JPM - PacWest Bancorp Plummets On Renewed Solvency Concerns

2023-05-03 20:33:08 ET

Summary

- Shares of PacWest Bancorp came under significant pressure after concerns arose about the company's ability to stay afloat.

- The picture definitely is riskier than I believed it to be prior to new data coming out, but it is not as bad off as First Republic Bank.

- Although I'm taking a neutral stance on the firm, there's no denying that it's a very binary prospect at this time, and investors should be cautious.

May 2nd proved to be a particularly painful day for shareholders of regional bank PacWest Bancorp ( PACW ). After news broke that First Republic Bank ( FRC ) was being absorbed by JPMorgan Chase & Co. ( JPM ) in a bid aimed at ending the banking crisis, shares of the company plunged, closing down nearly 28%. The fear here is that this particular enterprise could be the next shoe to drop. This follows the most recent earnings release provided by management. While I definitely will not say that this fear is baseless, I do believe that a lot of the panic surrounding this name is unwarranted. Yes, the company has faced a good deal of pressure over the past couple of months. And based on the most recent quarterly data, it is possible that further pressure could be applied. As a smaller bank, PacWest Bancorp is also more vulnerable than if it were a larger player, but the data available today suggests to me that it is in far better shape than First Republic Bank was before its collapse.

Fears are mounting

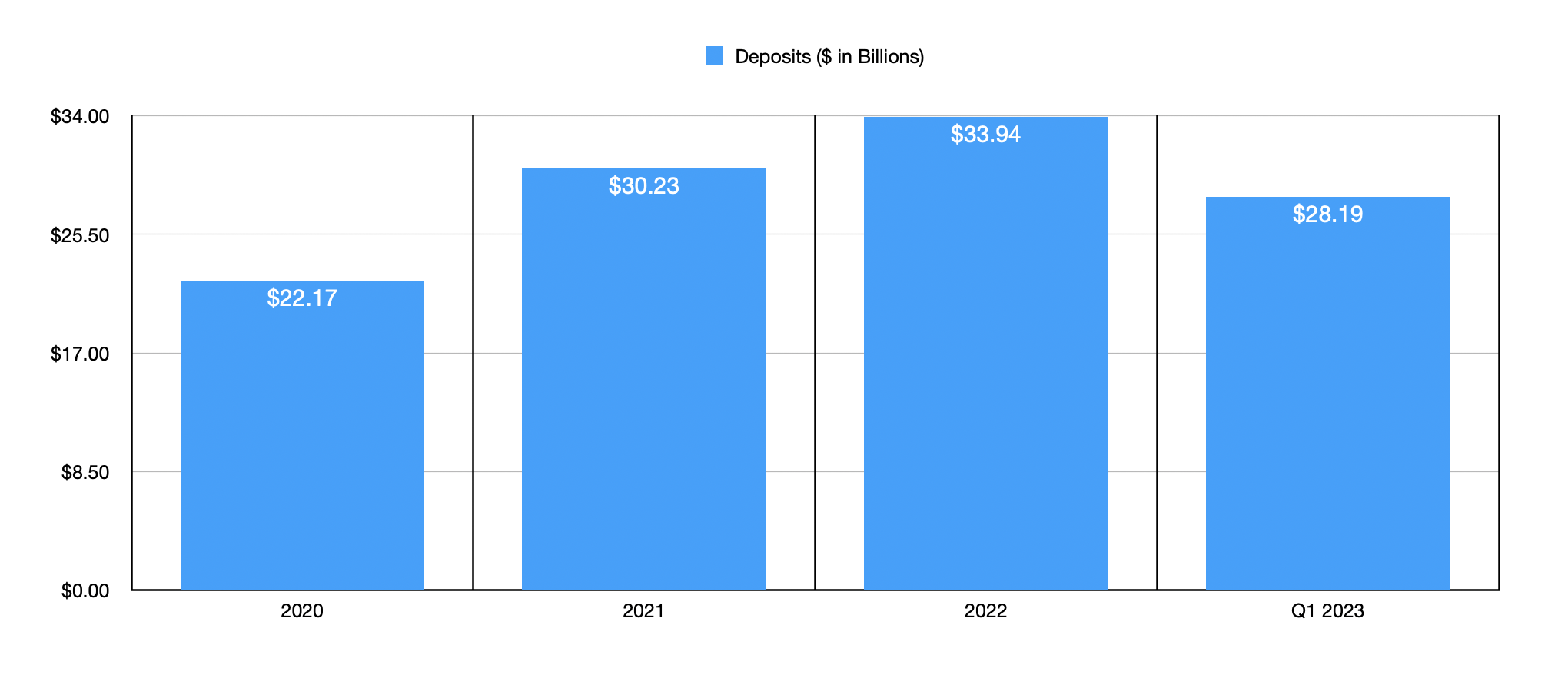

In an article that I published the other day, I made the case that the decision by JPMorgan Chase to acquire First Republic Bank essentially ended the banking crisis. To some at this point, this statement may seem premature. However, I do believe that my original statement will turn out to be more or less accurate. This is not to say that every bank will survive the current turbulence. But it does mean that I believe that the larger regional banks that have collapsed are the only ones that will. By comparison, PacWest Bancorp is a fairly small player. This much can be seen in the deposits that the company has, totaling $28.19 billion as of the end of the most recent quarter . By comparison, First Republic Bank had deposits of $92.4 billion.

{kind=link}

Regardless of this size difference, it cannot be denied that significant concerns now exist regarding the ability of PacWest Bancorp to survive in this environment. The good news is that we do have a good deal of recent data to rely on in order to help us assess this situation. As I mentioned already, deposits at the end of the most recent quarter were $28.19 billion. This is down, but not all that much from the $33.94 billion reported one quarter earlier. Of course, it's not the total deposit figure that actually matters. Rather, it's the amount that's uninsured that's important. Management pegs this number at about $8.1 billion. That's less than half the $17.8 billion in deposits that the company had at the end of the 2022 fiscal year and is down from the $22.5 billion seen at the end of 2021.

Absent intervention from the FDIC, the uninsured deposit amount is the total amount on the company's books that creates a risk of a bank run. So the question of whether or not the company is truly in crisis from a fundamental perspective depends on its ability to cover this amount, plus recent borrowings that it has taken out aimed at bolstering its balance sheet. If it can do this without a significant deterioration in its book value, it can survive and even go on to thrive from here. If it can't, it's destined to go the way of First Republic Bank and a few other names.

{kind=link}

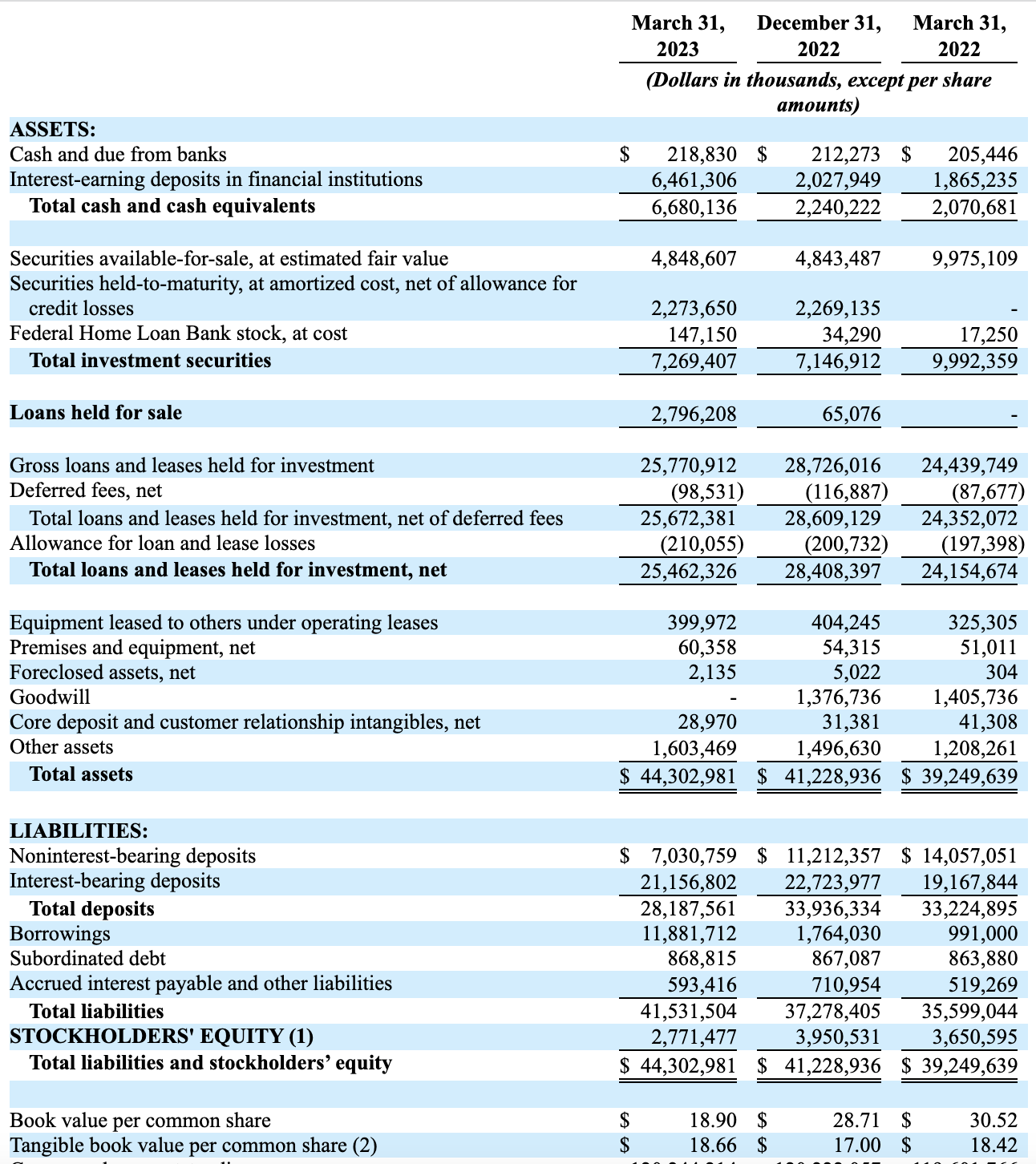

If we look at cash and cash equivalents on the company's balance sheet, as well as available for sale securities, we end up with about $11.53 billion that the company has. It also has $2.42 billion in securities that are classified as held to maturity, inclusive of $147.15 million of Federal Home Loan Bank stock. Naturally, selling any of these securities that it has on its books, totaling $7.27 billion in all, would likely result in a haircut. But the fact that the majority of these assets are classified as available for sale suggests that the company has been planning to have them as liquid assets if it needs them. Add on top of this another $2.80 billion in loans held for sale, as well as $25.46 billion in loans and leases that are held for investment, and the company has a tremendous amount of assets to work with. The problem, however, is that selling many of these will result in losses, especially if the company needs to make the sales in short order. But at least we know what the business has at its disposal.

{kind=link}

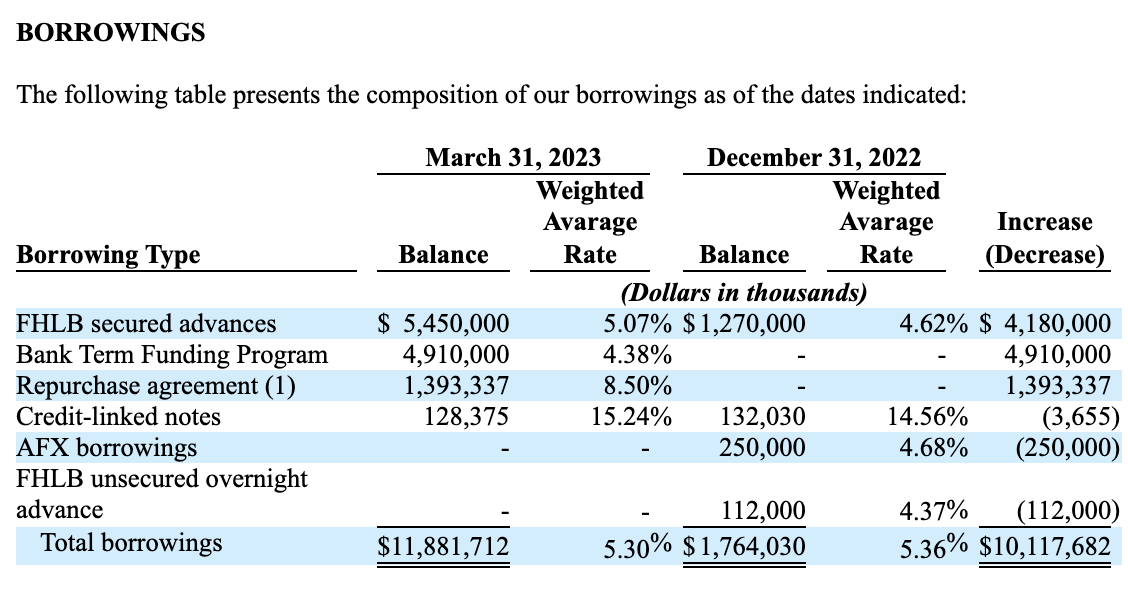

By the end of the most recent quarter, PacWest Bancorp had borrowings of $11.9 billion. This was on top of $868.82 million in subordinated debt. But it's really the borrowings on its books that the company needs to worry about paying back. This is for two reasons. For starters, these are amounts that are not meant to be on its books for a very long time. And second, they carry a rather lofty weighted average interest rate of 5.30%. By comparison, the company's assets during the most recent quarter generated A weighted average return of 5.35%. If a wash seems okay with you, consider that the company's net interest income of $281.63 million during the first quarter of the year was based on the average balance of its various accounts. Borrowings for that time were only $5.29 billion. So we have seen more than a doubling on that front alone. This means that, moving forward, the toll on the company's bottom line will be even greater if it doesn't pay back its borrowings.

In order for the company to survive, we need to understand that it must pay back the $11.9 billion in borrowings, plus be able to cover up to the $8.1 billion and uninsured deposits on its books. All combined, this is about $20 billion that's required. If we take only the most liquid assets being those that involve cash and cash equivalents, as well as available for sale securities, we end up with $11.5 billion. This means that, without tapping into its longer-term investments like its loans, the company has in north capital, without borrowing more, to cover nearly 58% of the sum of its uninsured deposits and borrowings. For First Republic Bank, this number was less than 13%. At the end of the day, this creates a much safer picture for PacWest Bancorp. But it by no means erases the probability that the company could ultimately go into receivership.

Takeaway

Right now, the picture for PacWest Bancorp stock is riskier than it was when I wrote about the company in late March. Market sentiment is most certainly working against the enterprise, which may cause a further flight of assets. This is not to say that the business will share the same fate as First Republic Bank and other financial institutions that collapsed earlier this year. But it does create a situation where risk is elevated. Given these facts, and in spite of the fact that shares of the business do look a lot cheaper now than they did when I last wrote about it, I have decided to downgrade the company from a ‘buy’ to a ‘hold’, with the qualifying statement that this truly is a binary prospect at this moment that could go on to generate significant upside or could experience a complete loss like First Republic Bank did.

For further details see:

PacWest Bancorp Plummets On Renewed Solvency Concerns