PACWP - PacWest Bancorp: Q1 Results Are Proof That Preferred Shares Are Too Cheap To Ignore

2023-04-27 12:46:04 ET

Summary

- PacWest Bancorp is a California-based bank. Due to its geographical footprint, it has been wrongfully associated with names such as Silicon Valley Bank and Federal Republic Bank.

- The bank has just posted strong Q1 results, and executives have skillfully handled last March's difficult situation while maintaining good communication with the shareholder base.

- PACW Preferred shares yield 13% and have considerable upside to face value. I rate PACWP a strong buy with the potential for a 30% annualized return over a three-year holding.

Last month, the Fed discovered that hiking rates at the fastest pace in history is not exactly problem-proof. The most risk-prone operators in the banking sector got caught swimming naked, and the ensuing turmoil caused a few casualties, namely Silicon Valley Bank ( SIVBQ ) and Signature Bank ( SBNY ). One more seems to be in the making, with First Republic Bank ( FRC ) reportedly struggling to sell assets in a last-ditch effort to shore up its balance sheet.

As it often happens, the troubles of a few names have triggered an industry-wide sell-off in the markets that smells like an opportunity to those astute investors who can identify the babies being thrown out with the bathwater. Last month, I highlighted an opportunity in micro-cap bank First Guaranty Bancshares Preferred ( FGBIP ). In this article, I am continuing the series by drawing investors' attention to PacWest Bancorp's ( PACW ) non-cumulative Preferred series A ( PACWP ), another issue which I believe has a superior risk-reward profile.

Investment Thesis

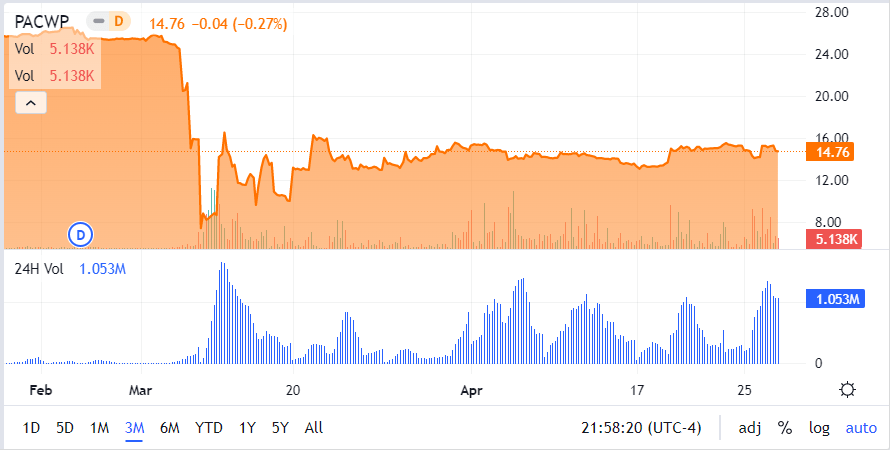

The investment case for PACWP is quite straightforward. This is a Preferred issue that currently trades around $15, well below its $25 face value. The reason for the drop is entirely guilt by association for PacWest Bancorp because shares traded at par up until the SIVB debacle and ensuing panic. Being Los Angeles-based and having some exposure to VC deposits did not help PACW one bit. Fast forward one month, the Preferred shares have somewhat recovered from all-time lows but still trade at a 40% discount to par. In the meantime, risks have also come down considerably from the uncertainty nadir of mid-March, hence still representing a highly attractive risk-reward adjusted opportunity.

{kind=link}

The present yield is still about 13% based on a $0.4845 quarterly payout, translating into a $1.938 annual dividend. The dividends are at minimal risk of suspension, the danger being limited to extremely volatile market conditions, new bank runs, and mass deposits fleeing for safety.

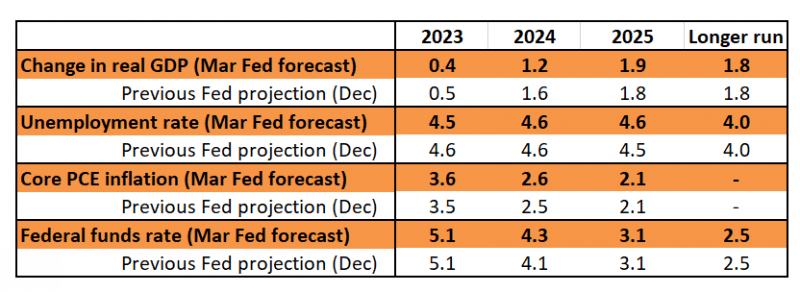

At par, the issue yields 7.75%. Since expectations are for the federal funds rate to peak slightly above 5% during 2023, then gently descend again towards 3% by the end of 2025, I see no reason for the preferred issue not to trade around that level again within two-three years. The spread offered over money market funds by then would be more than enough.

{kind=link}

Even without an immediate recovery, I project that buying at $15 today should yield an annualized three-year return of approximately 30% by collecting dividends and unloading shares at their fair value (face value). I rate shares a STRONG BUY.

Admittedly, I purchased shares for myself at a lower level during the March turmoil. At that time, I was impressed by PACW management’s transparency. During those busy weeks, executives took the time to reassure investors and came out with weekly updates on the business status on three separate issu es: March 10 , March 17 , and March 22 . The confidence shown, together with active buying by several insiders gave me the courage to commit significant capital during the March 17 sell-off. As I now must decide whether this was a successful short-term trade or a longer-term commitment, I am confident in choosing the latter because a lot more upside is likely ahead. Although the absolute total return has lowered, the adjusted risk-reward profile seems largely unchanged compared to last month. This is because in the meantime, PACW has smashed Q1 consensus estimates and provided an even more detailed update to investors, proving that the damage to its banking franchise is not nearly as bad as thought.

PacWest Bancorp Q1 results

During Q1 2023, revenues declined by 4.6% to $318 million, representing a slight beat of $6 million to consensus. The real knockout was earnings, coming at $0.66 per share, or 16% ahead of the $0.57 consensus. First news: PACW is still a profitable bank, and more profitable than Street analysts expected. But it gets even better. Compared to the last update provided when deposits stood at $27.1 billion, the total increased by $1.1 billion to $28.2 billion at March 31, 2023. In the following three weeks, an additional influx of $0.7 billion puts the likely actual amount at approximately $29 billion. While the level is still below December 31, 2022, it is obvious that the trend has reversed, and customers are coming back.

FDIC-insured deposits were approximately 73% of the total, significantly up from 48% at the end of the previous quarter. Available liquidity (which includes unused borrowing capacity) amounted to $12.4 billion, 153% of the uninsured deposits. Using the borrowing capacity would eventually represent a significant cost impacting the bank’s profitability but at least protects PACW from worst-case scenarios and ensures medium-term business survivability. Finally, the CET1 ratio of the bank improved from 8.7% to 9.2%, and unrealized losses on the Company’s investment portfolio declined by 7.7%.

The NIM declined to 2.89% compared to 3.41% for the fourth quarter of 2022 as the result of NII totaling $279.3 million vs. $322.9 million in Q4 2022. The metric will need to be monitored in the next quarter as the full extent of the funding mix shift happened in March 2023 and will appear in the bank’s upcoming results. This will be partially offset by the increase in borrowing interest going forward, and so I expect the next quarter to potentially mark the bottom.

Paul Taylor, PacWest President, and CEO, provided an upbeat commentary as well, in which he reaffirmed confidence for deposits to further come back in the upcoming quarters and further improve CET1 above the 10% mark (our emphasis added):

“ As we look forward, we continue to execute on our overall strategy, which includes managing the balance sheet around a stable and diversified funding mix, emphasizing our core business, preserving profitability with a strong asset base and reduced costs, and maintaining our capital and liquidity positions while prudently managing risks. We expect that our total assets will be closer to $35 billion within the next few months , after we complete certain asset sales and bring down liquidity to more normal levels. These actions will improve our liquidity position and are expected to increase our CET1 capital ratio to above 10% .”

Risks to the thesis

It is impossible to know for sure whether we have seen the worst part of this banking crisis yet. While the Fed cannot be blamed for the opportunistic, risk-prone behavior that ultimately caused the demise of certain operators, it is also true that its rate-hiking policy has been one of the most aggressive seen in decades. However, strong arguments can be made for expecting more accommodating moves going forward, and even a pivot in the second half of the year.

Excluding a new major flight to safety, which I view as unlikely given that now over 70% of PACW deposits are federally insured, the bank is in a position to continue to operate profitably. FY23 expectations still sit at $1.90 per share with no revision made by the Street yet. However, based on Q1 results, it is possible to see a 10%-20% upward revision, with expectations that PACW can earn more than $2 per share this year. However, NII will need to be further monitored in the coming quarter, and if the bank stops operating profitably, obviously both common and preferred dividends are at high risk. Beware that being a non-cumulative issue, if the bank stops paying dividends on the common, it makes sense to forego payments on the Preferred as well (the only damage being reputational). If the bank cancels its common distribution, there is no obligation to repay non-cumulative Preferred holders in the future for missed payments.

Investor takeaway

PACW has just reported strong financial figures for Q1 2023, and its deposit situation continues to normalize. Its common and preferred shares are, however, a long way from where they were prior to March 2023. With PACW shares trading at about $11, down 67% for the year and 50% YTD, the bank now trades at approximately 5x expected forward earnings. The common shares seem attractive as well here, and notably investors of the caliber of Bill Gross also stepped in buying shares. However, I’d argue that the preferreds are a better pick here for a few simple reasons:

- In times of economic uncertainty, moving up the capital ladder is never a bad idea.

- The upside to face value is huge, and it provides for a strong valuation floor.

- A new emergency could potentially translate into the necessity for PACW to raise capital and dilute the common shareholders. This would be a positive for PACWP owners, as long as the bank can quickly regain a certain degree of profitability. Before even paying $0.01 to holders of the common, the preferred must receive $1.938 per annum.

PACWP is the only Preferred issued by PACW and it costs approximately $40 million per year. This is not an overly burdensome issue for the bank. With PACWP shares trading close to $15, I expect investors to bank a 30% annualized return by 2025 or alternatively keep in their portfolios a steady 13% yielder.

For further details see:

PacWest Bancorp: Q1 Results Are Proof That Preferred Shares Are Too Cheap To Ignore