FRC - PacWest Bancorp: The Sell-Off Looks Overdone

2023-03-29 14:59:28 ET

Summary

- The slide in PacWest stock price seems to be unjustified.

- The extent of PacWest's exposure to uninsured deposits and unrealized losses on its HTM portfolio is significantly lower than one of its larger regional peers under scrutiny, First Republic.

- The bank likely has better liquidity management practices as evidenced by relatively larger liquidity buffers.

- A haircut on venture capital-related loans does not seem to be a base case implication of PacWest's path towards return to normalcy.

The name of PacWest Bancorp ( PACW ) has been splattered across headlines as one of banks facing strain on its deposits ever since the US banking sector was shaken by the collapse of Silicon Valley Bank ("SVB") on Mar 10, 2023 and Signature Bank on Mar 12, 2023. The crisis unfolded with real-time sharing of knowledge on potential vulnerabilities of various banks across a population connected to social media, amplified by algorithms. As wary depositors started moving their funds from smaller regional banks to larger too-big-to-fail nation-wide banks in a bid to safeguard their cash, stock market investors started making bets on the next dominoes to fall. It was not too long before attention zoomed-in on banks like First Republic Bank ( FRC ) and PacWest apparently due to their larger reliance on uninsured deposits, a geographic footprint more heavier in California and an exposure to the venture capital industry in the form of deposits and loans.

The ensuing sell-off has brought First Republic stock price down 89% and PacWest stock price down 66% from their closing level on March 3rd, just prior to the SVB fiasco. This compares with just a 13% decline in the Financial Select Sector SPDR ETF ( XLF ) over the same period. It's tempting to think that First Republic and PacWest stocks may be priced for a worst-case bank failure scenario and their stock price could sharply rebound when investor nerves get calmed down. Below is my take on separating fact from fiction on the PacWest story to help any investors looking for a hidden gem in the rubble of the SVB crisis. I will not go too much into First Republic's prospects as it has already been analyzed quite well by SA Contributor Siyu Li here and here .

Sizing up the Scale of the Bank Run

To put PacWest's situation in the context of regional banks, it's helpful to make a direct comparison with First Republic which was a bigger player in the regional banking space and faced far more of the deposit withdrawals onslaught as well as the stock price pummelling.

PacWest had total assets of $41 billion as of Dec 2022 which were just under 1/5th of First Republic's $213 billion total assets.

PacWest has borne a deposit outflow of 20% per management disclosures which is dwarfed by First Republic's losing nearly half of its deposits based on unconfirmed media reports.

First Republic lost roughly $70 billion in deposits in recent weeks - nearly half of its total depositor base as of the end of last year - said two people with knowledge of the matter

Source: New York Times, March 20, 2023

PacWest has gone to the Fed Discount Window and other facilities to shore up its liquidity by up to $17.7 billion (details below) which is far smaller than the approx. $149 billion in liquidity drawn by First Republic from various sources.

PacWest liquidity draws

Source: 8-K filing Mar 22, 2023 (PacWest Bancorp website)

First Republic liquidity draws

Source: 8-K filing Mar 16, 2023 (First Republic website)

All said and done, apparently outflow of deposits from regional banks to larger banks has slowed down and all of the above is old news now. However, with stock prices of these banks still under pressure, the comparison serves as a good yardstick to gauge the extent of damage.

PacWest Story

In my opinion, depositors' behavior in response to fears of contagion from the ill-fated SVB has been informed by a handful of rules-of-thumb namely:

- Higher Dependence on Uninsured Deposits

- Venture Capital Connection

- Solvency Concerns

- Poor Liquidity Management

Higher Dependence on Uninsured Deposits

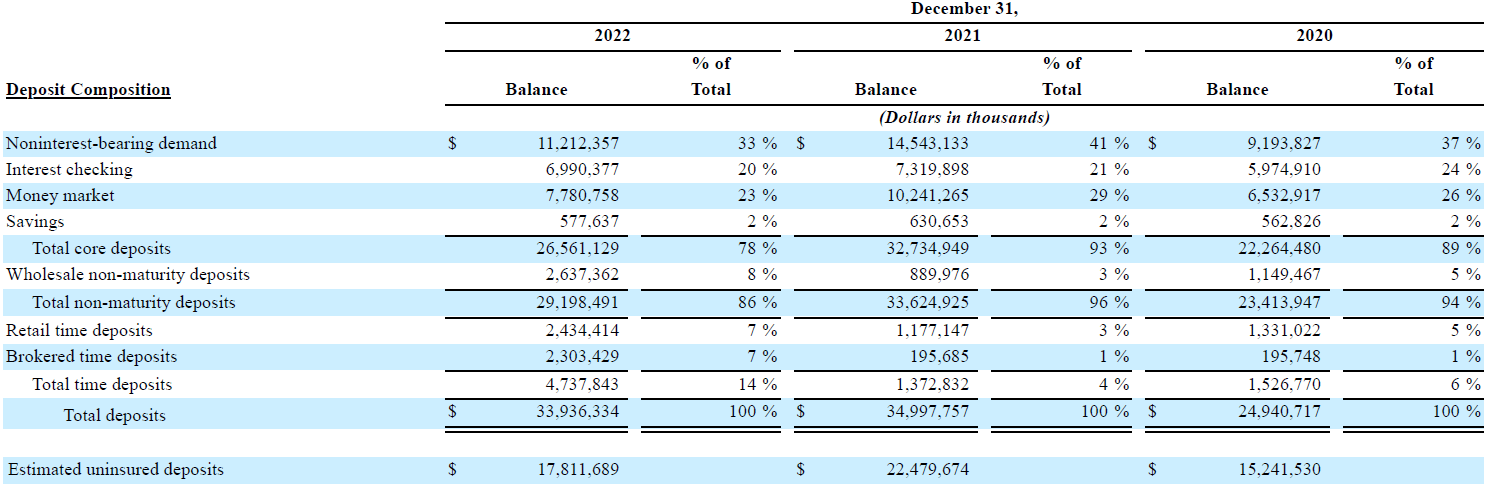

Uninsured deposits became the Achilles heel in the recent banking jitters because depositors were rightly concerned that deposits above the $250,000 FDIC insurance threshold were at risk in case of a bank failure. For anyone running a screen on banks reliant on uninsured deposits, it's not difficult to stumble upon PacWest which had 52% of deposits in the form of uninsured as of Dec 2022 as shown here:

Source: 2022 10-K report (page 78) (PacWest Bancorp website)

{kind=link}

The ensuing spree for moving uninsured deposits to other banks reduced the level of PacWest's uninsured deposits to just 35% of the total as of Mar 20th (per 8-K filing of Mar 22nd). Moreover, the filing shows that the bank is now braced to absorb further uninsured deposits withdrawals with a cash balance sufficiently covering approx. 120% of its remaining uninsured deposits. As noted earlier, the bank has shored up liquidity by drawing on liquidity facilities like the Federal Reserve discount window, the recently launched Bank Term Funding Program, Federal Home Loan Bank and most notably from private sector in the form of a new senior asset-backed financing facility from ATLAS SP Partners.

Venture Capital Connection

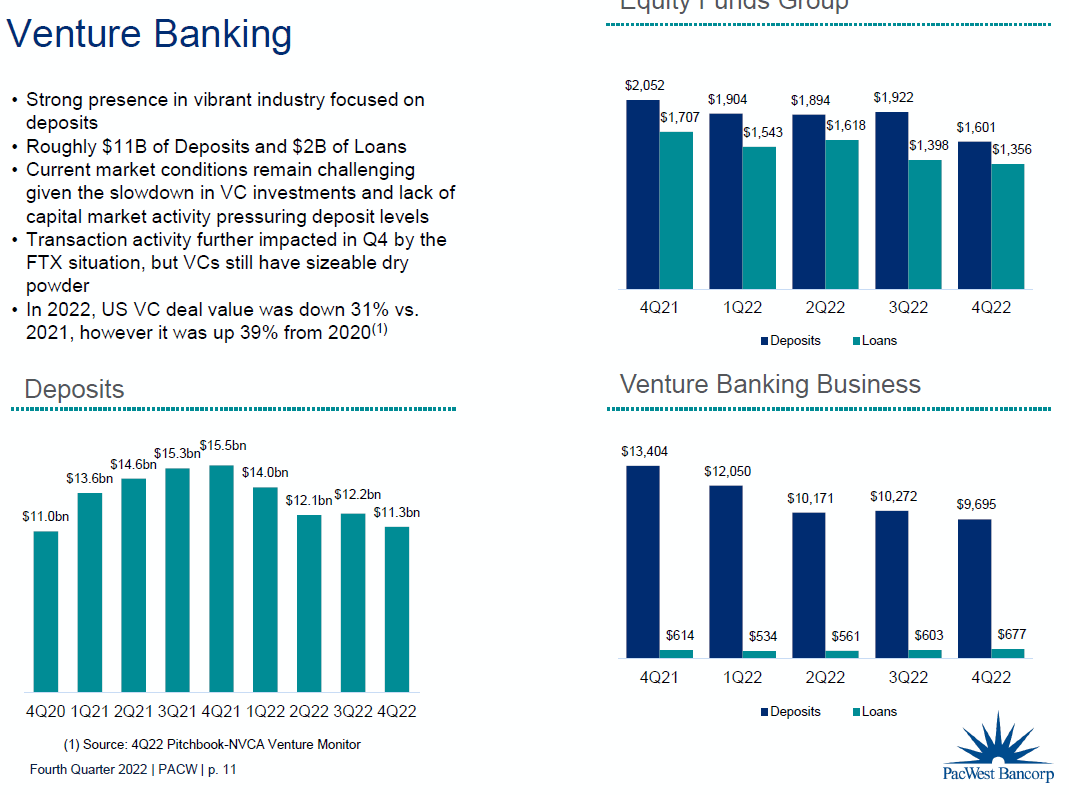

Many people would have singled out PacWest as similar to SVB in terms of doing a lot of business with California's venture capital industry.

Labeling PacWest as a bank of the venture capital industry was not an overstatement given that it is headquartered in Los Angeles, California with full-service branches throughout California and in Durham, North Carolina and Denver, Colorado and a significant concentration of collateral properties located in California. In hindsight, it seems that the venture capital funding drought which started in 2022 was a blessing in disguise for PacWest because its venture banking deposits recorded a 27% Y-o-Y decline during 2022.

Source: 4Q-2022 Results Presentation (PacWest Bancorp website)

{kind=link}

After this Y-o-Y decline, venture banking deposits were 33% of the total as of Dec 2022 and fell further to just 24% of the total by Mar 20th after facing a 43% decline in less than three months. In the meanwhile, other categories of deposits like community bank and wholesale deposits held-up quite well during the recent rush of deposit withdrawals.

8-K filing Mar 22, 2023 (PacWest Bancorp website)

{kind=link}

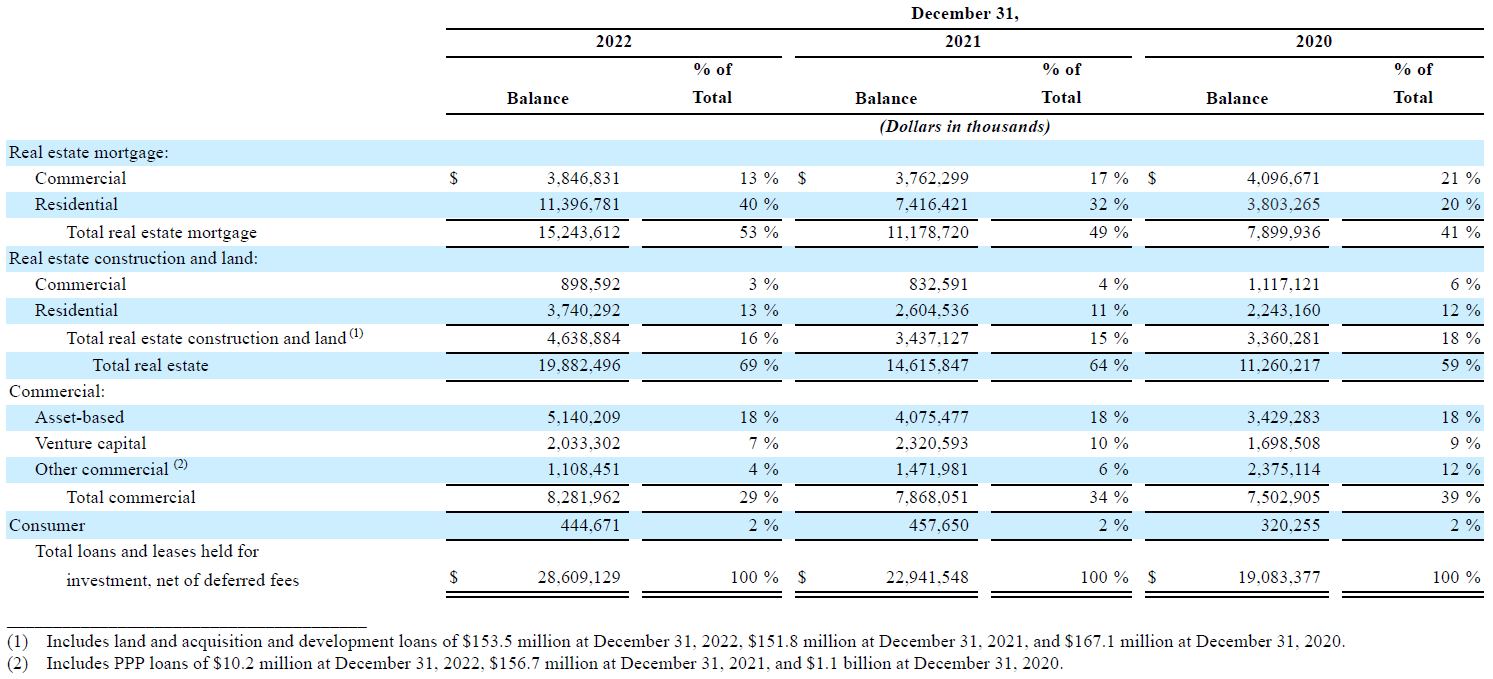

The bank's segmentation of assets is pretty sparse in terms of identifying exposure to the venture capital industry. For example, we see commercial loans to venture capital companies at 7% of the loan book as of Dec 2022. I would suspect further indirect exposure in the form of residential mortgages extended to people working in the venture capital industry and commercial mortgages backed by real estate owned by venture capital companies.

Source: 2022 10-K report (PacWest Bancorp website)

{kind=link}

Solvency Concerns

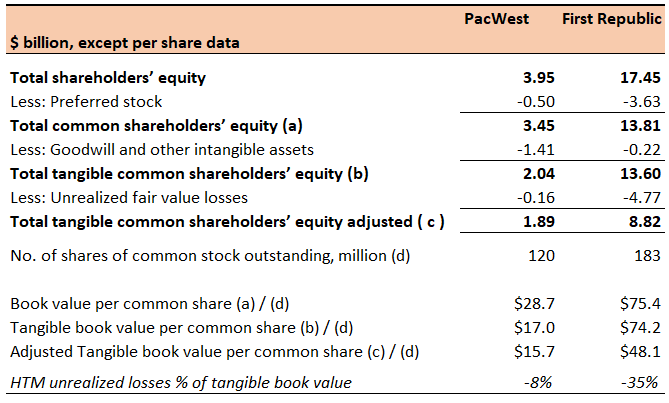

After the insolvency of SVB due to unrealized losses on Held-to-Maturity ("HTM") investments, investors looking for a similar play of events brought PacWest in their sights with an HTM portfolio equal to 5.5% of its total assets and a duration of 8.2 years as of Dec 2022. It also had a larger available-for-sale ("AFS") portfolio equal to 11.7% of its assets with a duration of 5.9 years whose unrealized losses were running through shareholders' equity but not through the bank's regulatory capital. People familiar would know that duration is a rule of thumb for a bond's sensitivity to interest rate changes in the sense that the larger the duration, the larger the decline in bond price for a given increase in interest rates and vice versa.

I think unrealized losses on its HTM portfolio create a smaller dent of 8% on the tangible book value ("TBV") of PacWest vs a 35% dent on the TBV of First Republic (calculations in table below).

Source: Analysis based on 2022 10-K reports (Author)

{kind=link}

In the context of valuation, PacWest is trading at 0.60x and First Republic is at 0.28x Price to Tangible Book Value multiple. I think the larger discount on First Republic is a reflection of investor doubts about its future strategic options.

A far bigger adjustment to tangible book value could potentially come from a haircut on loans in the event of a sale of loans to shore up liquidity or acquisition of the bank by a larger player as part of a rescue plan. Both of these are possible scenarios for First Republic given the larger extent of its liquidity strain and limited strategic options but PacWest seems to be in a better shape with management stating on Mar 22nd that it would not be prudent to move forward with a capital issue transaction at this time. If we are looking for a ball-park haircut adjustment, its pertinent to highlight that First Citizens Bank bought $72billion SVB loans at a $26.5billion discount (or 23% haircut). If the same haircut is applied to First Republic who may be looking to sell some loans or maybe putting itself up for sale, its tangible book value looks pretty shaky. In my opinion, PacWest TBV of $15.7/share looks like a more solid anchor for an investor looking to establish a base line value of its shares.

Better Liquidity Management

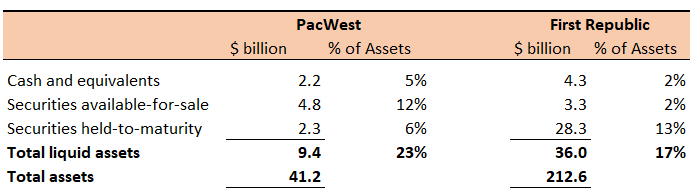

I think that PacWest was in a relatively better liquidity position vis-a-vis First Republic at Dec 2022. This was despite PacWest being a much smaller player. It's not really possible to replicate the usual liquidity metrics used by banks like Liquidity Coverage Ratio ("LCR") from 10-K disclosures, so we will have to look in other places like the amount of liquidity buffers held in the form of cash and high quality liquid securities. PacWest's liquidity buffers at 23% of the balance sheet were significantly larger than First Republic's 17% at Dec 2022.

Source: Analysis based on 2022 10-K reports (Author)

{kind=link}

I think there was no regulatory burden on both of these banks to hold any amount of liquidity reserves, so their level of liquidity was simply an indication of their management best practice.

I would also note that PacWest management stands out for its pro-active handling of the liquidity crisis. It has been providing updates on its liquidity situation and the actions it is pursuing in a more transparent way compared to other banks.

Final Thoughts

All in all, the slide in PacWest stock price seems to be unjustified in my view. The management has been actively updating the market about their liquidity status during this period of uncertainty. The extent of PacWest's exposure to uninsured deposits and unrealized losses on HTM portfolio were significantly lower than one of its larger regional peers. Moreover, the bank likely has better liquidity management practices. A haircut on venture capital-related loans does not seem to be a base case implication of PacWest's path towards return to normalcy. I think investors should look at building a position in this speculative micro-cap.

Take everything you read with substantial skepticism and a healthy grain of salt. Invest based on your own financial profile and your appetite for volatility. Information discussed here should not be considered as an "investment advice" or as a "recommendation."

For further details see:

PacWest Bancorp: The Sell-Off Looks Overdone