PACW - PacWest And Banc Of California Tie The Knot: And The Winner Is

2023-07-26 15:42:39 ET

Summary

- Shares of PacWest Bancorp fell by 27% on July 25th on rumors of a merger with Banc of California but later rose by over 30% after the market closed.

- The merger will create the fourth-largest mid-sized bank in California, with $36.1 billion of assets, and is expected to generate significant cost savings and boost annual net income.

- Despite the benefits of the merger, I think that PacWest is contributing more to the deal than it is receiving, making Banc of California the more favorable party in the transaction.

Talk about a roller coaster ride! On July 25th, shares of PacWest Bancorp ( PACW ) plummeted, closing down 27% on rumors that the company was going to be acquired by or merged into Banc of California ( BANC ). The assumption by the market seems to have been that this would be a take under aimed at preventing the bank from failing. After all, the business did struggle a bit because of the contagion that wracked the banking industry earlier this year. These fears were almost certainly exacerbated by the fact that the rumor came on the same day that both financial institutions reported updated financial results.

While PacWest suffered during the first quarter of the year compared to how it performed at the end of 2022, Banc of California performed quite well. So it's likely that market participants saw this maneuver as a rescue operation that could lead to shareholders of PacWest walking away with very little to show for their investments. However, after the market closed, shares of the enterprise shot up over 30%, at one point trading even higher than that. After seeing its own shares close up 11.2% on July 25th, Banc of California moved up a further 8.8% in after-hours trading as well. Sure enough, a merger between the two companies was announced . But it was not such a lopsided deal like market participants seemed to have feared. This is not to say that there was no disparity between the parties. In my view, Banc of California most certainly walked away with the better side of the arrangement. But compared to what the deal could have been, I don't see this as particularly bad for anybody.

A look at recent financial performance

As I mentioned, both financial institutions reported results covering the second quarter of their 2023 fiscal years after the market closed on July 25th. My goal is not to focus too much on those details but, to instead, focus on the merger between the parties in question. However, there are a couple of highlights from the earnings releases that I believe will help put my broader discussion into perspective. Let's begin with PacWest.

The most important thing in the banking sector this year has been the value of deposits. Large amounts of uninsured deposits stoked fears that a bank run could kill some of these financial institutions. And that is precisely what happened to some. Up to this point, PacWest was largely spared, but shareholders did pay a hefty price. Prior to the after-hours move higher, shares of the enterprise were down 71.7% over the past year. A lot of this pain was driven by two primary factors.

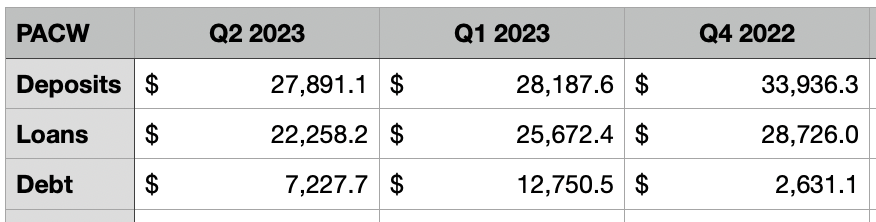

{kind=link}

The first of these was a rather sizable drop in deposits from the end of 2022 to the end of the first quarter of the year. Deposits declined from $33.9 billion to $28.2 billion. And much of this decline was associated with the aforementioned uninsured deposits on its books. In fact, overall insured and collateralized deposits currently account for 81% of all the company's deposits. But at the end of last year, this number was only 48%. Even though investors were concerned that the second quarter might see deposits plunge further, the drop was far more modest. By the end of the quarter, they came in at $27.9 billion. Although painful, it's really a decline of only 1%, or $290.5 million.

Debt has been another concern. As deposits left these banks, pressure built to sell off assets, primarily loans, in order to cover the outflows. While PacWest did sell off some of its loans, taking their total value down from $28.7 billion at the end of 2022 to $25.7 billion at the end of the first quarter and down further to $22.3 billion at the end of the second quarter, the company did also take on a significant amount of debt. Total borrowings at the end of 2022 were $2.6 billion. These increased to nearly $12.8 billion by the end of the first quarter. The good news is that management was successful in reducing debt to some degree by the end of the second quarter. During that time, the metric dropped to $7.2 billion. The aforementioned sale of loans most certainly helped in this regard. But the firm does need to make further progress in this regard because the debt on its books is eating away at its net interest margin. By the end of the first quarter, the net interest margin for PacWest was 2.89%. This was cut further to 1.82% by the end of the second quarter.

{kind=link}

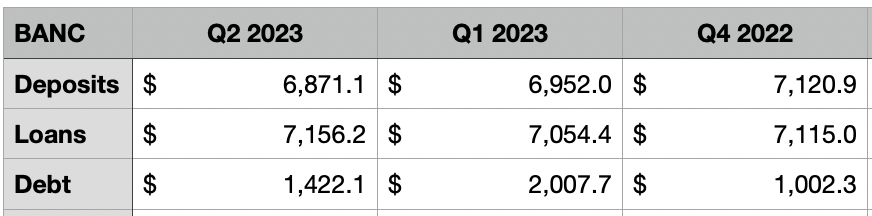

By comparison, Banc of California has held up much better. It is true that deposits have fallen, first from $7.12 billion at the end of last year to $6.95 billion by the end of the first quarter. They fell further to $6.87 billion by the end of the second quarter. But compared to what PacWest has dealt with, this is a minor dip. Over this window of time, loans actually increased for the company, climbing from $7.12 billion to $7.16 billion over the course of six months. And this was in spite of the fact that debt for the company also increased, climbing from $1 billion to $1.42 billion. However, that second reading was actually down from the $2.01 billion reported at the end of the first quarter. So management has been able to keep loans elevated and has been able to reduce debt without seeing a decrease in its loan portfolio.

A look at the terms

As I mentioned previously, it seems as though the market was expecting a take under of PacWest. But that's not exactly what happened. To begin with, it's important to note that, the transaction in question is all stock. For each share of PacWest that an investor owns, said investor will receive 0.6569 of a share of Banc of California when the deal closes. Following the completion of the deal, shareholders of PacWest will own 47% of the combined company. Meanwhile, shareholders of Banc of California will own 34%.

If you're quick with math, you would understand that this is only 81%, meaning that 19% is missing. That's because the rest of this is going to other parties. 16% is going to Warburg Pincus or entities controlled by it, while the rest is going to parties controlled by a firm called Centerbridge. Combined, these two entities are contributing $400 million in equity in the form of cash to help with the transaction.

Instead of receiving nothing but common units, they will receive 21.8 million common shares and 10.8 million common equivalent shares that will technically be considered fixed rate reset non-cumulative perpetual preferred stock that converts into common shares on a one-for-one basis. These units carry with them a 7.75% return. While this is great for them in and of itself, they are also receiving warrants that grant them the ability to buy 15.9 million common shares of the combined company with an exercise price of $15.375 apiece. They carry a seven-year term but must be exercised if common shares of the combined enterprise reach or exceed $24.60. As an example of how this might play out, if shares of Banc of California eventually hit $24.60 each, the extra payoff for these investors will be about $195.6 million.

{kind=link}

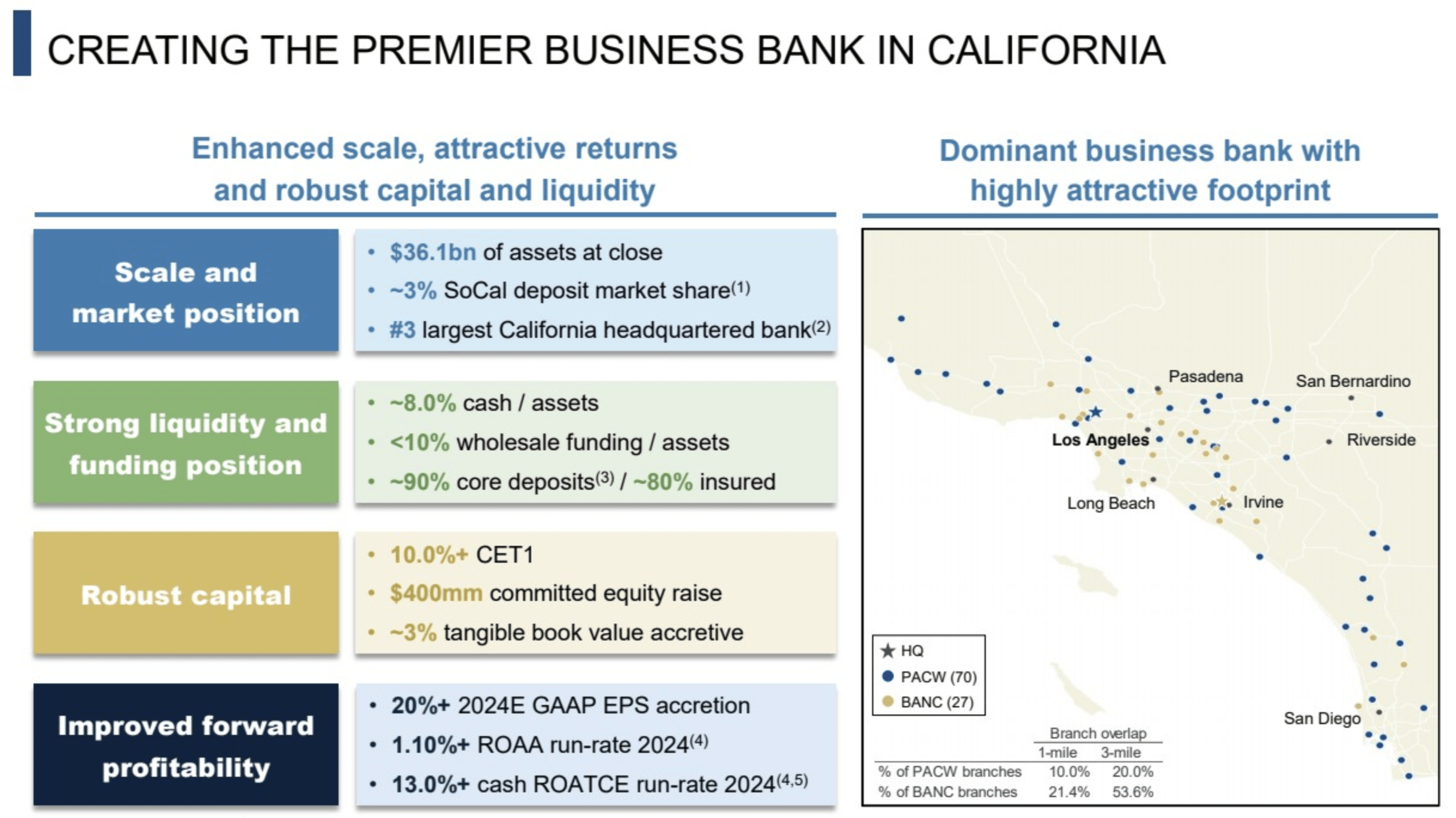

There are multiple legitimate reasons why this transaction might be pursued. For starters, the transaction will turn the combined enterprise into the 4th largest mid-sized bank in California. At close, the institution will have $36.1 billion of assets on its books. And it will also have a significant geographic overlap that opens the door for meaningful cost savings. Part of the cost savings should be an improved net interest margin. Earlier in this article, I talked about how this metric had changed for PacWest. While it had a net interest margin as of the end of the most recent quarter of 1.82%, Banc of California had one of 3.11%. This means that for every $1 billion in assets, Banc of California generates about $12.9 million in net interest income more than what PacWest currently does.

{kind=link}

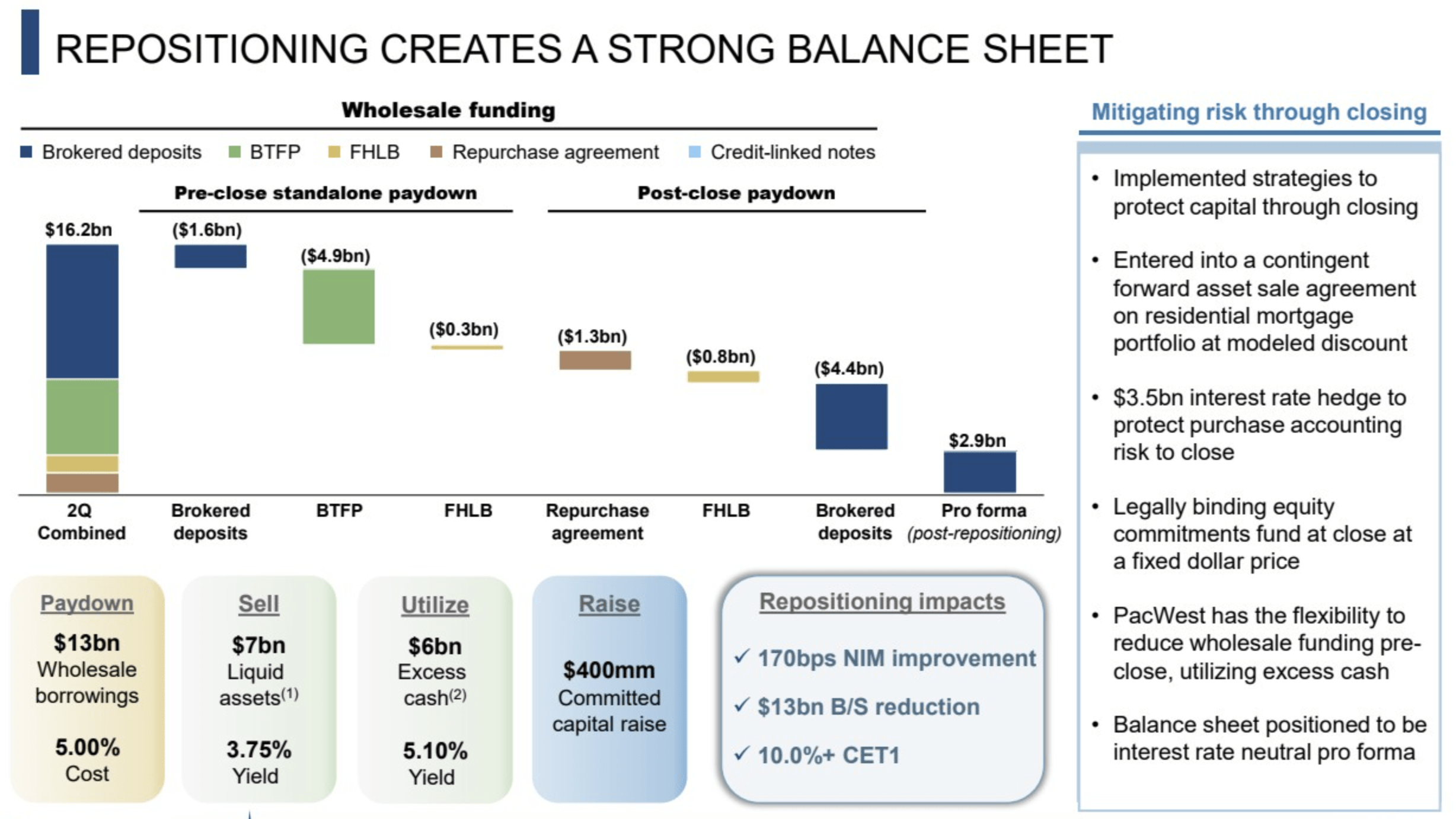

This will come largely from debt reduction, with management paying down $13 billion of wholesale borrowings with a weighted average cost of 5% per annum. $400 million of this will come from the aforementioned minority partners. However, the company also is going to accomplish this by selling about $7 billion of liquid assets that have a weighted average yield of 3.75% and by utilizing $6 billion in excess cash that has a 5.1% yield. The combined company will also take on a $3.5 billion interest rate hedge aimed at protecting itself from further interest rate fluctuations. These maneuvers should help increase the net interest margin for PacWest's assets by 1.7%. This should translate to $90 million of additional net interest income per annum.

{kind=link}

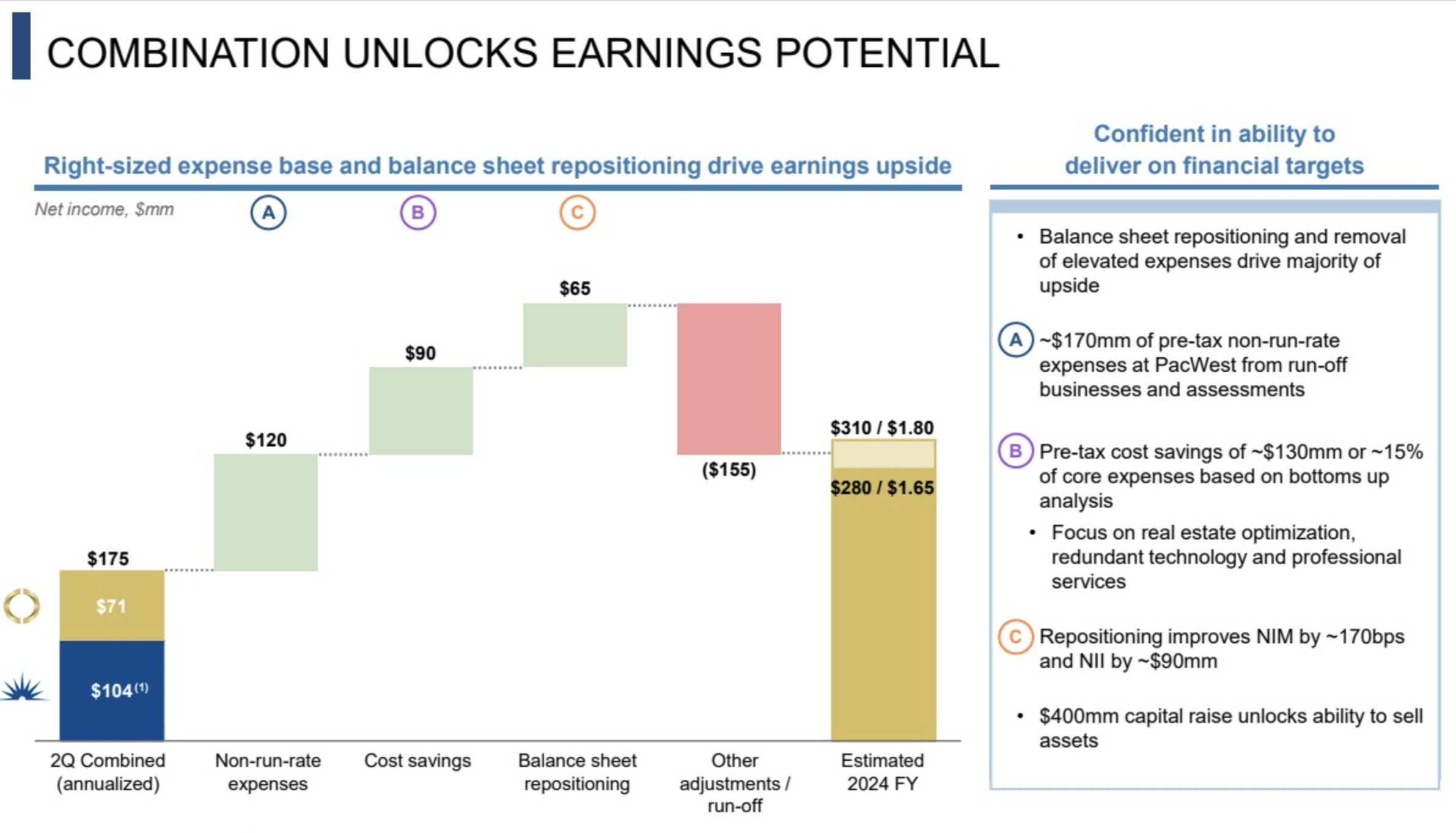

There will be other financial benefits to this maneuver also. Management is also targeting $170 million of pre-tax non-run-rate expenses associated with PacWest that should come off the income statement as certain assets are divested. And on top of this, the firm is targeting pretax cost savings of $130 million thanks to real estate optimization, eliminating redundancies in its tech stack, and when it comes to consolidating professional services. Though management did not state this, the combined company will likely have a smaller audit bill and smaller tax services bill than if the two enterprises remained separate. All combined, these changes should help boost annualized net income for the company from $175 million to $310 million by 2024. It is worth noting that these savings will bring with them certain one-time expenses. Including capital and hedging fees, management is expecting $280 million of pre-tax, or $215 million post-tax, worth of costs.

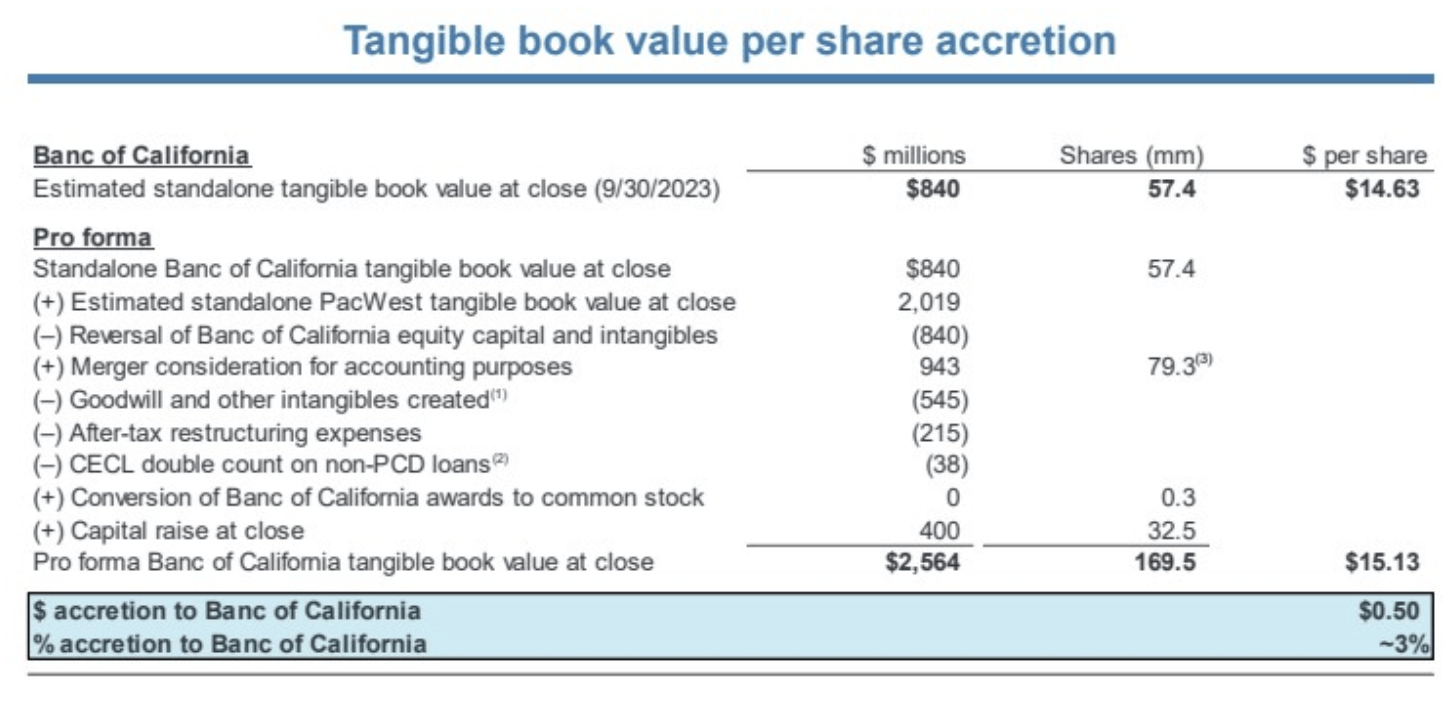

In general, I view this deal as beneficial for both parties. But I have no doubt that Banc of California is getting the better end of the transaction. Using the tangible book value per share calculations that PacWest and Banc of California provided in the investor presentation, it becomes clear that Banc of California is bringing 32.8% of the tangible book value into the combined company and receiving 34% of the value of it in return. This should bring its tangible book value per share up from $14.63 to $15.13. The incoming investors get an even better bargain, bringing in only 15.6% of the value to the deal and yet receiving 19%. And that excludes the value of the warrants. By comparison, PacWest is bringing in 51.6% of the value and receiving only 47%.

{kind=link}

It is important to note that the calculations provided by management factor in all of the restructuring activities, debt reduction, and other items that have been pointed out as being necessary to achieve and optimal operation. But if we cut all of that out, we do get a slightly different picture. If we look only at the estimated tangible book value of both companies as standalone enterprises and look at the $400 million of incoming capital, we find out that Banc of California is bringing 25.8% of the value to the deal, while the incoming investors are putting in only 12.3%. That means that PacWest is contributing 61.9% for the 47% of the combined company that it's receiving. This is not to say that the deal should not be done. Given some of the other factors that I spoke about earlier in the article, it is clear that Banc of California is a more stable enterprise and one that is generating more significant profits from its smaller asset base. But in theory, if PacWest could continue to pay down debt and work on its own capital structure, the end result would probably be more positive for it than this merger would be in my opinion.

Takeaway

In general, I feel like PacWest and Banc of California are both interesting prospects with attractive upside potential. This transaction looks set to create attractive value across the board. If I were an investor in PacWest, I would prefer that it remains separate given how much extra it's giving as part of the deal. But I can also understand, given the totality of the circumstances, why the company is heading in the direction that it is. In all, I have decided to rate both of these enterprises a 'buy' because, like many of the other players in the banking sector right now, they look attractively priced.

For further details see:

PacWest And Banc Of California Tie The Knot: And The Winner Is