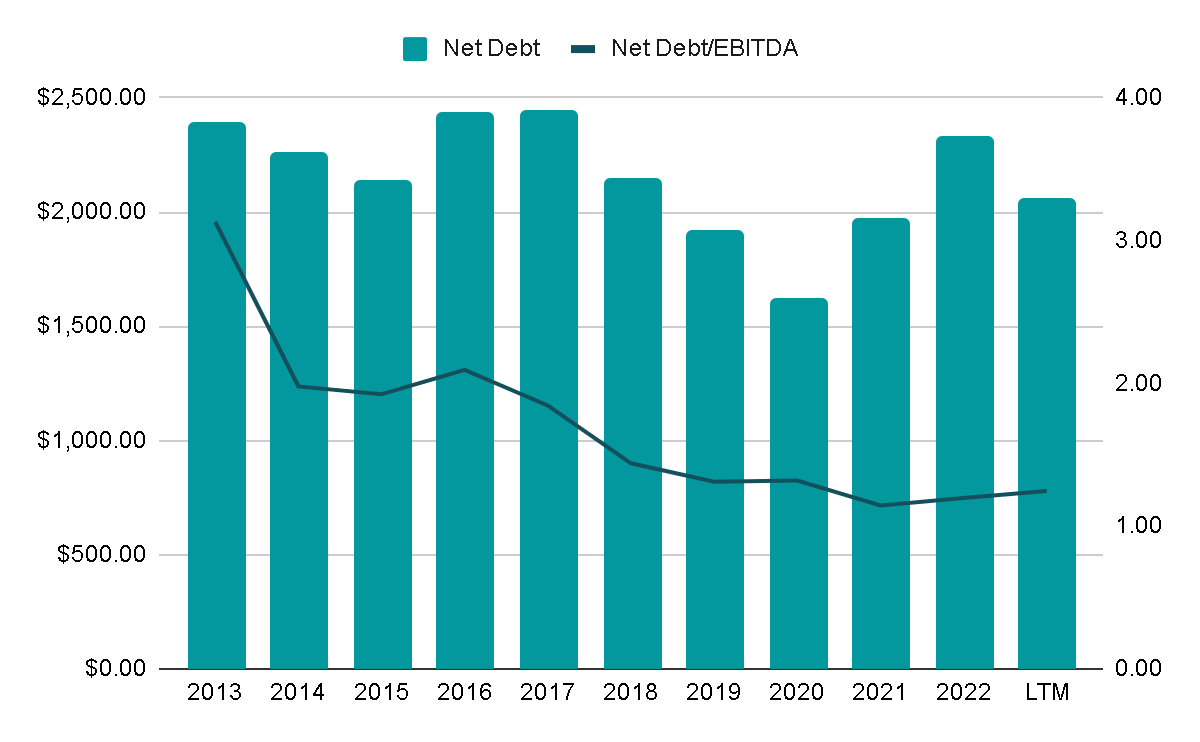

Another noteworthy aspect is the company's consistent deleveraging over the last decade. Currently, the Net Debt/EBITDA ratio stands at a mere 1.25x. In practical terms, it means that the EBITDA generated in just over one year would be sufficient to eliminate all net debt. This signifies an exceptionally solid financial position , particularly unusual within the sector, as we will explore further below.

{kind=link}

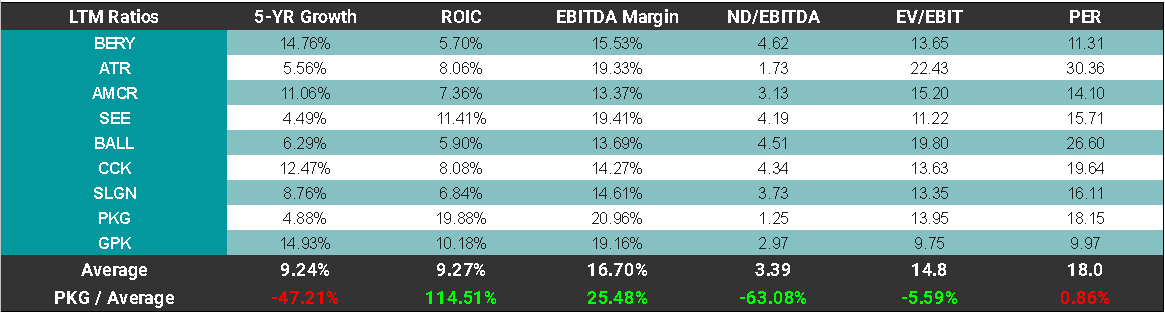

To provide a comprehensive overview of the metrics discussed earlier, the following comparative table includes Packaging Corporation of America alongside some other packaging companies.

Over the past 5 years, PCA stands out as the company with the lowest revenue growth. Nevertheless, noteworthy aspects include an impressive ROIC of 20%, significantly surpassing the sector average of 9%. Additionally, PCA boasts wider EBITDA margins and the healthiest financial position , evident in its favorable Net Debt/EBITDA ratio.

Despite these standout metrics, the company currently trades at multiples quite in line with the sector average. This reflects a scenario where an exceptional company is trading at average valuation multiples .

{kind=link}

Valuation

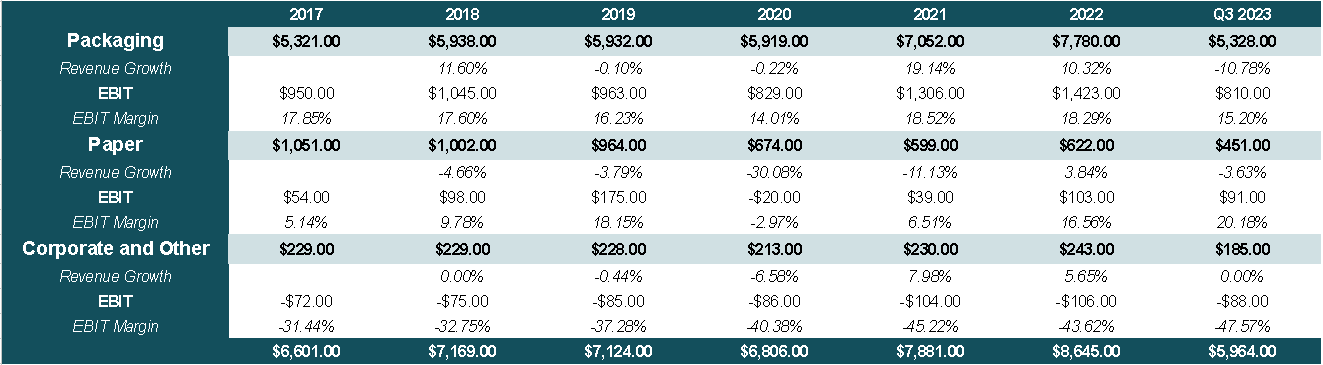

Analyzing the recent performance of each business line , we observe that both the 'Paper' segment and the 'Corporate and Other' segment (which is omitted due to its lack of relevance and consistent negative EBIT margins averaging -40% in recent years) have experienced either a decline or minimal growth annually. Conversely, the 'Packaging' segment has demonstrated robust growth, expanding by 8% since 2017. Notably, over the last 9 months, it has exhibited a remarkable 10% YoY growth. This acceleration can be attributed to the comparatively strong base in 2021 and 2022.

{kind=link}

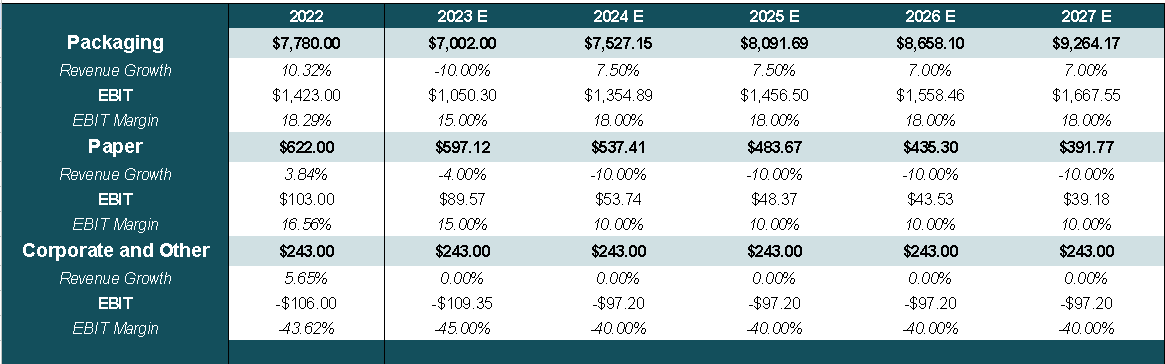

Looking ahead to FY2023, I anticipate a 10% decrease in revenues for the 'Packaging' segment, in line with the year-to-date trend. Additionally, I project that margins will dip below the historical average of 18%.

In the subsequent years, I expect the 'Paper' segment to persist in its decline, reflecting its diminishing importance within the overall business strategy. In 2017, it accounted for 15% of revenues, but it has since dwindled to just 7.5%. Meanwhile, the 'Packaging' segment is anticipated to resume growth at rates of 7-8% annually, maintaining average margins of 18%.

{kind=link}

While the disappearance of two out of three business lines may initially seem negative, it is anticipated to have a positive impact on the overall performance of revenues and margins. The increased predictability and focus on the 'Packaging' business are expected to drive growth, potentially representing 94% of revenues by FY2027.

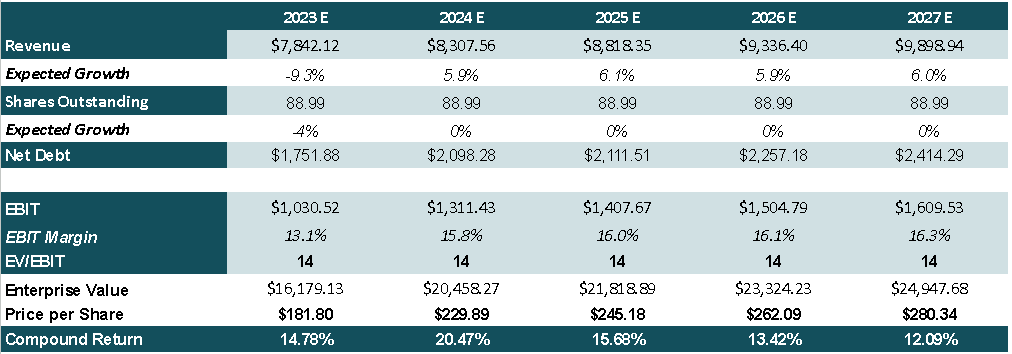

Considering the robust share repurchases undertaken in recent months and applying the average 14x EV/EBIT multiple observed above, the potential for annual returns of 12% over the next 5 years is plausible. This projection doesn't even account for the dividend, which currently yields 3%.

{kind=link}

Final Thoughts

Packaging Corporation stands as a stable business with predictable revenues, and beneath the surface, it is actively enhancing the quality of its operations by shedding unprofitable and lower-quality lines of business.

Considering the risk/reward ratio, the potential return of this business is compelling. Despite the initial impression that the multiple may not be excessively cheap, a closer look reveals that it trades in line with the sector average. However, key ratios suggest that it could be better managed or a higher-quality business compared to its peers.

Given these factors, I find a ' buy ' rating reasonable. While it may not be the fastest-growing company, it has the potential to deliver stable performance in the long term, with minimal surprises along the way.

For further details see:

Packaging Corporation of America: Valuation Is Justified By Its Quality